What’s Going on in Private Credit?

Membership required

Membership is now required to use this feature. To learn more:

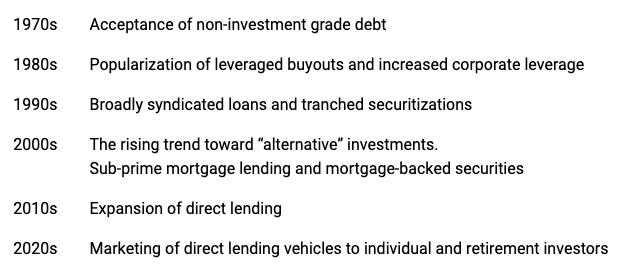

View Membership BenefitsThe general field called “credit” has seen massive innovation over the course of my career. Its popularity has increased steadily, and its scale and role in the world of finance have multiplied. The other day, an Oaktree colleague asked me about the developments that brought the credit sector to where it is today. I came up with the following list:

Time of Inception

The investment world I first encountered in the summer of 1968, consisting exclusively of stocks and high-grade bonds, seems quaint and provincial in retrospect given the developments listed above. These advances have transformed the investment management business, and Oaktree and its clients have been major beneficiaries. All the changes listed above involved – or were facilitated by – the thing now broadly called “credit” – essentially non-government debt. I’ll lay out a brief chronology to set the scene.

Prior to 1977-78, it was virtually impossible for a company lacking an investment grade credit rating (BBB or above) to issue bonds publicly. The speculative-grade debt that did exist was primarily that of previously investment grade companies that had run into trouble and been downgraded, so-called “fallen angels.” Companies lacking investment grade ratings were generally limited to taking out bank loans or borrowing from insurance companies through “private placements.” Michael Milken is generally credited with the idea, implemented in the late 1970s, that non-investment grade companies should be able to issue bonds if their interest rates are high enough to compensate for the risk of default. This kind of “risk/ return thinking” helped enable the development of today’s U.S. high yield bond market of roughly $1.5 trillion, along with most of the other developments under discussion here.

A few small leveraged buyouts took place in the mid-1970s, but the popularization of high yield bonds in the 1980s enabled LBO funds, small companies, and “takeover artists” to borrow enough money to acquire much larger companies than was previously possible. That led to a massive expansion of LBOs, creating the industry that renamed itself “private equity” in the 1990s.

The idea of pooling debt instruments and selling off tranches with varying seniority, risk, and thus interest rates began with the creation of mortgage-backed securities in the 1970s – most often associated with Louis Ranieri of Salomon Brothers – and expanded in the 1980s and ’90s.

Prior to the 1990s, banks made loans – some of them to non-investment grade companies – and “syndicated” them to a handful of fellow banks. But then “broadly syndicated loans,” “leveraged loans,” or “senior loans” were developed by Wall Street. They were sold to institutional investors in large amounts, growing to today’s market of roughly $1.5 trillion in the U.S. The significant increase in the ability to issue this type of financing helped fuel the growth of private equity.

After the tech bubble of the late 1990s imploded in 2000, leading to the first three-year decline in the S&P stock index since the Great Depression, investors became uninterested in the stock market and stayed that way for a decade. And when central banks reduced interest rates to fight the resulting economic and market malaise, investors sought returns above those available on bonds. With stocks and bonds out of favor, investors looked for a new solution. They turned to hedge funds and private equity, which had held up relatively well, and the label “alternative investments” was born. Hedge funds couldn’t find enough bargain-priced opportunities to accommodate large amounts of institutional capital, so many investors gravitated toward private equity as the solution du jour. The first $10 billion private equity funds were organized.

Around the same time, corporate debt began to be securitized in “structured credit” vehicles such as collateralized loan obligations, or CLOs. The banks that packaged these vehicles, with internal leverage from “tranching,” found eager buyers for both the high-yielding junior classes and the overcollateralized senior classes. The strong demand for CLOs and the profits available from structuring them created a need for loans to securitize, leading to increased issuance of broadly syndicated loans.

Many of the same banks packaged subprime mortgage loans extended to questionable borrowers into residential mortgage-backed securities, or “RMBS.” Remarkably, the bankers were able to obtain thousands of triple-A ratings on RMBS backed by “liar loans.” When the highly flawed nature of these loans and structures came to light, the result was the Global Financial Crisis of 2008-09.

The GFC ended with the banks poorer, chastened, and re-regulated, and as a result there weren’t enough bank loans available to meet the needs of the burgeoning private equity industry. Investment managers moved to fill the vacuum through non-bank lending or “private credit.” The fastest-growing component was “direct lending”: private loans to mid-market, private-equity-sponsored portfolio companies with sub-investment grade ratings. (Please note: “private credit” and “direct lending” aren’t synonymous; the latter is a subset of the former. The many stories mentioning private credit these days are really about direct lending. I’ll try here to be conscientious about making the distinction; most who comment aren’t.)

Most recently, it has become popular to market investment vehicles holding direct loans to individual investors and retirement accounts. This increased the capital available for direct lending and ballooned the assets under management of managers who scooped it up.

The Normal Pattern

Extreme upsurges in the popularity of novel forms of investment – those commonly labeled “bubbles” – invariably have certain features in common:

- The essential element is newness. When something is new, (a) it’s easy for its proponents to stimulate interest from buyers by touting its merits and (b) since it’s never been tested, its flaws have yet to come to light. This allows investment fads to grow into bubbles.

- Usually there’s a grain of truth. The Nifty Fifty were great companies. The internet and digital communication did change the world. And mortgages are usually safe for investment. These truths provided the basis for what eventually grew into highly destructive bubbles.

- Early investment in the new thing is often rewarding, since those who get in at the beginning do so at a price that hasn’t yet been elevated by rising popularity.

- The success of early investors makes those on the outside envious, convincing them to join the party. As Charles P. Kindleberger wrote in Manias, Panics, and Crashes: A History of Financial Crises, “There is nothing so disturbing to one’s well-being and judgment as to see a friend get rich.” Envy just might be the strongest force in the world.

- The possibility of great success inflames investors’ hopes. Possibility is confused with probability and then morphs into certainty. Skepticism and risk aversion go out the window.

- The critical question – rarely asked by investors in hot pursuit – is what price is safe to pay to participate. Envy, excitement, the dream of getting rich, and the fear of missing out are the mortal enemies of caution and reluctance to jump on the bandwagon.

-

Latecomers swallow promises, apply low standards, and push up prices, causing most investment trends to become overdone. For me, the most important investment adage of all is, “what the wise man does in the beginning, the fool does in the end.” Warren Buffett said it more colorfully: “First the innovator, then the imitator, then the idiot.”

- The flaws, potential pitfalls, and unfulfillable promises that investors readily overlook when things are going well invariably lead to disillusionment and loss when the optimism surrounding the new thing turns out to have been excessive or the prices paid simply turn out to have been too high.

When Mark Twain purportedly said, “History does not repeat itself, but it does rhyme,” this must be the kind of recurring pattern he had in mind. I consider it one of the eternal truths in investing.

Does That Apply to Direct Lending?

I think it’s fair to say aspects of this progression occurred over the last 15 years in direct lending, a part of the private credit universe:

- A new form of financing was developed.

- With banks less willing to lend, the demand for financing from private equity exceeded the supply. That allowed the early direct lenders to demand high interest rates and strong protections through robust loan documents.

- The low interest rates of the 2010s made the higher prospective returns on direct lending appear very attractive, especially given that returns could be levered through low-cost borrowing.

- Institutional investors noted the attractiveness of the early loans and joined the party.

- No doubt that attractiveness was enhanced by the fact that private loans don’t exhibit much price volatility, since there’s no market for them to mark to. That might have let their advocates say, “They’ll deliver high risk-adjusted returns,” but it wasn’t right. They could reasonably have been expected to deliver high volatility-adjusted returns (that’s what Sharpe ratios are), but I insist strenuously that risk and volatility aren’t the same thing. Direct loans embody no less credit risk than liquid credit instruments such as high yield bonds and broadly syndicated loans. It just isn’t reflected as readily in prices.

- Hundreds of investment firms offered their services in direct lending, the vast majority of which entered the private credit market after the end of the Global Financial Crisis, meaning they’d never been tested in rough times. Regardless, they were given plenty of money to manage.

- The arrival of many new managers and a great deal of incremental capital caused lenders to compete to make direct loans by accepting lower yields, narrower yield spreads, and reduced safety. Some managers were doubtless motivated to lower their standards in order to put a lot of capital to work.

- The benign economic and investment environment that generally prevailed during the 17 years since the end of the GFC made direct loans successful, despite signs of weakening underwriting standards, allowing these trends to become more and more pronounced. The sum of the above facilitated the sale of direct lending vehicles to individual and retirement investors hungry for return in a low-interest-rate environment.

The massive amounts of capital that have been available for investment in direct lending created a goldrush mentality. In the last 15 years, something like $2 trillion of direct loans has been made. (The whole private credit sector was only about $150 billion 20 years ago.) Thus, I imagine some direct lending managers accepted too much money and invested it too fast, applying standards that were too low and setting the scene for a correction.

In the last several months, the tide has begun to go out for direct lending (generalized to all of private credit by those who don’t make fine distinctions). To paraphrase Buffett, this created the possibility that some bare bottoms would be exposed.

As I described in my November 2025 memo, Cockroaches in the Coal Mine, two prominent bankruptcies – First Brands and Tricolor – caught credit investors by surprise in mid-2025. Both raised concerns about possible fraud, perhaps enabled by the low standards applied by lenders in good times.

This raised some concern regarding public vehicles for direct loans: business development companies, or “BDCs.” When some investors in “non-traded BDCs” wanted to withdraw their money and weren’t able to do so in full, questions began to be raised regarding liquidity. Likewise, there were questions about how these vehicles valued their private debt holdings, and thus about the accuracy of reported carrying values and the process of withdrawing from the vehicles. Perhaps as a result, the shares of “publicly traded BDCs,” which can be sold but not redeemed, came to be priced at wider discounts from their net asset values.

The preceding events were mostly treated as idiosyncratic, meaning there was no broad disillusionment or loss of confidence at the time. But it’s usually the case that if a confluence of troubling events builds up, a critical mass can eventually be reached, rendering investors no longer able to overlook the newly exposed flaws in the new thing. And that brings us to software debt.

Direct Lending and Software

Prior to the mid-2000s, investors in high yield bonds and leveraged loans were generally unwilling to lend money to technology companies, which were considered too fundamentally risky to be creditworthy. And since they couldn’t be levered, they weren’t candidates for purchase by private equity funds.

But when investment in private equity funds grew strongly, their managers needed companies to buy, and that caused them to expand the range of what they would consider. They concluded that companies with market-leading positions in essential software that was unlikely to be replaced would (a) enjoy the recurring subscription-based cash flows that can make a company bankable and (b) benefit from sustainable moats surrounding their businesses. Private equity funds began to buy software companies, and credit investors began to lend money for that purpose.

In my experience, the limiting factor in the credit markets is never borrowers’ appetite for capital, but rather lenders’ willingness to supply it. To paraphrase Kevin Costner’s character in the movie Field of Dreams, “If you provide capital, they’ll borrow and put it to work.” Thus, the makeup of the credit market was greatly influenced by the growth of private equity, the boom in capital available for direct lending, and both parties’ agreement that software companies were good candidates for investment.

In recent years, sponsors have increasingly turned to direct lending as an alternative to broadly syndicated loans, as the former allowed them to get the capital they needed from a few big lenders, freeing them from protracted road shows, widely distributed financial disclosure, and having to deal with a large number of counterparties if trouble necessitated renegotiation. Direct lenders have also shown a willingness to support higher debt levels, enabling sponsors to achieve leverage beyond what the syndicated loan market might accommodate. They’ve also been willing to lend more to companies that are not yet profitable in the form of “AAR loans” based on annual recurring revenue.

The attractiveness to sponsors of loans versus bonds and private versus public brought the representation of software debt in the U.S. sub-investment grade credit markets to roughly the following proportions:

In addition, thanks to the same factors, the percentage of software debt that is to companies that were the subject of leveraged buyouts (meaning they’re more highly levered) is higher in the broadly syndicated loan market than in the high yield bond market, and higher still in the direct lending market.

As a result of all the above, a significant portion of direct loans were made to software companies, which were often acquired at high EBITDA multiples of ~20x and with high leverage ratios. Now, suddenly, software company debt is in the news.

Over the last year or two, artificial intelligence has significantly reduced the need for humans to write code (that is, program computers or write software), largely relegating coders to instructing AI models what to do. The market for software company stocks and debt didn’t react much in 2024-25. Then, in November 2025, Anthropic released a powerful new model for coding, followed in late January by the release of 11 “plug-ins” to automate tasks in a number of fields. It seems a cognitive tipping point was reached in the first days of February. Investors finally took notice of the negatives that had accumulated, and the private credit market has faced scrutiny and volatility ever since:

- Worry about software debt made investors in semi-liquid public vehicles put in for redemptions.

- Limits on redemptions caused investors to question the safety of their investments.

- The process through which some investors got out at the stated net asset value might have caused those remaining to question whether the NAVs people exited at were overstated and if so what the impact might be on them.

- When funds limited redemptions, investors might reasonably have concluded that they should put more shares in for withdrawal next time.

The redemption limits built into the direct lending funds appear to have worked as designed so far, allowing managers to avoid fire-sale liquidations. But it would be understandable if investors reacted negatively to being told they can’t get their money out when they want.

Private Credit and Public Investors

There are two different things going on in private credit today. There are the developments in the fundamentals of borrowers and the solidity of loans, and then there are the reactions of investors. As Armen, Bob, and Craig wrote in a recent internal memo:

While these software companies are generally performing well (with a few outliers), there has been a growing concern in the market that they are at risk of significant disruption from AI, which has materially impacted their equity value and reduced the equity cushion for lenders. Today, investors are not discriminating between the potential winners and losers in the software space, and the entire sector is under pressure. . . . The disruptions and headlines are largely flow- and sentiment-driven rather than the result of credit deterioration.

Investors are rarely the informed, methodical, dispassionate weighing machine Benjamin Graham and David Dodd described in Security Analysis, and certainly not in the short run. As I wrote in my 2016 memo What Does the Market Know? in real life things fluctuate between pretty good and not so hot, but in the minds of investors they go from flawless to hopeless.

Investors initially fall in love with the new thing, swallow its promises whole, and overpay. Optimism and excitement are never conducive to skepticism, dispassionate analysis, the maintenance of appropriate risk aversion, and the insistence on high standards.

Then, when disappointment and disillusionment set in, the bravado and confidence that originally supported the investment evaporate. Now the analysis errs in the opposite direction, with excessive pessimism and skepticism replacing eagerness and gullibility, and with sheer terror replacing the blind faith that enabled investment when everything was going well.

The implications of AI for the software industry, limitations on liquidity in private assets, and uncertainty regarding the accuracy of direct lending funds’ pricing have been there for years. But, simply put, people may not have asked enough questions or paid enough attention in the good times . . . as usual.

This has led to the current discomfort of investors in direct lending vehicles. Individual investors in a new phenomenon like direct lending are unlikely to fully grasp its potential complications, especially if it has never been seen in action during tough times. The inclusion of leverage in the vehicles may have been touted as profit-enhancing, and now investors are seeing it at work in the opposite direction. And the investment vehicles’ limitations on liquidity – which may have been glossed over with a representation that “most of the time, you’ll probably be okay” – has come into play with surprising effect.

True believers make the most money in manias, and skeptics lose the least when they crash. But the key to the investment success we aim for lies in always maintaining a healthy balance between belief and doubt. As Charlie Munger used to say, quoting the ancient philosopher Demosthenes, “For that which a man wishes, that he will believe.” Most people dream of getting rich and are willing to trust when promised a way to do so without risk. But the new thing rarely pays off as expected, especially if invested in unskeptically while it’s raging.

It’s safest to stick to tried and true investments and leave the more innovative developments to experts who are able to understand and cope with the implications. But few can resist the siren song of easy profits that accompanies most untested fads. It will ever be so.

The Lessons of 1929

The best investing book I’ve read in years, one that pulled me along from chapter to chapter, is 1929: Inside the Greatest Crash in Wall Street History – and How It Shattered a Nation, by Andrew Ross Sorkin. It describes the leadup to the Great Crash of October 29, 1929, and its aftermath, and it does so not by dryly recounting the events, but through profiles of the protagonists of the day. There are a lot of lessons to be learned from 1929, along the lines of my favorite books about market excesses: A Short History of Financial Euphoria by John Kenneth Galbraith (1994) and Devil Take the Hindmost: A History of Financial Speculation by Edward Chancellor (2000).

My take from 1929 was that three things in particular were primarily responsible for the bubble that ended in the Great Crash:

- the sale of stock to the public without regard for suitability,

- the provision of heavy leverage to the buyers, and

- the mismatch between the illiquidity of the assets bought and the short-term nature of the loans that financed the purchases.

Individual investors were lured into the stock market following an ascent that had gone on for years; the major stock market averages had already risen by roughly 400% between 1921 and 1928. Brokerage firms, hungry for commissions and markups on larger transactions, provided margin loans for up to 90% of the purchase price. And those loans could be called – and the positions sold out – if a decline wiped out the investor’s 10% equity and additional cash couldn’t be posted. The story sounds familiar (and has been repeated several times since):

- A lack of financial sophistication on the part of individual investors leaves them susceptible to promotions and too-good-to-be-true promises.

- Leverage is described as capable of magnifying the fruits of success, but the corresponding downside risk is often omitted from the sales pitch.

- The perhaps-unmentioned terms of margin debt – and the difficulty of imagining the full depth of a potential market decline – expose investors to the risk of ruin.

It’s not easy to lose everything in the stock market, but the combination of these three elements can do the trick in a bad-enough boom/bust cycle.

The things described above took place in 1929 against the background of a near-total absence of laws governing the investment business, including requirements for honesty in prospectuses, and were compounded by the self-serving delusion, lack of principles, and downright venality of some Wall Street leaders. The result was a market and economic catastrophe that scarred several generations.

Sorkin mostly limits himself to chronicling his characters’ behavior, leaving the drawing of conclusions and morals until the very end. But he finishes with a punch:

The devastation wrought by the stock market’s decline – not just during the crash itself but for most of the ensuing decade – caused millions of Americans insufferable pain. It caused them to not just turn away from the market but to revile those who made their living buying and selling stocks.

Yet the forces that drove the market to such stratospheric levels – optimism, ambition, and the belief that the future could be endlessly brighter – did not disappear forever. They never do.

Ultimately, the story of 1929 is not about [interest] rates or regulation, nor about the cleverness of short sellers or the failures of bankers. It is about something far more enduring: human nature. No matter how many warnings are issued or how many laws are written, people will find new ways to believe that the good times can last forever. They will dress up hope as certainty. And in that collective fever, humanity will again and again lose its head.

The enduring lesson is not that booms can be prevented, or that busts can be fully averted. It is that we need to remember how easily we forget. The antidote to irrational exuberance is not regulation by itself, nor skepticism, but humility – the humility to know that no system is foolproof, no market fully rational, and no generation exempt. The greater the heights of our certainty, the longer and harder we fall.

Sorkin’s concluding observations capture the lessons that can be learned from the mistakes that rhyme from cycle to cycle.

What’s a Manager to Do?

In my opinion, perhaps the conscientious manager’s biggest problem arises when too much capital is being pushed into their market and investors are too eager to put it to work. I talked about this at length in my February 2007 memo, The Race to the Bottom, on the doorstep of the Global Financial Crisis (I can’t believe it’s almost 20 years old). That’s roughly when Citibank’s CEO, Chuck Prince, was moved to say, “As long as the music is playing, you’ve got to get up and dance.” What a choice for a manager: join in when feverish investors are lowering their standards in order to put money to work, or sit on the sidelines and not invest, watching as other managers pile up AUM, and likely causing clients to close their accounts in the seemingly interminable period before your skepticism and discipline finally pay off?

I never want to present Oaktree/Brookfield as the paragon of investment virtue, and I never say we’re perfect. However, superior investing doesn’t result from omniscience and perfect decision making, but rather from decisions that are better than those made by others. In truth, we’ve had defaults in our high yield bond portfolios nearly every year since I started the effort 48 years ago . . . just far fewer than most and far fewer than were allowed for by the yield spread we were paid for bearing default risk. Having said that, I want to describe where we stand with regard to private credit, direct lending, and public vehicles. I’m very proud of our performance, and I think this will be instructive.

First, we’ve been investors in high yield bonds and broadly syndicated loans since their inception decades ago, but we never went overboard in private credit. As I mentioned a year ago in my memo, Gimme Credit, whereas for a few years the most popular question has been “can we talk about private credit?” my rejoinder has been “can we talk about credit?” We insisted there was a place in portfolios for both private credit and liquid credit.

Second, we’ve been investing in private credit for decades – buying bank loans in our distressed debt funds and engaging in mezzanine lending and asset-backed lending – but we never pursued direct lending to the same extent as others. At the beginning of its existence in the early 2010s, we thought the returns from direct lending, while high in relative terms, were low in the absolute. And later, we thought the superiority in pricing and terms had been competed away by the newly arrived managers and capital, rendering it average in attractiveness, not exceptional.

For these reasons, private credit represents well under half of Oaktree’s performing credit assets, and direct lending represents less than half of our private credit book. Thus, direct lending is only around 20% of Oaktree’s investments in performing credit and less than 15% of our overall assets under management.

Third, since (a) we expanded our assets far less than many other alternative credit managers (Oaktree’s AUM “only” doubled over the last decade) and (b) direct lending was a limited part of our AUM growth, we’ve felt less pressure to invest quickly or compromise our standards. That meant we could remain highly selective, limiting the amount invested in software and restricting it to what we believe to be the best opportunities.

Our exposure to software companies across our entire credit platform is extremely small on an absolute basis and relative to peers. Most of Brookfield/Oaktree’s private credit funds operate outside of direct lending and thus have only limited holdings in software. Even our direct lending portfolios generally have limited software exposure, and over the last 12-18 months we’ve maintained a particularly high bar for participating in new software transactions.

Thus, we believe our private credit investments have been defensively underwritten and conservatively structured. Our software exposure is substantially less than that of our peers, predominantly first-lien, and with very little of it payment-in-kind.

Fourth, 80% of Oaktree’s total investment in private credit is on behalf of institutional clients, meaning very little was placed with the public. While the leading managers of public direct lending vehicles have $40-50 billion or more there, we have just over $10 billion.

Because our investment in direct lending was limited, we didn’t experience all the AUM growth some other credit managers did. That positions us well to take advantage now that investor enthusiasm has become more tempered. Investors’ newly elevated skepticism is likely to give us investment opportunities in the days ahead that are much better than those we passed up in the period just ended. Staying disciplined and resisting the latest fads isn’t the route to short-term maximization, but it’s essential for the excellence in investing we seek.

Direct Lending and Private Equity

Because it’s so much a part of the development of direct lending, I want to bring in private equity here and talk about the ways the two sectors will impact each other in the years ahead. Private equity took a lot longer to develop than direct lending, but their fates are very much intertwined.

As I described earlier, private equity was birthed in the 1970s, grew with the popularization of high yield bonds in the 1980s, became a consensus solution in the 2000s, and was amped up by the trend toward direct lending starting in the 2010s. The result was a very successful private equity industry and an asset class that gave investors the returns they wanted. In large part, those gains are attributed to PE firms’ ability to identify good companies to buy, install an ownership culture, and add value through strategic and financial actions. However, a substantial part of the gains resulted – without as much recognition as might have been due – from the interest rate climate private equity grew up in.

In December 2022, I wrote a memo called Sea Change. In it I talked about a bank loan I had outstanding in 1980 and the slip I got in the mail informing me that my interest rate had risen to 22¼%. Then, I said, I was able to borrow at 2¼% in 2020. I consider that 40-year, 2,000-basis point decline in interest rates the most impactful event in the financial world in the last half-century, but one that has received inadequate attention.

Among other things, declining rates make assets more valuable (leading to the asset bubbles central bankers worry about) and reduce the cost of borrowing. Thus, when rates fall, people who bought assets using borrowed money get a double bonus. And that’s exactly what private equity does. Thanks to declining and/or ultra-low rates, as I wrote in Sea Change, the private equity industry enjoyed a great tailwind for much of its existence. This was particularly true of the period 2009-21, thirteen years in which the fed funds rate was zero most of the time and averaged about half a percent. Bottom line: private equity was born and existed through 2021 in an interest rate climate that was supportive of it in the extreme.

Unsurprisingly, things went great. Investors concluded that private equity was a panacea; LP capital flowed in; and GPs were able to lever it up with freely available, low-cost debt capital, especially from direct lending after its arrival on the scene. The economic climate was supportive, featuring the longest recovery in U.S. history. A 10-year bull market made it easy for PE firms to sell their portfolio companies, as did the eagerness of new PE funds to deploy capital by buying companies from old PE funds. Returns lived up to expectations, as did distributions to LPs, and this enabled PE funds to continue attracting LP capital, perpetuating the “virtuous circle.”

But early in 2022, the central banks decided to fight inflation by raising rates, and the fed funds rate (for example) went from zero to 5¼-5½%. The essential message of Sea Change was that the days of ultra-low and secularly declining interest rates were over, and the investment strategies that had benefitted most from them would do less well in the future.

The Sea Change memo was the product of a trip Bruce Karsh and I made to clients in the fall of 2022, when travel first became possible post-pandemic. I’ll never forget the way Bruce summed up the situation: “In the last several years, a lot of private equity companies have been saddled with capital structures that didn’t anticipate a 400-basis point increase in interest rates.” The rate rise “threw sand in the gears” of private equity, and the picture today is very different from that described above:

- Higher interest costs have made many portfolio companies less profitable. Deals that were very lucrative when the cost of leverage was low now make less economic sense.

- Higher rates have meant higher interest bills and thus lower coverage ratios – the ratio of earnings to interest expense – making it more difficult to refinance debt taken on when rates were low.

- Rising interest rates reduced the value to buyers of companies’ future cash flows, just as falling rates had increased it.

- Thus, the prices at which portfolio companies can be sold is lower, and sales of portfolio companies have slowed.

- As a consequence, distributions to private equity LPs have fallen, and capital commitments LPs made based on expectations of “normal” distributions from older funds have become burdensome.

- As a further consequence, LPs are less able to commit to new funds.

- Returns on private equity funds have fallen precipitously. According to Claude, “MSCI estimates that between 2022 and Q3 2025, an index of U.S. private equity funds saw annualized returns of 5.8%, compared to 11.6% for the S&P 500.” This further reduced enthusiasm for new PE funds.

In the future, the performance of portfolio companies will be heavily influenced by the amount of skill private equity firms applied in selecting, financing, and managing them. These things – plus the salability of companies – will do a great deal to determine the performance of the debt that financed buyouts, including private loans. Declining profitability can require companies to increase the amount they owe through the payment-in-kind feature rather than service their debt as scheduled. Repayment of debt at maturity can be complicated by the combination of (a) difficulty monetizing portfolio companies, (b) refinancing challenges, and © company valuations that fall below the face amount of the companies’ total debt. Will lenders kick the can down the road? If so, what are the implications for investors in credit funds?

Lenders derive their eventual security from the performance of the companies they lend to and the margin of safety they receive from being senior in the capital structure. Lenders who performed skillful due diligence, upheld high standards, and made good credit decisions will be successful (note that high yield bonds and broadly syndicated loans, the precursors of direct lending, did fine in multi-year periods that included the Global Financial Crisis). Even if some borrowers have to delever, decent company performance should permit the payment of interest and principal. Of course, the outlook is less good if business models falter or lower valuations are assigned to companies, as that reduces the lender’s margin of safety, especially with regard to junior debt tranches.

* * *

Illustrating the tendency of developments to rhyme, I’ll close with something Bob O’Leary wrote to me the other day:

It strikes me that there are interesting parallels between credit markets today and the late 1980s/early ’90s, when you and Bruce started the first Special Credits funds. Back then, there was a new financial innovation (high yield bonds) that many investors had over-indulged in. The market suddenly got spooked by a war in the Middle East, and investors couldn’t dump high yield fast enough.

Substitute direct lending for high yield and add an element of technological creative destruction, and you have some of the same dynamics (including another war in the Middle East sparking fears of recession). Ultimately, high yield was fine (even great), and direct lending will be as well, but it may have to go through a credit cycle to get to a better place.

April 9, 2026

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Legal Information and Disclosures

This memorandum expresses the views of the author as of the date indicated and such views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

This memorandum is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree Capital Management, L.P. (“Oaktree”) believes that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of Oaktree.

© 2026 Oaktree Capital Management, L.P.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All