Ever since the pandemic – when surging housing demand collided with a decade of underbuilding – housing affordability has become an increasingly important political issue and a larger focus for policymakers. President Donald Trump has made it a component of his agenda heading into the midterm elections in November, including issuing several executive orders on housing (read them here), and Congress has recently taken steps to pass legislation that, among other things, would reduce the federal regulatory burden on new home construction, though much of the red tape exists at the local level.

While we believe housing affordability has improved and will continue to do so (read our recent commentary), some policy ideas circulating in Washington, DC could marginally enhance affordability, while others, albeit well-intentioned, could actually hinder affordability. We enumerate and expand on these concepts:

1) Changing the mix of agency mortgage-backed security (MBS) purchases and increasing the $200 billion amount could help lower mortgage rates. In January, President Donald Trump announced that Fannie Mae and Freddie Mac – government-sponsored entities (GSEs) – would purchase up to $200 billion of agency MBS in the coming months. The goal is to increase demand, which typically raises bond prices and lowers yields, thereby reducing mortgage rates.

Mortgage rates initially declined following the announcement – the 30-year mortgage rate fell below 6% for the first time in more than three years. However, rates have since rebounded amid the Iranian conflict as well as due to confusion about the GSE purchase program’s objectives and which mortgages the GSEs are purchasing. There has also been concern that $200 billion is too small relative to the roughly $9 trillion agency MBS market to materially impact rates.

To maximize effectiveness, we believe Fannie and Freddie should concentrate purchases in segments where rate impacts would be most significant (the so-called “par coupon”). Additionally, we think the Trump administration should consider expanding purchases beyond $200 billion – indeed, even announcing an increase could lower rates. Lastly, while the Federal Reserve should remain independent, mortgage rates could decrease further if the Fed halted the roll-off of mortgage bonds on its balance sheet (read more in our commentary “A Fed Housing Fix That’s Hiding in Plain Sight").

We believe the GSEs buying the par coupon and the Fed stopping the run-off could decrease mortgage rates up to 25 basis points (bps), with further rate declines possible if GSE MBS purchases were to increase. These policies have the added benefit of not requiring Congressional approval.

2) Clarifying the future of the GSEs could also lower mortgage rates. We have written extensively about the future of the GSEs and maintain that policymakers should “not fix what is not broken” (read more here). We believe the GSEs are doing an excellent job of delivering mortgage liquidity and providing access to mortgage credit, not to mention they are profitable (and at times, significantly so), benefiting taxpayers – a nice reversal, since taxpayers funded the bailout of the GSEs during the 2008 financial crisis.

Despite functioning well in their current state, there has been ongoing discussion and speculation about the possible public offering of Fannie and Freddie stock. We believe talk alone of a GSE IPO may be self-defeating as it raises questions about future government support. This uncertainty can add risk premium to MBS, increasing mortgage rates for borrowers. As such, if the administration were simply to stop talking about a potential IPO of the GSEs, we could see some of this uncertainty premium decrease and rates could decline by ~10bps.

Of course, Congress could eliminate this uncertainty altogether – and lower mortgage rates significantly – by passing legislation to explicitly guarantee all GSE mortgage-backed securities. Doing so would provide significant (and welcome) clarity to investors globally about the current and future state of the GSEs and likely lead to even more demand from investors. Such a change could also lead to increased appetite for MBS from banks due to better risk-weighting under the existing capital treatment rules.

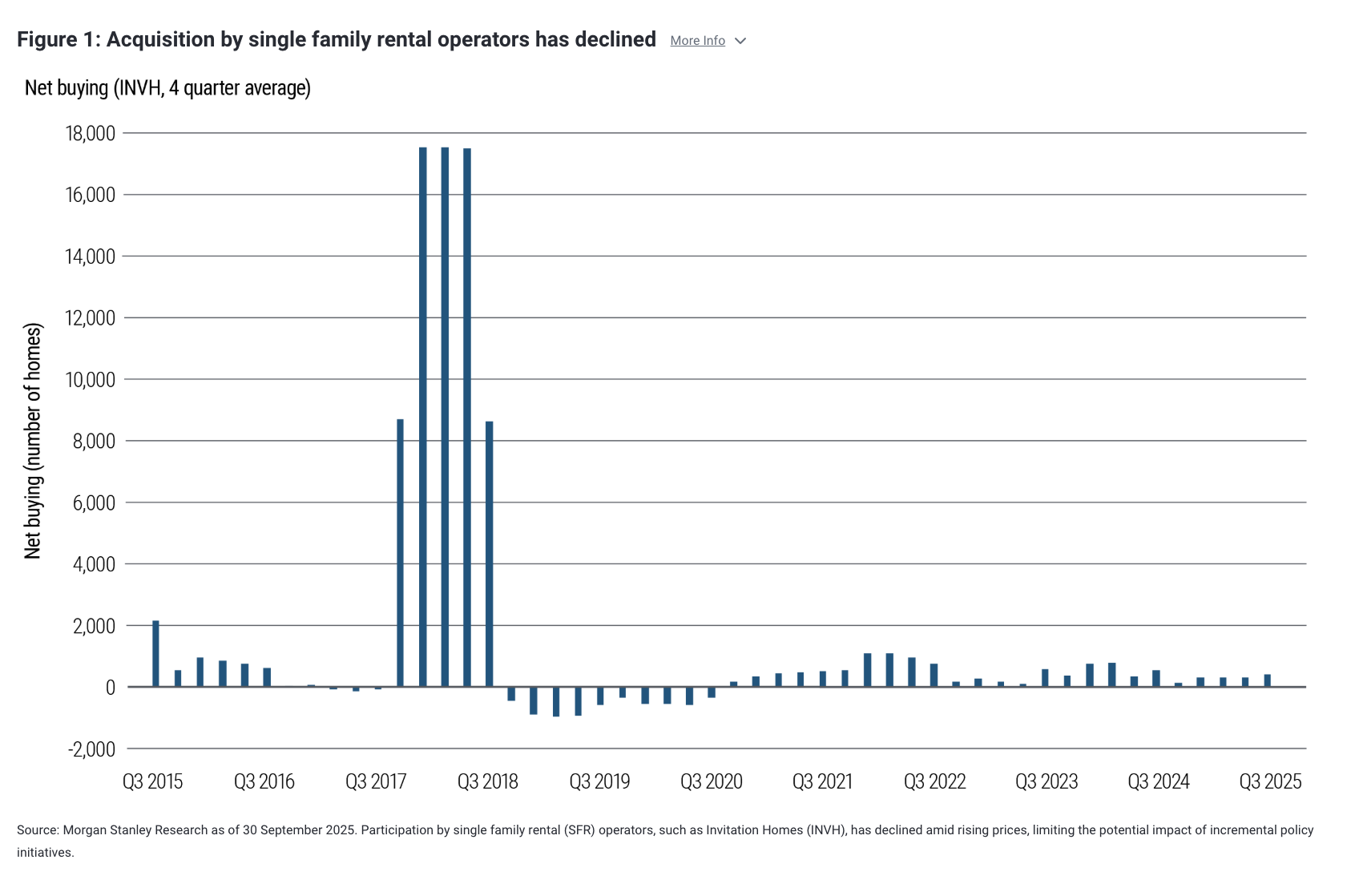

3) Modifying the GSE rules to limit the number of investment properties allowable could – at the margin – increase the supply of housing. A recent executive order (read it here) requires the Treasury to evaluate the impact of purchases by institutional investors on the housing market and propose recommendations. From our perspective, these institutional investors, primarily single-family rental (SFR) companies, are not significantly exacerbating affordability (see Figure 1). Indeed, rents have declined while costs have increased, reducing the investment appeal of large-scale acquisitions. Regardless, such a policy would require Congressional action, and we do not think the policy has sufficient support in Congress as of now.

Still, policymakers could more effectively limit potential investor crowding-out without Congress; the GSEs could limit the number of homes they guarantee for investment purposes. Currently qualified investors can finance up to 10 properties. This policy is relatively new and was borne out of a time – in 2009 – when the U.S. had “too many homes” and policymakers decided to raise the number of allowable properties to 10. This seems silly now, and we believe an update could and should be implemented to ease supply to ensure access for first-time homebuyers.

4) If a “g-fee” cut is considered at all, it should be narrowly targeted to avoid unintended consequences. We do not believe that policymakers need to (or should) cut the “g-fee,” the fee that GSEs charge to cover the costs of guaranteeing an underlying mortgage. These fees are small relative to the overall mortgage rate and are an important component of Fannie and Freddie’s profitability and capital accumulation. Indeed, given the cloud of uncertainty in the market regarding this issue, mortgage rates could decline by five to 10 bps if policymakers were to simply announce that they will not cut the g-fee.

If policymakers pursue this idea, we believe it is essential that the g-fee reduction be limited to first-time homebuyers and not those looking to refinance. If a g-fee cut were implemented across-the-board, it would likely lead to higher, not lower mortgage rates.

Why? One of the primary reasons agency MBS trade at higher yields than U.S. Treasuries, even though they are both government-guaranteed (and bear the same credit risk), is because MBS are “callable” – borrowers can pre-pay their mortgages at any time. Investors require greater yield as compensation for the potential that borrowers will prepay and investors will get their money back before they want it. Given a broad-based g-fee cut would make bonds more callable as more borrowers would refinance, we would expect mortgage rates to increase, rather than to decrease, since MBS investors would demand a higher yield premium. Instead, if the cut were targeted only at new first-time homebuyers, a broad-based increase would not occur, which would better achieve the goal of policymakers to lower rates for home purchasers.

5) Avoid policies that could unintentionally increase mortgage rates. Similar to an across-the-board g-fee cut, we believe policymakers should avoid other policies that could increase mortgage rates because they either increase prepayment risk (investors getting their money when they don’t want it – i.e., rates are decreasing) or increase extension risk (investors not getting their money back when they do want it – rates are increasing). Both outcomes lead to investors demanding more MBS yield, driving up mortgage rates. Such policies include 1) a cut to the loan level pricing adjustments (LLPA) – one-time, upfront fees charged to lenders and passed onto borrowers – which would lead to prepayment risk, 2) funding a 50-year mortgage, which could lead to prepayment risk, as well as much less equity build-up, and 3) allowing mortgage portability – a borrower could transfer their mortgage to another property – which would lead to extension risk.

6) End homebuilder buydowns, which artificially inflate home prices. As housing affordability has declined, homebuilders have started offering “buydowns,” providing borrowers a below-market mortgage rate (typically one to two percentage points lower). While this reduces the interest homebuyers pay, homebuilders pair the lower rate with a higher priced home. This may sound good in theory, but in practice it inflates the price of the home above where it would typically clear and can artificially elevate neighboring home prices as well. Should the homebuyer need to sell shortly after purchase, the realized value would likely be well below the original sale price, exposing both taxpayers and subsidized homeowners to risk. Also, the homebuyer loses the opportunity to refinance if interest rates decline one or two points in the future – i.e., they could have bought a cheaper home at a higher mortgage rate and then refinanced if rates declined, enjoying a lower monthly payment. Finally, home insurance and property taxes are higher because of the artificially elevated home price. Overall, this practice further exacerbates affordability issues. We believe Ginnie Mae and the Federal Housing Authority (FHA) should limit this practice, something they have the power to do unilaterally.

Conclusion

We expect some improvements in housing affordability will occur organically, so it may behoove policymakers to do very little. In fact, they could help lower rates by simply clarifying they are not going to IPO the GSEs and will not pursue a broad-based g-fee cut.

If policymakers take a more active approach, however, they should ensure their policies do what they are intended to do – decrease mortgage rates – and avoid unintended consequences that accomplish the opposite.

If all the policies outlined above were pursued, we believe mortgage rates would decline by nearly 75 bps, bringing the mortgage rate closer to 5%, than the 6% we see today.

Disclosures

All investments contain risk and may lose value.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author] and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0402-5360302

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO