Municipal Sell-Off Presents Attractive Entry Point

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsFixed income markets have faced a challenging stretch following the escalation of conflict in the Middle East. Sharply rising oil prices and renewed inflation concerns have pushed US Treasury yields higher, and municipal bonds have moved in tandem.

As a result, the muni asset class experienced its weakest monthly performance in nearly two years, with broad municipal indexes declining 2.3% in March.

While periods like this can feel uncomfortable, they may also create opportunity. Let’s look at why today’s combination of higher yields, a steeper yield curve and improved relative value has set up a potentially attractive entry point ahead of stronger supply/demand technicals expected this summer.

Yields have reset higher

The recent backup in rates has meaningfully improved forward-looking return potential across fixed income—and municipals are no exception.

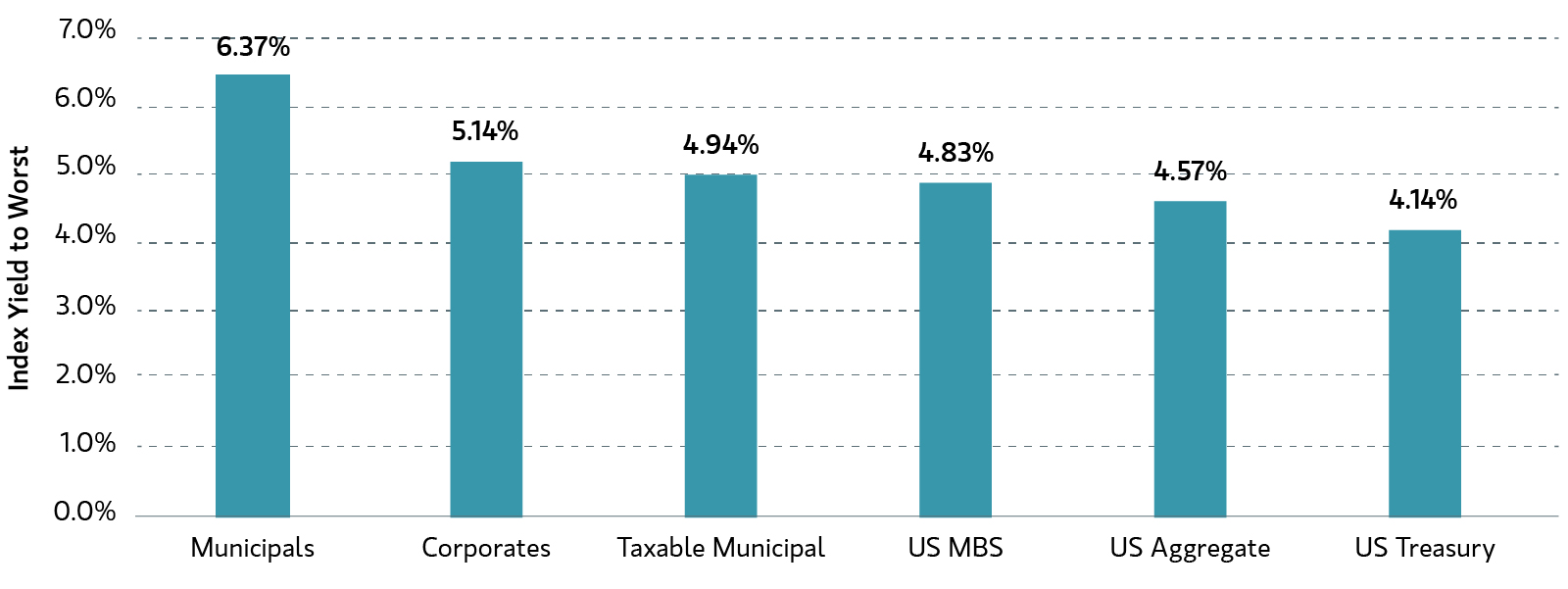

Benchmark municipal yields rose 40–60 basis points (bps) during March, bringing absolute yields into the 3.5%–4.5% range. On a taxable-equivalent basis, that translates to roughly 6%–8% for many investors. Importantly, current yields now sit approximately 120–150 bps above their 10-year averages.

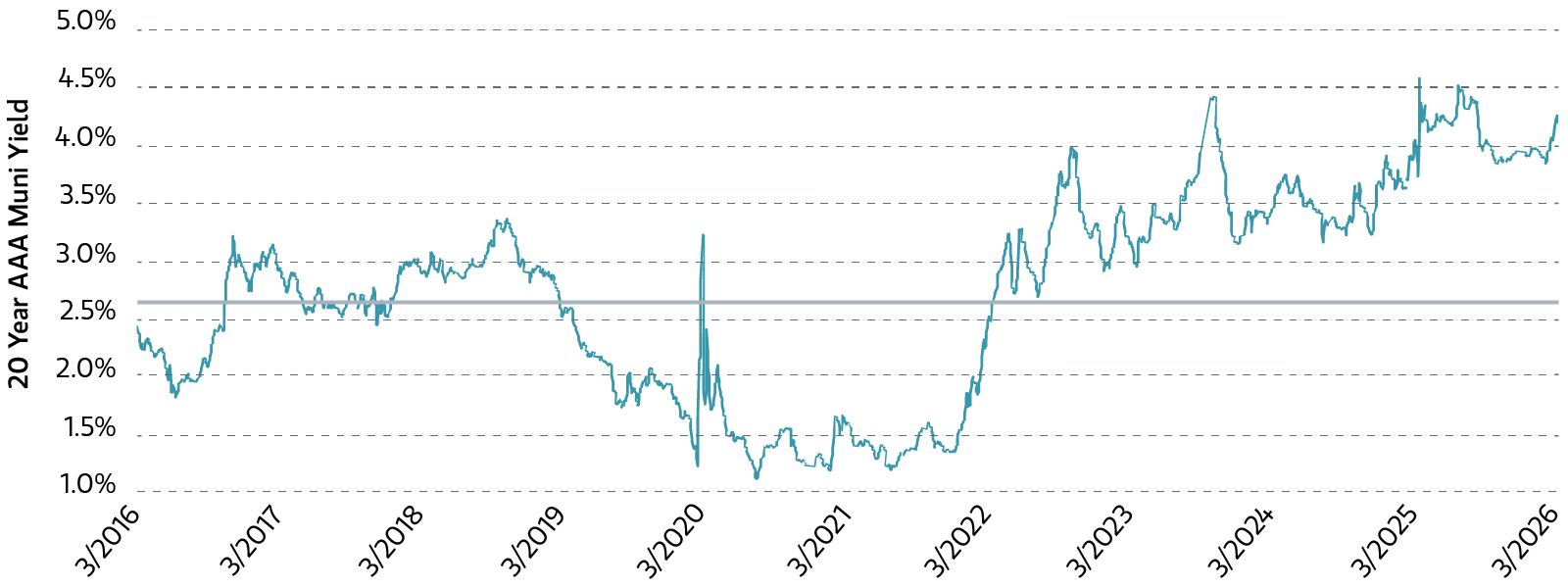

At the same time, the municipal curve has steepened to historically elevated levels. Investors are now being compensated to step out of cash, lock in yields near a multidecade high and get some duration in a portfolio. The 20-year segment of the curve stands out in particular, with yields at levels that have been exceeded only about 5% of the time over the past decade. Tax-adjusted yields in this part of the market have now approached equity-like return profiles.

Following the recent reset, the 20-year segment of the muni curve is steep and cheap

Long muni yields are near a two-decade high and over 100 bps above longer-term averages. For long-term investors, we believe this is a compelling backdrop to thoughtfully add duration and lock in higher income.

Relative value has improved

After an extended period of strong demand and tight valuations, municipals have become more attractively priced relative to taxable alternatives.

Heavy issuance has played a role. Following a record $565 billion of new supply in 2025—roughly 30% above the five-year average—issuance has remained elevated into 2026, with over $130 billion brought to market year-to-date. While demand has remained solid, the combination of supply pressure and recent rate volatility has led to a reset in valuations.

The 10-year municipal-to-Treasury ratio has risen to approximately 72%, up from around 62% earlier this year and at its highest level since last fall. In our view, this repricing has created a more compelling entry point—particularly as we approach the summer months when reinvestment flows typically accelerate and net supply often turns negative.

After a challenging March, tax-equivalent yields stand out relative to taxable alternatives

Although recent volatility triggered the first weekly outflow from municipal funds in several months, year-to-date inflows have remained strong at roughly $24 billion—on pace for one of the strongest starts to a year on record. We believe this underlying demand should help support the market as geopolitical conditions improve.

Volatility has created opportunity—especially for tax alpha

Periods of rate volatility, while unsettling, tend to expand the opportunity set—particularly for tax-aware investors.

Higher yields allow portfolios to be reset at more attractive income levels, improving long-term return potential. At the same time, price volatility may create opportunities to systematically harvest losses, generating tangible after-tax value. Over the past three years, our disciplined tax loss harvesting process has generated approximately $350 million in tax savings across our fixed income strategies.1 Volatility is never comfortable—but it often provides both potential entry points and tax alpha that has been a consistent source of excess returns.

Municipal credit fundamentals have remained strong

Despite macro uncertainty, the fundamental backdrop for municipal credit remains solid.

State and local governments continue to maintain healthy balance sheets, with rainy day fund levels averaging roughly 15% of expenditures. Credit quality trends also remain constructive, with upgrade-to-downgrade ratios holding above parity.

Importantly, municipal credit spreads have remained stable throughout the recent sell-off. This resilience reflects the high-quality nature of the asset class and suggests municipals may continue to provide downside mitigation in diversified2 portfolios should volatility persist.

Uncertainty has elevated the value of professional management

Geopolitical uncertainty tends to increase dispersion across markets—whether across interest rates, sectors or individual issuers. In these environments:

- Yield curve dynamics may shift quickly.

- Credit spreads may reprice unevenly.

- Liquidity conditions may vary meaningfully across segments.

Navigating this landscape requires disciplined duration positioning, rigorous credit analysis and thoughtful portfolio construction. In our view, professional management becomes even more valuable when risks are harder to assess and markets are less uniform.

The bottom line

While uncertainty surrounding the geopolitical backdrop remains, the recent municipal bond sell-off has meaningfully improved the opportunity set.

Taken together, higher yields, the steeper curve, more attractive relative value and the prospect of stronger seasonal technicals have created a favorable entry point for municipal investors. For those with a long-term horizon, this environment offers a potential opportunity to enhance income, add duration selectively and position portfolios more constructively for the period ahead.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

1 Source: Parametric, 12/31/2025. The information is provided for illustrative purposes only. Values are aggregated across all municipal laddered strategies, managed municipal strategies and municipal total-return strategies. Only client positions with unverified cost basis were excluded from calculations. Loss calculation is based on the amortized book price minus the sell price, represents historical information and should not be construed as future results. Loss information illustrates the effect to a portfolio and is not representative of, and should not be construed as, performance. There is no assurance that tax loss harvesting will continue in the future. There is no guarantee that any specific account may engage in tax loss harvesting.

2 Diversification does not eliminate the risk of loss.

Parametric and Morgan Stanley do not provide legal, tax or accounting advice or services. Clients should consult with their own tax or legal advisor prior to entering into any transaction or strategy.

The views expressed in these posts are those of the authors and are current only through the date stated. These views are subject to change at any time based upon market or other conditions, and Parametric and its affiliates disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Parametric are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Parametric strategy. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Past performance is no guarantee of future results. All investments are subject to the risk of loss. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the Disclosure page on our website for important information about investments and risks.

All investments are subject to the risk of loss. Fixed income securities are subject to the ability of an issuer to make timely principal and interest payments (credit risk), changes in interest rates (interest rate risk), the creditworthiness of the issuer and general market liquidity (market risk). In a rising interest-rate environment, bond prices may fall and may result in periods of volatility and increased portfolio redemptions. In a declining interest-rate environment, the portfolio may generate less income. Longer-term securities may be more sensitive to interest rate changes. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. Please refer to the Disclosure page on our website for important information about investments and risks.

Investment advisory services offered through Parametric Portfolio Associates LLC ("Parametric"), an investment advisor registered with the US Securities and Exchange Commission (CRD #114310). Parametric is also registered as a portfolio manager with the securities regulatory authorities in certain provinces of Canada (National Registration Database No. 42850) with regard to specific products and strategies. Parametric provides advisory services directly to institutional investors and indirectly to individual investors through financial intermediaries. The information on this website does not constitute an offer to sell, or a solicitation of an offer to purchase, securities in any jurisdiction to any person to whom it is not lawful to make such an offer. Investing entails risks, and there can be no assurance that Parametric (and its affiliates) will achieve profits or avoid incurring losses. All investments are subject to potential loss of principal. Parametric does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision. Please refer to the disclosure page for important information about investments and risks.

S&P Dow Jones Indices are a product of S&P Dow Jones Indices LLC (“S&P DJI”) and have been licensed for use. S&P® indexes are registered trademarks of S&P DJI; Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); S&P DJI, Dow Jones, and their respective affiliates do not sponsor, endorse, sell, or promote Parametric and its strategies, will not have any liability with respect thereto, and do not have any liability for any errors, omissions, or interruptions of the S&P Dow Jones Indices.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All