AI hasn’t just increased demand for memory — it has fundamentally recast memory as a defining strategic asset in the AI era.

Quick read:

- Rising demand for critical microelectronics, bolstered by AI capex and defense spending, is driving semiconductor prices higher and posing upside risks to global goods inflation.

- Developed Asia (Japan, South Korea, Taiwan) is at the epicenter of the semiconductor boom. As the dominant producers of advanced chips and commoditized memory chips, these economies are benefiting from improving terms-of-trade dynamics that support corporate earnings and debt sustainability.

- In the BlackRock Tactical Opportunities Fund, we remain short global government bonds on the back of upside risks to inflation from upstream commodity prices. Trade competitiveness insights help to inform long exposures in DM Asia stock and bond markets.

Solid state electronics control the modern economy. The critical nature of these microelectronics became front page news during the COVID pandemic when supply chain related chip shortages forced the shutdown automotive production lines and doubled the secondary market prices for consumer goods like the PlayStation 5 console. Those acute 2020 supply shortages contributed to the surge in global good price inflation and also catalyzed numerous fiscal expansions, like the US CHIPS ACT, as countries sought to create incentives to reshore microelectronic production and reduce supply chain dependencies. Whereas the 2020 jump in microelectronics prices were primarily attributable to supply chain disruptions, we now see a booming global industrial cycle generating excessive demand for these critical microelectronics. The current investment boom in artificial intelligence (AI) datacenters and remilitarization is generating a demand-driven increase in microchip prices.

Sharp rises in integrated circuit prices have the potential to generate another bout of global goods price inflation in 2026. In portfolios like the Tactical Opportunities Fund, inflation-related insights help to inform our directional short government bond positions. Higher chip prices also boost the international trade competitiveness of the developed market (DM) North Asian countries – Japan, South Korea, and Taiwan – that control the production of many of these critical microchips. The improvement in this region’s terms-of-trade helps to inform our cross-sectional longs to the stock and bond markets of these countries.

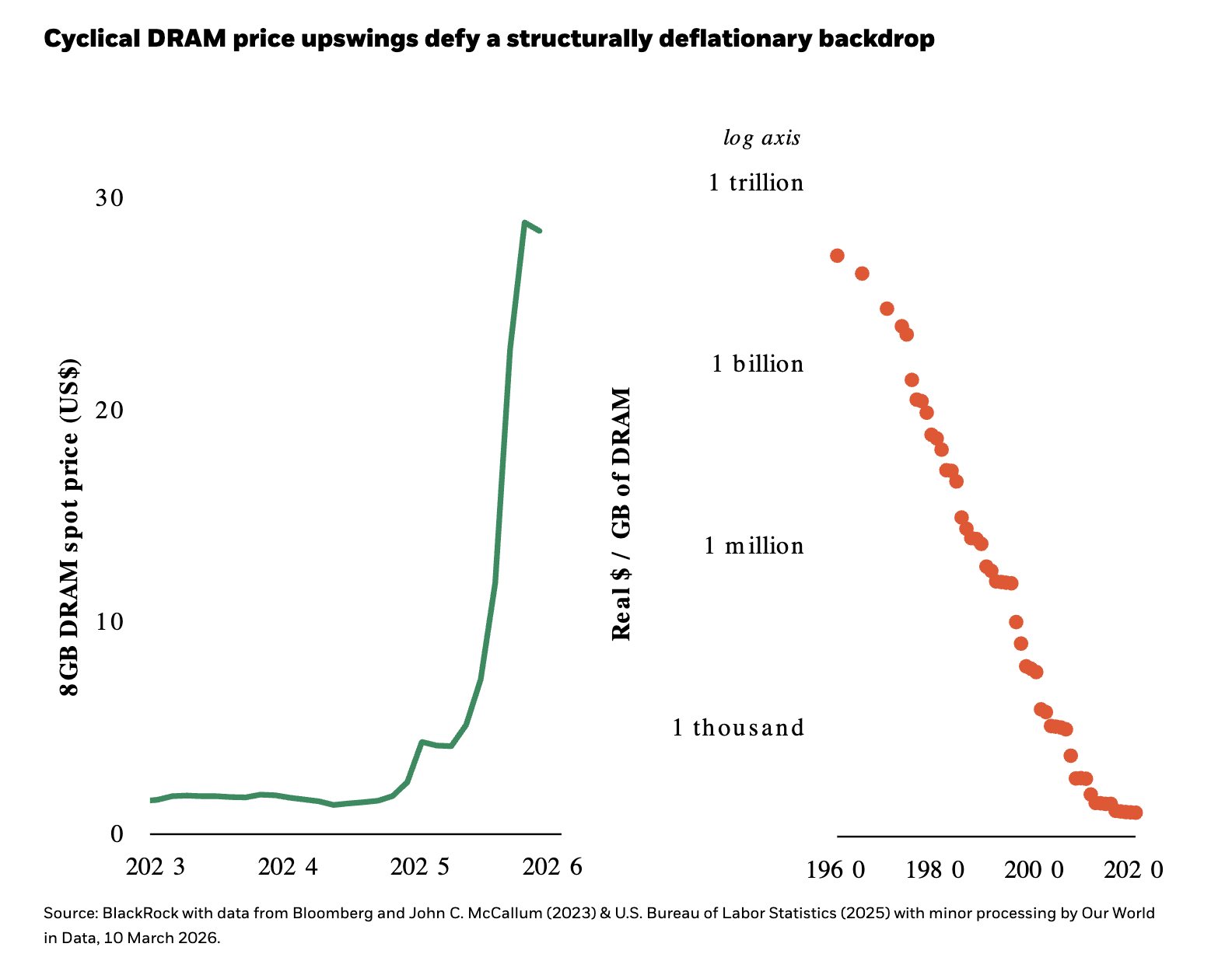

Integrated circuit prices defying Moore’s Law

The plots below show the recent price jumps for DRAM chips alongside the longer-term deflationary price dynamics. Prices for these critical but commoditized microelectronics have risen 17-fold over the last year, which is a sharp discontinuity from the multi-decade price declines. It is also worth noting that there had been a slowdown in exponential price declines even before the recent inflation: “The price of a gigabyte of DRAM has fallen by about a factor of ten every 5 years from 1957 to 2020. Since 2010, the price has fallen much more slowly, at a rate that would yield an order of magnitude over roughly 14 years.”1 Without Moore’s Law driving sustained price declines in commoditized microelectronics there will be upside risks to consumer goods prices in the coming years.

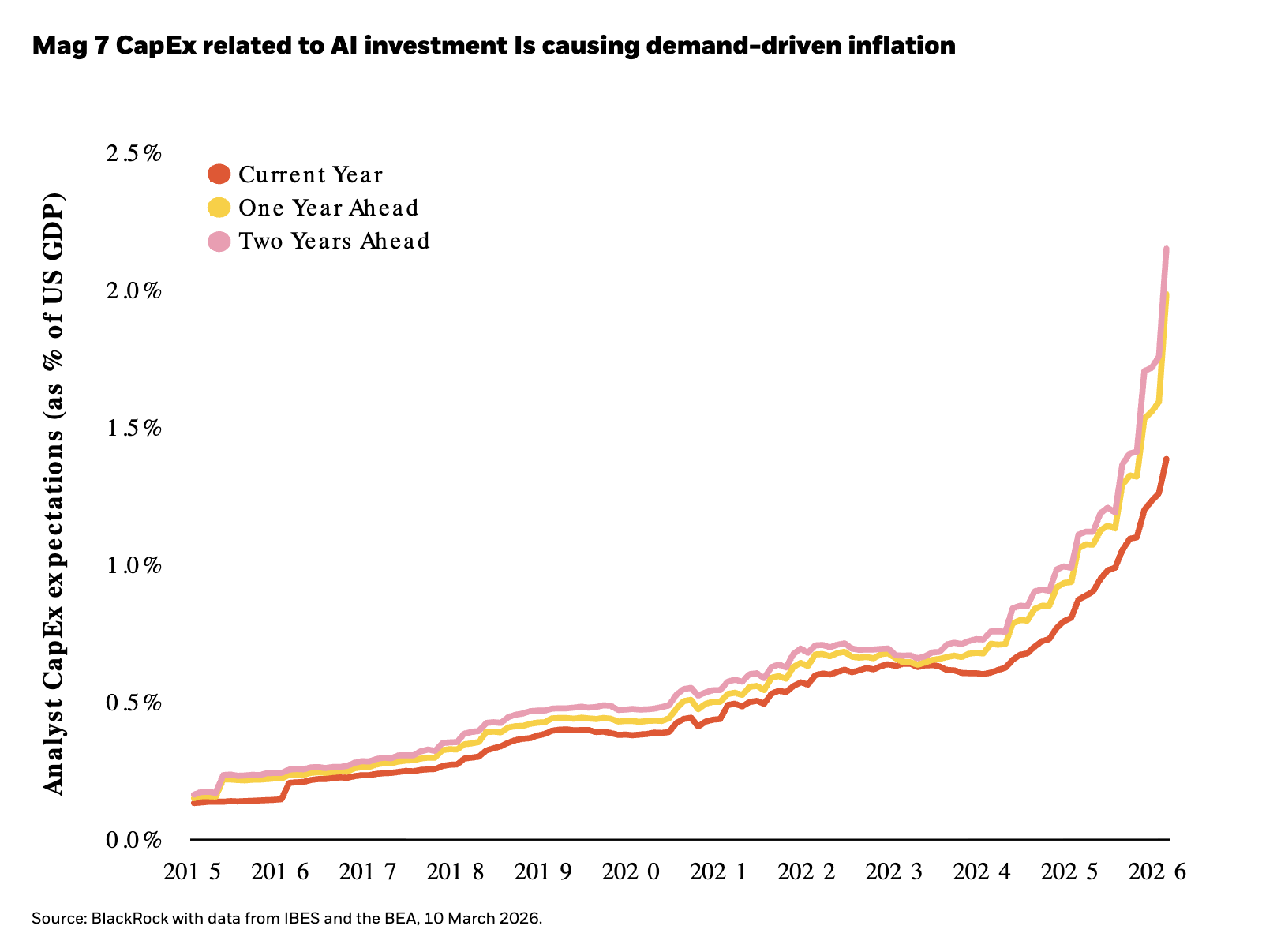

Recent commentary on microchip prices has tended to apply a supply side framing that we view as misplaced. Instead, we see exponential price rises as a natural outcome of exponential demand. The chart below shows the analyst estimates for annual capital expenditures across the MAG 7 hyperscalers as a percentage of GDP. This is only a sub-set of the demand for microelectronics and doesn’t include the expanding national defense and consumer electronics demand. We believe that rising DRAM prices are rationally anticipating a price inelastic surge in microelectronics demand.

The global chips investment boom flows through DM Asia

Developed Asia is the production epicenter for the world’s most advanced microchips – centered around TSMC in Taiwan. The region also controls the global production of less sophisticated but no-less-critical integrated circuits – with South Korea alone producing nearly 75% of the global DRAM chips. Those Dynamic Random Access Memory chips inspired the title of my favorite Daft Punk album but, more importantly, are a necessary component for all electronic devices. DRAM chips store data for rapid retrieval for AI data centers, military equipment, your iPhone, and any other good that touches the digital economy.

Terms-of-trade (ToT) is the ratio of a country’s export prices to its import prices. An improving ToT corresponds to a gain in international competitiveness and a rise in a country’s national income relative to its trading partners. The sources of ToT improvements are manifold – an appreciation of the exchange rate, shifts in product and commodity prices, or the deployment of new technologies. Typically associated with exchange rate appreciations, sustained ToT improvements make a country’s stocks and bonds attractive in the global cross-section as the rising national incomes support corporate earnings and debt sustainability.

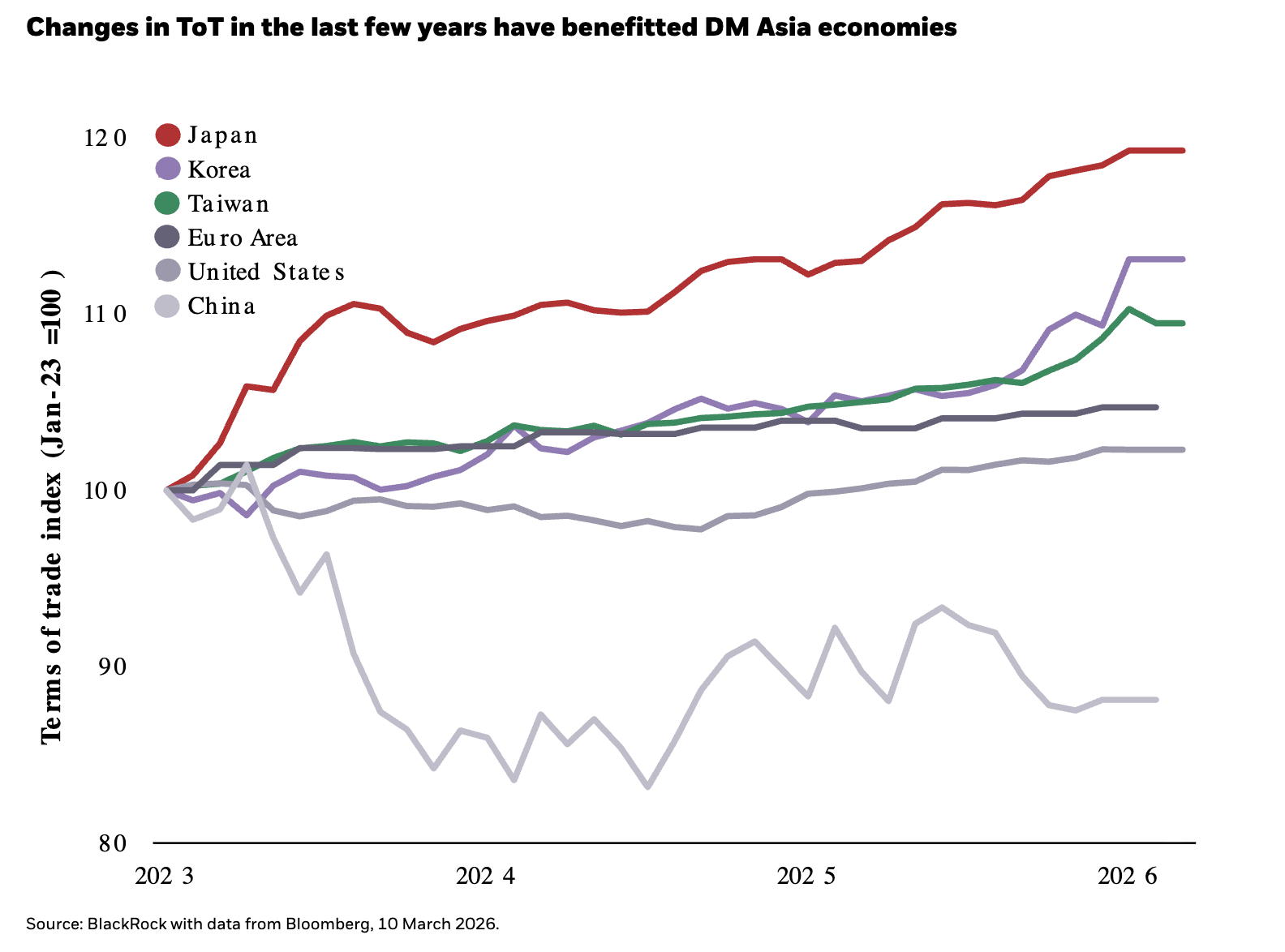

The plot below helps to visualize how the price rises of high-tech goods has generated a sustained improvement in of DM Asia’s terms-of-trade relative to the large economies of the US, China, and the Eurozone. Despite having relatively weak currencies, Japan, South Korea, and Taiwan export goods – industrial goods like semiconductors, high tech machinery, and automobiles – that have been steadily rising in value in the global marketplace. Corporations in these countries have thus been able to grow margins and profits as their customers have been willing to ante up for the critical inputs fueling the simultaneous AI capex and defense spending booms. The governments in these countries have also benefitted from rising national incomes that have bolstered their debt sustainability dynamics.

So what does it all mean for portfolios?

In our diversifying liquid alternative portfolios like the BlackRock Tactical Opportunities Fund, we seek to deliver returns that are lowly correlated with stock and bond markets. We do so primarily by seeking out tactical relative value opportunities across countries’ stock, bond, and currency markets.

DM Asian equity markets have outperformed global equity indices over the last few years. We’ve been overweight the region to varying degrees since 2020 and we’ve tactically rotated positioning across Japan, Taiwan, and South Korea. The high-tech exports of all three of these countries and sustained ToT improvements have translated into material earnings outperformance relative to other regions. On the back of recent price outperformance and positioning, we’ve trimmed regional exposures but continue to overweight Japanese equities.

In fixed income, we have increased government bond exposures across DM Asian issuers as rising national incomes boost debt sustainability metrics and overall borrowing capacity. On the back of late 2025 bond market sell-offs, we added cross-sectional longs in the portfolios in South Korea and Taiwan. In the last couple of months, we have added to directional short duration positions based on inflation insights. We see upstream microelectronics price jumps translating into higher consumer goods prices in the coming quarters - an effect already visible in the computer software prices subcomponent of Consumer Price Index (CPI) that has posted a cumulative gain of 15.5% in the past 3 months.2

Source

1. Asya Bergal at AIIMPACTS summary of the longer-term price dynamics.

2. Computer software prices were up 6.5% month-on-month in the February CPI. This is a component with a stark weight difference between CPI vs PCE, with a weight of 0.03% in CPI and 1.1% in PCE. PCE is the Federal Reserve’s target variable for inflation and we see growing risks that PCE prices overshoot CPI based on weight and methodological differences.

The Morningstar Rating™ for funds, or “star rating”, is calculated for managed products (including mutual funds, variable annuity and variable life sub-accounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product’s monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10 of products in each product category receive 5 stars, the next 22.5 receive 4 stars, the next 35 receive 3 stars, the next 22.5 receive 2 stars, and the bottom 10 receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100 three-year rating for 36-59 months of total returns, 60 five-year rating/40 three-year rating for 60-119 months of total returns, and 50 10-year rating/30 five-year rating/20 three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods. Past performance does not guarantee future results.

To obtain more information on the funds, including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please click on the fund product profile page above.

Tom Becker, Senior Portfolio Manager, Global Tactical Asset Allocation Team

Simon Wan, Portfolio Manager, Global Tactical Asset Allocation Team

Ryan Zamani, Portfolio Manager, Global Tactical Asset Allocation Team

Carefully consider the investment objectives, risks, charges and expenses of the funds carefully before investing. The prospectuses and summary prospectuses contain this and other information about the funds and are available, along with information on other BlackRock funds, by calling 800-882-0052 or at blackrock.com. The prospectus and, if available, the summary prospectus should be read carefully before investing.

Important risks: These funds are actively managed and their characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Asset allocation strategies do not assure profit and do not protect against loss. These funds may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

The opinions expressed are those of the fund’s portfolio management team as of 30 March 2026, and may change as subsequent conditions vary. Information and opinions are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Investing involves risk, including possible loss of principal.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA.

©2026 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

MASS0326-5300662-EXP0327

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© BlackRock

Read more commentaries by BlackRock