From dilution drag to shareholder discipline

For much of the past two decades, the performance gap between emerging markets (EMs) and the United States has been viewed through the lens of macro volatility, currency weakness and sector composition. Recent analysis also highlights that persistent differences in share-count behavior have been an additional factor in explaining divergent performance.

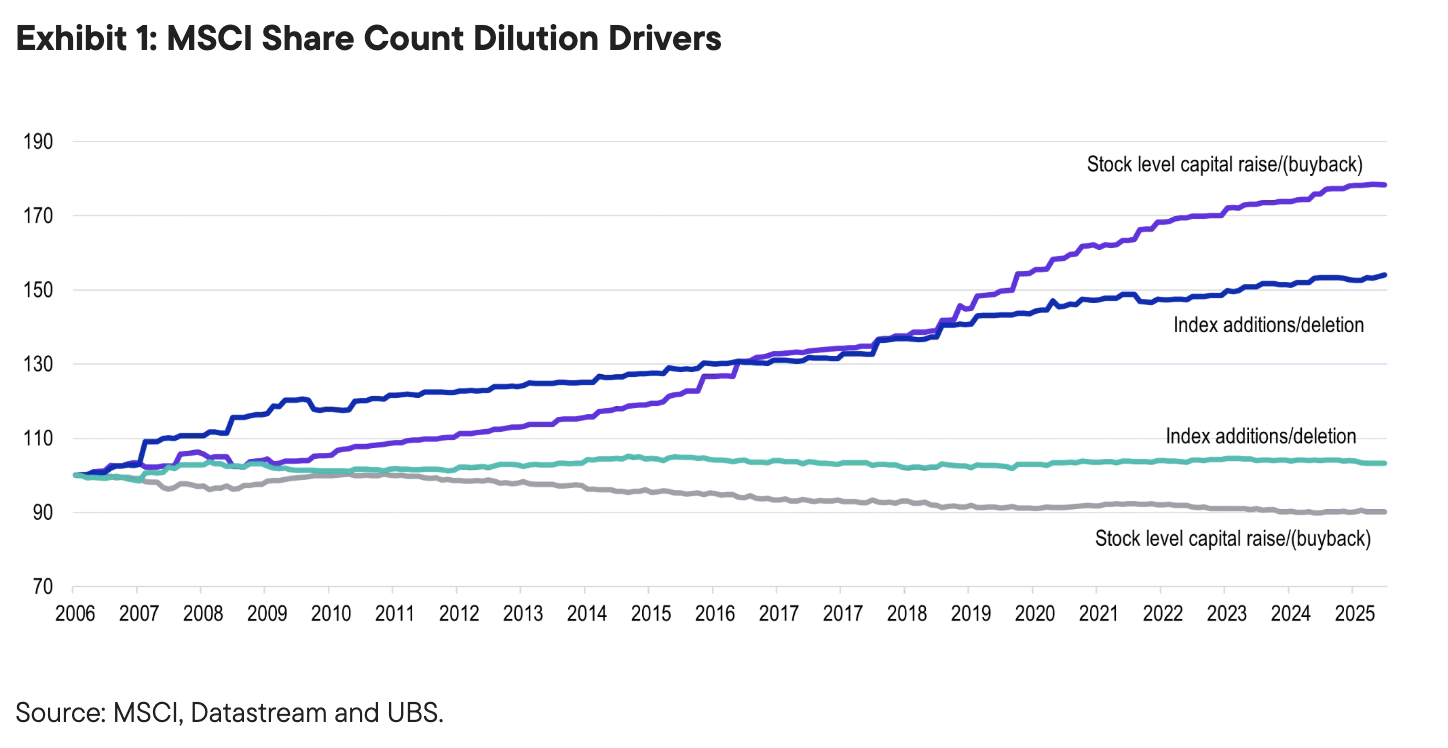

Exhibit 1 highlights the cumulative change in share count for the MSCI EM Index versus the MSCI USA Index since 2005. The divergence is striking. EM share count has trended steadily higher, reflecting sustained net issuance, while US share count has been broadly stable to declining, reflecting structural net buybacks.

The implications of this trend are straightforward. If aggregate net income grows while the share base expands, earnings-per-share (EPS) growth is diluted. If share count contracts, EPS compounds faster than underlying profits. Over long horizons, this mechanical difference materially affects total returns.

This structural dilution has been a persistent headwind for EM investors. Even when operating earnings improved, per-share outcomes frequently lagged. The long-standing valuation discount of EM relative to developed markets must be viewed through this lens.

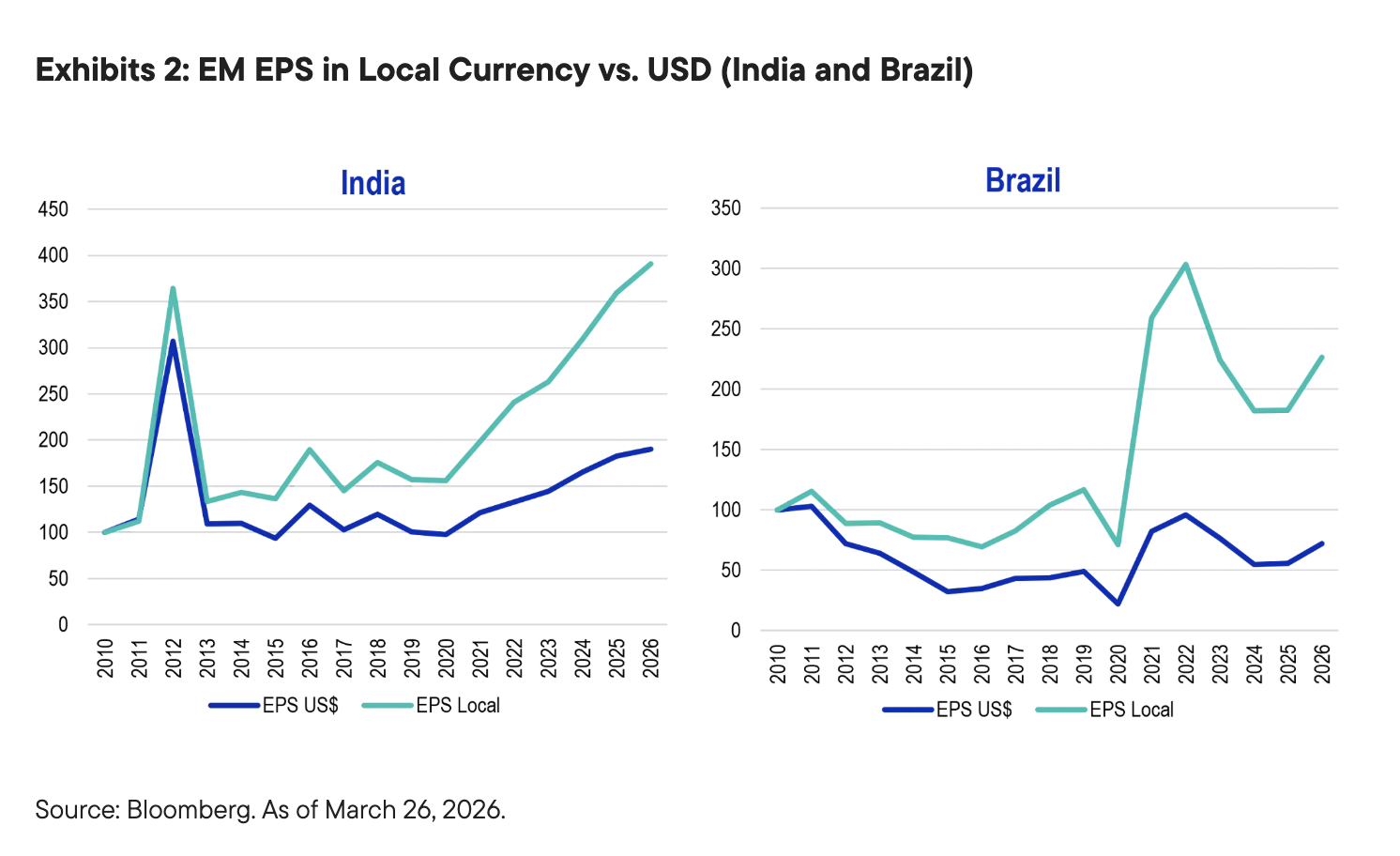

It is also important to distinguish between local currency earnings and what a US dollar (USD)-based investor ultimately experiences. Over the past two decades, EM corporate profitability in local currency terms has grown materially. However, EPS in USD terms has diverged sharply from that trajectory. The gap reflects two forces operating simultaneously: persistent share-count expansion and sustained USD strength against EM currencies. Even when underlying businesses delivered comparable aggregate earnings growth to developed markets, the translation into USD terms, combined with an expanding share base, meant that per-share USD earnings failed to keep pace.

This distinction is critical, as relative operating performance between EM and the United States has not always been as wide as relative USD EPS performance might suggest. For extended periods, non-diluted earnings growth was broadly comparable, with the divergence emerging at the per-share, USD-translated level. In effect, EM investors faced a double drag: currency translation and dilution.

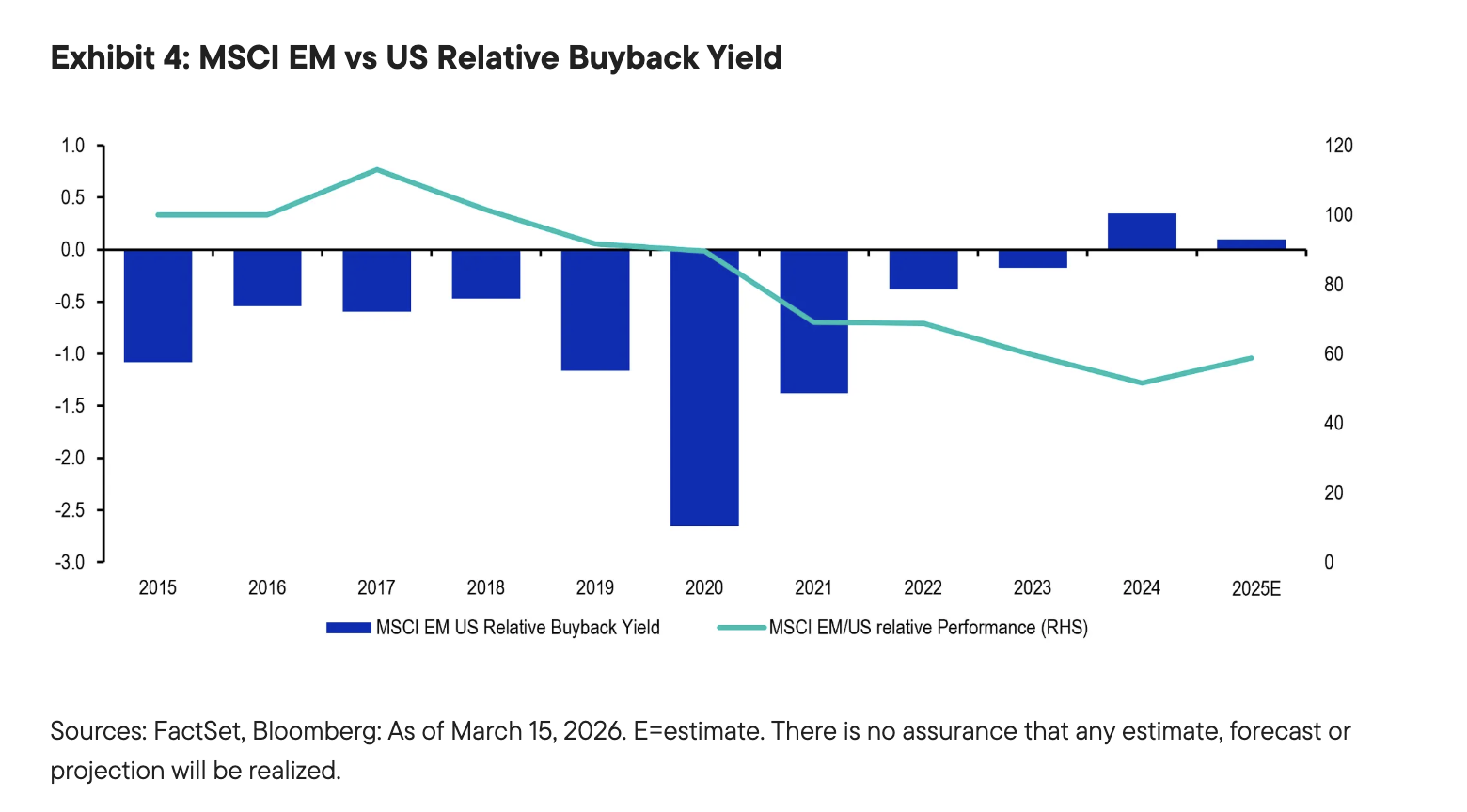

While currency cycles remain inherently difficult to forecast, a sustained shift from net issuance toward net buybacks directly addresses one of these structural headwinds. Recent data suggest that such a shift may be underway.

China as the marginal driver of change

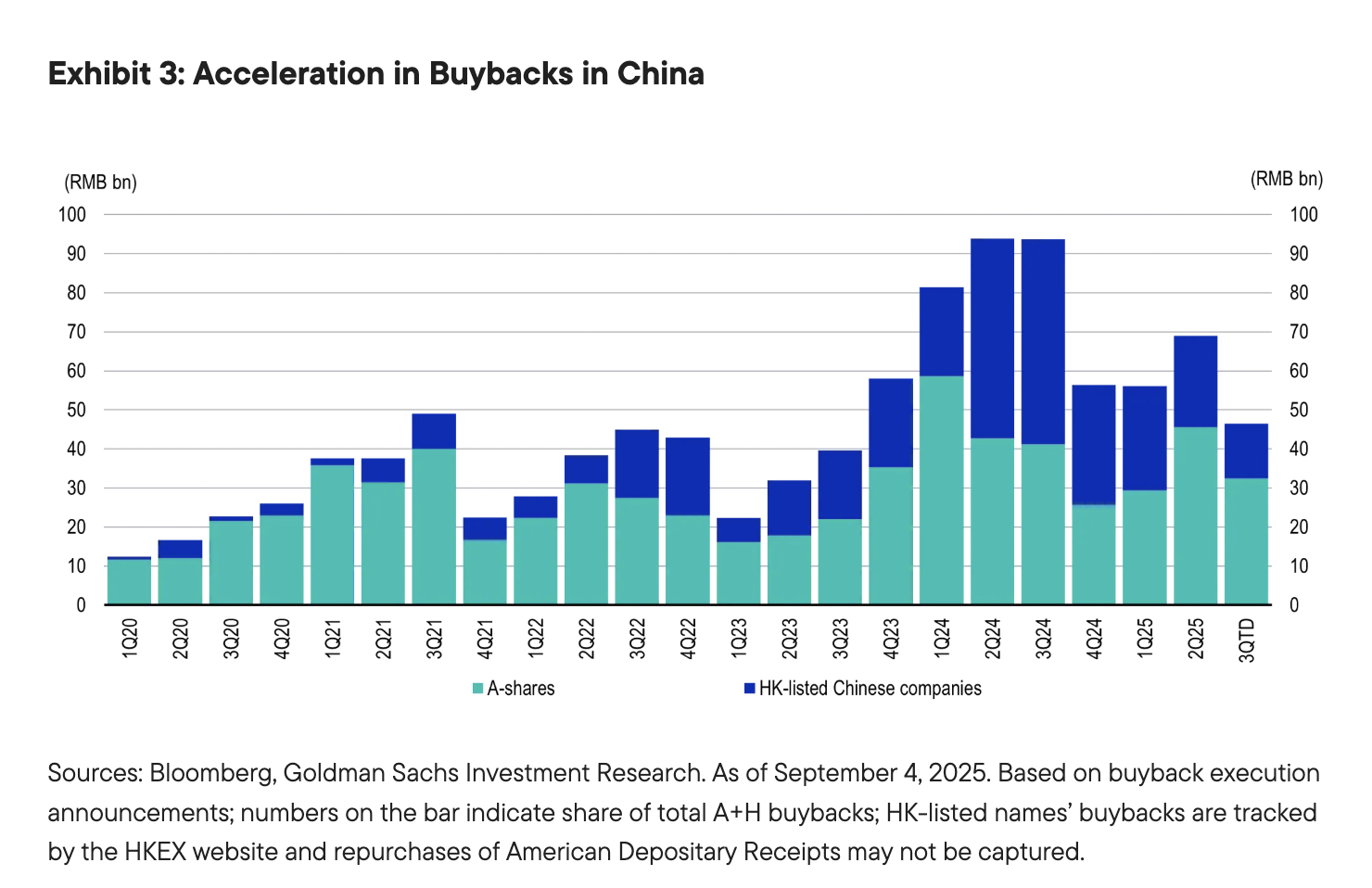

The most visible inflection is occurring within China’s large-cap internet and ecommerce platforms.

Exhibit 3 shows a sharp rise in buyback amounts across major China technology companies in recent years. The step-up is meaningful relative to prior periods and coincides with a measurable decline in outstanding shares.

Since these firms carry significant weight in the MSCI EM Index, their capital allocation decisions disproportionately influence the index’s net buyback yield. A shift from net issuance to sustained buybacks at this scale alters the index-level share count trajectory.

The question is not whether buybacks have increased—the data clearly confirm that they have—but whether this reflects a cyclical deployment of excess cash or a structural shift in capital discipline.

Broadening the narrative: Korea’s push for shareholder returns

While China has been the most visible driver of improving buyback activity, it is not the only market where capital allocation behavior is evolving.

South Korea has also begun to show early signs of a structural shift toward improved shareholder returns. Policy initiatives such as the government’s “Corporate Value-Up Program,” alongside increasing pressure on corporates to enhance capital efficiency, are encouraging higher payouts, improved return on equity and more disciplined capital allocation. While still at an early stage, the direction of travel is notable given the country’s historically low payout ratios and persistent valuation discount.

Importantly, this shift is being driven not only by corporate balance sheet strength but also by a broader policy and governance framework aimed at improving market quality. In contrast to China, where the buyback story is more company-led and subject to investment trade-offs, South Korea’s evolution reflects a more coordinated push toward shareholder alignment.

Taken together, developments in China and South Korea (two of the largest weights in EM indexes) suggest that the improvement in capital return behavior is not isolated, but may be part of a broader shift across key markets.

Assessing sustainability

Several fundamental observations support the case that the shift may be structural.

First, balance sheets across the major internet platforms remain strong. Many companies are still in positive net cash positions, providing flexibility to fund both investment and shareholder returns.

Second, core businesses continue to generate cash flow. With the notable exception of specific competitive segments such as food delivery, most large platforms remain profitable and cash generative even in a subdued macro environment.

Third, it is notable that the buyback acceleration is occurring while the broader Chinese economy remains near cyclical lows. Capital return programs are often associated with peak-cycle excess profits. In this case, they are being implemented during stabilization rather than exuberance. If growth improves, incremental free cash flow capacity could expand further.

While we believe the underlying fundamentals are supportive, there are still variables to monitor. Investment intensity in AI and related technologies is rising. The pace of increase in capital expenditure will determine whether companies can simultaneously fund innovation and maintain elevated buybacks. A material acceleration in strategic investment could, at the margin, moderate capital return momentum. Recent trends already suggest some moderation in buyback activity among large China internet platform companies, as capital is increasingly being deployed toward AI-related investment.

At present, financial capacity does not appear to be the binding constraint; the more relevant risk lies in potential strategic reprioritization of capital toward investment rather than shareholder returns. From a relative perspective, this dynamic may not be unique to EM, as US large-cap technology companies are also increasing investment in AI. However, the net impact will depend on the balance between reinvestment and capital return across markets.

Regional nuance and risks

The improvement in capital return behavior is not yet uniform across EMs. While large-cap China internet platforms have shifted decisively toward buybacks, equity issuance remains active elsewhere. Initial public offering pipelines in India and parts of the Association of Southeast Asian Nations remain robust, and secondary issuance has not disappeared. In several markets, equity continues to be an important funding channel for growth and balance sheet expansion.

The durability of the shift therefore depends on whether the behavioral change broadens beyond a handful of mega-cap names. It also depends on investment intensity. A sustained acceleration in AI-related capital expenditure, renewed competitive pressures or policy shifts could reorient cash deployment toward growth rather than shareholder return. While financial capacity appears ample, strategic reprioritization remains the key risk variable.

Additionally, share-based compensation remains an area of concern, particularly in China. The continued use of restricted stock units to reward senior management can act as a source of ongoing dilution, potentially offsetting the impact of buybacks at the aggregate level. More importantly, elevated reliance on equity-based compensation may reflect weaker corporate governance and create misalignment between management incentives and shareholder returns.

However, with both China and South Korea—together representing a substantial portion of EM indexes—showing signs of improved capital discipline, the direction of travel at the index level is increasingly relevant.

Implications for EM equities

If positive net buyback yield becomes a structural feature in EMs, several investment implications follow:

- Greater consistency in EPS growth

- Improved return on equity stability

- Greater alignment between aggregate profit growth and shareholder outcomes

- Potential narrowing of the valuation gap versus developed markets

This does not eliminate macro or policy risks. Nor does it imply uniform improvement across all EM regions. The shift is currently most visible in China’s internet sector and remains uneven elsewhere.

However, in our opinion, the combination of strong balance sheets, resilient cash generation and buybacks implemented at cyclical lows strengthens the case that this may represent more than opportunistic capital deployment.

Conclusion

Emerging markets have long been characterized by expansion of the share base rather than contraction. Exhibit 1 captures the structural divergence that constrained per-share growth. Exhibit 3 suggests that, at least in key segments, this pattern may be reversing, with developments in both China and South Korea pointing toward a potential shift in capital allocation behavior.

The durability of the trend will depend on investment intensity and strategic priorities. Yet current financial conditions provide ample buffer for continued capital return.

The central question for EMs is no longer the growth opportunity, but whether that growth accrues to shareholders on a per-share basis. Given the combined weight of these markets within EM portfolios, even incremental improvements in capital discipline could have a meaningful impact on aggregate index-level earnings quality. If capital discipline persists, we believe the long-run compounding profile of the asset class could improve meaningfully.

Index Definitions

Past performance is not an indicator or a guarantee of future performance. Indexes are unmanaged and one cannot invest directly in an index. Important data provider notices and terms available at www.franklintempletondatasources.com.

- The MSCI EM Index is a free float-adjusted, market capitalization-weighted index designed to measure the equity market performance of global emerging markets.

- The MSCI US Index is designed to broadly and fairly represent the full diversity of business activities in the United States.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries. There are special risks associated with investments in China, Hong Kong and Taiwan, including less liquidity, expropriation, confiscatory taxation, international trade tensions, nationalization, and exchange control regulations and rapid inflation, all of which can negatively impact a portfolio. Investments in Hong Kong and Taiwan could be adversely affected by its political and economic relationship with China.

WF: 9648461

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments