2026 Q1 Market Recap & 2Q Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsA geopolitical shock in the Middle East sent oil prices surging more than +70% in Q1, erasing all expected Fed rate cuts and testing how well-diversified portfolios actually were. For many investors, the answer was: considerably better than the S&P 500’s -4.3% return suggests.

KEY POINTS

The Quarter Oil Changed Everything

- Oil at $100. The Strait of Hormuz closure sent crude prices up more than +70% in Q1, raising inflation concerns and erasing all expected Fed rate cuts for 2026.

- Diversification worked. The equal-weight S&P 500 and Russell 2000 each gained roughly 1% while the cap-weighted index fell 4.3% (largely helped by a nearly 3% final day of the quarter rally). A real-world test of why concentrated portfolios carry meaningful risk.

- Rate cuts are off the table. Markets shifted from pricing two to three cuts by year-end to pricing zero, with a potential hike being discussed by quarter-end; Q2 inflation data will determine the Fed’s next move.

- AI is repricing. Software stocks fell nearly 30% (one of the largest non-recessionary drawdowns) from their October peak as AI shifted from productivity tool to potential industry disruptor.

-

Earnings still rising. Despite the market’s decline, analyst earnings estimates continue to climb, an important distinction between a volatility-driven correction and the start of a fundamental downturn.

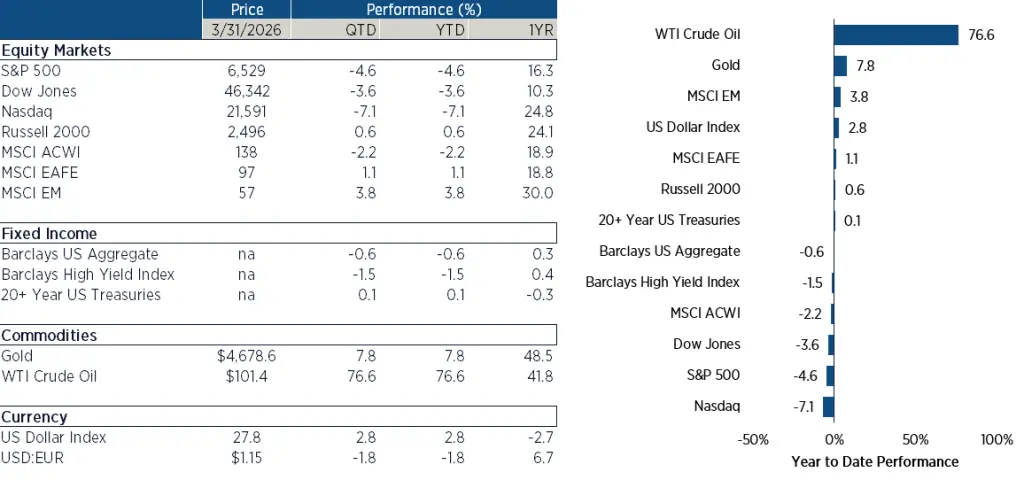

Exhibit 1:

Key Markets Performance through March 31, 2026

One Shock, Two Very Different Markets

For markets, the start of 2026 has a clear before and after. Through February, the broad market setup had been encouraging: market breadth was widening as mega-cap technology lagged and the average stock quietly outperformed the index, manufacturing data was showing signs of life, and a market rotation that many investors had been waiting on was finally underway. In fact, January posted a modest gain for the S&P 500, and the broader picture beneath the surface was meaningfully better than any single index return suggested.

Everything then changed in March with the US-Iran war.

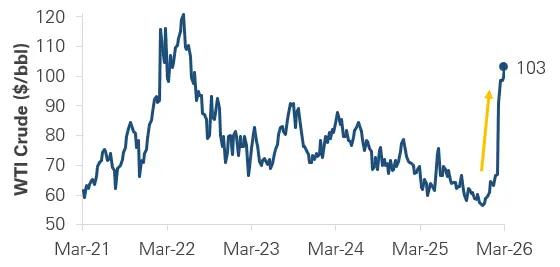

Almost immediately after the war started the Strait of Hormuz effectively closed, cutting off roughly 20% of the global oil supply. And with this closure the global economic outlook, and markets, changed entirely. Crude oil surged nearly 50% in March and finished the quarter up more than 70% to near $100 per barrel.

Exhibit 2:

Oil Prices (March 2021 – March 2026)

Equity and bond markets experienced steep drawdowns, with nearly every sector but energy teetering on correction. But the more lasting effect may be on the inflation and Fed policy outlook. At the start of 2026, markets expected two to three rate cuts by year-end. After the events of March, not only have these cuts been completely priced out, but rate hike speculation is once again back.

Heading into 2Q, the economic outlook hinges almost entirely on one question: how long does the Strait of Hormuz stay closed. While this is likely to cause significant near-term volatility (both up and down as negotiations progress), ultimately we remain constructive on equities and risk assets. As we talked about at the beginning of the year, “Returns need to be earned.” And so far they have. Earnings estimates are still rising even as prices have fallen, and that distinction suggests economic momentum is still strong. While near-term noise and geopolitical events are troubling, we continue to see strength in the US economy and maintain a risk-on view of markets.

The Economy and Markets

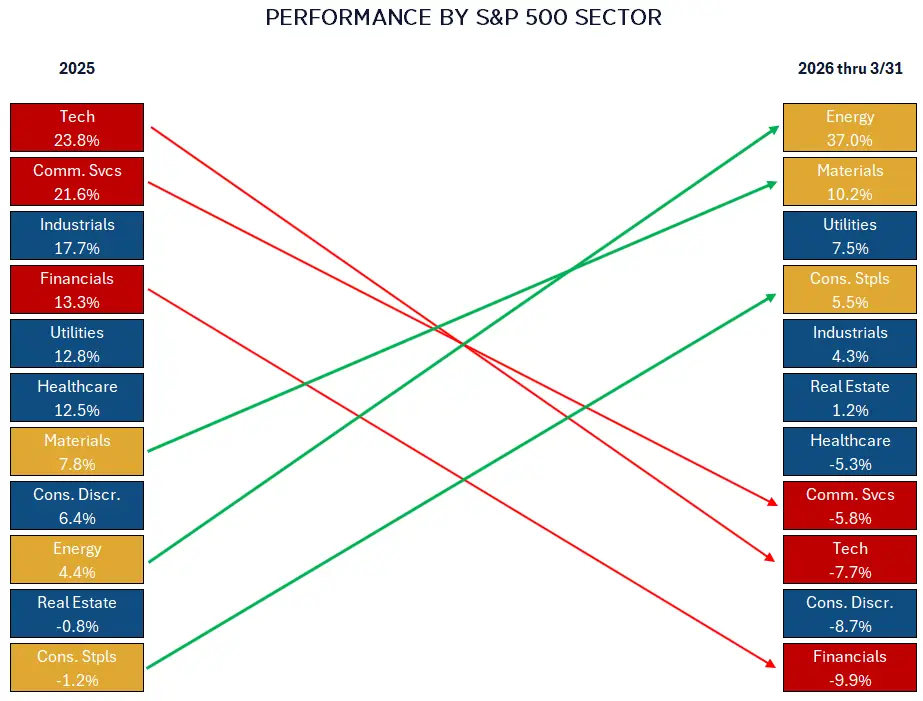

- The S&P 500 fell 4.3% in Q1, but the picture beneath the surface told a very different story. Energy led all sectors with a +38% return while Technology, Financials, and Consumer Discretionary each fell more than 9% (a 45%+ spread). Value beat growth by more than 12%, and the Russell 2000 finished up nearly 1% as six of eleven sectors outperformed the broad index in a quarter where the headline number badly misrepresented what actually happened beneath the surface.

Exhibit 3:

Performance by S&P 500 Sector

- The bond market finished roughly flat, ending a four-quarter streak of positive returns. The 10-year Treasury yield rose to 4.32%, its highest since June 2025, as markets aggressively repriced Fed rate cut expectations. High yield spreads widened to their highest level since early 2025, though they remain well below recessionary levels, which suggests markets are cautious, not stressed.

- International equities outperformed U.S. stocks for a second consecutive quarter, gaining roughly 1% vs. the S&P 500’s 4.3% decline. Emerging markets returned -0.1%, with Latin America holding up on rising energy prices. Developed markets returned -1.1%, with Europe and Asia weighed down by their heavier reliance on Middle Eastern energy imports.

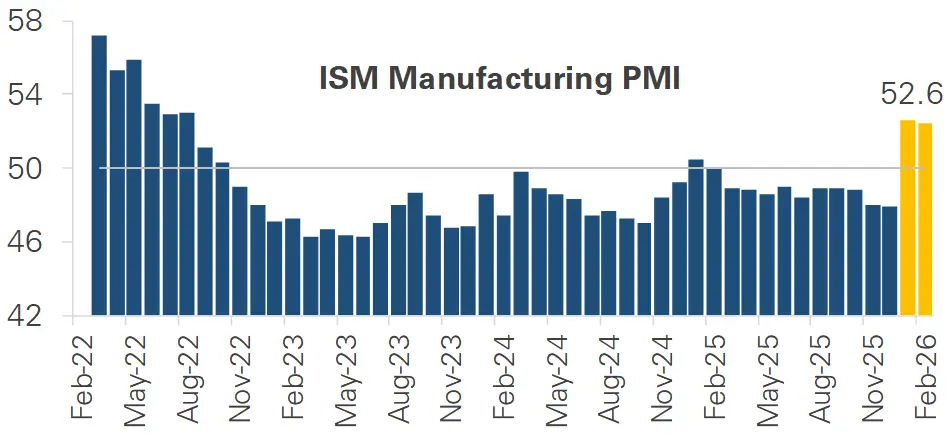

- The ISM Manufacturing Index crossed back above 50 in February – its first expansion reading in nearly a year. The Industrials sector reflected the improvement, setting a new all-time high in late February before the March sell-off. Since Q1 data covers activity largely through February, the manufacturing sector entered the conflict with underlying momentum, and the upcoming ISM releases will be the first real read on whether that held through March.

Exhibit 4:

ISM Manufacturing Data

TIMELY TOP

ICS

AI’s Reckoning: The Disruption Trade Becomes the Disrupted

For the past two years, AI was a productivity story – tools that helped existing companies do more with less. And more importantly, its implications were wrapped around bubble concerns that what AI could actually “do” was theoretical, and couldn’t truly drive bottom line earnings improvement.

That narrative shifted in January and February as multiple product launches changed how investors, and corporate users, view the technology. Two important things happened:

- First, investors started to realize that the AI “hype” was real and that these tools would be sticking around.

- Second, markets realized that rather than an efficiency layer on top of existing business models, AI had the potential to be a replacement for entire categories of professional services. That’s a fundamentally different valuation story, and the market repriced accordingly.

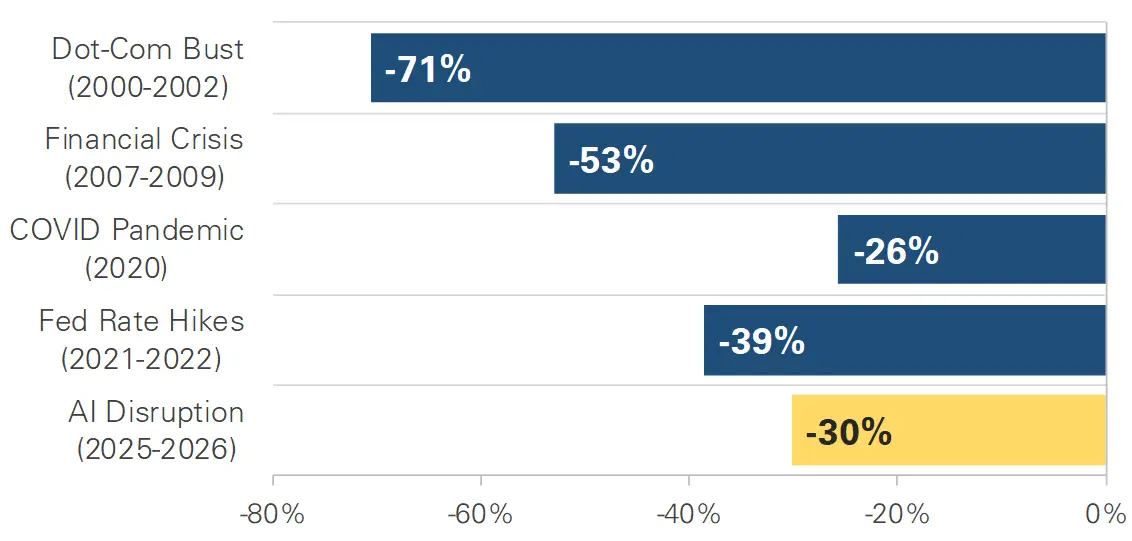

Software stocks have now fallen nearly 30% from their October 2025 peak – one of the largest non-recessionary drawdowns in the sector’s history (and more than their COVID decline). The only larger declines came during the dot-com bust and 2008 financial crisis, both actual recessions. The market hasn’t settled on how AI will reshape the enterprise software business model, and until it does, this volatility is likely to continue. For portfolios, the Q1 experience reinforced a straightforward lesson: diversification matters. Concentrated exposure to any theme, even one that’s been right for two years, carries real risk when the narrative shifts.

Exhibit 5:

Software Stock Performance

Q2 2026 Investment Outlook: What to Watch

The connection between oil prices, inflation, and Fed policy is the single thread that tied Q1 together and will likely do the same in Q2. Looking ahead, markets are intently focused on the situation in the Middle East and its direct impact on oil prices. As of this writing, the Strait of Hormuz remains closed, with negotiations ongoing. Interestingly, while current oil prices hold near $100 per barrel, December Brent futures contracts have come down to $81, suggesting undercurrents of optimism.

In our view, any progress toward reopening the Strait would likely ease energy costs, reduce inflation pressure, and give the Federal Reserve more flexibility on interest rate policy. The longer the disruption, and higher oil prices, the more their impact works into the economy, which will likely affect spending, investment, and ultimately the robust corporate earnings supporting market momentum.

Near-term, we will be closely watching the April and May inflation reports, both of which we expect will impact the Fed’s posture and investors’ view on risk assets.

One thing worth keeping in perspective amid the noise: earnings estimates are still rising. Analysts continue to expect earnings growth in the coming quarters, and profit margins remain healthy. In fact, the recent decline can almost entirely be attributed to multiple contraction due to uncertainty around oil, inflation, and Fed policy – not deteriorating fundamentals. Any reversal in that uncertainty will likely be perceived quickly by markets.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All