Key takeaways

-

Oil shocks tend to matter if they persist. History suggests markets reprice risk not on the initial spike in prices, but when elevated energy costs linger long enough to tighten financial conditions.

-

Consumer strength is increasingly split by income. Higher prices and tighter credit are straining lower‑income households, while asset‑rich households remain supported by elevated housing and equity wealth.

-

Credit stability masks growing dispersion. Structural buffers are helping contain stress in senior securitized credit, but widening gaps between prime and subprime areas point to differentiation beneath the surface.

The Middle East ceasefire sparked a relief rally last week as markets dialed back the risk of a deep, drawn‑out oil supply shock. Stocks have already erased much of the post-conflict drop. Bonds haven’t gotten the memo: Yields are still elevated, keeping a bit of extra term premium on the table.

That gap is telling. Bond investors are still pricing a messier growth‑inflation mix than the pre‑conflict baseline. And crude isn’t exactly flashing “all clear,” either, with spot prices still near $100 a barrel as of this writing.

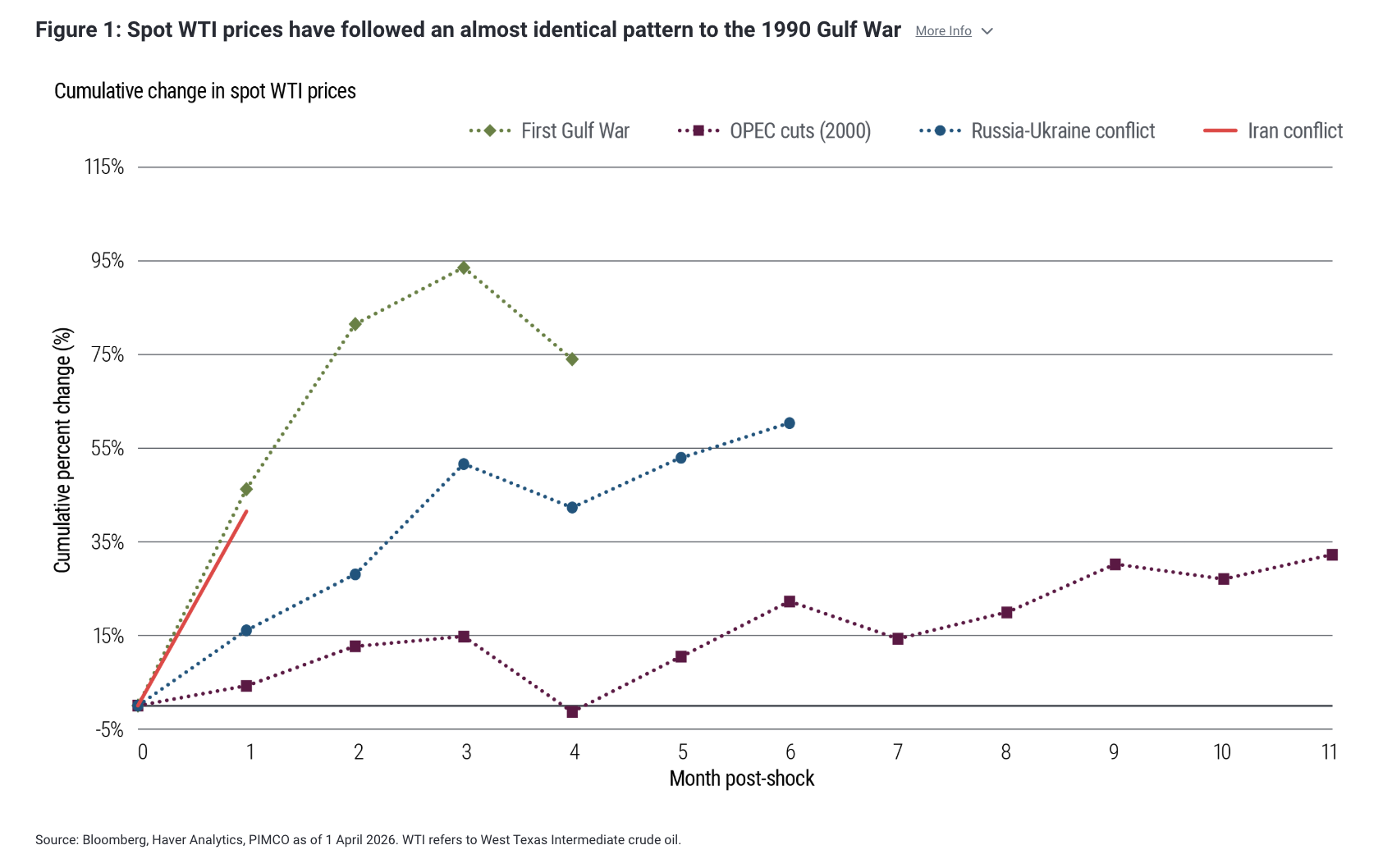

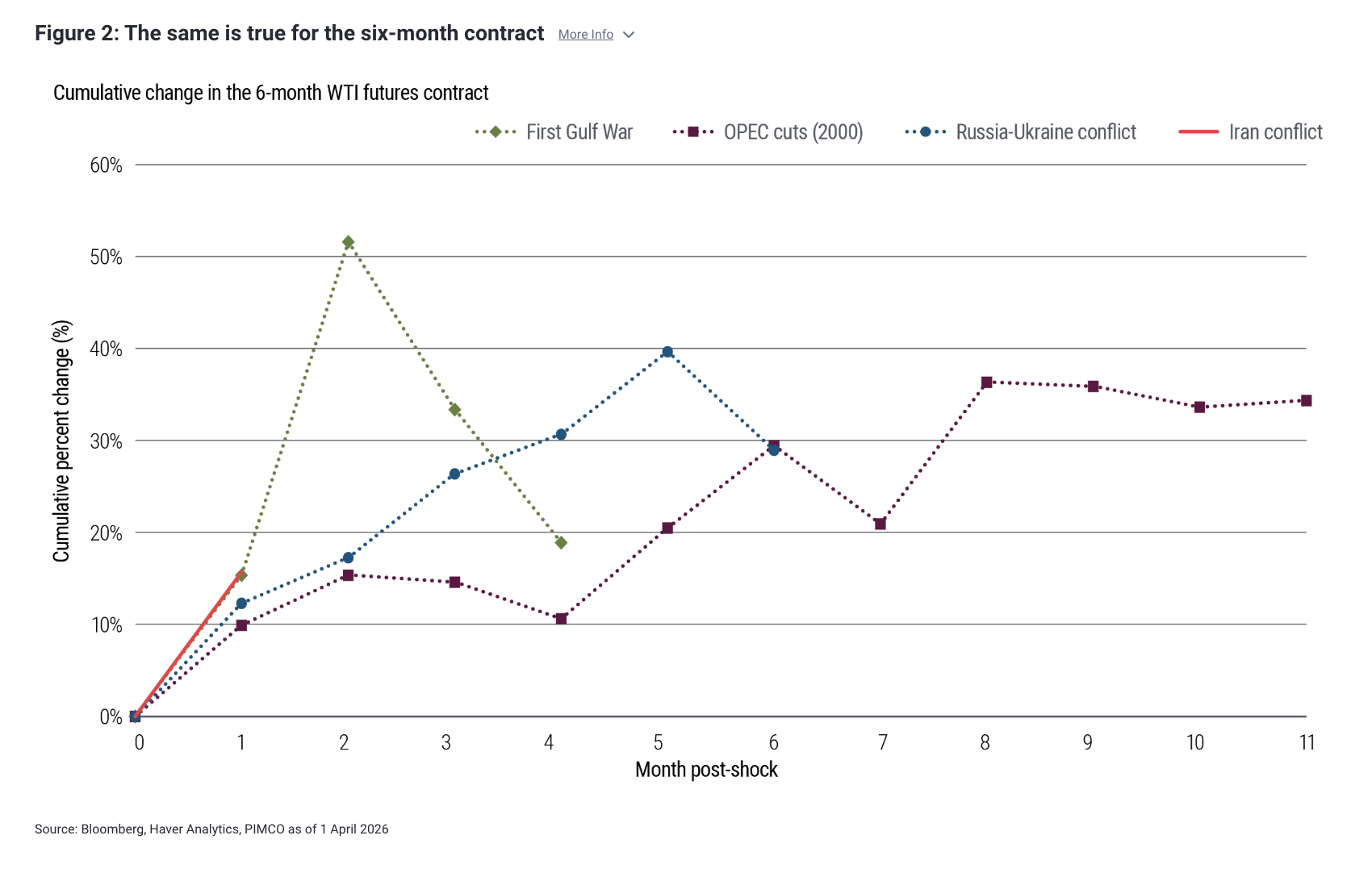

History is blunt on this point: It’s not the oil spike that breaks risk appetite, it’s how long it sticks around. Figures 1 and 2 illustrate this pattern by comparing cumulative changes in spot and six‑month crude futures across the four major oil supply shocks of the past four decades: the 1990 Gulf War, the 2000 OPEC production cuts, the 2022 Russia–Ukraine conflict, and the current Middle East war. Just over a month into the current episode, both spot and six-month futures have tracked a path remarkably similar to the early phase of the 1990 Gulf War.

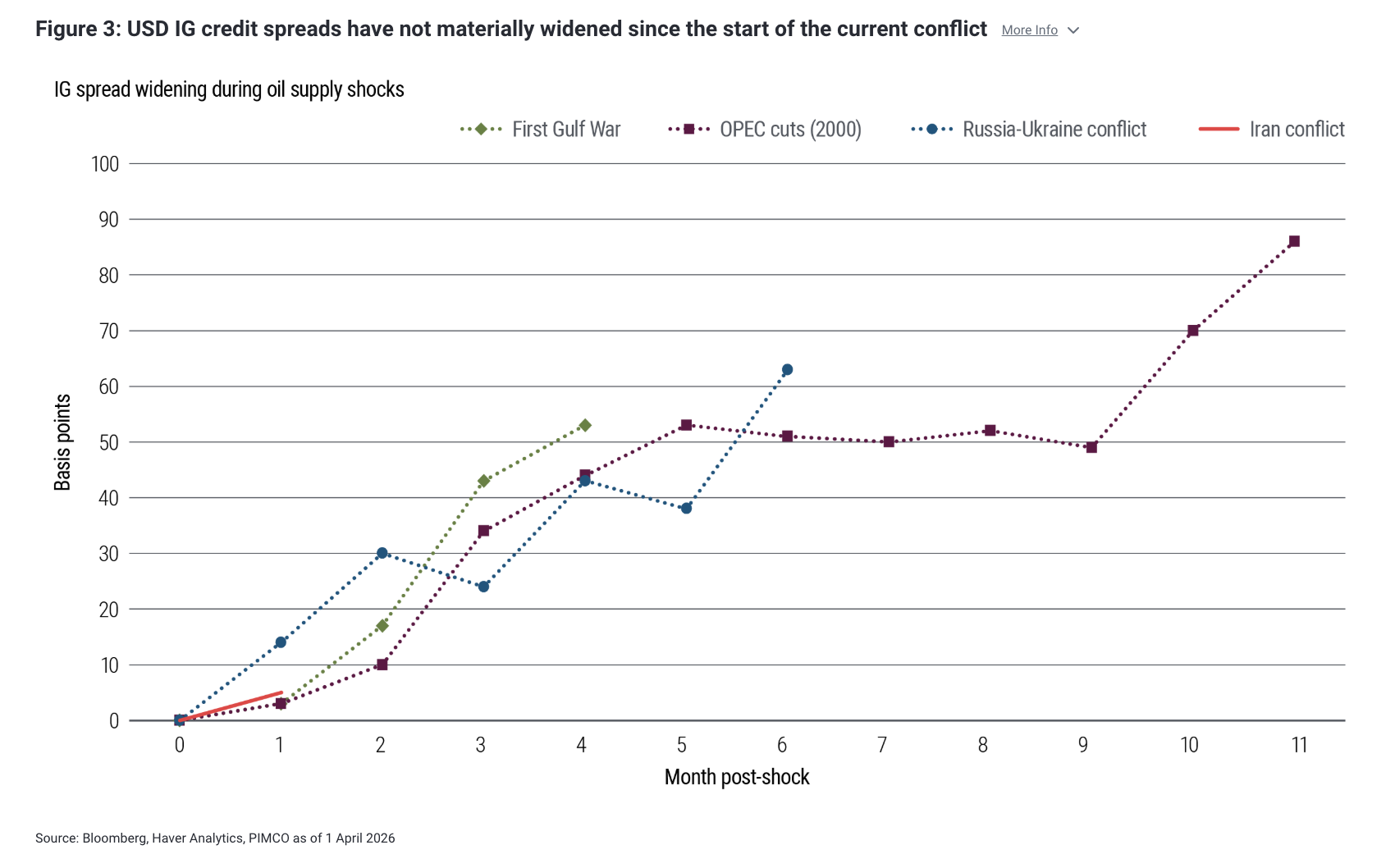

The bottom line is that it was only as the 1990 conflict dragged on – energy infrastructure was taken offline and excess inventories depleted – that markets began to sharply reprice longer dated oil futures. That inflection coincided with material widening of U.S. dollar investment grade credit spreads (see Figure 3) and lower Treasury yields, as investors increasingly treated the shock as a negative impulse for economic growth.

Whether the current episode follows a similar trajectory remains uncertain – but if it does, time is not your friend.

A potentially deeper K-shaped divide

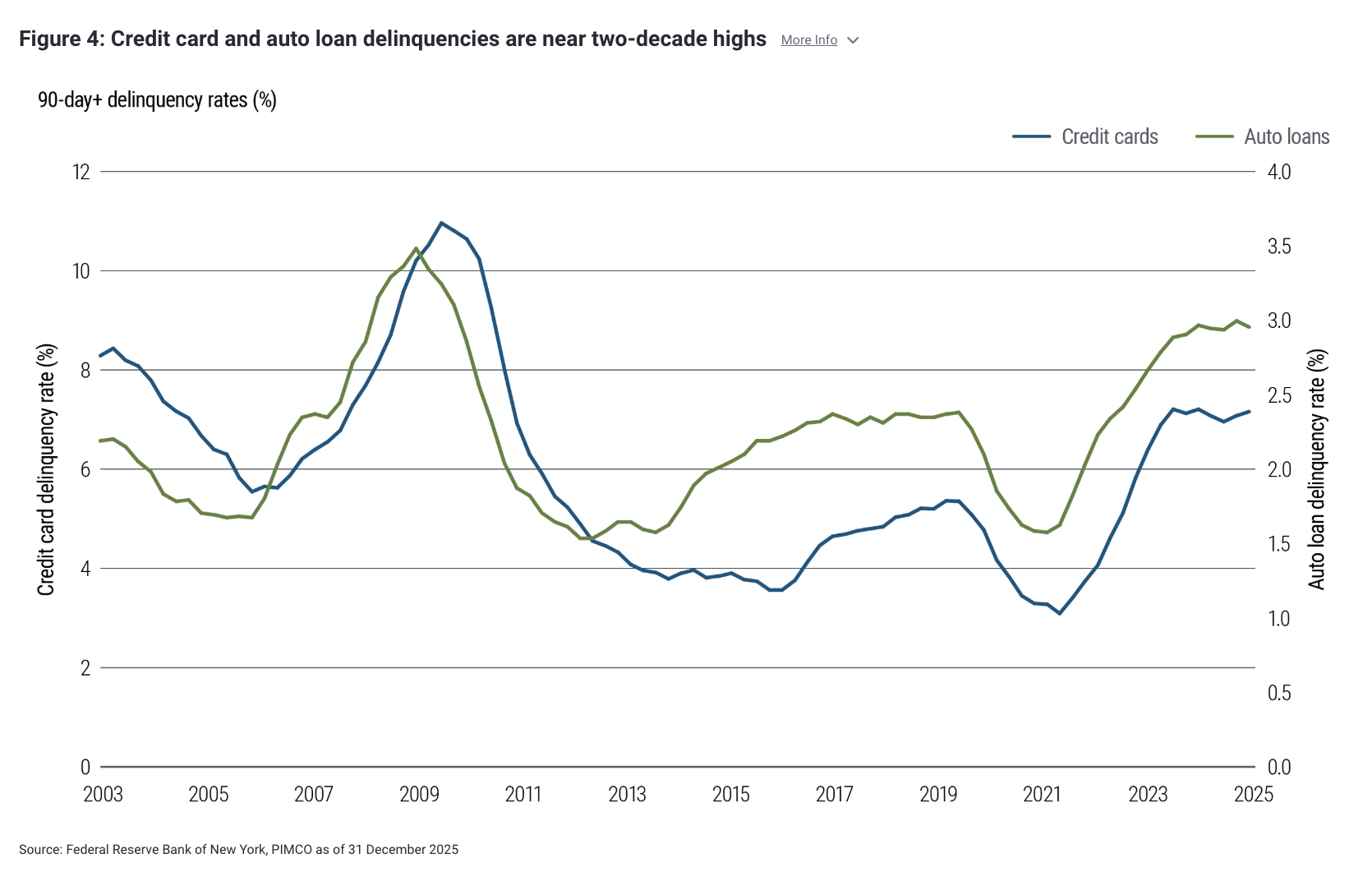

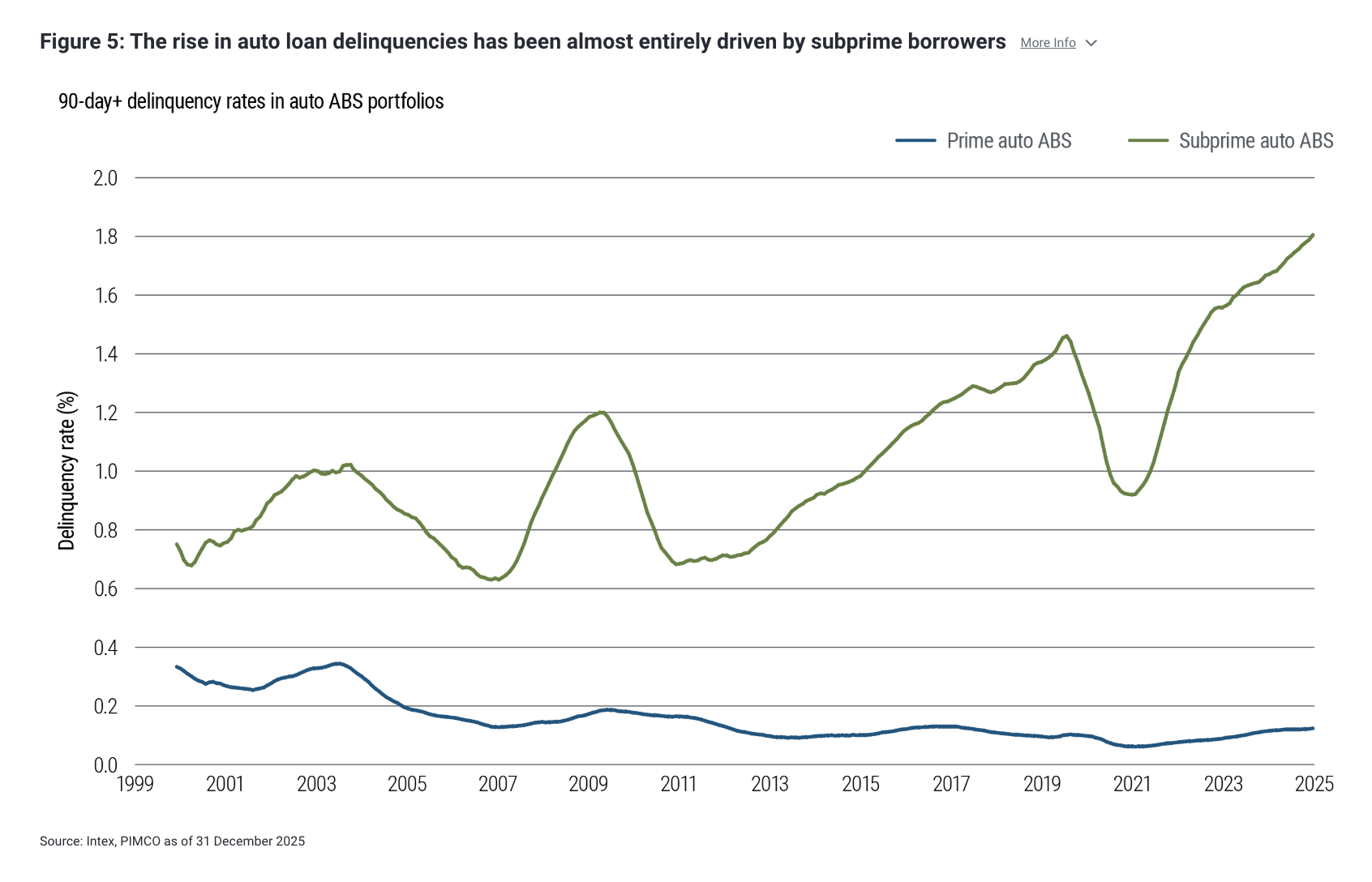

The K-shaped economy narrative has regained momentum as higher gas prices weigh more heavily on lower-income U.S. households than on others. As of year-end 2025, data from the Federal Reserve Bank of New York show credit card and auto loan delinquencies near two‑decade highs (see Figure 4), despite low unemployment and healthy aggregate metrics such as debt service and debt‑to‑income ratios.

Lower‑income households have largely exhausted excess savings and remain disproportionately exposed to elevated prices for essentials such as rent, insurance, and healthcare, while higher interest rates have raised debt servicing costs and tightened access to credit. The result is a bifurcated consumer: resilience at the top of the income spectrum and growing stress at the bottom.

Nowhere is this more apparent than in the auto loan market, where asset-backed securities (ABS) data indicate that the rise in delinquencies has been driven almost entirely by subprime borrowers (see Figure 5). At the start of the year, consensus economic expectations centered on stronger growth, easing inflation, and lower monetary policy rates helping to relieve pressure on subprime borrowers. The current backdrop challenges that narrative, leaving lower‑income households even more exposed.

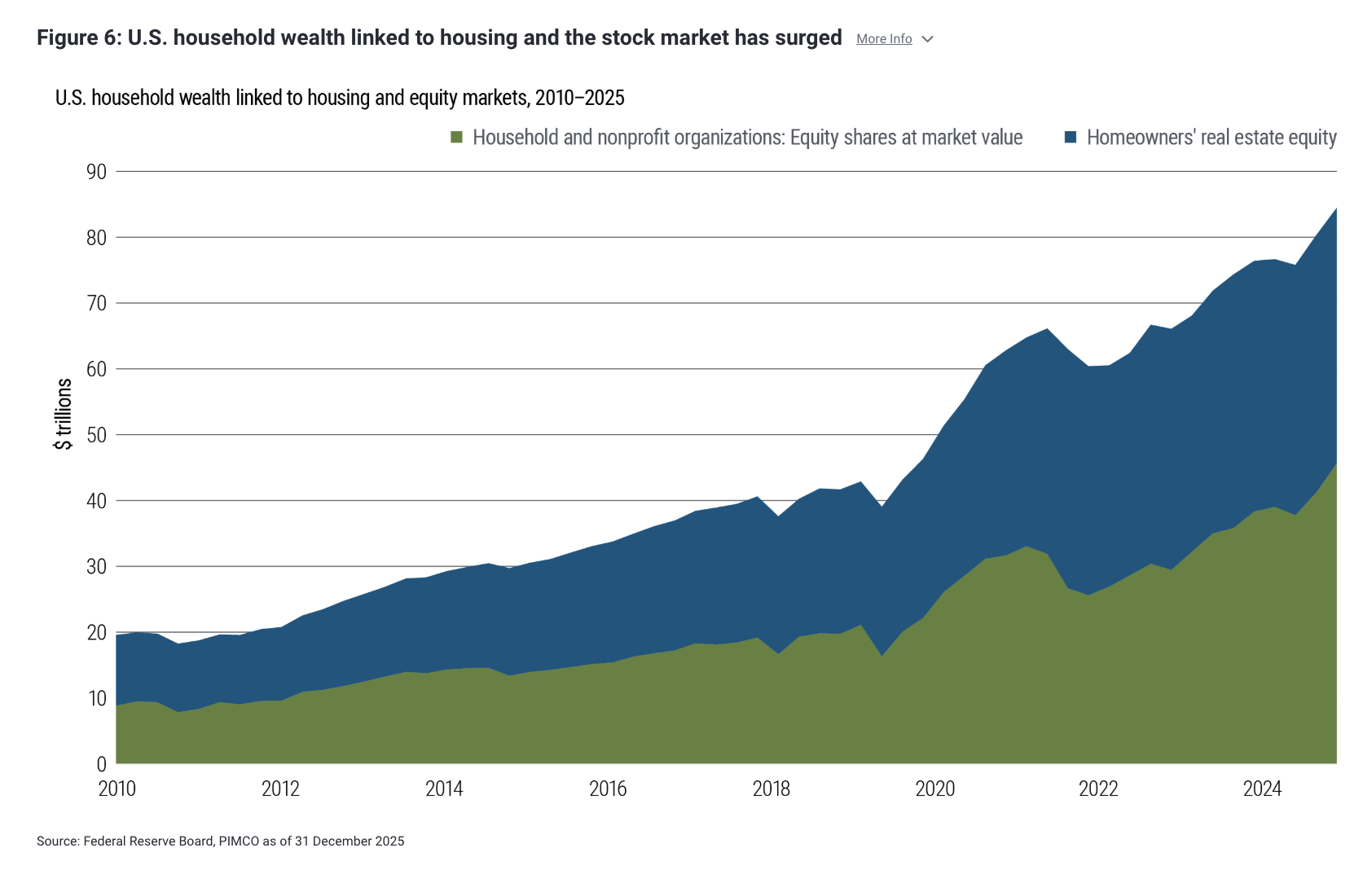

This bifurcation does not mean higher-income U.S. households are fully insulated from an economic slowdown. Here again, data from the Federal Reserve Board show that the combined value of household real estate equity and equity shares, a measure of household wealth tied to the housing and stock markets, has increased roughly fourfold since the end of the global financial crisis, far outpacing nominal GDP (see Figure 6).

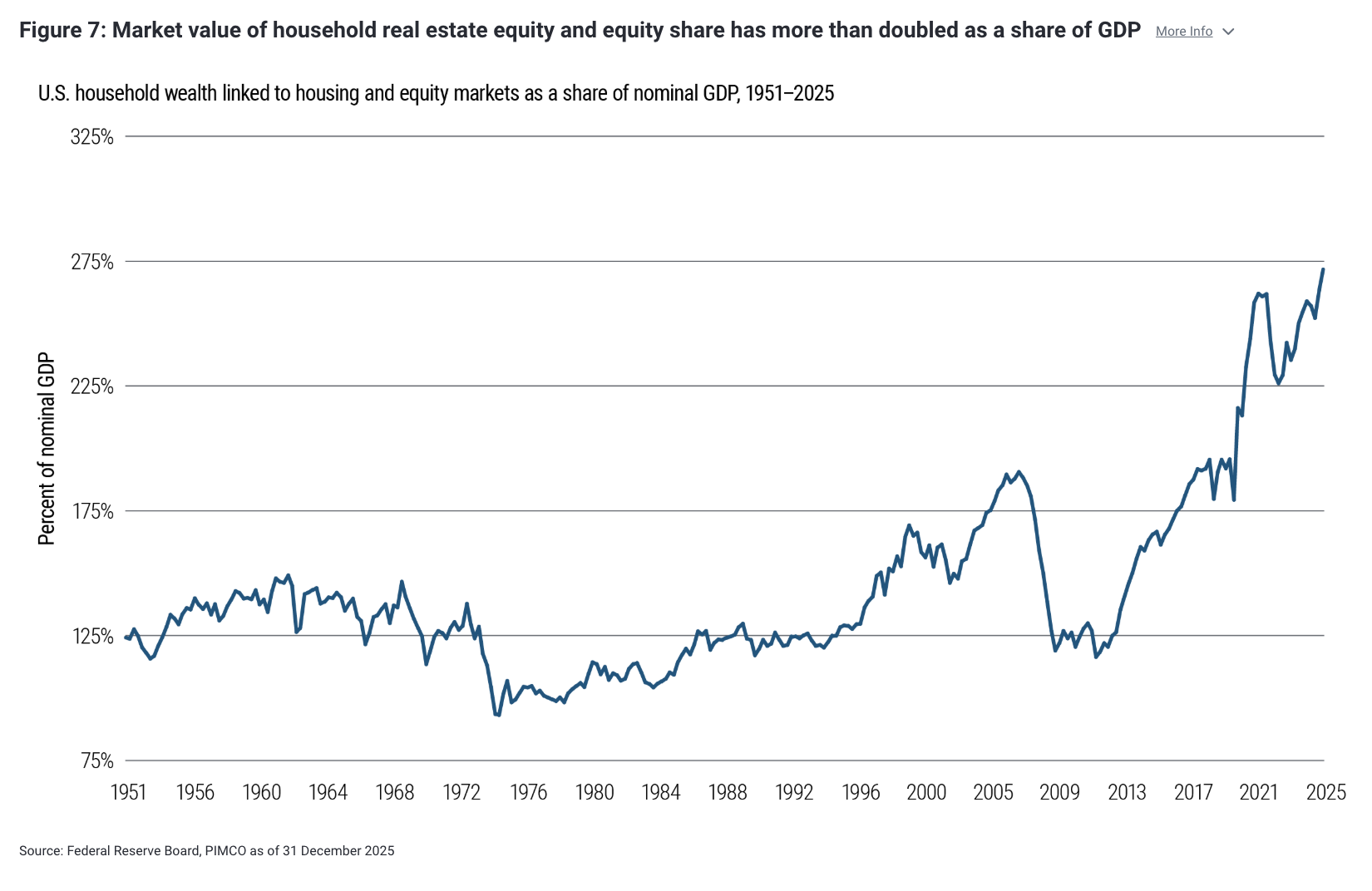

To put this in context, as a share of nominal GDP, the value of household real estate equity and equity share has risen from about 120% at year-end 2009 to roughly 271% as of year-end 2025, the highest level on record (see Figure 7).

Securitized products: Strong buffers, sharper fault lines

Despite the continued deterioration in fundamentals among lower-income households, the ABS market appears largely unfazed. At face value, spreads in benchmark ABS have shown little to no movement year-to-date. Does that signal complacency? Not necessarily.

The strong credit enhancement levels in senior ABS tranches – those highest in the capital structure – remain exceptionally robust, providing substantial buffer against underlying credit stress. That said, the primary market, where new deals are sold, is beginning to reveal a more nuanced picture. There, a clear bifurcation has emerged between prime and subprime collateral, with investors demanding greater compensation for lower-quality exposure.

The implication is straightforward: While headline spreads may appear stable, dispersion is likely to increase under the surface. In this environment, staying higher up in the capital structure and focusing on quality remain key.

Michael Puempel and Gabriel Cazaubieilh contributed to this report.

Disclosures

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Past performance is not a guarantee or a reliable indicator of future results. References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

All Investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Mortgage and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market’s perception of issuer creditworthiness; while generally supported by some form of government or private guarantee there is no assurance that private guarantors will meet their obligations. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0410-5385368

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO