Last week, we discussed the risk of an oil shock leading to a recession. To wit:

“After more than three decades of watching oil markets upend economies, one pattern keeps repeating: investors learn the wrong lessons from the last shock. The 1973 OPEC embargo taught us that geopolitical disruptions are temporary. That lesson then got everyone killed, financially speaking, in 1979. The 2003 Iraq War produced only a mild oil bump and no recession, so traders got comfortable. Then 2008 happened. Today, with Brent crude having spiked over 60 percent since U.S. and Israeli strikes on Iran began in late February, the same dangerous reasoning is circulating again. That narrative is that this ‘event” is manageable and will resolve quickly. If that is the case, then the economy will absorb it.

That may indeed be the case. However, the conditions that determine whether an oil shock becomes a full recession are specific, quantifiable, and worth examining with clear eyes. That is what this analysis does.”

That article digs into the plumbing behind oil shocks and recession, and exposes why, over the years, I’ve learned to distrust the loudest voices in the room. Right now, some of the most prominent macro commentators, the “Persistent Purveyors of Doom,” are making a variation of the same argument: the Strait of Hormuz closure is not merely a serious risk of an oil shock and recession; it’s the beginning of the end. Markets will crash within weeks. Stocking up on essentials is the rational response. The global financial system, already fragile, cannot survive what’s coming.

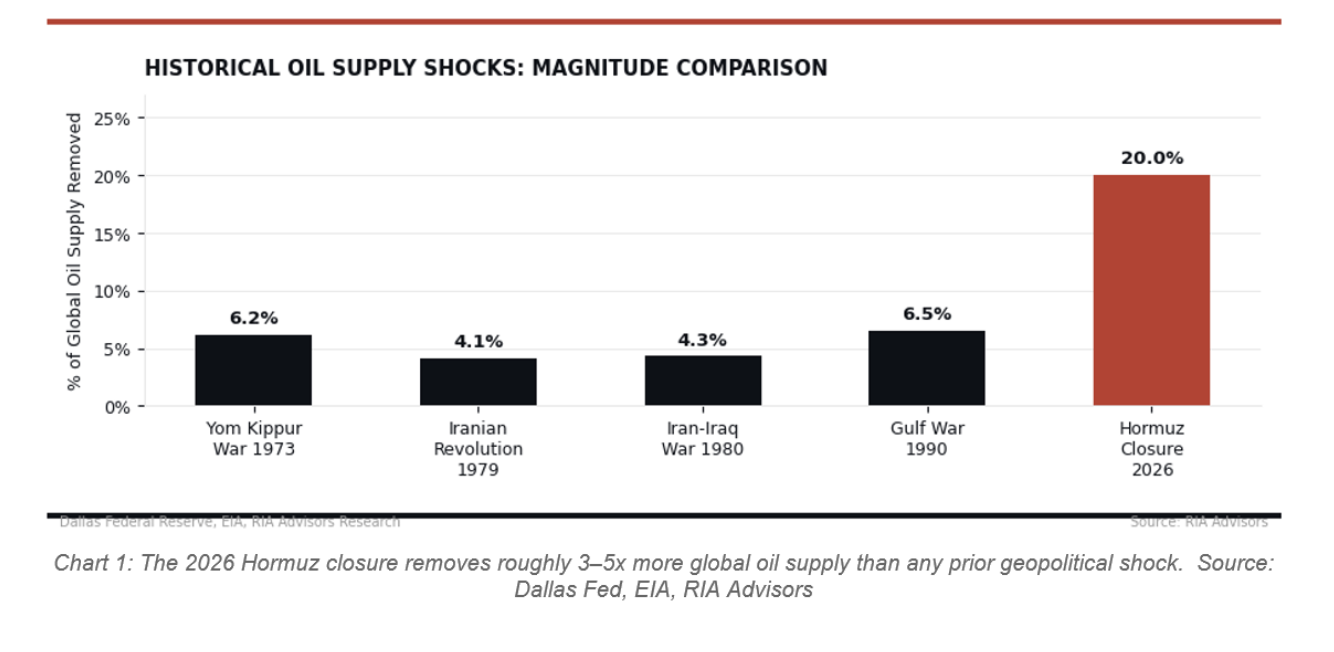

I certainly can understand the appeal of that thesis. The disruption is genuinely unprecedented. Roughly 20% of global oil and LNG now sit stranded behind a military blockade. Furthermore, the secondary effects on fertilizer prices, food inflation, and petrochemical supply chains are real and compounding. This is, as they say, “not nothing.” But ‘this is serious’ and ‘this is the worst crisis in anyone’s lifetime’ are two very different claims. The evidence, as we will discuss today, supports the first one far more than the second.

The catastrophist argument rests on a critical hidden assumption: that the global economy, central banks, and governments sit passively while a supply shock plays out. History doesn’t support that assumption — not once.

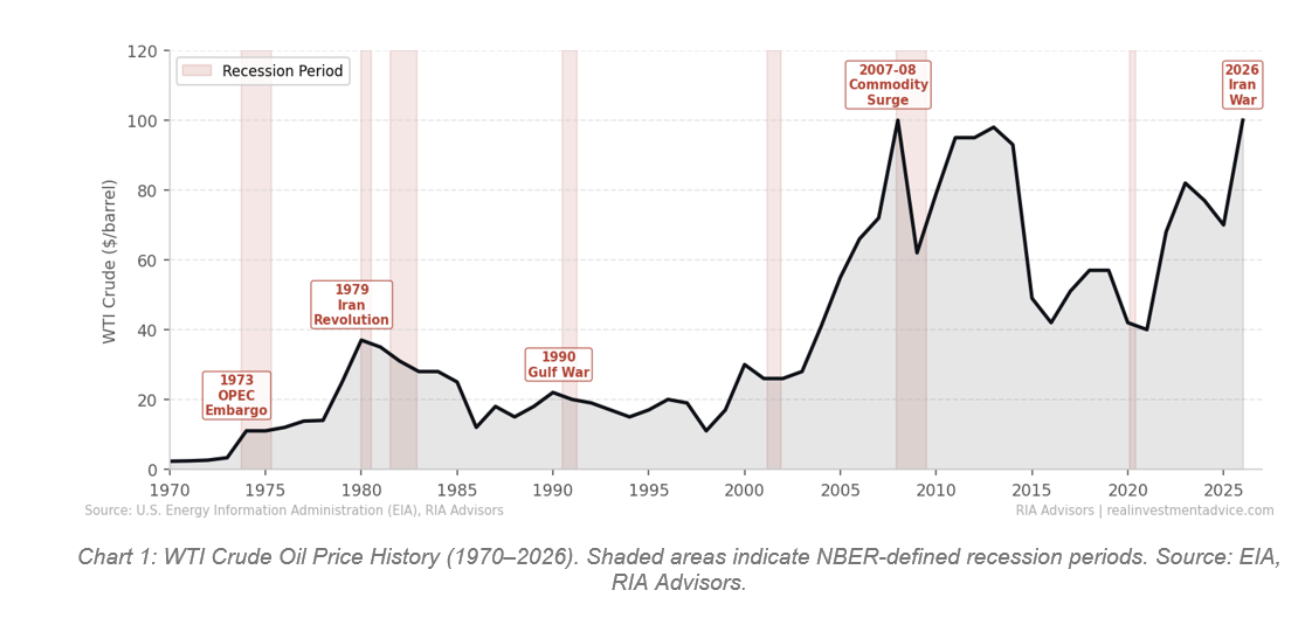

In 1973, the Arab oil embargo removed roughly 6% of global oil supplies from the market. Painful, yes. Civilizational collapse, no. Markets adjusted, alternative suppliers ramped up, and policymakers, however clumsily, responded. In 1990, Iraq’s invasion of Kuwait spiked oil prices by nearly 80% in three months. Within six months, prices had reversed almost entirely as supply alternatives emerged and the military situation resolved. Even in 2008, when oil hit $147 per barrel, the story wasn’t that oil destroyed the financial system. The financial system had already built its own bomb. Oil just lit the fuse faster.

What we’re seeing today follows the same pattern. The IEA has already authorized the release of 400 million barrels from strategic reserves, the largest emergency release in history. Saudi Arabia rerouted production through the East-West pipeline to Yanbu port on the Red Sea. The U.S. military launched an active campaign to reopen the strait on March 19th. These are not the actions of a world sitting passively in the path of an unstoppable freight train. They’re the messy, imperfect, and historically consistent responses of a system under stress. More crucially, it is doing what systems under stress do: adapting.

The Real Risk: The Sequencing Trap

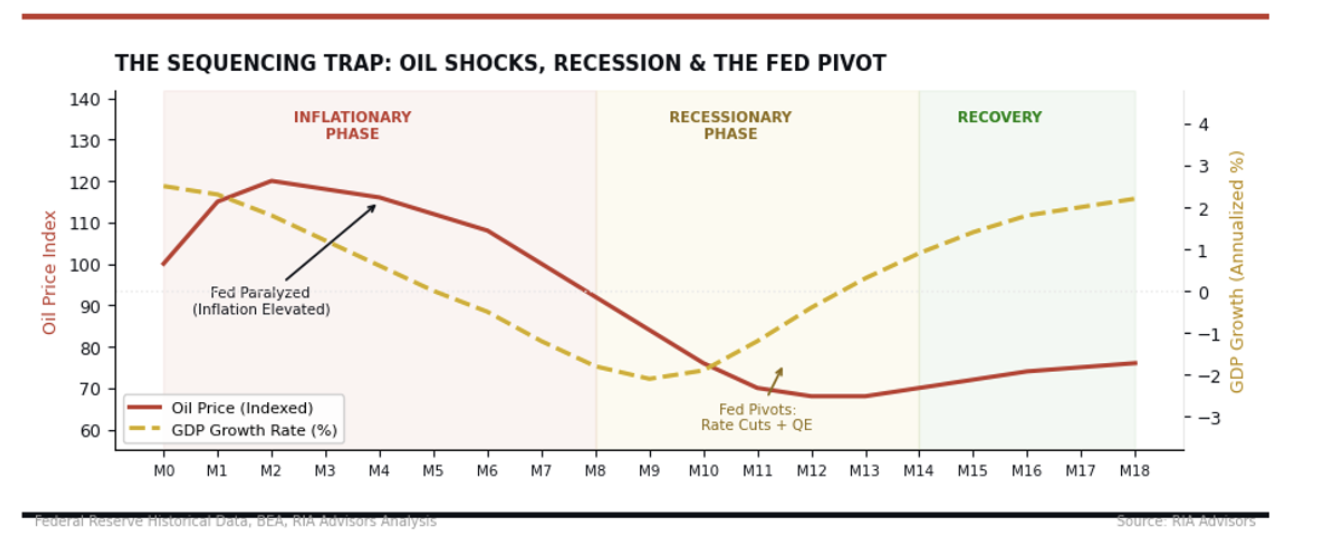

Here’s what the catastrophists get right, though it’s not the story they’re telling. The genuine danger isn’t a sudden market collapse in three weeks. It’s the sequencing trap that every major oil shock has sprung, and the Federal Reserve is already caught inside it.

Oil shocks are simultaneously inflationary and recessionary. That’s what makes them so insidious and so difficult to manage. In the short run, energy prices spike, headline inflation surges, and the Fed cannot ease. But elevated energy costs act as a regressive tax on every consumer regardless of income. Disposable income gets crushed, business input costs compress margins, and hiring freezes give way to layoffs. Eventually, consumer demand collapses faster than supply adjusts, and at that point, the inflationary impulse reverses hard.

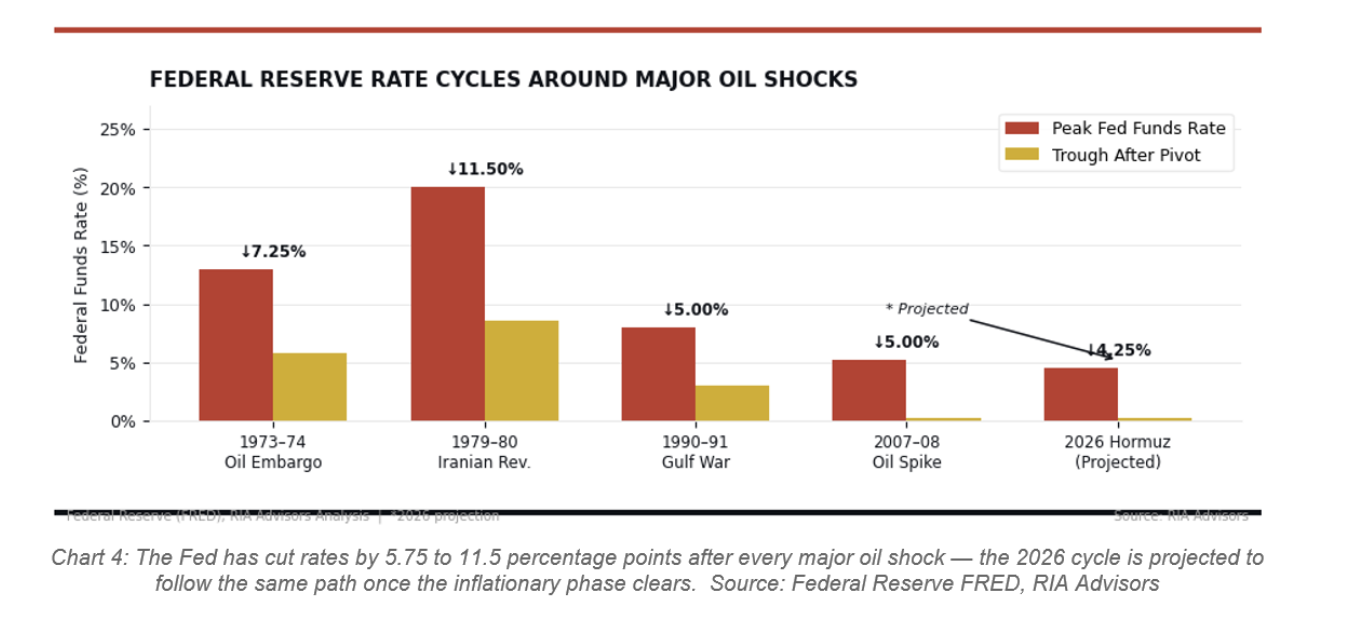

Has such a cycle occurred previously? Yes, in 1974, 1980, 1982, and in 2008, when oil at $147 in June had fallen to $32 by December. The self-limiting nature of oil shocks is one of the most reliable patterns in macroeconomic history. The inflation doesn’t last. The recession that follows it does.

That’s why positioning right now matters enormously. Ben Bernanke’s QE doctrine worked brilliantly in 2008-09, 2011, and again in March 2020 because each episode shared a common condition: a demand-side deflationary shock. Credit froze, spending collapsed, and inflation fell. The Fed could inject liquidity without stoking inflation because there was no inflation to stoke.

A supply-side stagflationary shock inverts that logic entirely. Aggressive rate cuts into $120 oil weaken the dollar, making energy priced in dollars more expensive for U.S. consumers. QE signals panic and risks re-igniting the wage-price spiral the Fed spent 2022 and 2023 fighting to break. Arthur Burns made exactly this mistake in the 1970s, and the result wasn’t stabilization. It was stagflation that took Paul Volcker and 20% interest rates to unwind. That institutional memory lives in every Fed governor’s DNA right now.

To be fair, today’s Fed operates from a meaningfully stronger position than Burns did. The U.S. economy is roughly 60% less energy-intensive per dollar of GDP than it was in 1973, and American shale production has transformed the country into a net energy exporter. That one fact is a structural buffer that simply didn’t exist when the Arab embargo hit. Those differences reduce the severity of the transmission from high oil prices into core inflation, and they give the Fed slightly more room to maneuver before a full-blown wage-price spiral takes hold. What those differences don’t change, however, is the fundamental sequencing dynamic. That is, a sustained supply shock still produces the same inflationary-then-recessionary arc, and the Fed still cannot ease aggressively until inflation visibly cracks. However, when that moment arrives, it will be with somewhat less economic damage already baked in.

Yet the Fed isn’t completely paralyzed. Targeted liquidity facilities, repo operations, and coordinated dollar swap lines with the ECB and BOJ can prevent a credit market seizure without the inflationary optics of full QE.

The Fed will provide plumbing support. The only question is whether it has political cover to do more, and with oil near $120, it almost certainly does not. At least, not yet.

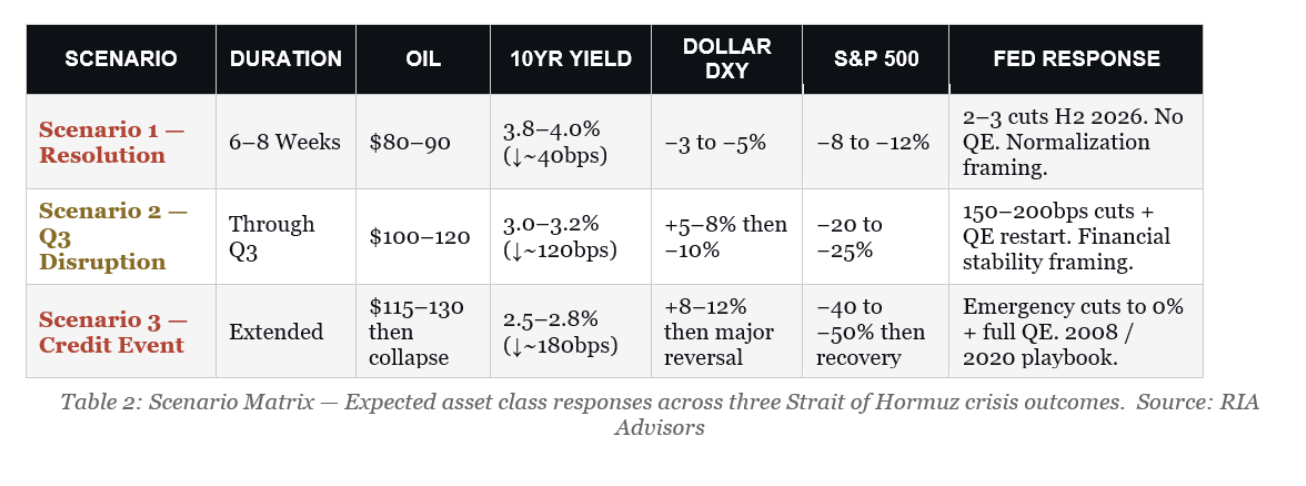

Three Scenarios and What They Mean for Your Portfolio

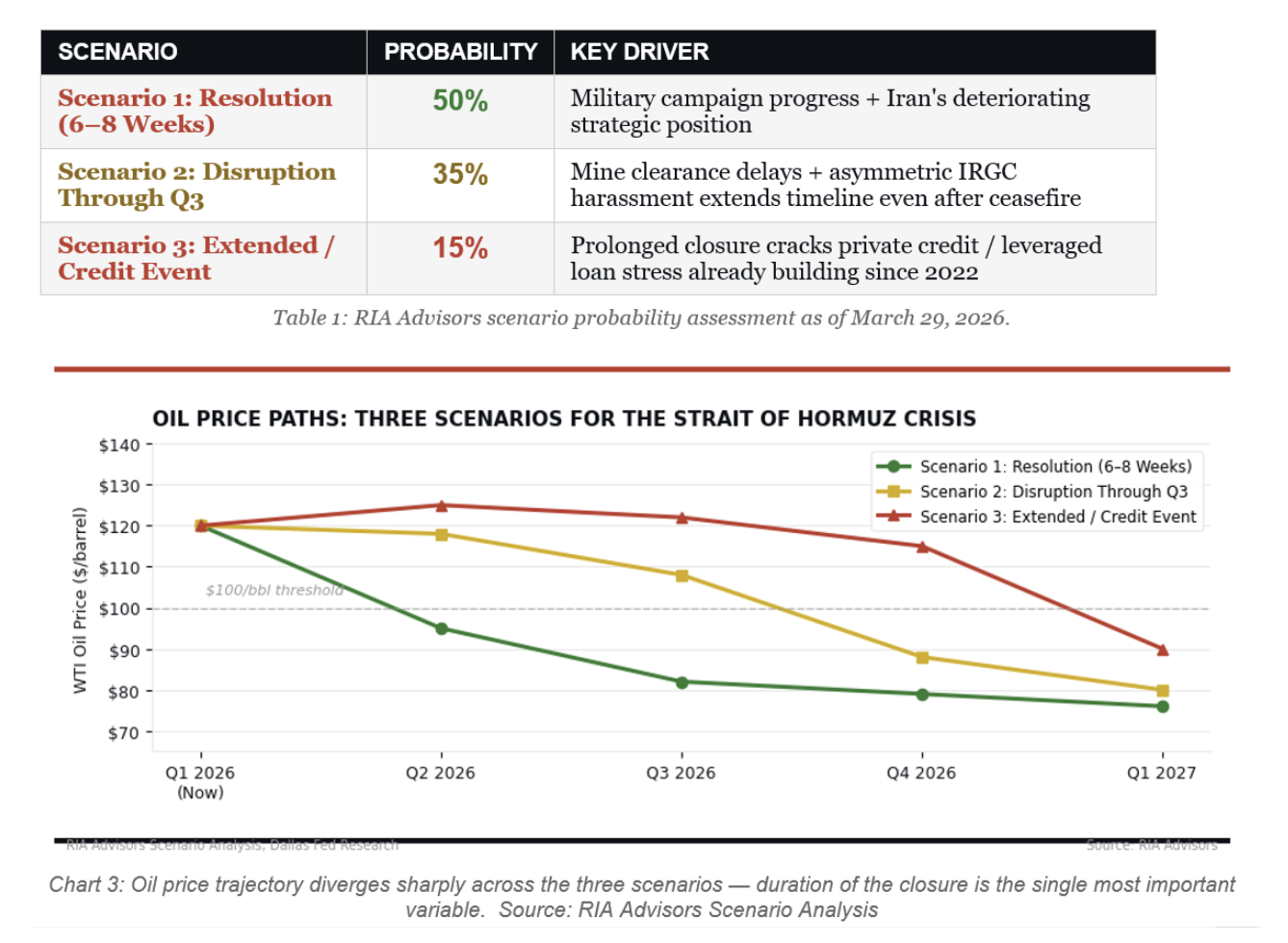

The specific outcome depends almost entirely on how long the Strait of Hormuz disruption persists. Based on what we know as of March 29 — the U.S. military campaign underway since March 19, Iran’s leadership structure fractured, but mines still in the water and attacks continuing — here is how I’d assign the probabilities across the three paths. Let me walk through each in detail, including what I expect from Treasury yields, the dollar, and equities in each case.

SCENARIO ONE — 50% Probability: Resolution within six to eight weeks. This remains the base case, though it’s a coin flip rather than a certainty. The U.S. military campaign, which has been underway since March 19th, is the dominant variable — Iran’s strategic position is deteriorating by the week, its economy is imploding, its leadership structure is fractured, and it has no viable endgame that involves a prolonged closure. Historical precedent also favors shorter disruptions. The 50% odds reflect the fact that mine clearance and war-risk insurance reinstatement add weeks even after hostilities formally subside. A combination of diplomatic pressure, military progress, and economic pain on all sides produces a partial reopening.

- Oil retreats from the current $120 range toward $80 to $90.

- The Fed cuts two to three times in the second half of 2026, framing it as normalization rather than a crisis response.

- Treasury yields move from 4.4% to 3.8%-4.0% as recession fears moderate.

- The dollar weakens 3% to 5% on the DXY.

- Equities recover but remain 8% to 12% below pre-conflict highs through year-end as multiple compression persists.

SCENARIO TWO — 35% Probability: Disruption persists through Q3 2026. The second most likely outcome. Even a nominal ceasefire doesn’t instantly reopen commercial shipping. Things such as war-risk insurance, mine sweeping, and shipper confidence all take time to restore. A grinding, partial resolution that keeps oil elevated and supply chains stressed through summer is entirely plausible, particularly if Iran’s remnant forces pursue asymmetric harassment rather than formal closure. Oil stays in the $100 to $120 range for two full quarters. Demand destruction compounds into a genuine recession. Headline inflation initially stays elevated, but core starts rolling over as consumer spending collapses. By September or October, the Fed faces the sequencing trap in full: an undeniable recession, inflation reversing, and financial conditions tightening into the downturn.

- The Fed cuts aggressively, 150 to 200 basis points in rapid succession, restarting QE and framing it as financial stability support.

- The 10-year Treasury yield falls toward 3.0%-3.2%.

- The dollar surges by 5% to 8% on safe-haven demand before weakening sharply once QE restarts.

- The S&P 500 tests the 4,800 to 5,000 range, a 20% to 25% decline before the Fed backstop stabilizes sentiment.

SCENARIO THREE — 15% Probability: Extended closure triggers a credit event. This is a genuine tail risk, not a rounding error, and the 15% odds reflect that. The private credit, leveraged loan, and commercial real estate stress has been building since the 2022 rate cycle finally fully cracks under the combined weight of the energy shock and prolonged elevated rates. A major credit vehicle or institution fails. Suddenly, it’s not just a recession, it’s a credit seizure.

- The Fed cuts to 0% and launches a full QE program simultaneously.

- Treasury yields collapse toward 2.5% to 2.8%.

- The dollar surges 8% to 12% in the acute phase before a sustained multi-quarter reversal as the balance sheet expands.

- Equities decline more sharply as forward earnings estimates are slashed (roughly 40-50%), before recovering sharply once intervention takes hold. The S&P 500 could conceivably test the 3,800 to 4,200 range at the trough.

The Critical Takeaway For Investors: Scenario 3 has only a 15% probability but could imply a 40–50% drawdown in equities. That’s an expected loss contribution too large to ignore, even in a base-case world. Therefore, we continue to maintain a defensive posture regardless of which scenario ultimately plays out.

What Investors Should Do Right Now

I have lived and worked through four major market crises in my career. Over that time, I’ve repeatedly watched two destructive instincts play out with near-perfect reliability. The first is panic-selling everything at the worst possible moment. The second is dismissing real risk because the sky hasn’t fallen yet. Both have cost investors dearly, and neither is the right posture here.

The evidence of previous oil shocks supports a deliberate defensive shift for the time being. Increasing cash levels, holding short-duration treasuries, and reducing exposure to more globally cyclical equities. In other words, the “reflation trade” that began the year has likely come to an abrupt end. The sequencing trap is real, and the Fed will likely be slower to arrive than bulls are pricing unless the inflationary impulse reverses rapidly. However, in reality, the gap between the inflationary phase and the Fed pivot is the danger zone. That is potentially two to four quarters of deteriorating growth, declining earnings, and no central bank backstop, leaving plenty of room for portfolio damage.

Yes, the Fed will eventually ride to the rescue, and history makes that impossible to ignore. The question is always the same: how much permanent capital loss accumulates before that pivot arrives?

What is most crucial to your outcomes is not letting the “doom crowd” paralyze you. However, don’t let the optimists convince you that the risks of an oil shock are already priced in. The damage in a sequencing trap happens quietly, over quarters, not in a sudden crash that gives you time to react. The time to position defensively is today, not after the recession data confirms what the oil market is already telling you.

“Defense over offense — and trade accordingly.”

References

- Federal Reserve Bank of Dallas — “What the closure of the Strait of Hormuz means for the global economy,” March 2026. dallasfed.org

- International Energy Agency — Emergency strategic reserve release statement, March 2026. iea.org

- Wikipedia — “Economic impact of the 2026 Iran war,” updated March 29, 2026.

- Al Jazeera — “Iran’s closure of the Strait of Hormuz is an international crisis,” March 25, 2026.

- CNBC — “Strait of Hormuz closure: which countries will be hit the most,” March 3, 2026.

- Atlantic Council — “The Strait of Hormuz crisis will ripple across plastics and food supply chains,” March 2026.

- Atlas Institute for International Affairs — “The Strait that Moves the Market,” March 2026.

- Ben Bernanke — “What the Fed did and why,” Washington Post, November 4, 2010.

- Federal Reserve (FRED) — Historical Federal Funds Rate data. fred.stlouisfed.org

- Kpler Energy Research — Hormuz transit volumes and crude flow data, March 2026.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Real Investment Advice

Read more commentaries by Real Investment Advice