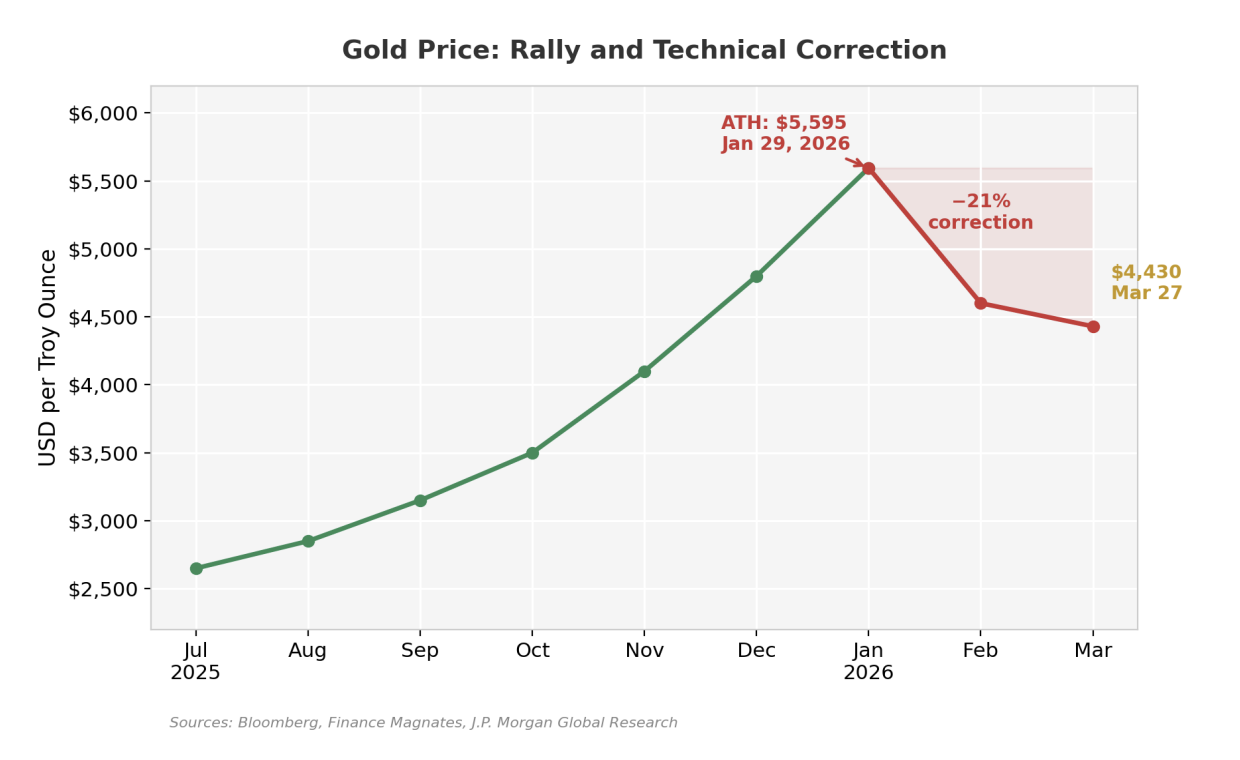

Gold has fallen roughly 21 percent from its all-time high of nearly $5,595 reached in late January to approximately $4,430 as of this writing, and the prevailing narrative in markets is that this correction reflects a genuine shift in the metal’s outlook. We disagree. In our view, the decline is overwhelmingly technical in nature—driven by forced selling from sovereign balance sheets, a wave of institutional and retail profittaking, and the temporary disruption of a key physical demand channel in the Middle East. The fundamental case for gold has not only remained intact through this correction; it has strengthened considerably as the fiscal trajectory of the United States deteriorates further under the weight of a new military conflict and a political cycle that demands ever more accommodation.

The most visible source of selling pressure has come from Turkey, where the central bank is actively preparing to tap its $135 billion in gold reserves to defend the lira. According to Bloomberg, Ankara has been in discussions about conducting gold-forforeign-currency swap transactions on the London market, a mechanism that would allow it to temporarily exchange physical gold for dollars or euros without permanently depleting its reserves. The urgency is real: since the beginning of March, Turkey has burned through approximately $33.7 billion in foreign exchange reserves defending its currency, and inflation remains elevated at 31.5 percent as of February. Turkey imports nearly all of its energy, and the surge in crude oil prices triggered by the Strait of Hormuz crisis has placed extraordinary pressure on its current account. When a nation with one of the world’s largest official gold holdings begins monetizing those reserves to fight a currency crisis, the selling is not a reflection of gold’s diminished value—it is a confirmation of exactly why central banks accumulated gold in the first place.1

Compounding the sovereign selling, the broader investor base has been unwinding positions at a rapid clip. JPMorgan reported that gold ETFs experienced nearly $11 billion in outflows during the first three weeks of March, marking a sharp reversal from nine consecutive months of inflows that had characterized the rally through early 2026. CME futures data shows a steep decline in open interest since January, indicating that both institutional and retail participants have been aggressively cutting exposure. This is textbook behavior following a parabolic advance: the same momentum-driven buying that carried gold above $5,500 created fragile positioning that was vulnerable to a catalyst. That catalyst arrived on January 30, when President Trump’s nomination of Kevin Warsh as the next Federal Reserve chair sent gold futures plunging as much as 16 percent intraday before settling roughly 11 percent lower, while silver collapsed over 30 percent on the day, reaching intraday lows nearly 39 percent below recent peaks, as markets repriced expectations around a perceived hawkish pivot in monetary policy. The selling since then has been an extended de-leveraging event, not a fundamental reassessment of why gold was rising in the first place.2,3

There is also a less discussed but potentially significant demand channel that market observers believe has been disrupted by the Strait of Hormuz closure. A widely discussed thesis among gold analysts and de-dollarization commentators holds that Saudi Arabia accepts yuan-denominated payments for a portion of its oil sales to China, with the Saudis then converting that yuan into physical gold through the Shanghai International Gold Exchange. Neither government has officially confirmed the existence or scale of this channel, and audited volume data from the exchange remains unavailable. However, the thesis has gained credibility among institutional observers, supported by tangible infrastructure: the China-Saudi $7 billion currency swap agreement, expanded yuan settlement arrangements, and reports of SGEI vault facilities being developed in the Gulf region. The logic is straightforward—oil exporters seeking to diversify away from the dollar but unwilling to hold large yuan reserves could use the Shanghai exchange as an intermediary, effectively converting energy exports into gold. What is not in dispute is the scale of the underlying oil disruption. Before the war, China received approximately 5.35 million barrels of oil per day via the Strait of Hormuz; that figure has plummeted to roughly 1.22 million barrels per day, according to Foreign Policy. Saudi Arabia has partially offset the disruption by rerouting exports through its East-West pipeline to the Red Sea port of Yanbu, but Bloomberg reported that the kingdom has only recovered about half its normal export volume through this bypass. If this conversion channel was operating at any meaningful scale—and the circumstantial evidence suggests it may have been—then the sharp reduction in Saudi-to-China oil flows would logically impair it, potentially explaining a portion of the price weakness we have observed.4

The market’s other prevailing explanation for the correction—that gold should fall because the new Fed chair signals a more restrictive monetary stance—deserves serious scrutiny. Kevin Warsh is indeed perceived as a monetary hawk, and his nomination clearly spooked precious metals markets in January. But the practical reality of his confirmation tells a very different story. As of this week, the Senate Banking Committee has not even received the necessary paperwork from the White House to schedule a confirmation hearing, according to Semafor. Senator Thom Tillis, a Republican whose vote is essential given the committee’s narrow 13-11 majority, has publicly stated he will block the nomination until a Department of Justice investigation into Jerome Powell is resolved. CNBC reported that Powell himself has said he will remain as chair until a successor is confirmed. In short, the hawkish Fed narrative that triggered the initial selloff is built on a nomination that may not produce a confirmed chair for months—and by the time it does, the political calculus may look entirely different.5,6

That political calculus brings us to what we believe is the most important variable for gold over the remainder of 2026: the midterm elections in November. As The Boston Globe and Morgan Stanley have both noted, the Trump administration’s economic strategy is explicitly oriented toward running the economy hot ahead of the ballot box. The incentive structure is transparent—deliver visible growth, lower borrowing costs, and favorable asset prices to strengthen the Republican position. This means sustained pressure on the Federal Reserve to accommodate fiscal expansion, regardless of who occupies the chair. The Fed held rates steady in January despite vocal White House demands for cuts, but as the election approaches and economic softness materializes from the trade disruptions and geopolitical uncertainty, the path of least resistance for any Fed leadership—whether Powell, Warsh, or an interim arrangement—will be toward accommodation. That environment is unambiguously supportive of gold.7

The fiscal backdrop reinforces this conviction. The Congressional Budget Office estimated that the federal deficit reached $1 trillion in just the first five months of fiscal year 2026, with $308 billion borrowed in February alone. That projection, already alarming, did not account for the Iran conflict that began on February 28. Fortune reported that the war is costing American taxpayers roughly $800 million to $1 billion per day, and the Pentagon has requested an additional $200 billion in supplemental funding, according to Military.com. The national debt has surged past $39 trillion. The Committee for a Responsible Federal Budget warned that even a 60-day conflict would add approximately $66 billion in net new expenses including interest costs, and the 4Foreign Policy, “Iran War: Strait of Hormuz Closure Is Squeezing China’s Oil Supply,” March 17, 2026; Bloomberg, “Saudi Arabia Has Revived Half Its Oil Exports Via Hormuz Bypass,” March 18, 2026. 5Semafor, “Senate Still Waiting on Fed Nominee Warsh’s Paperwork,” March 16, 2026; CNBC, “Tillis Maintains Blockade on Fed Pick Kevin Warsh Over Powell Probe,” March 10, 2026. 6CNBC, “Powell Says He Will Stay On as Head of the Fed Until Warsh Is Confirmed,” March 18, 2026. 7The Boston Globe, “Trump Wants to Run the Economy Hot, as Midterm Elections Approach,” February 8, 2026; Morgan Stanley, “7 Political Trends Investors Should Watch in 2026.” CBO’s own long-term outlook projects the deficit growing to $3.1 trillion by 2036, driven by interest payments and entitlements. This is the fiscal environment in which markets are being asked to believe that the United States will pursue tighter monetary policy. We find that proposition implausible.8,9

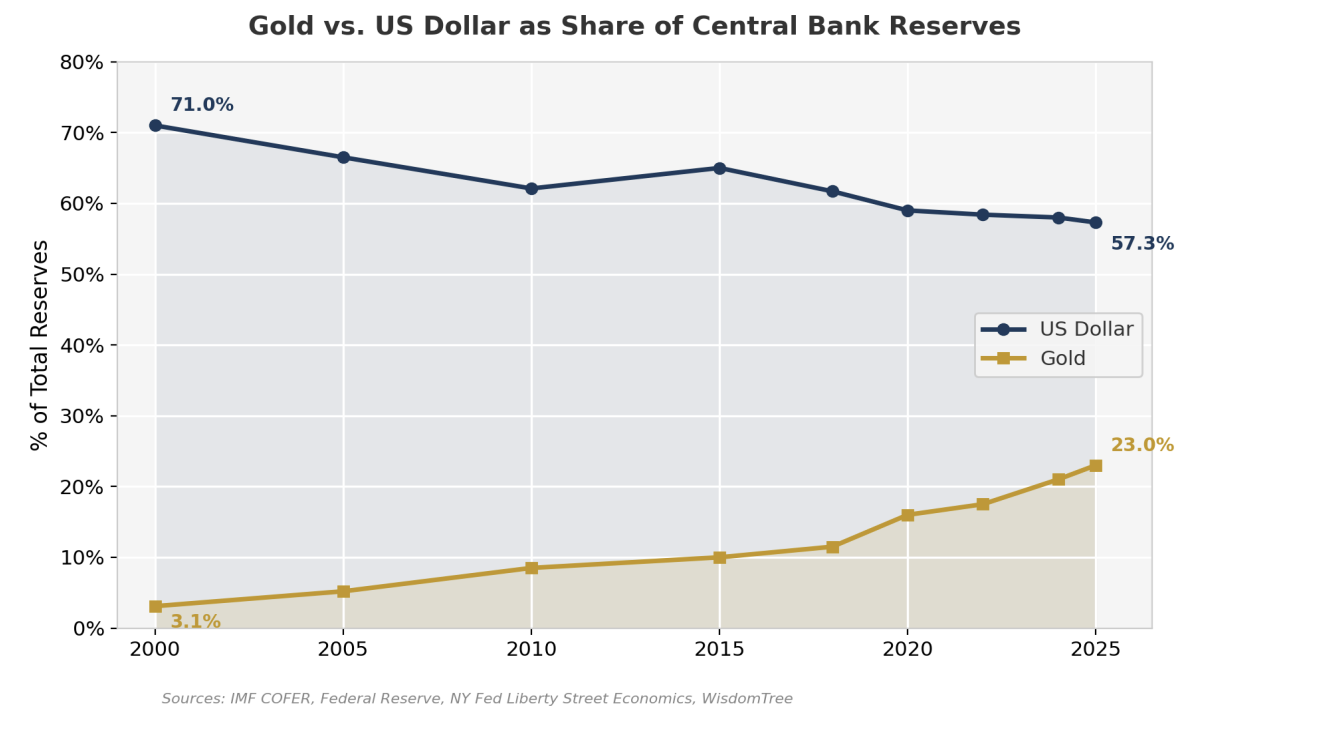

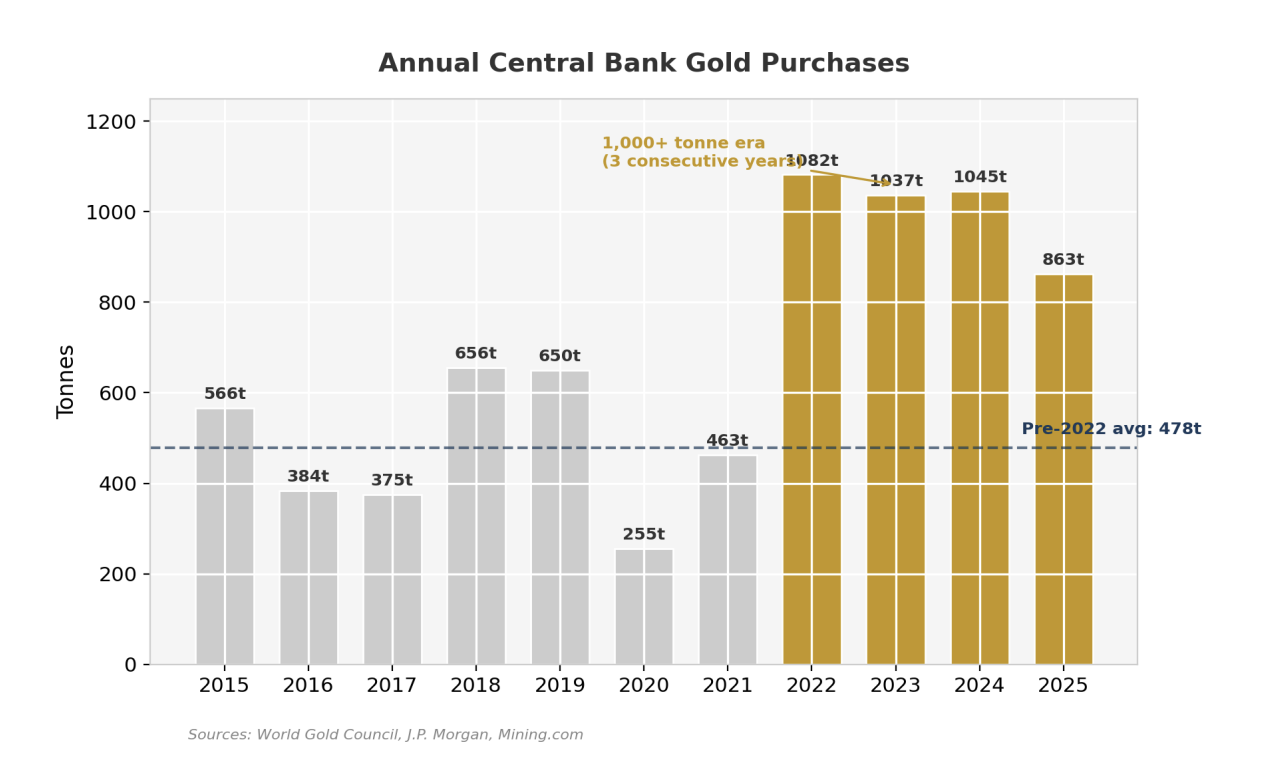

Stepping back from the near-term noise, the structural case for gold remains as strong as it has been at any point in this cycle. Central banks purchased 863 tonnes of gold in 2025, and a record 43 percent of central banks surveyed indicated plans to increase their gold holdings in 2026, according to industry data—the highest proportion ever recorded. The broader trend is unmistakable: since 2022, central banks have sustained purchases well above the pre-2022 average of roughly 478 tonnes per year, accumulating more than 1,000 tonnes annually for three consecutive years before moderating slightly in 2025. Meanwhile, gold’s share of total central bank reserve assets has more than doubled from below 10 percent in 2015 to over 23 percent today, while the U.S. dollar’s share has declined from 65 percent to approximately 57 percent over the same period, according to IMF COFER data and Federal Reserve research. The forces driving that accumulation—de-dollarization, geopolitical hedging, and concerns about the sustainability of U.S. fiscal policy—have not abated; they have intensified. For investors, the message of this correction is not that gold’s rally is over, but that the technical unwind of crowded positioning and the forced liquidation from sovereign balance sheets have created an opportunity. The fundamentals—chronic deficits, political pressure on the central bank, a weakening dollar, and sustained central bank demand—point decisively toward higher prices over the medium and long term. We encourage clients to view this pullback as a chance to add exposure and to contact a Euro Pacific Asset Management advisor to discuss how gold and precious metals fit within a diversified, internationally oriented portfolio.10

1Bloomberg, “Turkey Eyes $135 Billion Gold Reserves for Lira Defense,” March 24, 2026.

2JPMorgan via CoinDesk, “Bitcoin Holds Ground as Gold, Silver Slide on ETF Outflows and Liquidity Strains,” March 26, 2026.

3Fortune, “Kevin Warsh’s Fed Nod Sends Gold Plunging,” January 31, 2026.

4Foreign Policy, “Iran War: Strait of Hormuz Closure Is Squeezing China’s Oil Supply,” March 17, 2026; Bloomberg, “Saudi Arabia Has Revived Half Its Oil Exports Via Hormuz Bypass,” March 18, 2026.

5Semafor, “Senate Still Waiting on Fed Nominee Warsh’s Paperwork,” March 16, 2026; CNBC, “Tillis Maintains Blockade on Fed Pick Kevin Warsh Over Powell Probe,” March 10, 2026.

6CNBC, “Powell Says He Will Stay On as Head of the Fed Until Warsh Is Confirmed,” March 18, 2026.

7The Boston Globe, “Trump Wants to Run the Economy Hot, as Midterm Elections Approach,” February 8, 2026; Morgan Stanley, “ 7Political Trends Investors Should Watch in 2026.”

8CRFB, “CBO Estimates $1 Trillion Deficit for First Five Months of FY 2026”; Fortune, “Trump’s Iran War Is Costing American Taxpayers $1 Billion a Day,” March 11, 2026; Military.com, “Pentagon Seeks $200 Billion in Additional Funds for the Iran War,” March 19, 2026.

9U.S. News, “US National Debt Surges Past $39 Trillion Just Weeks Into War in Iran,” March 18, 2026; CBO, “The Budget and Economic Outlook: 2026 to 2036.”

10IMF COFER; Federal Reserve, “The International Role of the U.S. Dollar – 2025 Edition”; World Gold Council; J.P. Morgan; Mining.com.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Euro Pacific Capital

Read more commentaries by Euro Pacific Capital