Tax management is about more than just deferring taxes to reduce this year’s bite. It’s also about managing where and how taxes show up over time. For high-net-worth investors with diversified portfolios, permanently reducing taxes versus deferring them may bolster long-term after-tax wealth. Many investors overlook a potent tax reduction tool: bonds.

The Mechanics of Tax-Loss Harvesting with Stocks

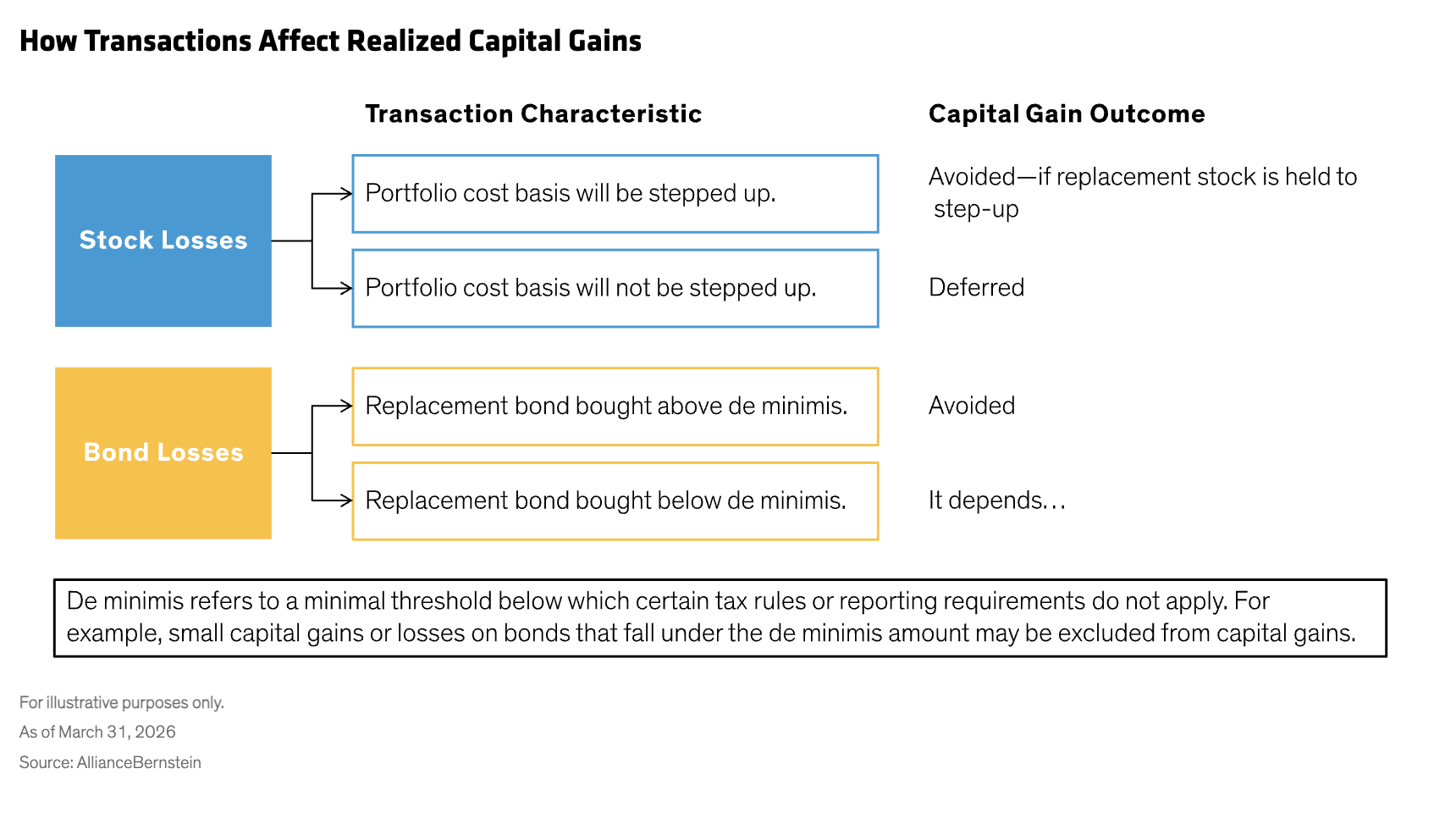

With tax-loss harvesting, realizing a loss on one stock can offset a realized gain elsewhere, reducing the current year’s capital gains expense.

Let’s say you previously bought 10 shares of ABC Corporation’s stock at $100 per share. Its cost basis is $1,000 (10 shares times $100). You sell the stock for $50 per share and reinvest the proceeds in a replacement stock; its cost basis would be $500 (the reinvested amount).

Your portfolio’s cost basis drops by $500 but its market value has already fallen. This increases the net unrealized gain, so future turnover will likely create a bigger realized gain or a smaller realized loss. You didn’t eliminate taxes, but you did alter when and how you’ll pay them.

Taxes Deferred Keep More After-Tax Dollars at Work

But the “kicking the can down the road” strategy of tax deferral can be effective, even if that can is bigger later on. With a reduced tax burden this year, you keep more after-tax dollars at work in your portfolio. If you invest smartly, you have the potential to boost your after-tax wealth by more than enough to pay the bigger bill later.

In truth, there’s really only one way to avoid having to pay more taxes in later years. That’s to never sell the replacement stock. If you die before selling it, the portfolio qualifies for a step-up in cost basis, eliminating the unrealized gain. But that “fix,” as we see it, restricts the ability of your investments to build the wealth you need to support your lifestyle.

Bonds’ Design Creates a Low Profile for Capital Gains and Losses

This dynamic raises a key question: is there a way to harvest losses without boosting future tax exposure? In our view, bonds can play a powerful and often overlooked role in this respect, making them a key part of the tax-loss harvesting tool kit in their own right (Display).

Much of it has to do with the way bonds work. When you sell a bond at a loss and reinvest the proceeds in another bond, that investment will mature at its face value, or par. Often, it does so without producing a taxable gain. The key is to buy the replacement bond generally at a price that’s above its par value and higher than the de minimis threshold.

Using this technique means that the difference between your portfolio’s market value and cost basis is not a reliable guide to your future capital gains. Of course, any bond can be sold before it matures at a price that creates a realized gain or loss. But bonds can also be held to maturity and—if they were bought above the de minimis threshold—don’t result in a capital gain or loss.

Bonds, particularly municipals, typically generate fewer capital gains over time, so investors can harvest losses today without significantly increasing future tax exposure. As a result, they may be especially effective for reducing or even fully offsetting smaller capital gains in a given year.

The Big Picture

As we’ve said before, investors should leave no stone unturned in boosting after-tax returns. In that effort, both stocks and bonds are useful in tax-loss harvesting. If you have only small capital gains to offset, it may make sense to start your tax-loss harvesting on the bond side of your portfolio.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. The views should not be considered to be legal or tax advice. The tax rules are complicated, and their impact on a particular individual may differ depending on the individual’s specific circumstances. Views are subject to revision over time.

Paul Robertson is the Chief Investment Officer of AllianceBernstein’s Tax Managed Strategies team, a part of the Equities department.

Gavin Romm is a Senior Vice President and Head of Separately Managed Accounts (SMA).

Mark Gleason is a Vice President, Managing Director and Head of the Americas Multi-Asset Business Development team, where he's broadly responsible for portfolio strategy and communications.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein