Key takeaways

- Markets remain focused on inflation risk, not growth – leaving duration increasingly attractive if that balance shifts.

- High-quality credit has absorbed recent shocks, but valuations are becoming locally stretched versus securitized assets and derivatives.

- Dispersion, rather than broad market performance, is driving returns – rewarding selective exposure across regions and sectors.

Until the middle of last week, markets had exhibited a noticeable gap between the behavior of global rates and risk assets. Across foreign exchange (FX), equities, and especially credit, risk premia had moved only modestly, even as front‑end yields rose sharply and curves flattened – suggesting a market still more focused on inflation risks than on a material growth shock.

That stance was partly shaped by last year’s “Liberation Day” tariff volatility episode, which conditioned investors to look through policy noise and avoid leaning too aggressively into downside scenarios, despite a more complex geopolitical backdrop today. Price action over the past two trading sessions suggests this gap may now be narrowing as markets may be starting to shift their focus toward downside risks to growth.

While the ultimate path of the Middle East conflict remains highly uncertain, a more prolonged return to pre‑conflict conditions would likely prompt a broader and sharper repricing of growth risk. That asymmetry continues to make owning duration (a gauge of interest rate risk that tends to be higher in longer-dated bonds) increasingly compelling, particularly given key differences between today’s conditions and the 2022 inflation episode, including a more balanced labor market, higher borrowing costs, and weaker aggregate demand (for more, see our latest Cyclical Outlook, “Layered Uncertainty: Conflict, Credit Stress, and AI”).

The dollar, bonds, and risk: A tougher hedge, but only locally

While Treasuries provided effective protection during risk-off episodes in February, their performance has since been more mixed, as yields have moved higher even amid bouts of softer risk sentiment. This has reignited the debate around the value proposition of duration and the U.S. dollar as hedges in an inflation‑dominated regime.

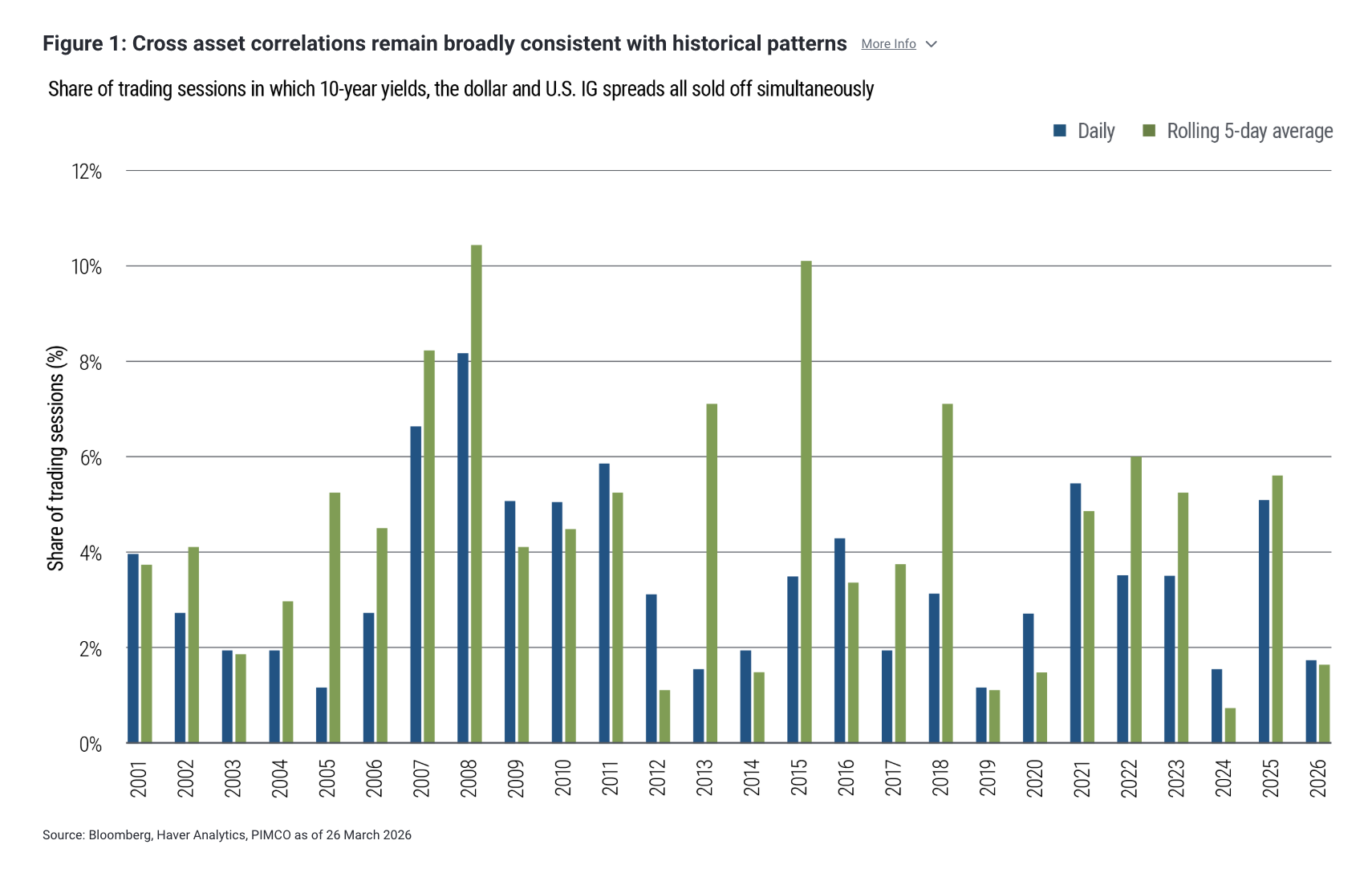

So far, cross‑asset correlations remain broadly consistent with historical patterns. Of the roughly 60 trading sessions year‑to‑date, there have been very few instances – on either a daily or rolling basis – where higher 10‑year Treasury yields coincided with wider U.S. dollar investment grade (USD IG) spreads and a weaker dollar (see Figure 1). The frequency of such episodes in 2026 remains below its long‑run median. To find a more persistent clustering of this dynamic, one must look back to the immediate aftermath of “Liberation Day” in April 2025. Since then, evidence of its persistence has been muted.

USD IG holds firm, but relative value looks locally stretched

As of 27 March, USD IG spreads are only 5 basis points (bps) wider relative to their level prior to the start of the Iran conflict. A few factors likely explain this resilience:

- First, USD IG spreads entered this episode with some embedded risk premium, largely reflecting earlier technical pressure from heavy supply in the first two months of the year and providing some cushion.

- Second, the back-up in yields has made high-quality credit incrementally more attractive, helping to stimulate demand.

- Third, primary market activity has moderated, easing the technical overhang.

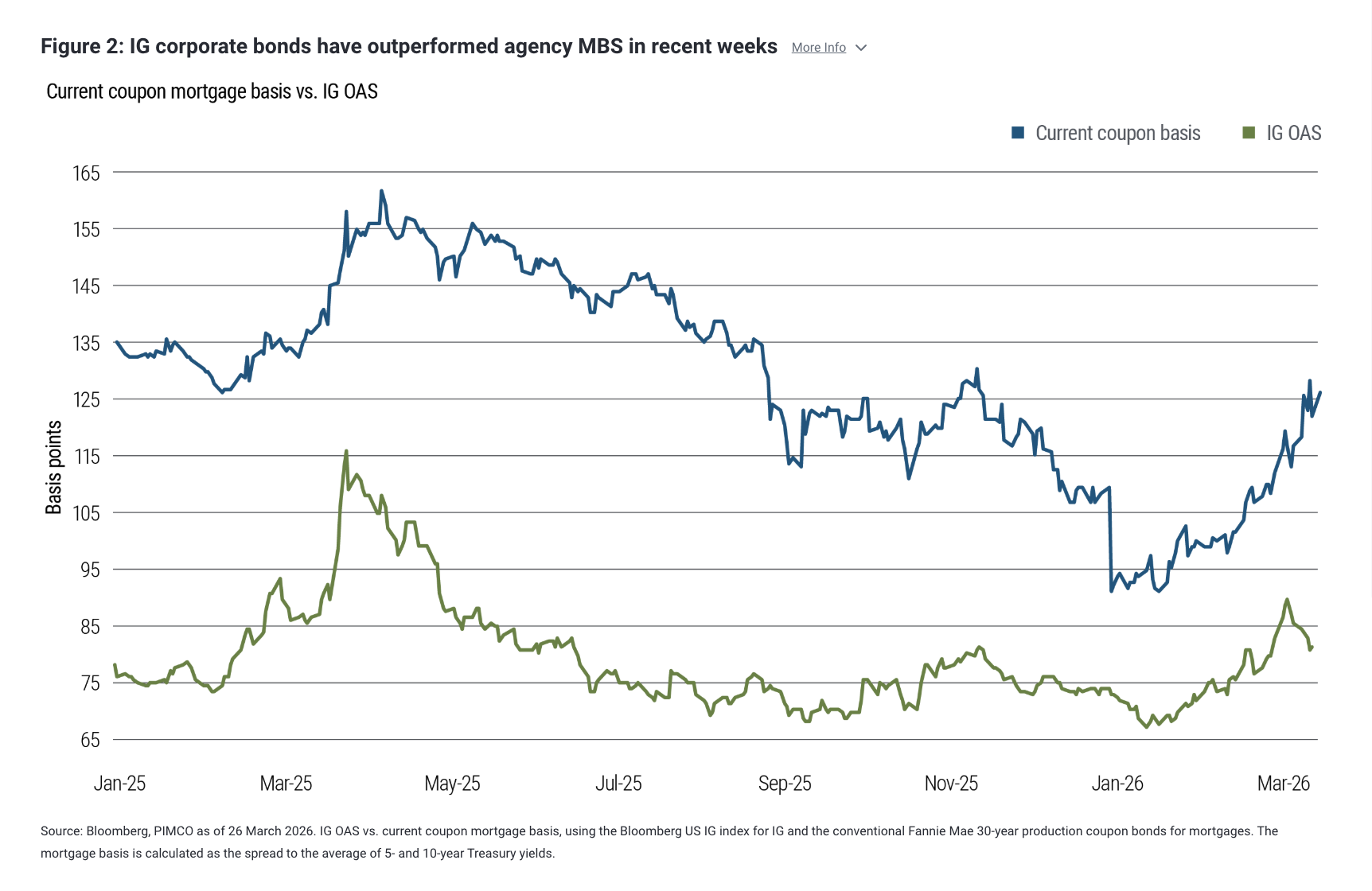

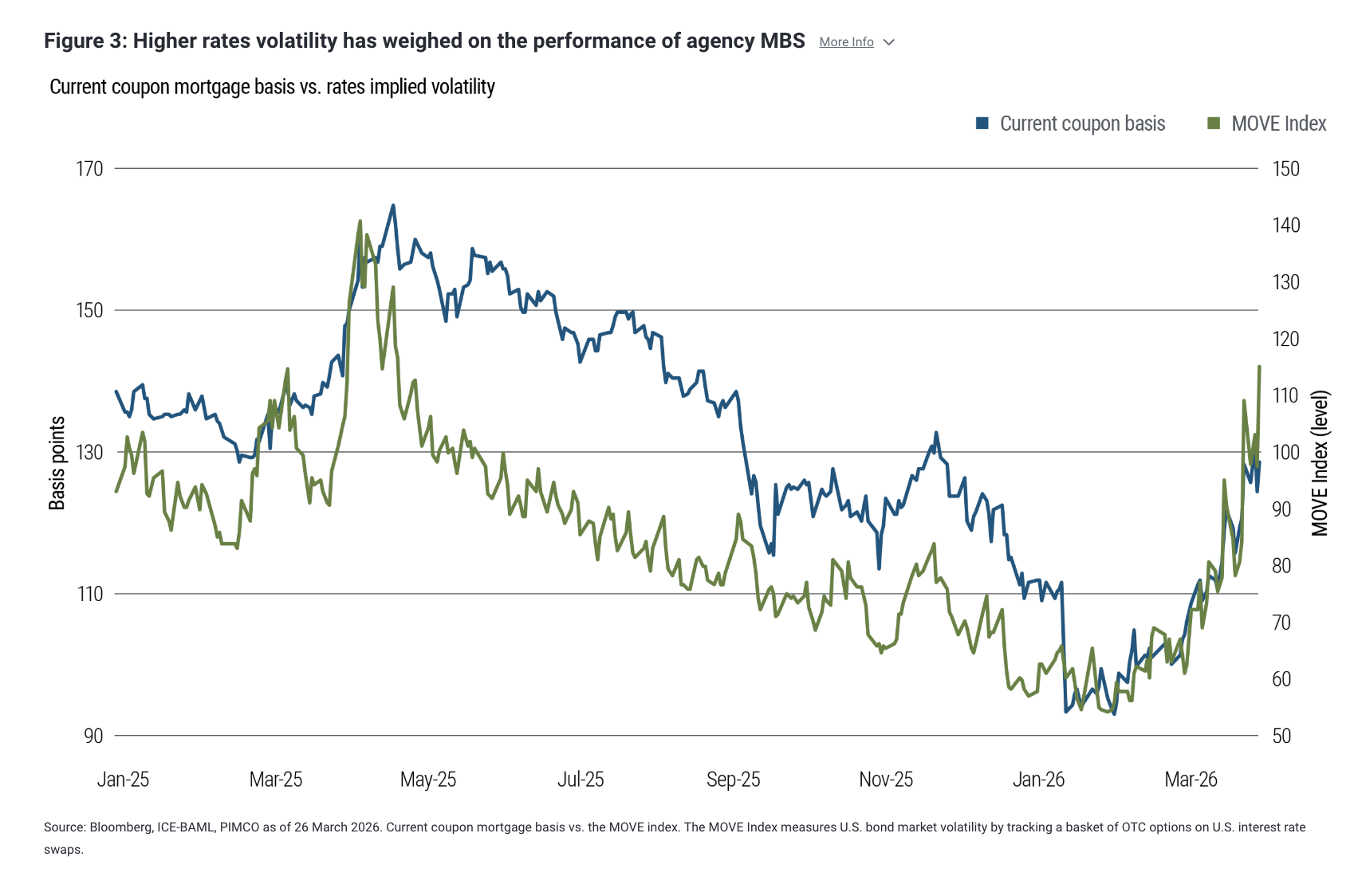

Whatever the precise mix of drivers, the outcome is clear: IG cash bonds now screen locally rich relative to the CDX IG credit-default swap index and, somewhat surprisingly, relative to agency mortgage-backed securities (MBS), where spreads have continued to widen as rates volatility has picked up (see Figures 2 and 3).

Credit breaks the equity link

Aside from the strong showing in USD IG, three broader themes have also emerged in recent weeks.

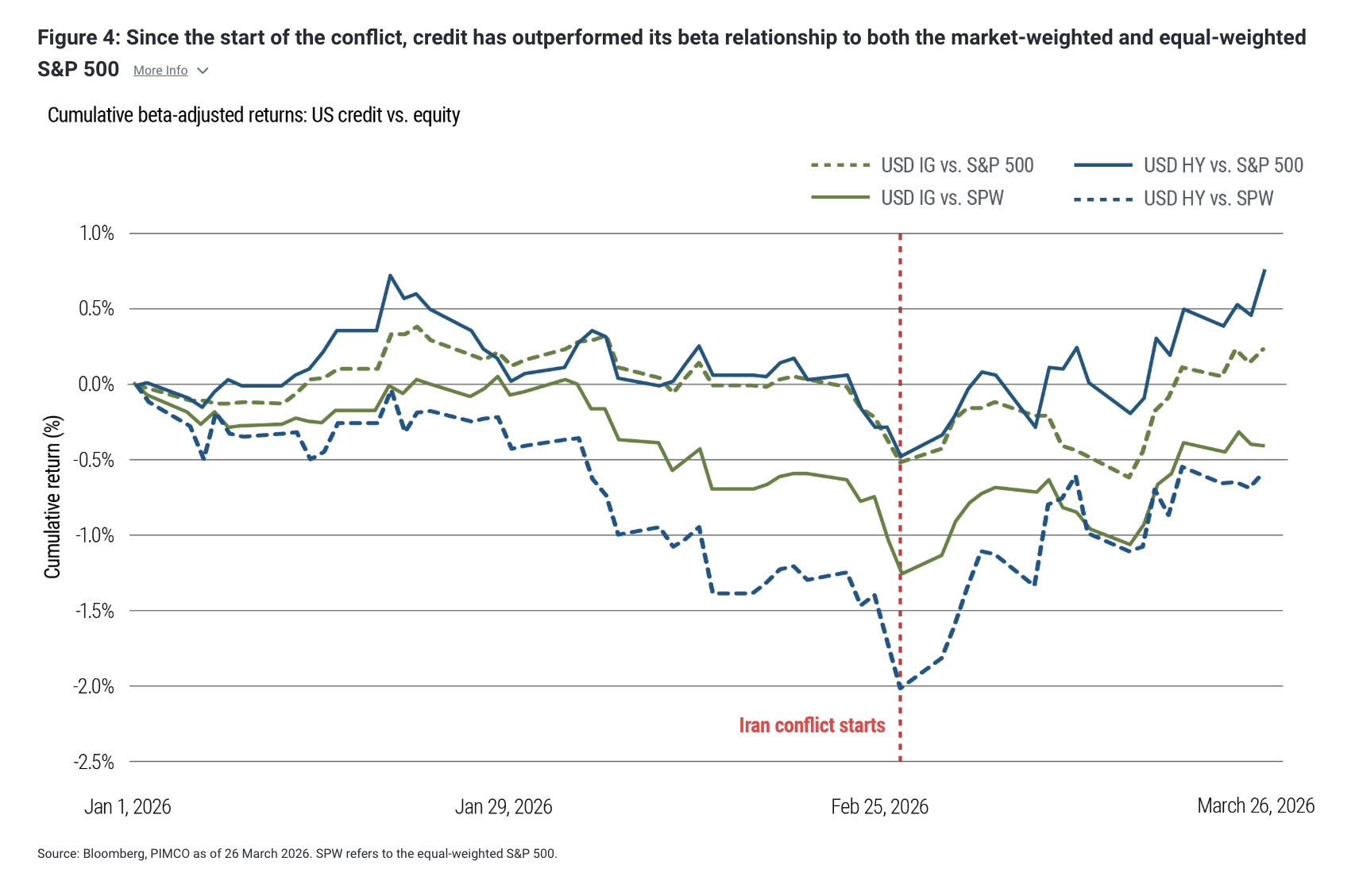

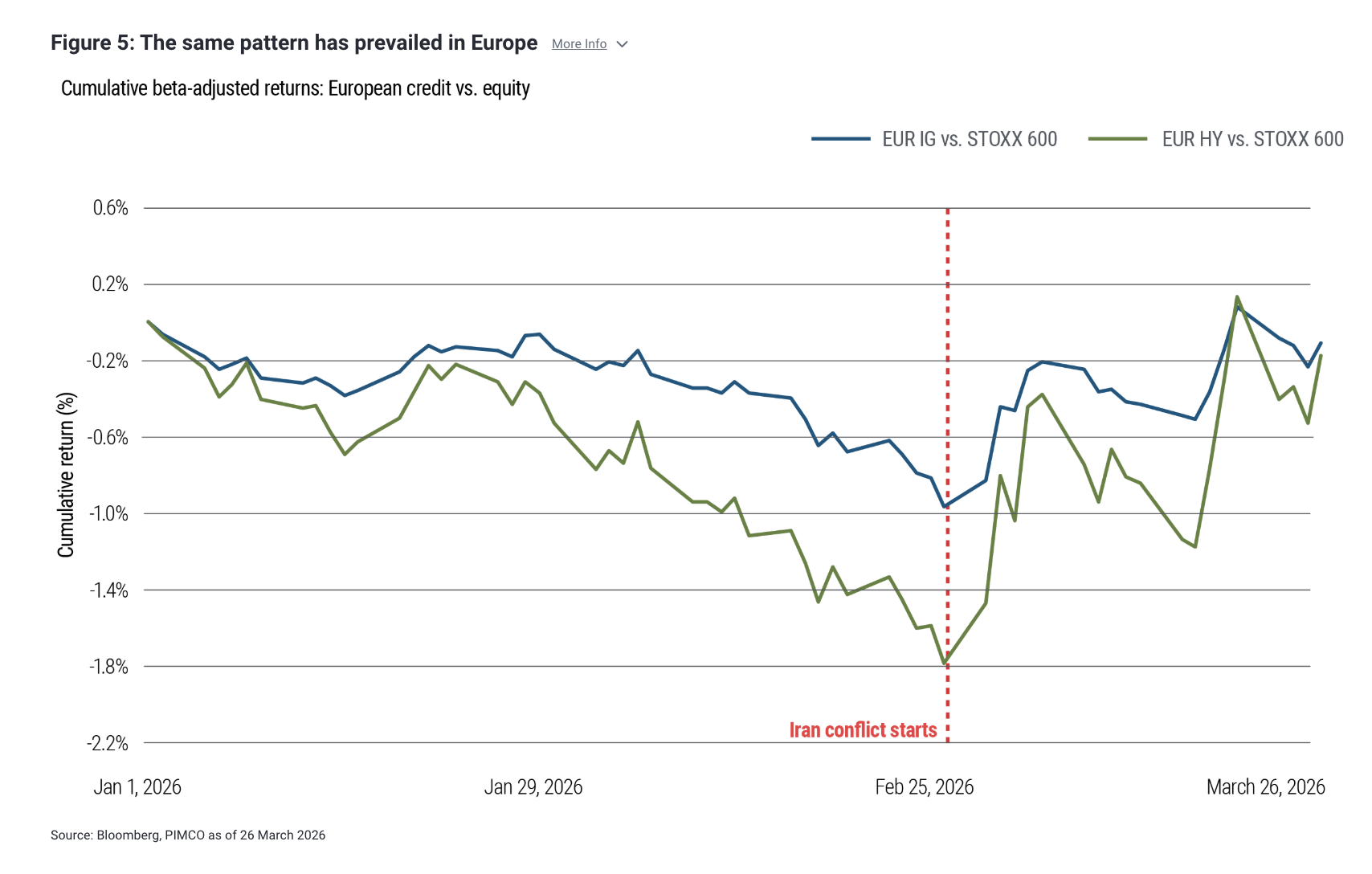

First, in both the U.S. and Europe, credit has outperformed its beta relationship – or typical degree of sensitivity – to equities since the start of the Iran conflict (see Figures 4 and 5). We would note that the strong concentration of the S&P 500 does not fully explain the outperformance of U.S. credit since the start of the conflict. Even when taking the equal-weighted S&P 500 (SPW) as a benchmark, the outperformance still holds true, as seen in Figure 4.

Second, U.S. credit spreads have outperformed their European peers, consistent with a macro backdrop in which the growth, inflation, and policy mix has deteriorated more meaningfully in Europe. Third, in Europe, corporate IG credit has outperformed sovereign credit, as evidenced by the more modest widening vs. BTP (10-year Italian vs. German) and OAT (10-year French vs. German) spreads, pointing to a market that is more focused on fiscal risks than corporate credit quality. Absent a reversal in oil prices, it is difficult to see this relative value dynamic reversing.

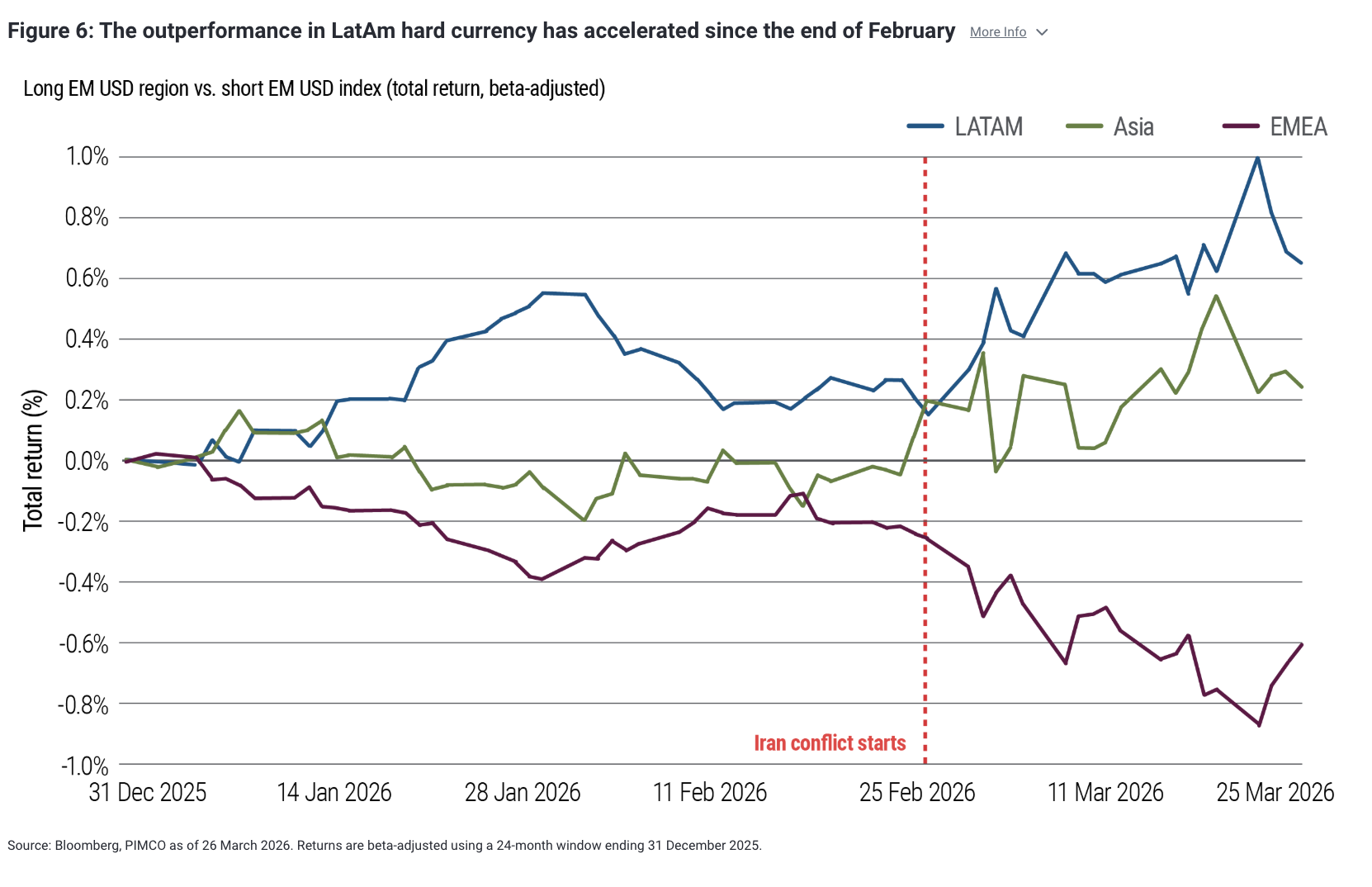

Emerging market (EM) credit: Latin America shines

While the Bloomberg EM USD hard currency index has delivered negative total returns year-to-date, under the surface there has been a high degree of dispersion across regions in the wake of the Iranian conflict, with Latin America materially outperforming (see Figure 6). This outperformance has been underpinned by three key ingredients: starting valuations, commodity exposure, and the region’s beta to the U.S.

First, on valuations, relative to the other regions, LatAm spreads screened as the most attractive at the start of the year, offering almost 80 bps of pick-up vs. the index. And despite this year’s outperformance, the region still offers 60 bps of excess spread vs. the index. Second, around half of LatAm country exposure is concentrated in Mexico, Brazil, and Argentina. Thus, higher oil and agricultural commodity prices have been a tailwind to the region, while LatAm is also less reliant than Asia on oil from the Middle East. Lastly, the region has historically had a high beta to U.S. growth and, despite economic headwinds of its own, the U.S. is still likely to outperform the rest of its advanced economy peers.

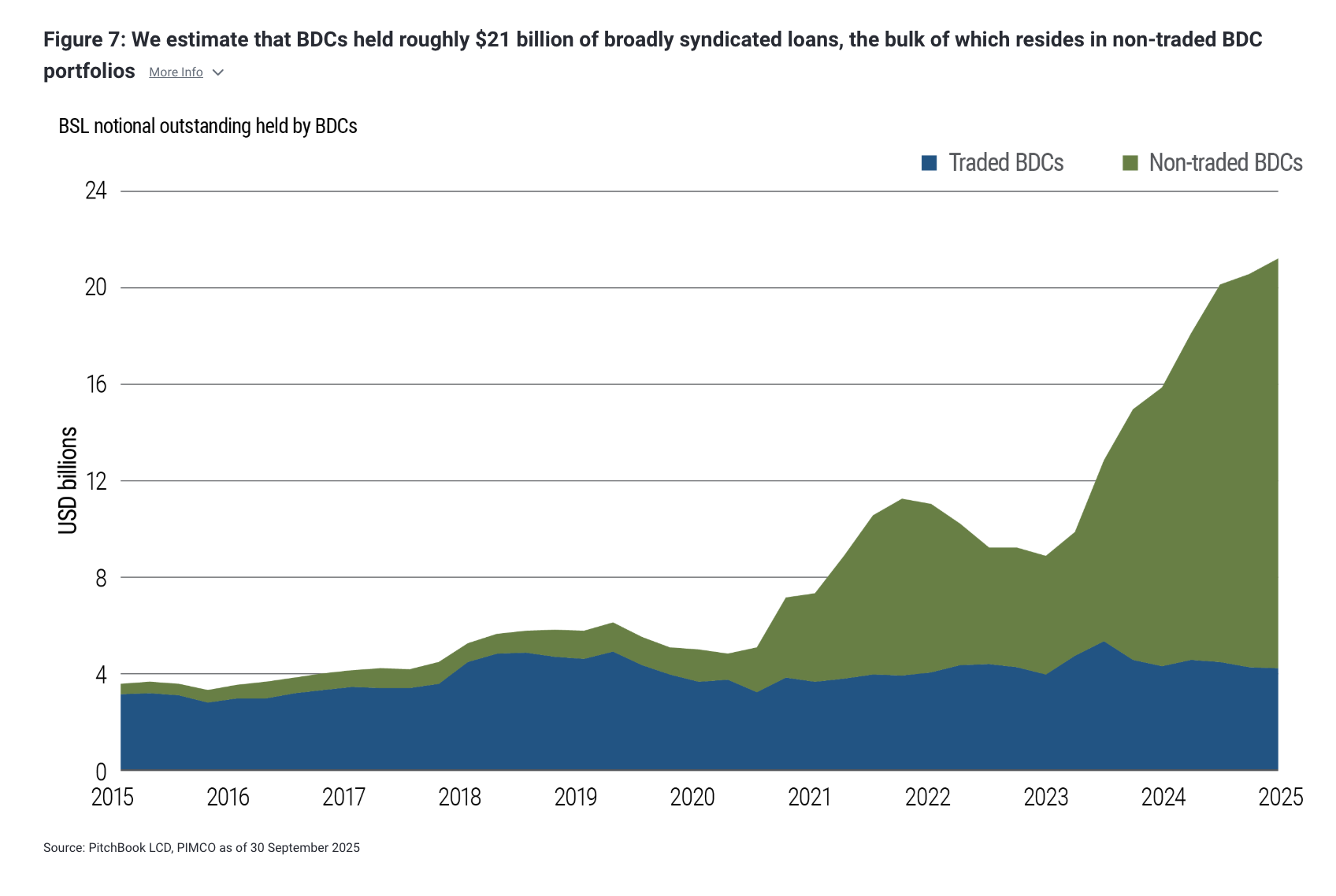

Sizing the spillover: BDC BSL exposure in context

Two more non‑listed business development companies (BDCs) – investment vehicles for corporate direct lending – have joined the list of vehicles effectively capping investor redemptions. A frequently asked question is whether these redemption pressures could spill over into adjacent public markets if managers are forced to raise liquidity by selling more-liquid assets, such as broadly syndicated loans (BSLs).

The holdings of public and non‑traded BDCs provide useful context. As of the end of the third quarter of last year, we estimate that BDCs held roughly $21 billion worth of BSLs, the bulk of which resides in non‑traded BDC portfolios (see Figure 7). This represents about 1.4% of the total amount of BSLs outstanding and a little under 6% of total BDC net asset value (NAV).

Even under stress, this exposure is too small to generate meaningful forced selling in the BSL market. To be clear, redemption pressure is real – and increasingly widespread across non‑traded BDCs – but the risk of a direct flow‑driven spillover into the BSL market remains modest.

That said, the loan market faces its own fundamental challenges – most notably its sizable exposure to the software sector – which have weighed on performance independent of any private‑credit‑related flows.

B3E: Marginally supportive for high-quality securitized products; mixed implications for bank bond supply

The Office of the Comptroller of the Currency (OCC), the U.S. Federal Reserve, and the Federal Deposit Insurance Corporation (FDIC) have released their revised capital proposal, broadly in line with expectations, replacing the more punitive Basel III “endgame” (B3E) with a simpler, more risk-sensitive, framework. While the changes fall well short of a return to pre‑global financial crisis (GFC) norms, they deliver modest, but tangible, capital relief through lower and more granular risk weights.

For mortgages in particular, a more generous loan‑to‑value definition further reduces capital intensity. Taken together, the adjustments should free up balance‑sheet capacity, allowing banks to retain more high‑quality assets – especially residential mortgages and senior securitized products.

On the margin, this is supportive for high‑quality securitized markets, as it could unlock incremental demand while lowering borrowing costs. By contrast, corporate leveraged lending is unlikely to see a meaningful return to bank balance sheets.

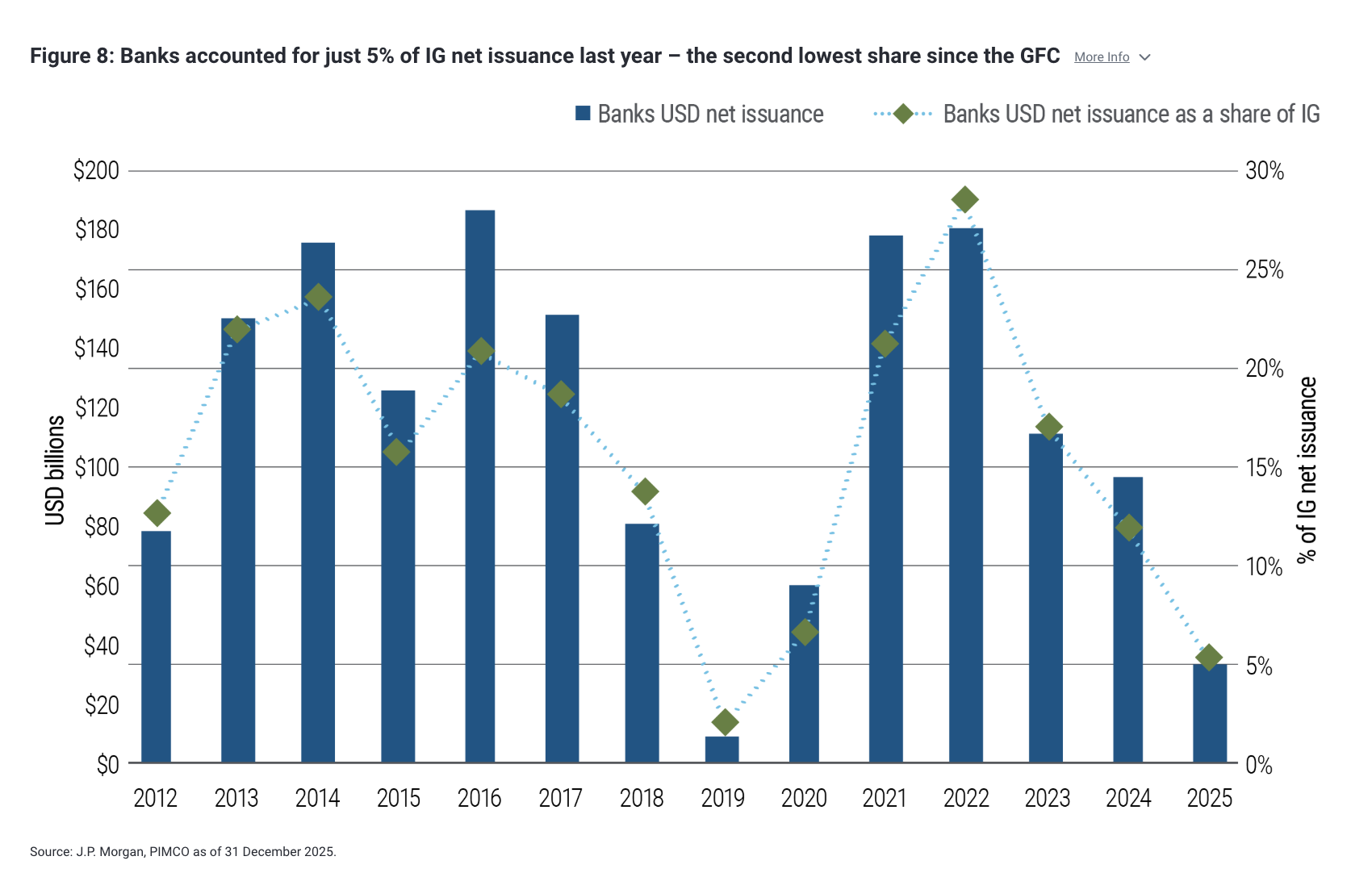

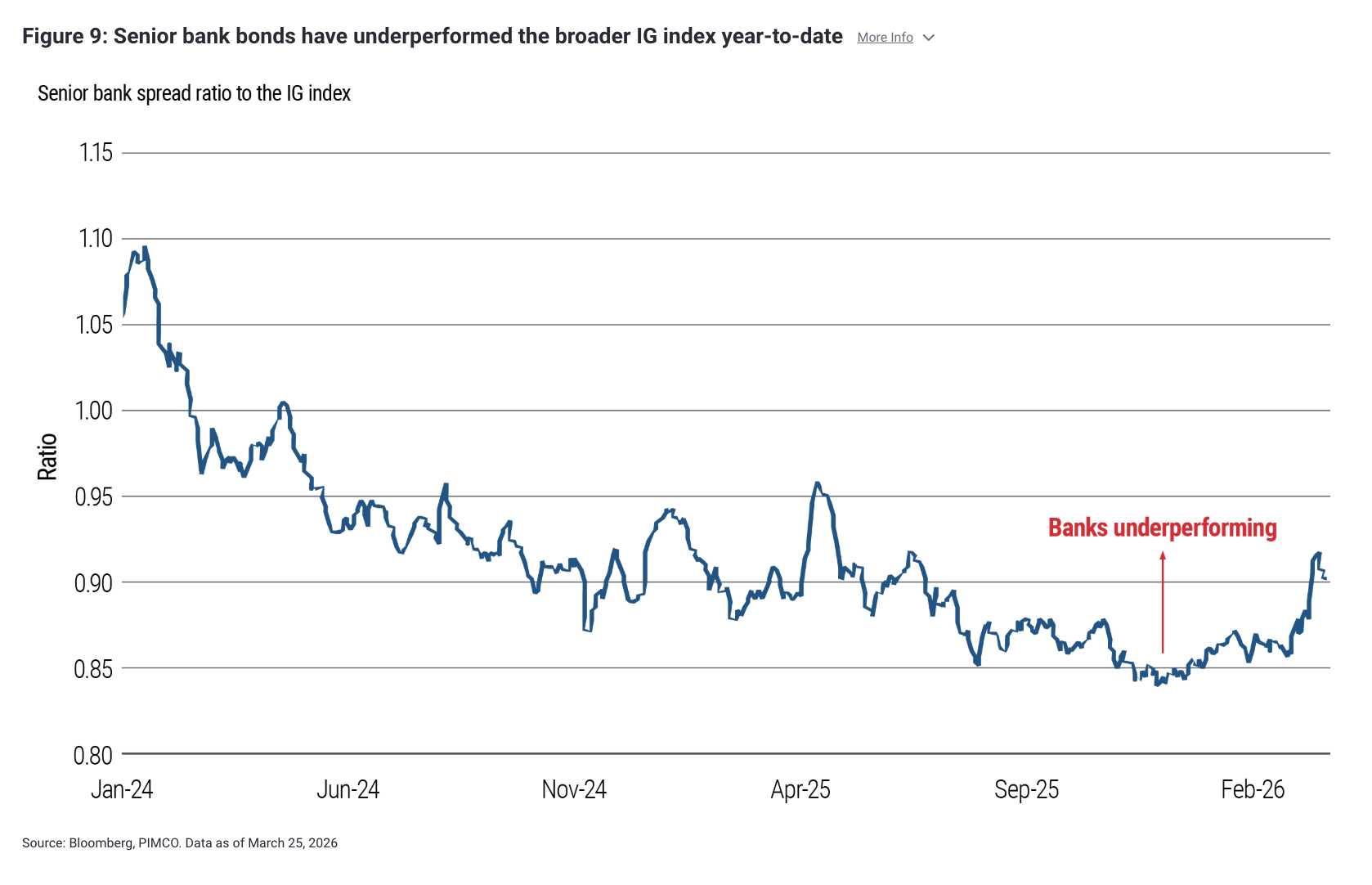

The implications for bank bond issuance are more nuanced: Although regulatory relief could, in principle, support balance‑sheet expansion and higher supply, recent dynamics suggest this effect may be limited. For context, banks accounted for just 5% of IG net issuance last year – the second lowest share since the GFC – while senior bank bonds have modestly underperformed the broader IG index year-to-date (Figures 8 and 9).

Bank–private markets linkages: An interesting transatlantic contrast

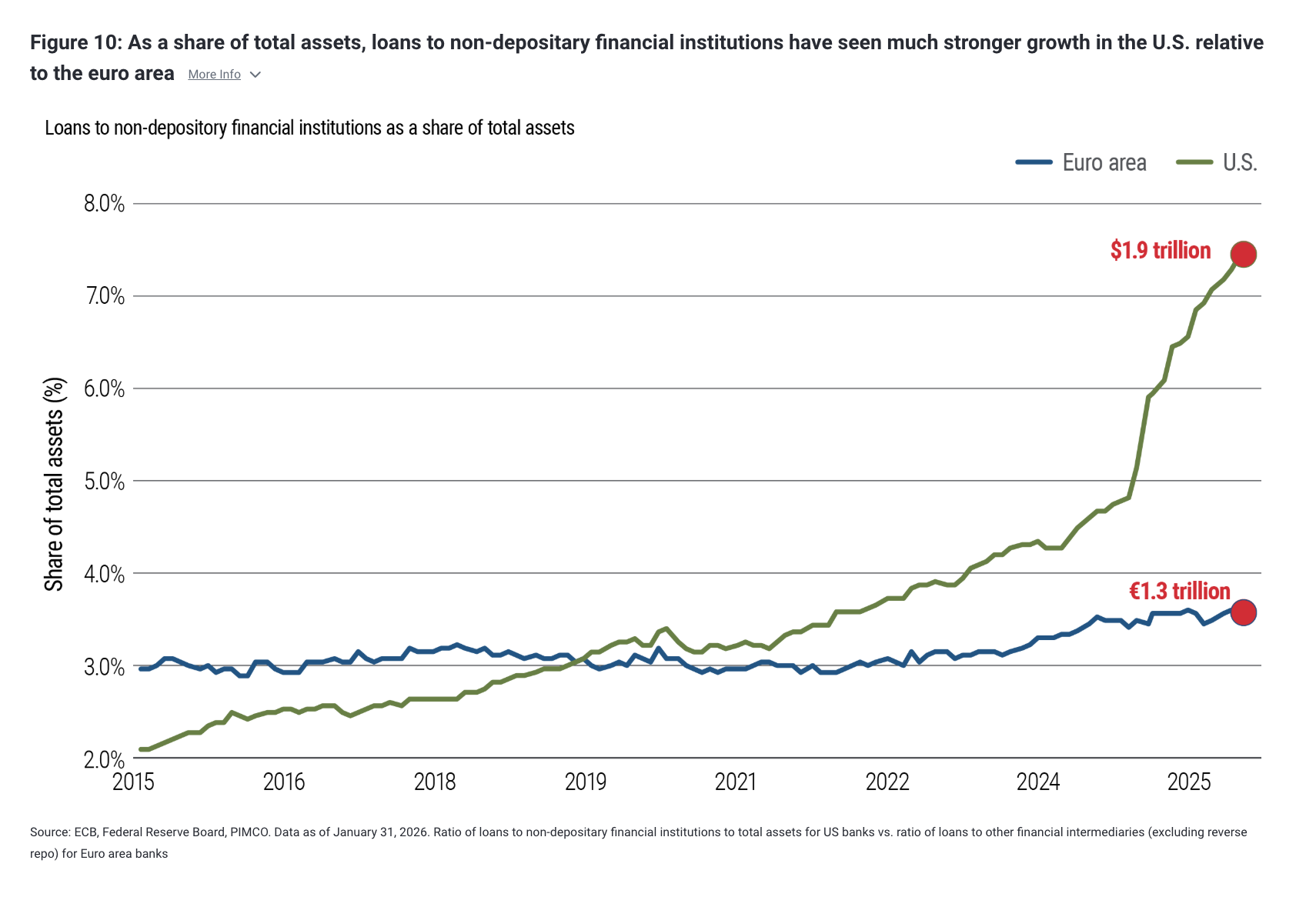

Recent headlines suggest the ECB is taking a closer look at European banks’ exposure to private credit. Similar questions have long been debated in the U.S., but the degree of bank interconnectedness with the sector appears to differ meaningfully across regions.

Direct, granular data are readily available in the U.S. but are more limited in Europe. As a result, the comparison necessarily relies on two different datasets that are not fully internally consistent. In the euro area, European Central Bank (ECB) data on loans to other financial intermediaries (including investment funds) serve as a crude proxy for fund‑finance activity, while U.S. figures are based on more granular classifications.

With that caveat in mind, the contrast is still instructive. As shown in Figure 10, loans to non‑depository financial institutions as a share of total bank assets in the U.S. have nearly doubled over the past decade, reaching roughly 8%. By contrast, the corresponding ratio in the euro area remained broadly stable at around 3.5%.

This divergence reflects both the faster growth of private credit and private markets more generally in the U.S., as well as the more central role European banks continue to play in direct lending to non‑financial corporations. Put differently, while banks have become an increasingly important source of liquidity and leverage to private credit managers in the U.S., that linkage has remained more muted in Europe.

Michael Puempel and Gabriel Cazaubieilh contributed to this report.

Disclosures

All Investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. Mortgage and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee there is no assurance that private guarantors will meet their obligations. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Investing in banks and related entities is a highly complex field subject to extensive regulation, and investments in such entities or other operating companies may give rise to control person liability and other risks.

It is not possible to invest directly in an unmanaged index.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0327-5345607

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO