The conflict in Iran has brought rapid consequences for the global outlook. All nations will be challenged by a curtailed supply of commodities and the higher prices that ensue. The impacts will be greatest for nations that are more reliant on imports of energy and other critical materials. War-related inflation will complicate decisions for central banks; rate reductions are off the table. Some will contemplate rate hikes, though they are an imperfect solution to inflation caused by supply shocks.

This outlook assumes the Iran situation carries on at its current intensity, without substantial escalation, before the involved parties move toward a ceasefire. The longer that hostilities continue and the Strait of Hormuz remains impassable, the greater the downside risks. Even if a ceasefire takes shape and trade flows resume, a complete return to prior levels of activity will take months, and potentially years in the case of destroyed energy infrastructure. We have adjusted our growth expectations accordingly.

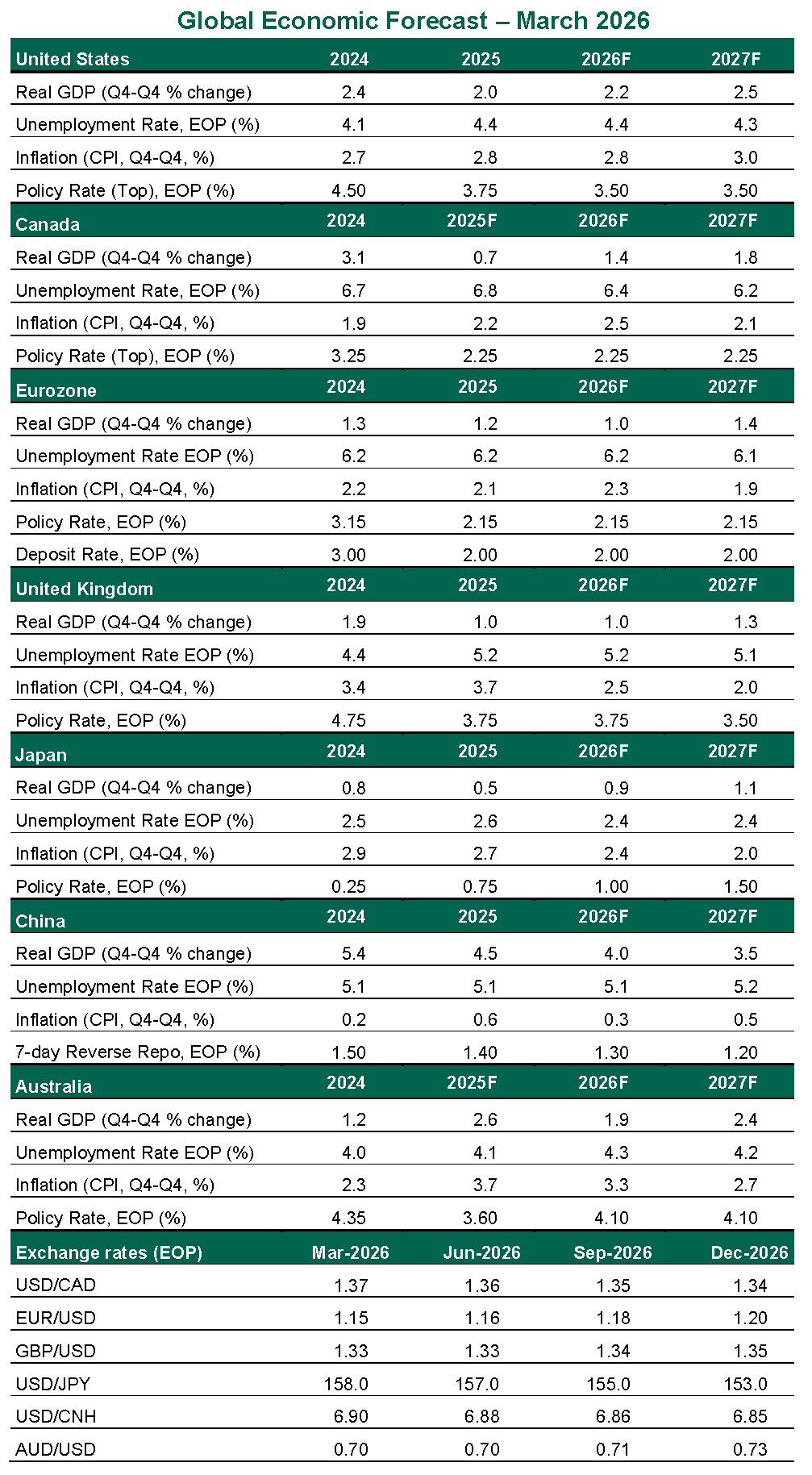

Despite the fog of war, developed markets have demonstrated their ability to grow in the face of uncertainty. Consumption carries on; most countries’ labor markets are firm; trade tensions have lost some urgency; past rate reductions are now stimulating with a lag. For now, our outlook for major markets remains one of modest growth.

United States

- The U.S. is relatively insulated from the consequences of the conflict, with ample domestic supplies of energy and fertilizer. However, commodity prices are set globally, and higher costs are already evident. Energy expenditures will offset some of the near-term gains from a more favorable year of income tax returns. Inflation had already been stuck above target, with services prices showing modest acceleration. The February employment report revealed a surprising decline of 92,000 payrolls and a rise in the unemployment rate; the labor market is sluggish at best.

- Expectations of a Federal Reserve rate cut hung on a stable inflation outlook, which is now in jeopardy. We now expect no further rate cuts until late in 2026, with risk of a further deferral or even a hike should inflation prove persistent.

Canada

- While no nation is better off from global circumstances, Canada is well-positioned to weather the energy market surge. The nation’s fuel supply is secure, and as an energy exporter, it stands to gain from higher prices. Prior to this uncertainty, the Canadian economy had been slowing; the February unemployment rate rose two tenths to 6.7%, undoing the progress shown in January. Overall growth showed declines in the second and fourth quarters of 2025, though gains in the first and third quarters delivered an adequate real gain of 1.7% for the full year. Economic slack should help to buffer inflationary shocks from energy prices.

- The Bank of Canada held rates steady at its March meeting, and we expect no further policy changes. Inflation worries will be offset by limited growth and signs of a deteriorating labor market. Policy uncertainty looms with the U.S.-Mexico-Canada Agreement due for renegotiation this summer. U.S. leadership has a preference for bilateral engagement, which may leave Canada exposed to sudden changes in its terms of trade.