The Dollar’s Plumbing: Conspiracy vs. Data

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEvery few months, a headline appears declaring that the U.S. dollar’s reign as the world’s reserve currency is over. China is dumping Treasuries. Central banks are hoarding gold. The BRICS are building a new monetary order. The sanctions that froze $300 billion of Russia’s reserves in 2022 proved, the argument goes, that dollar-denominated assets are no longer safe. The “risk-free” asset has become a weapon.

The data tells a more nuanced, and arguably more important, story. One that investors ignore in favor of the simpler narrative is the risk of getting it badly wrong.

The Numbers Don’t Support “Flight from the Dollar”

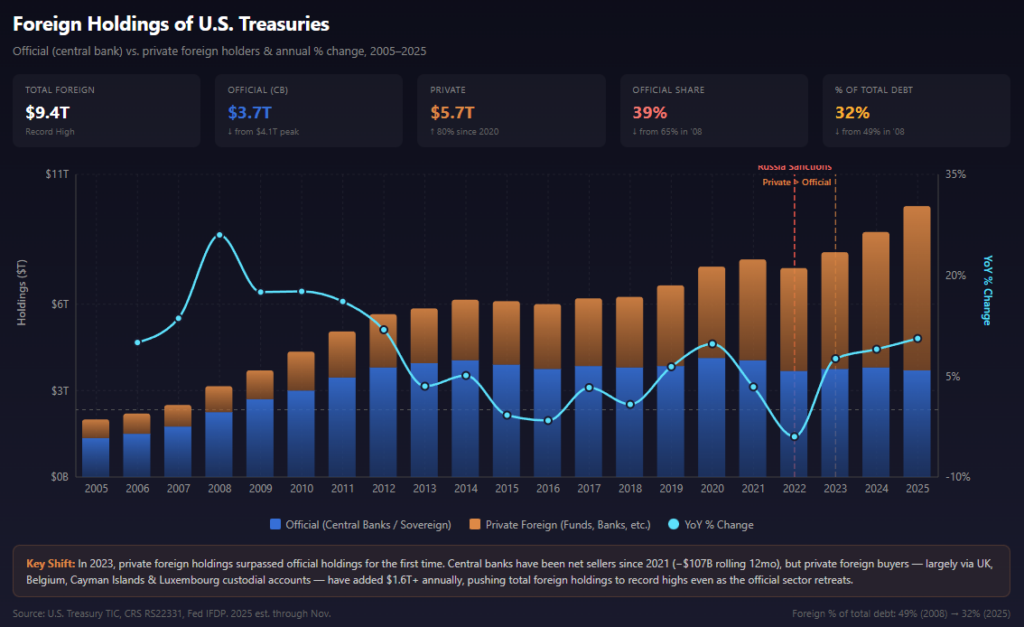

Total foreign holdings of U.S. Treasury securities reached a record $9.4 trillion as of December 2025, according to the U.S. Treasury’s Treasury International Capital (TIC) data, up from $8.7 trillion a year earlier—a gain of more than $700 billion or approximately 8%. Since 2020, when foreign holdings stood at roughly $7.1 trillion, the total has risen by more than $2.3 trillion. Far from fleeing dollar assets, foreign investors in aggregate are buying them at an accelerating pace.

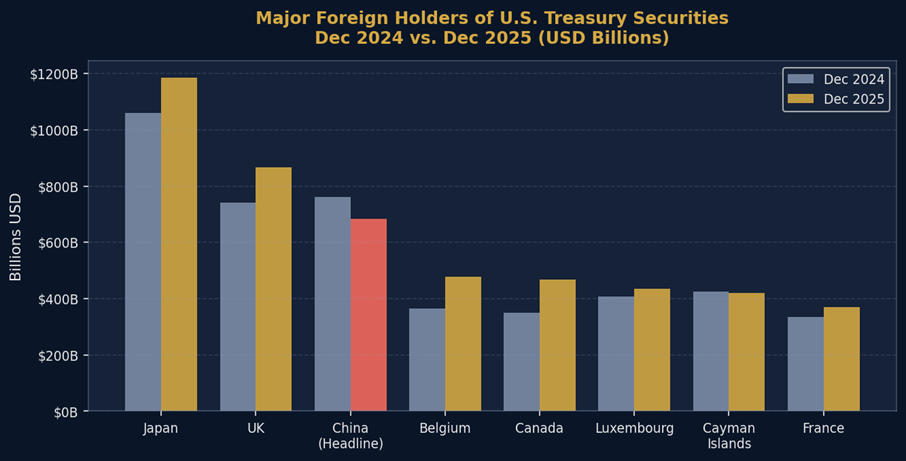

The UK, Belgium, and Japan were the three largest buyers of U.S. debt from November 2024 to November 2025, each adding more than $115 billion. The UK alone increased its holdings by roughly $150 billion over the past 12 months. Belgium, home to Euroclear, the world’s largest international central securities depository, saw a 26% increase in holdings, the largest percentage gain among major holders.

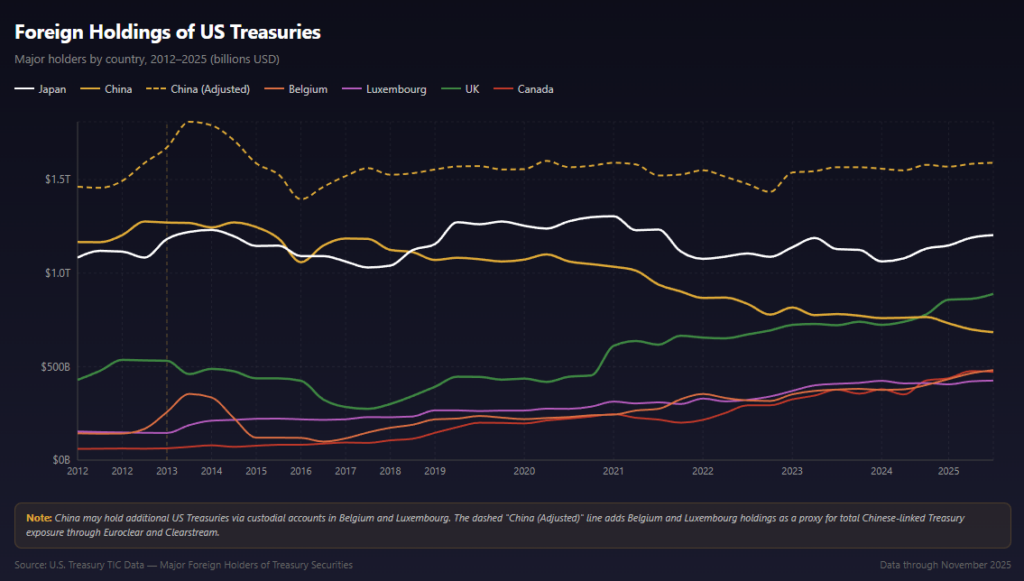

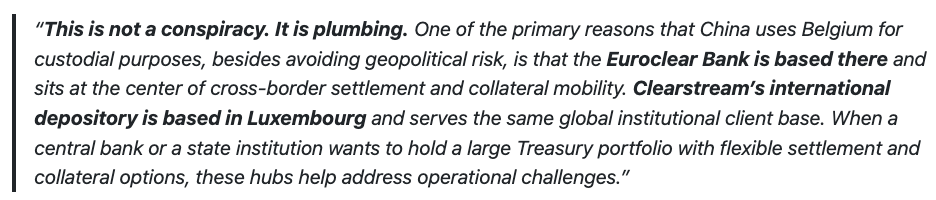

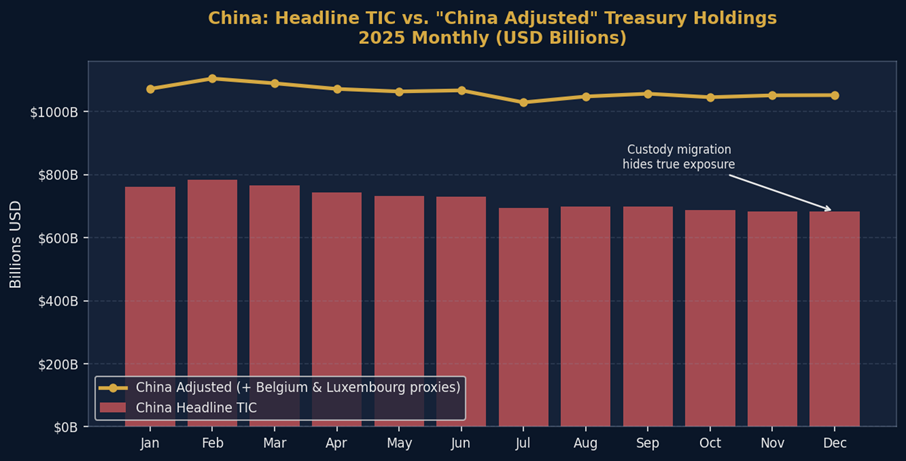

China, meanwhile, reduced its holdings by approximately $86 billion over the same period. But China’s headline TIC number of $683 billion understates its actual exposure, because it measures only securities held in U.S. custody. As discussed in our previous article, a significant and growing share of China’s Treasury positions is custodied through European intermediaries, precisely the Belgian and Luxembourg accounts that have been growing so aggressively.

As noted in that article:

The truly meaningful story is not about the dollar. It’s about who holds the debt and where they custody it.

It is true that Foreign official (central bank) holdings peaked around $4.1 trillion in 2020 and have since declined to approximately $3.7–$3.8 trillion. Notably, official institutions have been net sellers since 2021, with rolling twelve-month outflows of roughly $107 billion. As discussed previously, this is due to risk management by Central Banks to offset sanction risks.

However, private foreign investors, such as banks, asset managers, hedge funds, sovereign wealth funds, and corporate treasuries, have more than compensated for the slight reduction in Central Bank holdings. Private foreign holdings surpassed official holdings for the first time in 2023 and now stand near $5.7 trillion, an 80% increase since 2020.

This is not de-dollarization. It is de-officialization. The dollars are still flowing in. They’re just flowing through different pipes.

The Custody Migration: Sanctions, Regulation, and Plumbing

The most crucial aspect of the entire thesis rests on “risk mitigation.” Central banks and foreign investors are not “de-dollarizing” from the U.S. As noted above, the subtle shift is not whether foreigners hold Treasuries, but where they hold them following the post-2022 sanctions regime. The freeze on Russian central bank reserves held at Euroclear accelerated a shift in custody away from New York-based institutions toward European clearinghouses.

The evidence for this migration is unambiguous. Euroclear’s assets under custody exceeded €43 trillion for the first time in 2025, completing thirteen consecutive quarters of growth. Turnover rose 20% year over year to €1,390 trillion. These are not the metrics of an institution handling a declining business.

However, the claim that this migration is driven purely by sanctions fear overstates one factor and understates several others.

Regulatory cost arbitrage is the bigger driver. The SEC’s December 2023 mandate requiring central clearing of most Treasury cash and repo transactions, with compliance dates of December 2026 and June 2027, respectively, represents what Vanderbilt Law’s Yesha Yadav calls “the most significant change to the structure of the Treasury market” in decades. The rule could bring as much as $4 trillion in daily transaction volume into central clearing through FICC, imposing new margin, capital, and operational costs on participants. As Yadav and Columbia’s Josh Younger note, “parties may relocate their Treasury trades to offshore jurisdictions and into entities that fall outside the scope of the SEC’s mandate and the visibility of U.S. authorities.”

Add to this the cumulative impact of Basel III capital charges on dealer inventories, mandatory derivatives margining under Dodd-Frank, and post-trade transparency requirements, and the economic incentive to custody and trade Treasuries through Euroclear or Clearstream rather than through DTCC becomes substantial, regardless of any geopolitical considerations.

Notably, while the sanctions signal is real, those sanctions are asymmetric, with the 2022 freeze of Russian assets being a paradigm-shifting event. Euroclear now holds approximately €185 billion in frozen Russian central bank assets and has contributed roughly €5 billion to the European Fund for Ukraine from the interest earned on those balances. The message to every non-allied central bank was unambiguous: assets custodied in Western institutions are subject to seizure under extreme circumstances. But the irony is that Euroclear itself was the custodian of Russia’s frozen assets, so “fleeing New York for Brussels” doesn’t actually escape the Western sanctions apparatus. It merely shifts the jurisdictional risk from U.S. to Belgian and EU law.

The Gold Signal Is Real—But Complementary, Not Substitutive

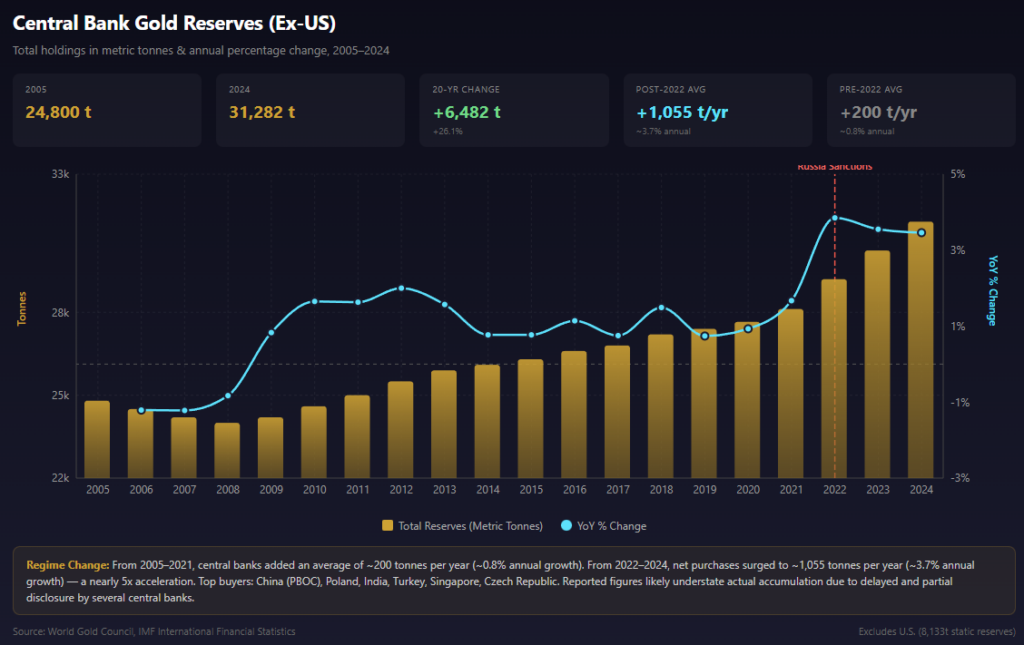

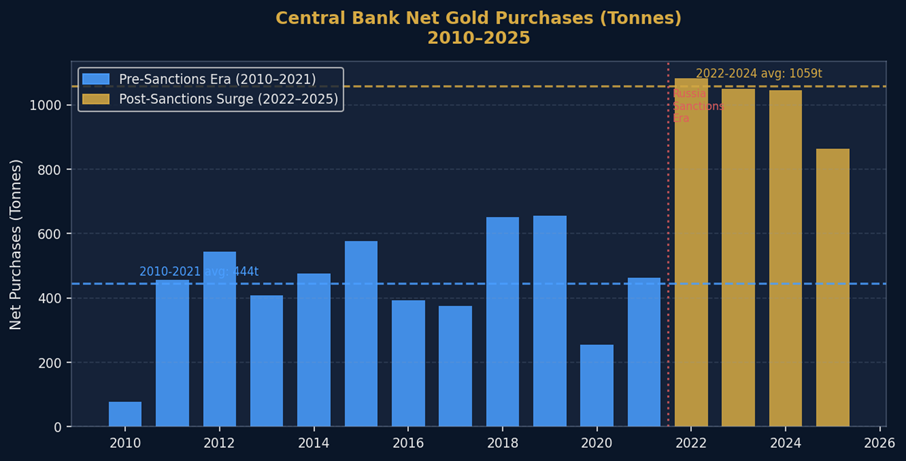

Central bank gold purchases have been extraordinary. In tonnage terms, which strips out price effects and reveals raw physical accumulation, the story is stark. Ex-U.S. central bank gold reserves grew from roughly 24,800 tonnes in 2005 to 31,282 tonnes in 2024, a 26% increase (or 1.3% annualized) over twenty years. But the trajectory was anything but linear. From 2005 through 2021, central banks added an average of roughly 200 tonnes per year, a sleepy 0.8% annual growth rate.

From 2022 through 2024, net purchases surged to approximately 1,055 tonnes per year, a 3.7% annual growth rate. More than half of the total twenty-year accumulation occurred in just three years. However, since 2022, purchase rates have slowed.

The de-dollarization crowd points to this chart as Exhibit A for the dollar’s demise. But there is a fundamental paradox embedded in the data that almost no one discusses.

Gold is traded, priced, and settled in U.S. dollars.

The LBMA, the epicenter of wholesale physical gold trading, publishes its benchmark price twice daily in U.S. dollars per troy ounce. COMEX futures, which dominate price discovery, are quoted in U.S. dollars and cents per troy ounce, with contracts settled in U.S. dollars. When the PBoC, the Reserve Bank of India, or the National Bank of Poland buys gold, the transaction is denominated in dollars, clears through dollar-based infrastructure, and the resulting asset’s value is universally marked to market in dollars. Even the Shanghai Gold Exchange, which quotes in renminbi, effectively tracks the dollar-denominated LBMA price adjusted by the USD/CNY exchange rate.

This creates an uncomfortable logical problem for the de-dollarization thesis. When a central bank sells $10 billion in U.S. Treasuries and uses the proceeds to buy $10 billion worth of gold, it has not reduced its dollar exposure in any meaningful economic sense. It has converted one dollar-denominated asset (a Treasury bond with counterparty risk, yield, and maturity) into another dollar-denominated asset (gold with no counterparty risk, no yield, and no maturity). The gold bar sitting in the vault is the only aspect that is truly “non-dollar,” it has no issuer, no coupon, and no CUSIP. But its acquisition required dollars, its valuation is in dollars, and any future liquidation will produce dollars.

What central banks are actually doing is not de-dollarizing. They are de-risking within the dollar system. This is accomplished by swapping an asset that can be frozen or sanctioned for an asset that cannot. This is an important distinction. Gold accumulation does not weaken the dollar’s role as the global unit of account. Every tonne of gold purchased at prevailing prices represents demand that flows through dollar-clearing infrastructure.

The correct framing is not “gold vs. the dollar.” It is “gold vs. Treasuries,” a rotation within the dollar ecosystem from an asset with counterparty risk to one without.

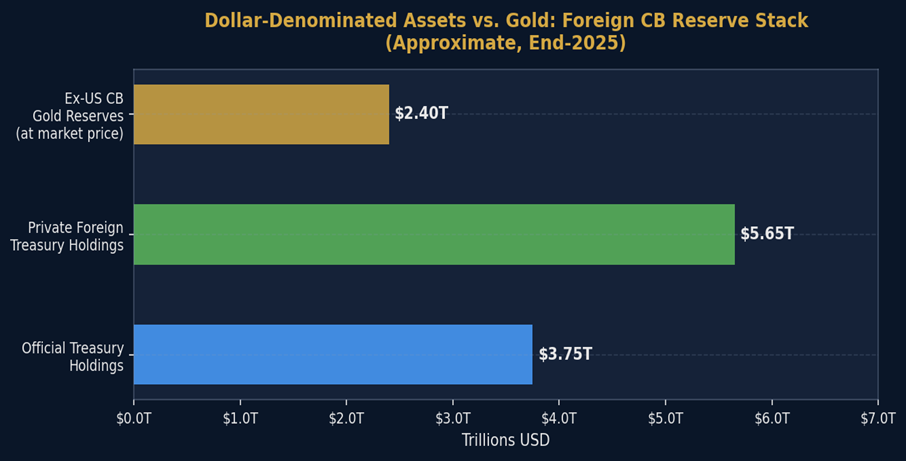

Gold reserves also remain a fraction of the total. At current prices, ex-U.S. central bank gold is worth roughly $2.4 trillion. That is significant, but still below the $3.7–$3.8 trillion in official Treasury holdings alone. It is also a small fraction relative to the $9.4 trillion in total foreign Treasury holdings. No central bank is liquidating its Treasury portfolio wholesale. The PBoC still holds at least $684 billion in reported Treasuries (and likely far more through custodial intermediaries) versus roughly $200 billion in gold reserves. Even the most aggressive gold accumulator in history is running a strategy of marginal diversification, not wholesale substitution.

The reality is that gold is being added at the margin as a hedge against dollar weaponization. However, no central bank is liquidating its Treasury portfolio wholesale to buy gold. The two are complements in a diversification strategy, not substitutes in a currency war.

What’s Actually Happening: The Five-Layer Shift

- Custody migration, not asset flight. Treasuries are moving from New York custody to European clearinghouses. That is being driven by hedging against regulatory and sanctions risks. But the assets remain U.S. dollar-denominated obligations of the U.S. government. The dollar’s role as the unit of account is undiminished.

- Official-to-private rotation. Central banks are reducing holdings while private foreign investors are increasing them dramatically. The marginal buyer of U.S. debt is no longer the PBoC or Bank of Japan. It is now hedge funds, asset managers, and foreign banks seeking yield and collateral.

- Share erosion despite nominal growth. Foreign holdings as a share of total outstanding debt have declined from roughly 49% in 2008 to 32% in 2024. However, the nominal total reached records. With the U.S. issuing debt faster than foreign purchases, domestic absorption (the Fed, banks, and money market funds) must fill the gap.

- Gold as insurance, not replacement.Central banks are adding gold at the fastest pace in decades as a hedge against geopolitical risks (i.e., sanctions). This is rational portfolio diversification, not a bet on the dollar’s collapse.

- Regulatory fragmentation. U.S. market structure choices—mandatory clearing, capital charges, transparency requirements—are pushing Treasury market activity offshore. This is self-inflicted, not externally imposed. It represents a potentially larger long-term risk to U.S. financial primacy than Chinese gold purchases.

The Bottom Line

The de-dollarization narrative is mostly wrong on the facts, but captures something real in the sentiment. The dollar is not dying. Foreign demand for Treasuries is at record highs. But the architecture through which the world interacts with dollar assets is quietly being rebuilt. This is not by adversaries seeking to destroy the system, but by participants seeking to insulate themselves from its political risks and regulatory costs.

The world is not abandoning the dollar. It is hedging against the people who control it. That distinction matters enormously for how investors should position portfolios. It is also a warning for how policymakers should think about the long-term consequences of weaponizing the world’s reserve currency.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All