With Q1 earnings season well underway, it was Johnson & Johnson (JNJ) giving investors a peek at how the broader healthcare sector might perform. The healthcare giant beat expectations on Tuesday in revenue ($24.1 billion actual versus $23.6 expected) and earnings per share ($2.70 actual versus $2.66 expected). JNJ’s earnings could set a precedence on how healthcare-focused ETFs could perform given its strong presence in key funds.

Key Takeaways:

-

Johnson & Johnson’s Q1 earnings beat demonstrates how a strong MedTech division and innovative oncology drugs can successfully offset revenue headwinds from increased competition in legacy pharmaceutical products.

-

Investors can choose between high-conviction pharmaceutical exposure via or broad-based healthcare stability through ETFs.

-

As the healthcare sector lags the broader market in 2026, JNJ’s aggressive investment in immunology and medical devices highlights the importance of quality and product diversification for navigating the industry.

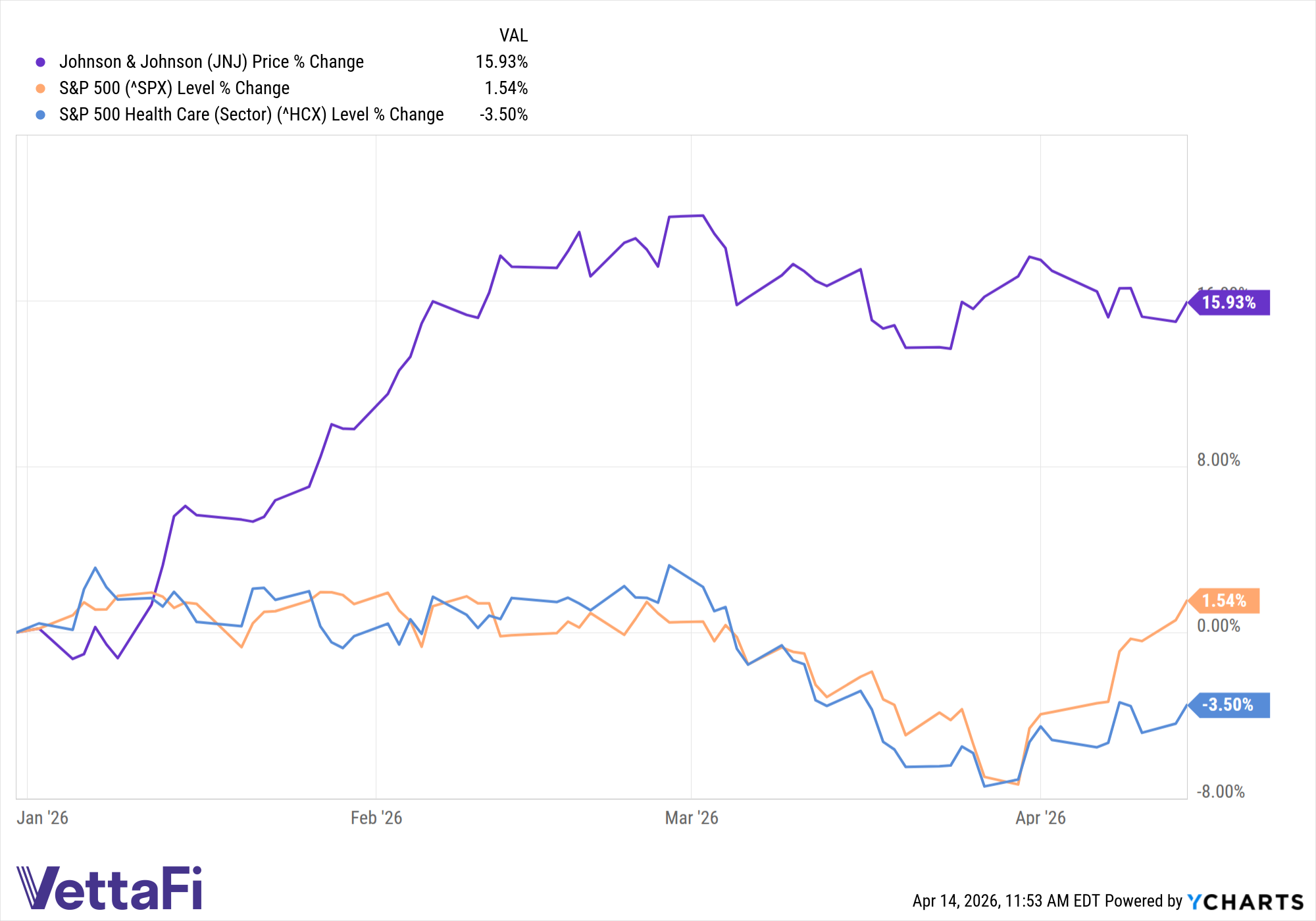

Relative to the S&P 500 indexes, the healthcare sector has been lagging the broader sector this year. However, JNJ’s stock is up nearly 16% thanks to strong demand for its cancer drug Darzalex and psoriasis treatment Tremfya as well as its strengthening medical technology division.

JNJ data by YCharts

Pharma Headwinds, MedTech Strength

According to Reuters, Johnson & Johnson posted a Q1 profit despite its psoriasis treatment, Stelara, showed signs of lagging sales. Stelara has been the company’s prime revenue generator, but it’s facing increased peer competition, which has kept investors on edge. However, the company’s Innovation Medicine did grow its operational sales by 7.4%.

Additionally, the healthcare giant’s Q1 beat was helped by strength in its MedTech division, which saw operational sales grow by 4.6% globally. With elective surgeries returning to their pre-pandemic levels, JNJ’s recent acquisitions in the cardiovascular space is bolstering their medical device sales. As result, this can help offset any weakness in drug sales in the interim.

That said, this dual structure of long-cycle drug development and high-margin surgical-orthopedic tools gives JNJ its competitive advantage in 2026.

See More: Healthcare Exposure Focused on Big Pharma? You’re Missing Out

Gaining JNJ Exposure

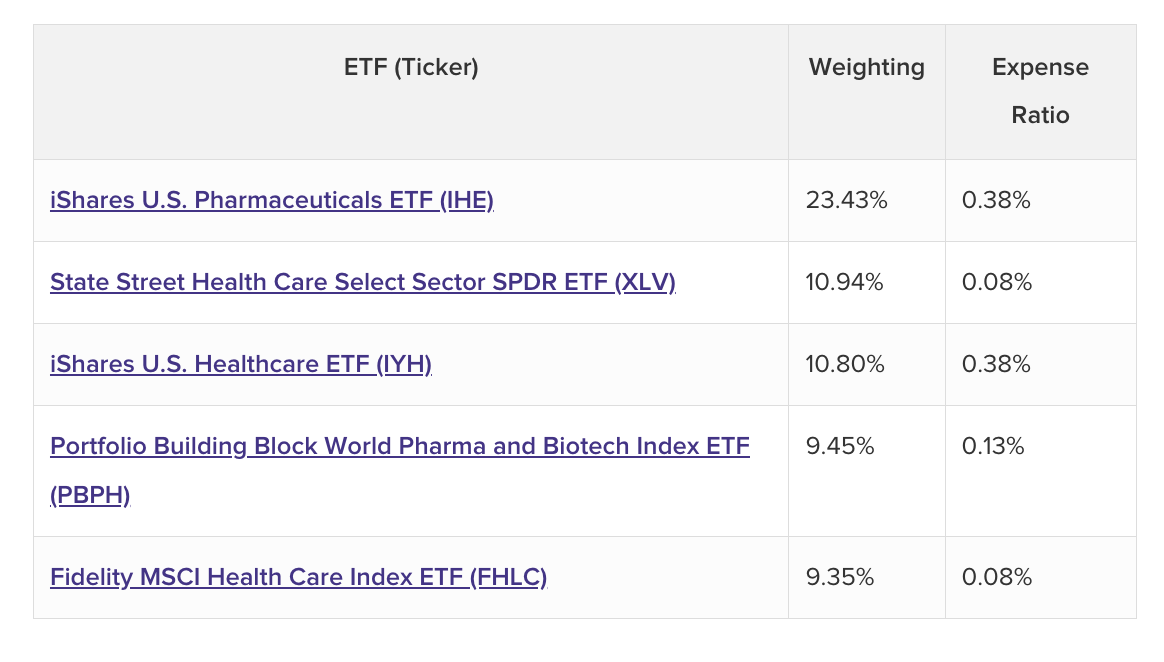

JNJ has a prominent presence in healthcare/biotech/pharma indexes. According to data from ETF Database, here are the five ETFs with the highest allocations to Johnson & Johnson as of April 2026:

At the top of the weighting heap is IHE, which offers high-conviction exposure to the U.S. pharmaceutical industry. The fund targets companies engaged in the research, development, manufacture, and sale of pharmaceutical products. In contrast, those looking for broad healthcare exposure will want to consider the next two funds instead.

At eight basis points apiece, XLV and FHLC present the most cost-effective options of the aforementioned quintet. The former adds exposure to the broader healthcare sector names in the the S&P 500, making it an ideal benchmark for large-cap U.S. healthcare performance. The latter tracks the MSCI USA IMI Health Care Index, giving it greater market cap diversification across large, mid, and small-cap companies.

IYH adds additional diversification within the broader healthcare scope. It tracks the Russell 1000 Health Care RIC 22.5/45 Capped Index, which adds exposure to large- as well as mid-cap companies across pharmaceuticals, biotech, and medical equipment.

Global Biotech & Pharma

Finally, for a global exposure to biotech and pharma, PBPH is the play. It tracks the BITA Global Pharma and Biotech Select Index, which offers exposure to companies in developed markets (domestic and international) that derive a significant amount of their revenue from the discovery and commercialization of human therapeutics.

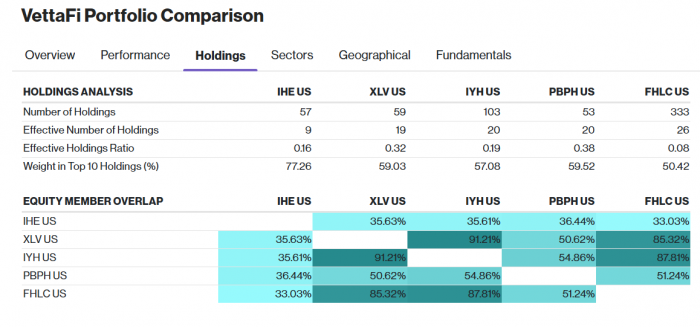

Given their sector focus, broader healthcare or more specifically biotech/pharma, there will be some parity amongst the funds in terms of holdings. Those in the broader healthcare sector will see the most overlap so it’s ultimately up to the investor how they want to tilt their exposure.

See More: AI Opens The Door to This Active Healthcare ETF

Innovative Medicine Focus

As markets delve deeper into 2026, JNJ is focused on its innovative medicine offerings. Moreover, the company is aggressively investing in oncology and immunology, which can help to offset any further revenue loss from Stelara.

For ETF investors, funds like IHE and XLV can take advantage of JNJ’s innovative medicine focus while also providing broad-based exposure to healthcare innovations through their respective holdings. The biotech industry, in particular, can be a tricky space to navigate as expertly noted in a whitepaper by Verdad Capital.

For financial advisors and investors, an emphasis on quality as well as diversification can help navigate the multi-faceted healthcare industry. Whether through a pure healthcare sector play or a biotech focus, ETFs can provide this level of access through a tax-efficient, cost-effective, and flexible investment vehicle.

Originally published on ETF Trends

For more news, information, and strategy, visit ETF Trends.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi