U.S. Employment Volatility Masks Structural Shift

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsU.S. headline employment rebounded strongly in March, posting the largest monthly gain since late 2024. The jobs rebound, which was broad-based across industries, was a welcome sign after February’s data showed a sharp decline not usually seen outside of recessions. Weather-related disruptions and a healthcare workers’ strike likely contributed to the monthly volatility.

Beneath these swings, however, we’re seeing a more consequential shift: Structural changes in the U.S. labor market are changing the composition of U.S. real GDP growth – and therefore changing how we should interpret labor market data when assessing the broader health of the economy.

More restrictive U.S. immigration policies along with long-running demographic trends are reducing labor supply growth and employment trends essentially to zero. This means that the U.S. economy now relies solely on real productivity growth to maintain its 1.5% to 2% trend in overall GDP growth – an unprecedented dynamic.

In the near term, stagnant labor force growth will likely provide a strong incentive for businesses to invest in labor-saving technology. Indeed, AI investment and implementation accelerated dramatically in 2025, and investment trends are likely to remain strong. In terms of monetary policy, weaker headline payrolls figures aren’t likely to garner the reaction they have in the recent past, as larger and more sustained employment contractions are now needed to increase the unemployment rate.

Over the medium term, economic growth may largely depend on how quickly and effectively AI implementation can contribute to sustainably higher productivity growth. At this point, AI’s trajectory is an open question. Without a significant boost from AI, stagnant labor force trends could eventually lead to lower investment, slower growth, and lower rates.

Declining size of the U.S. labor force

At its most basic level, real GDP growth can be broken down into two factors – growth in aggregate hours of employed labor (which depends on population and labor force trends) and the productivity of workers during their hours worked. Changes in labor force growth – or those individuals who are currently employed or looking for a job – will have important implications for broader growth trends.

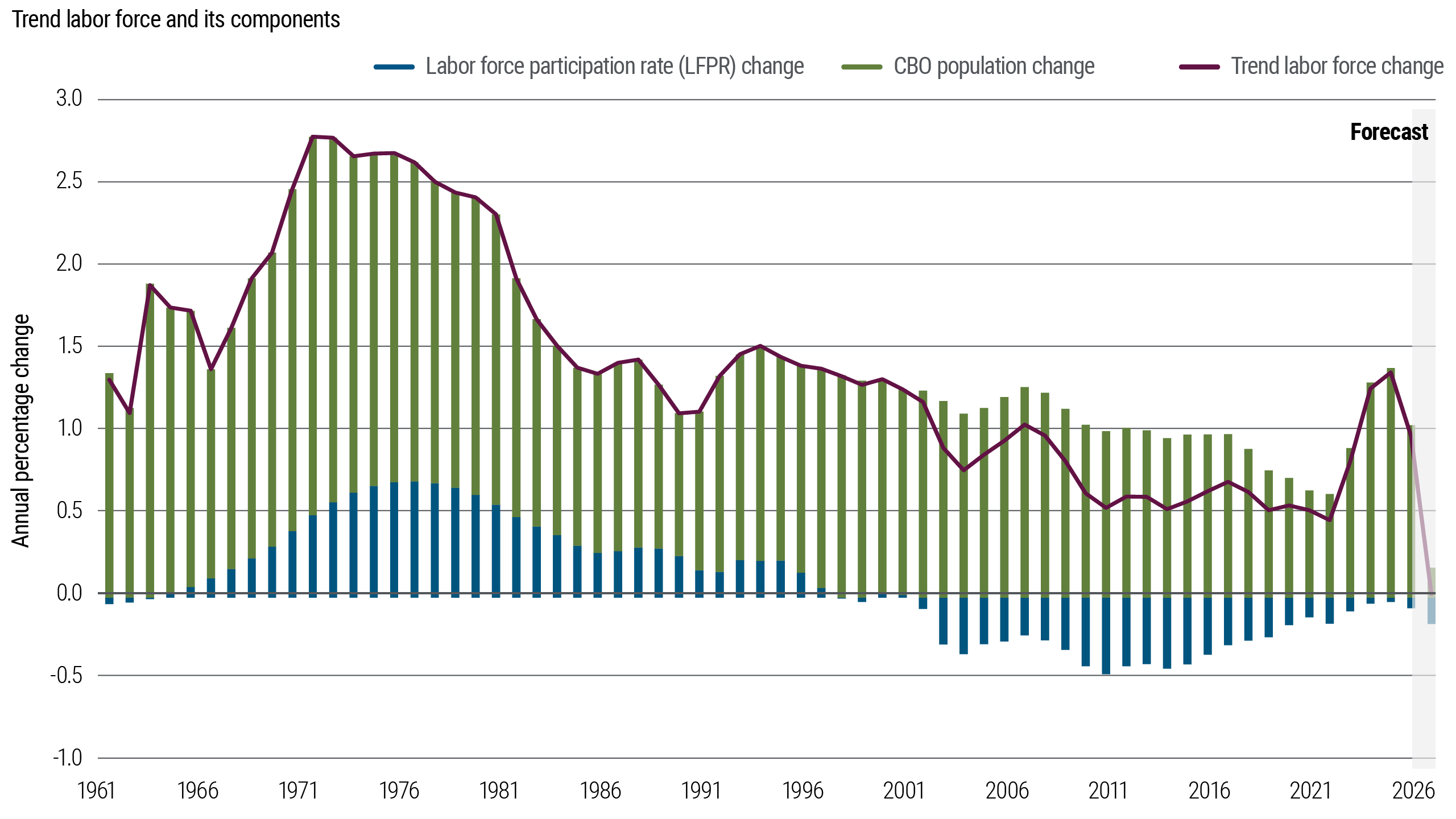

Since the 1960s, trend labor force growth in the U.S. has shifted due to demographic trends. At its peak in the 1970s, trend labor force growth was 2%–3% per year as more women joined the workforce and as both men and women from the post-WWII baby boom reached working age. Since then, labor force growth has slowly declined along with fertility rates, and the aging population has meant more retired workers – see Figure 1.

Figure 1: Size of the U.S. labor force resumes its long-term decline

These demographic trends left the U.S. increasingly reliant on net immigration to sustain labor force expansion. Over the past decade, foreign‑born workers accounted for roughly half to two‑thirds of net U.S. labor force and employment growth – nearly all of it in the post‑pandemic period.

Humanitarian immigration – mainly asylum seekers – surged in the wake of the pandemic and contributed to a reacceleration in U.S. labor force growth from 2022 to 2024. More recent policy changes have not only reduced the inflows of immigrants, but also increased the outflows. Research by Wendy Edelberg and other labor economists at Brookings1 has found that net migration was likely close to zero or negative over calendar year 2025 and is very likely to be net negative in 2026.

Changing U.S. growth composition

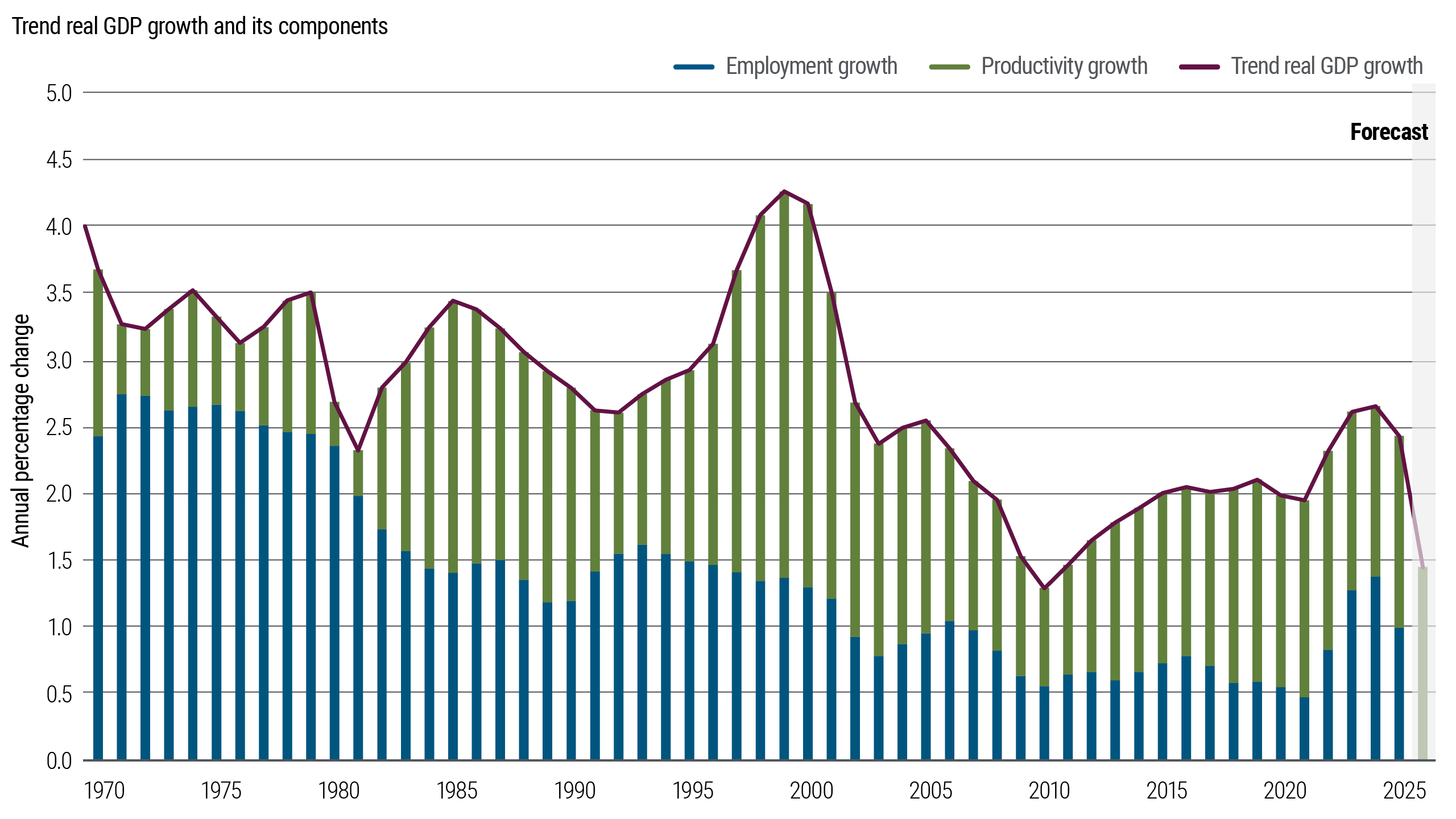

Unless immigration policy returns to a less restrictive stance, labor force growth will likely remain stagnant or even decline. Recent Federal Reserve staff research2 highlights two important implications: First, near-zero labor force growth implies that average monthly job gains needed to keep the unemployment rate stable are also near zero – making negative job growth as likely as positive in any given month. Second, growth in potential GDP is likely to depend entirely on productivity gains.

In its latest economic outlook, the U.S. Congressional Budget Office (CBO) projected the trend in productivity growth to be 1.5%, while under pre-pandemic immigration policies the trend labor force growth was 0.5%. Combining these components left trend real GDP growth at 2%. If labor force growth is now zero, that should mechanically lower trend GDP growth as well – see Figure 2.

Figure 2: Productivity could become the main driver of overall real U.S. GDP growth

Why the productivity offset is not automatic

It may not be as simple as adjusting trend growth down by the now lower contribution of the labor force. An economy generating moderate productivity growth with little or no labor force expansion would be historically rare, in part because labor and capital trends are linked in two important ways:

First, production of goods and services requires both people and tools. Capital makes labor productive and labor makes capital useful. More specifically, people (labor) do the work, but how much they can produce depends on the tools, machines, software, and structures they have to work with (capital). Higher productivity growth requires continued investment in capital per worker, but the extent to which labor makes capital useful tends to diminish at higher levels of investment. As a result, stagnant labor force growth could eventually slow investment and productivity trends.

Second, the economy needs a stream of new ideas to guide productivity-enhancing investments, and people generate those ideas. As Paul Romer asserted in his 1990 paper,3 new ideas are the heart of economic growth because ideas are “non-rival” – no matter how many people use the idea, there is not less of the idea to go around. If more people are participating in the labor market, then there are more people who can use old ideas to create new ones, which in turn can drive investment and future productivity. With fewer people, the pace of innovation could slow, reducing investment in future productivity growth.

Artificial intelligence to the rescue?

AI offers the potential to support continued innovation that drives investment and future productivity growth, despite a stagnant labor force. Unlike past technologies that have given humans faster and better tools, AI also has the potential to replace humans across a range of tasks, including new idea generation. To the extent that AI is a substitute for labor (in addition to complementing it), it could also at least in theory drive sustainably stronger capital deepening trends for a time.

Companies are racing to implement AI in hopes of transforming their businesses in ways that increase productivity and efficiency. However, the timing and magnitude of the productivity gains are highly uncertain. In the near term, if AI-driven productivity is slow to materialize, then consensus expectations for above 2% U.S. growth over the next several years are likely too high. In the medium term, low labor supply increases the burden on AI (or other technologies) to maintain recent trend growth levels.

Bottom line

With labor force growth grinding to a halt, job gains no longer carry the same signal they once did. Investors should expect the frequency of monthly employment contractions to increase as the U.S. job market adjusts to limited labor supply.

The U.S. economy is increasingly reliant on productivity. That makes AI not just a cyclical force, but a structural one that shapes investment, productivity, and long-run growth prospects.

For the medium-term outlook, this is yet another layer of uncertainty that increases the attractiveness of high quality bonds as a generally stable source of income and store of value.

Read our views on the global economy and markets in our latest Cyclical Outlook, “Layered Uncertainty: Conflict, Credit Stress, and AI.”

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Footnotes

1 Wendy Edelberg, Stan Veuger, and Tara Watson, “Macroeconomic implications of immigration flows in 2025 and 2026: January 2026 update.” Brookings Institution research (13 January 2026). ↩

2 Seth Murray and Ivan Vidangos, “Labor force growth, breakeven employment, and potential GDP growth.” Federal Reserve economic research / FEDS Notes (2 April 2026). ↩

3 Paul M. Romer, “Endogenous Technological Change.” The Journal of Political Economy 98.5, Part 2 (October 1990): S71–S102. ↩

Disclosures

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

Pacific Investment Management Company LLC (“PIMCO”) is an investment adviser registered with the U.S. Securities and Exchange Commission (“SEC”). PIMCO Investments LLC (“PIMCO Investments”) is a broker-dealer registered with the SEC and member of the Financial Industry Regulatory Authority, Inc. (“FINRA”). PIMCO and PIMCO Investments is solely responsible for its content. PIMCO Investments is the distributor of PIMCO investment products, and any PIMCO Content relating to those investment products is the sole responsibility of PIMCO Investments.

The information provided herein is not directed at any investor or category of investors and is provided solely as general information about our products and services and to otherwise provide general investment education. No information contained herein should be regarded as a suggestion to engage in or refrain from any investment-related course of action as none of PIMCO nor any of its affiliates is undertaking to provide investment advice, act as an adviser to any plan or entity subject to the Employee Retirement Income Security Act of 1974, as amended, individual retirement account or individual retirement annuity, or give advice in a fiduciary capacity with respect to the materials presented herein. If you are an individual retirement investor, contact your financial advisor or other fiduciary unrelated to PIMCO about whether any given investment idea, strategy, product or service described herein may be appropriate for your circumstances.

Check the background of this firm on FINRA's BrokerCheck.

PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world. ©2026 PIMCO. All Rights Reserved. Investment Products: NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All