A Systematic Lens on Global Equity Opportunities Within Multi-Asset Portfolios

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhat are systematic equities?

Systematic equity investing is a way to invest in the stock market using clear rules and data, rather than guesswork or hunches. Instead of trying to pick stocks based on trends or headlines, this approach uses research, data, and technology to systematically identify opportunities across global markets.

The goal? To help investors in PIMCO’s multi-asset strategies grow their investments more steadily, avoid over concentrations in big-name stocks, and help mitigate the volatility that often comes from following the “crowd”.

Over the past several years, global equity markets have been defined by concentration, with a handful of mega-cap technology companies accounting for an outsized share of returns. This has led to a narrow bull market and pushed valuations higher, particularly in the U.S. Yet, as we enter 2026, the broad perception of “expensive equities” masks pockets of value and a growing opportunity set, supported by solid economic growth and improving earnings.

For more than two decades, PIMCO has designed and managed global asset allocation strategies in which equities play a pivotal role. Within these multi-asset portfolios, equity exposures are implemented through a disciplined, data-driven and repeatable approach to pursuing equity alpha that is designed to help complement broader portfolio objectives rather than operate in isolation. In this context, we believe our systematic equity approach is well positioned for navigating toward more balanced and broader market participation.

Our rules-based, systematic equity investment process focuses on identifying well-rounded companies across regions and sectors, helping our multi-asset portfolios remain broadly diversified while accessing sources of return potential that more traditional approaches may overlook.

In an environment where equity markets have become increasingly concentrated, we believe this discipline is particularly important and can contribute meaningfully to outcomes across the multi-asset portfolios that incorporate it.

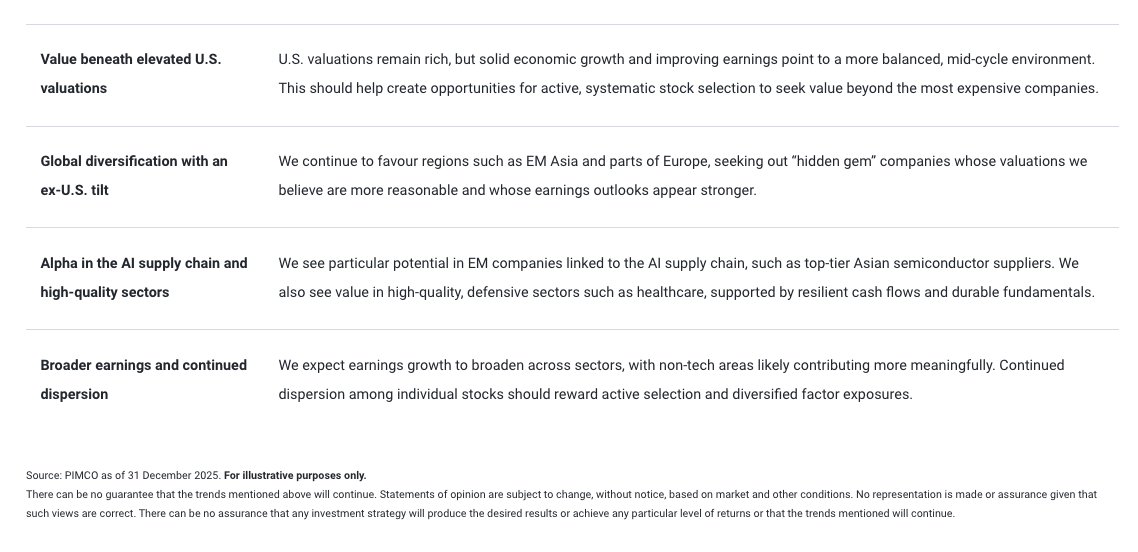

How are our strategies positioning for opportunities in 2026?

In 2025, global equity markets returned more than 22%Footnote1 as valuations approached historically high levels. Following over a decade of U.S. equity market outperformance, markets outside the U.S. – notably emerging markets (EM) in Asia as well as parts of Europe – delivered higher returns than the U.S. in 2025Footnote2. Across investment styles, value, momentum, and growth factors all contributed positively, while quality lagged. Despite market concentration, differences between individual stocks widened materially.

Against this backdrop, our 2026 positioning focuses on:

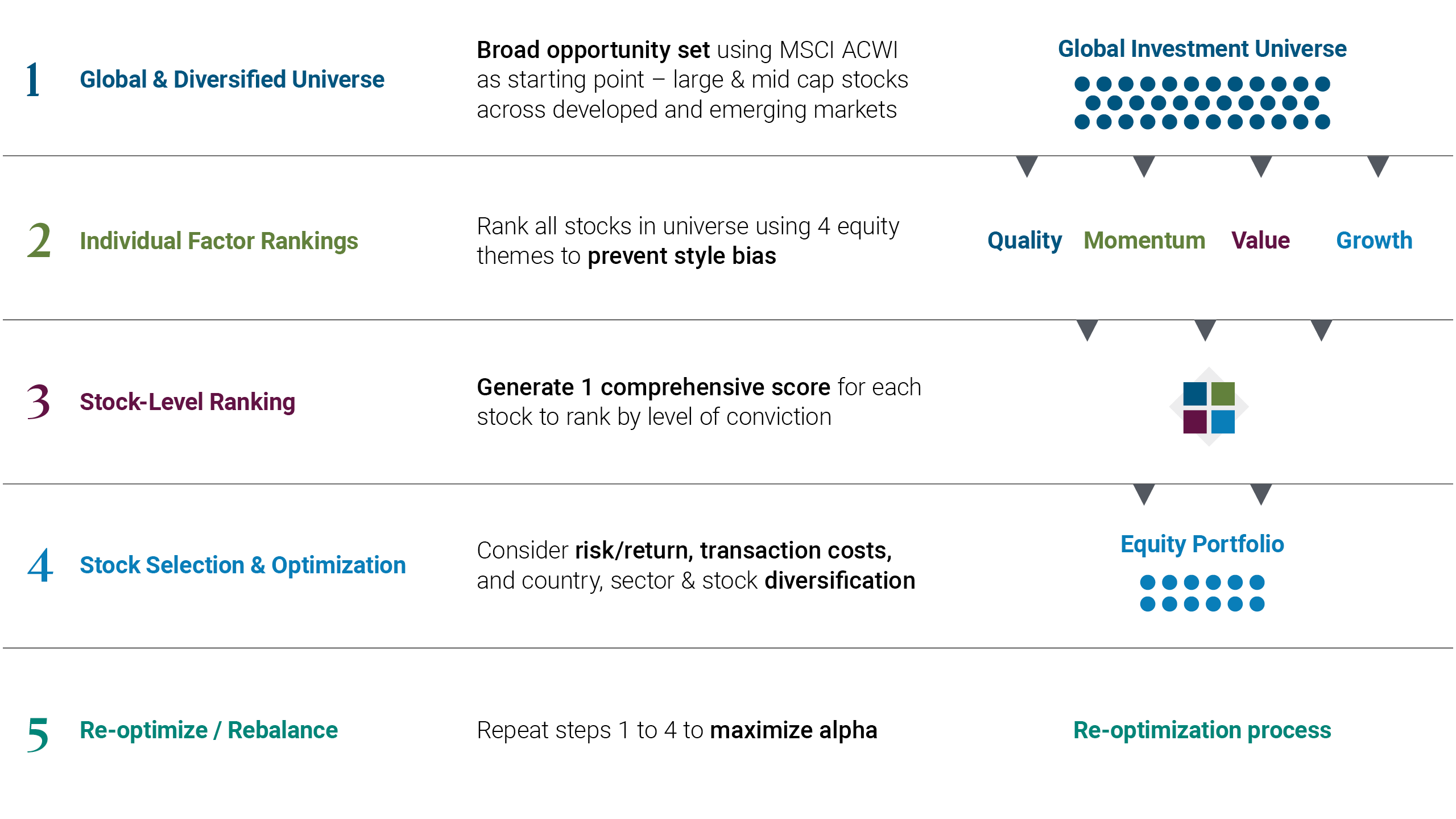

PIMCO’s systematic equity approach

Our systematic equity strategies are grounded in the belief that markets are not perfectly efficient and that persistent sources of return can be accessed through a transparent, time-tested process (see Figure 1).

- Multi-factor lens (four themes): We analyse companies using momentum, growth, quality, and value factors – drawing on both traditional data (earnings, cash flows) and alternative data (text analytics from company filings, customer-supplier relationships).

- Research-driven signals: We use more than two dozen distinct “alpha signals”, including over 15 proprietary PIMCO-designed indicators, to help identify well-rounded companies with strong return potential.

- Quality of signals over quantity of signals: Return generation can often stem from the robustness of individual signals rather than their sheer number. Our process aims to only include signals grounded in sound economic theory that we believe are capable of generating alpha net of transaction costs across the global opportunity set.

- Diversified portfolios with risk controls: We look to spread exposure across countries, sectors, and companies, supported by guardrails designed to pursue a balance between identifying companies poised to outperform and avoiding concentration risk.

Figure 1: PIMCO’s systematic equity portfolio construction process

Case studies: How PIMCO's systematic strategies responded to 2025's shifting signals

Throughout 2025, our systematic equity process dynamically adjusted portfolio positioning as underlying factor signals evolved. This approach helped increase exposure to securities where multiple signals strengthened in tandem and reduced exposures where signal profiles weakened or became less differentiated.

The examples below are provided for illustrative purposes only and were selected by PIMCO to demonstrate how our process is designed to respond to changing market conditions. They do not represent all portfolio decisions or outcomes, and signal changes are one of the many inputs within our overall investment processFootnote3:

- AI-linked semiconductor supplier in emerging markets

As 2025 progressed, this company’s score profile strengthened meaningfully, with improving earnings indicators, firmer momentum trends, and supportive industry data. With these signals reinforcing one another, our portfolios increased exposure to the stock as its scoring profile continued to improve. - Global technology infrastructure provider

Mid-year, momentum indicators strengthened while quality and valuation signals remained steady. With several strong indicators aligning at once, our portfolios increased their positioning to reflect what we believe was a notable improvement in the stock’s overall attractiveness. - Large global healthcare company

After delivering solid early-year performance, this company’s earnings-quality metrics began to soften and its overall signal strength moderated. In line with our disciplined process, our portfolios reduced exposure as the stock’s scores weakened.

Why systematic, active equity matters now

Passive strategies can overweight areas where valuations are stretched, while traditional discretionary active management may expose investors to concentration risk. A globally-diversified, systematic, and rules-based approach can help address these challenges by:

- Identifying diverse sources of return potential across regions, sectors, and companies

- Managing concentration risk and reduce imbalanced exposure across investment styles

- Adapting as market conditions shift, through disciplined, rules-based re-balancing

The challenge with fundamental active management

Most active equity managers have struggled to consistently outperform their benchmarks, particularly in markets dominated by a small number of stocks. Over the trailing one-year periodFootnote4, less than 40% of active managers in Morningstar’s Global Large-Cap Blend Equity category outperformed their benchmarks. Over longer periods, the success rate falls dramatically, with only 3.7% outperforming over the past decade. Notably, over the last 10 years, the median active global equity manager underperformed the MSCI All Country World Index (ACWI) by a cumulative 76%.

Several behavioural biases may contribute to this:

- Overconfidence: Making outsized bets on familiar companies

- Performance chasing: Buying recent winners

- Familiarity bias: Focusing too heavily on home markets or well-known brands

A disciplined, data-driven, and rules-based approach helps mitigate these biases and helps support more consistent decision-making.

Conclusion

Heading into 2026, headline equity valuations remain elevated, but opportunities are expanding across regions, sectors, and styles. In this environment, a disciplined, systematic approach can help identify emerging leaders while avoiding overexposure to a more concentrated set of stocks.

Within the equity allocations of PIMCO’s multi-asset strategies, we are consistently reviewing and evaluating long-term themes to balance exposures across quality, value and momentum factors, and allocating to markets where earnings growth prospects appear to be improving, with the goal of improving portfolio outcomes over time.

By combining clear, intuitive alpha signals with robust research, data, and risk controls, PIMCO’s systematic equity approach is well-positioned to help navigate the next phases of market evolution in pursuit of consistent, long-term outcomes across our asset allocation strategies.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Footnotes:

1 Source: Bloomberg. Global equities represented by the MSCI ACWI Index. Return to content

2 Source: Bloomberg. EM equities represented by the MSCI Emerging Markets Index; European equities represented by the Euro STOXX 50, FTSE 100, and MSCI Europe indices; U.S. equities represented by the S&P 500 Index. Return to content

3 Past performance, factor signals, and portfolio positions are not a guarantee or a reliable indicator of future results. Return to content

4 Data as of December 31, 2025. Source: Morningstar.

Disclosures

Past performance is not a guarantee or a reliable indicator of future results.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Investing in foreign-denominated and/or -domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Management risk is the risk that the investment techniques and risk analyses applied by an investment manager will not produce the desired results, and that certain policies or developments may affect the investment techniques available to the manager in connection with managing the strategy. Diversification does not ensure against loss.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

INDEX DESCRIPTIONS

The Morningstar Global Large‑Cap Blend Equity category consists of funds that primarily invest in large‑capitalization companies across developed global markets, including regions such as North America and Greater Europe. Funds in this category typically allocate at least 75% of total assets to equities and pursue a balanced blend of growth and value characteristics across industries and geographies. This category is intended to provide diversified exposure to large global companies with potential for long‑term, steady growth

The MSCI All Country World Index (ACWI) is a free‑float adjusted, market‑capitalization‑weighted benchmark designed to measure the equity performance of both Developed Markets (DM) and Emerging Markets (EM) worldwide. The index captures approximately 85% of the global investable equity opportunity set and includes more than 2,500 large‑ and mid‑cap constituents spanning 49 countries. ACWI is widely used as a comprehensive measure of global equity market performance.

©2026 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

It is not possible to invest directly in an unmanaged index

This document contains examples of the firm's internal investment research capability. The data contained within the reports may not be related to the strategies discussed herein, may be stale and should not be relied upon as investment advice or a recommendation of any particular security, strategy or investment product. In selecting case studies, PIMCO considers investment performance in addition to other factors, including, but not limited to, whether the example illustrates the particular investment strategy being featured and processes applied by PIMCO to making investment decisions. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

The terms “cheap” and “rich” as used herein generally refer to a security or asset class that is deemed to be substantially under- or overpriced compared to both its historical average as well as to the investment manager’s future expectations. There is no guarantee of future results or that a security’s valuation will ensure a profit or protect against a loss.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0304-5276777

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All