The US dollar's obituary has been written many times—with increasing frequency over the past year. Each time we get a fresh round of analyses declaring that de-dollarization is accelerating, the world is reorganizing its financial architecture around alternatives and the greenback's reign is drawing to a close. Most recently, a Deutsche Bank (DB) Research Institute report1 argues that the conflict in the Middle East represents a "perfect storm for the petrodollar." A catchy tag line, but the report exemplifies the weakness of most dollar-doom analyses: they focus on one side of the equation and miss the full picture.

The petrodollar argument—and why it misses the point

The “Petrodollar Thesis” in a nutshell goes as follows: the global dominance of the dollar rests, to a crucial extent, on the fact that global oil trade is denominated in US dollars (USD). This goes back to the petrodollar arrangement formalized between the United States and Saudi Arabia in 1974, which tied dollar invoicing of oil exports to US security guarantees. Because oil is central to global manufacturing, this arrangement boosted dollar demand across the entire global trading system—not just in energy markets. The DB report argues that this arrangement is now fraying: 85% of Middle Eastern crude oil goes to Asia rather than the United States; Saudi Arabia is localizing defense under Vision 2030; Iran's oil exports are increasingly priced in renminbi through agreements with China; and with the war in Iran, the United States has actually brought turmoil to the Middle East, undermining regional security.2 Therefore, the argument goes, oil trade will be increasingly priced in currencies other than the dollar, and the dollar's decline will become inevitable.

This view is remarkably simplistic, in my view. In fact, it gets the causation partly backwards. Oil is not priced in US dollars simply because the United States has long acted as the world's policeman. Oil exporters have a strong self-interest in getting paid in USD, because of what dollars represent: access to the deepest, most liquid capital markets in the world, backed by an institutional and legal framework that protects property rights and enforces contracts, supported by a strong, dynamic, and innovative economy. Three pillars sustain this.

- The US economy's scale and dynamism. The United States produces roughly 25% of global gross domestic product (GDP) at market exchange rates. It remains the largest single destination for global capital flows. Even with elevated debt and fiscal concerns—which I take seriously—US nominal growth has consistently supported returns that attract foreign investment.

- Institutional credibility. The Federal Reserve (Fed) is among the most credible central banks in the world. US courts enforce contracts. The rule of law in US capital markets is not a platitude; it is a quantifiable factor that reserve managers price when deciding where to hold their savings. The European Central Bank's 2025 “international role of the euro” report underscores that the euro area, despite meaningful progress, remains constrained by fragmented capital markets and the absence of a unified safe-asset market at the scale of US Treasuries.

- Unmatched market depth. A reserve manager in Riyadh or Delhi who wants to park US$50 billion overnight has one serious option: dollar markets. The renminbi cannot absorb that flow—China's capital account remains substantially closed, renminbi-denominated assets have limited convertibility, and China's legal system does not provide the external-creditor protections that dollar markets do.

No credible alternative exists

These strengths are currently unrivaled. What is the alternative? The euro area cannot issue a unified safe asset at sufficient scale. The renminbi operates behind capital controls and lacks convertibility. Digital currencies—whether central bank digital currencies such as those underpinning Project mBridge, or private stablecoins—settle transactions but do not provide the store of value function that reserve currency status requires. A basket of currencies is not a reserve currency; it is an accounting convention. And most stablecoins are anyway denominated in US dollars.

The US dollar's real competition, in my mind, is not yet on the horizon. Not because alternatives are inconceivable in principle, but because building the institutional infrastructure required—deep markets, rule of law, full convertibility, a track record of macro stability—takes decades, not years.

Dollar dominance: what the data show

That is where most predictions of the dollar's demise fall short. Some have pointed to signs of weakness in the US economy. Others have argued that the weaponization of the dollar-based financial system in geopolitics provides an overwhelming incentive for countries to move away from the dollar. Others still argue that the current administration is terminally undermining the robustness of US institutions. Even though there might be a grain of truth in all of these observations, none of them moves the needle.

Consider the evidence across the four key functions that define reserve currency status.

- According to the International Monetary Fund's Currency Composition of Official Foreign Exchange Reserves data for the fourth quarter of 2025—covering a total foreign exchange (FX) reserve pool of US$13.14 trillion—the dollar accounts for close to 57% of allocated reserves, with the euro at 20% and the renminbi at 2%. The dollar has drifted down from a peak of around 72% in 1999 but remains dominant by a wide margin.

- In cross-border payments, according to Fed staff compilations of SWIFT (the Society for Worldwide Interbank Financial Telecommunication) messaging data, the US dollar's share of international payments rose from 31.8% in 2010 to hover around 50% by early-2026—while the euro fell from 40.4% to 22.8%. Trade finance remains even more concentrated: SWIFT's March 2026 Global Currency Tracker puts the dollar's share of documentary credits and collections at approximately 82%.

- In FX markets, the Bank for International Settlements 2025 triennial survey finds the dollar on one side of 89% of over-the-counter FX turnover, compared to just 8.5% for the renminbi.

- US Treasury markets—the deepest pool of safe assets in the world—stand at US$30.6 trillion outstanding as of February 2026, with average daily secondary-market trading around US$1.29 trillion, according to the Securities Industry and Financial Markets Association. No other sovereign bond market comes close.

These are not the metrics of a currency in decline. They are the metrics of a currency under mild pressure at the margin—pressure that has been simmering for two decades without producing a fundamental shift.

The dollar's weakness is cyclical, not structural

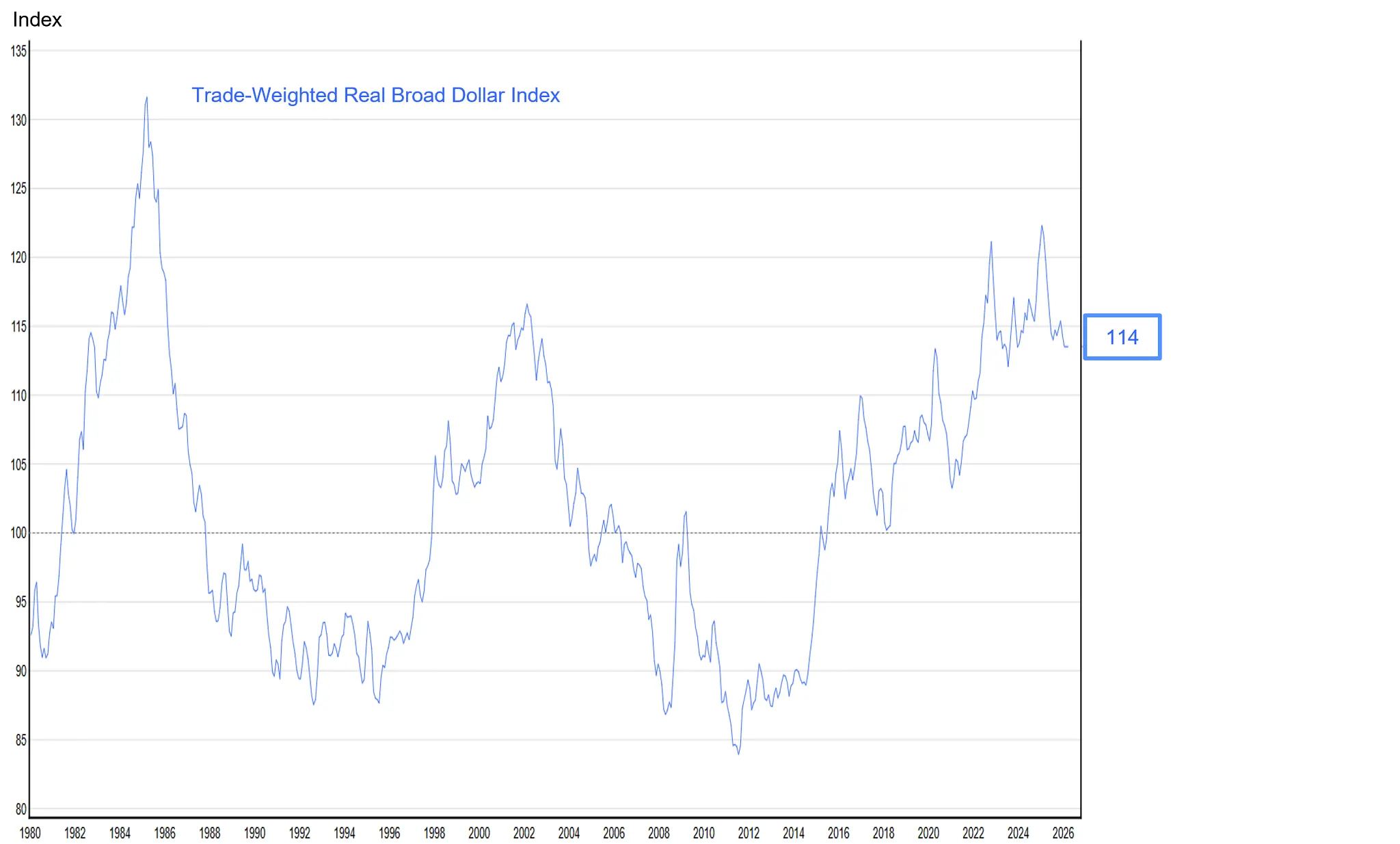

The USD has depreciated meaningfully over the past year, and some commentators have pointed to this as evidence of structural decline. I see it differently. In broad, real, trade-weighted terms, the dollar remains well above its troughs of the mid-1990s and the late 2000s—levels at which no serious analyst argued dollar primacy was ending. Some dollar softness is perfectly consistent with global reserve currency status. Unlike the renminbi, the dollar is a freely floating currency. It floats. Up and down.

Trade-Weighted Real Dollar Remains Overvalued Despite Meaningful Weakness Over the Past Year

1980-2026

The dollar's genuine vulnerability

The dollar's own worst enemy is US fiscal policy. Federal debt held by the public is projected by the Congressional Budget Office to exceed 110% of GDP by 2032, with no credible consolidation plan currently on the legislative table. Sustained deficits at this scale risk, over time, undermining the very institutional credibility that makes dollar assets attractive. However—and this is crucial however—virtually every major competitor faces the same problem. The euro area's debt-to-GDP ratios are elevated; Japan's are higher still; and China's total debt load, including local government financing vehicles, is hardly reassuring.

What this means for investors

I remain constructive on the dollar's reserve currency status over the foreseeable horizon. The dollar faces headwinds, and we are currently in a highly volatile environment. Investors would be wise to stay nimble about currency exposure at the margin—the dollar's real effective exchange rate remains to be determined by shifting growth differentials and fiscal paths. But the US dollar also enjoys a resilient set of tailwinds, with no credible competitors currently on the horizon. Some marginal erosion of its dominance is possible, perhaps even likely. But replacement appears unrealistic. I see no basis for positioning as though reserve currency displacement is imminent. The dollar's dominance, for now, remains unchallenged.

This, I repeat, is fully compatible with phases of cyclical weakness. And this is even more true when we look at key bilateral exchange rates. Against the yen, for example, the dollar is clearly overvalued and therefore on a fundamental basis the Japanese currency seems set to appreciate. Against the euro, by contrast, the dollar is much more fairly valued on a fundamental basis and even has room to gain ground. Europe's economy continues to suffer from structurally lower productivity growth compared to the United States, and it is much more vulnerable than the US economy to the current energy shock, since Europe depends on imports for about 60% of its energy needs, whereas the United States is an energy exporter.

Therefore, I believe that investors are probably better advised to look at fundamentals and focus on moves in bilateral exchange rates, rather than betting on an end to the dollar dominance regime.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

EndNotes

1Source: “What Iran means for the dollar: a perfect storm for the petrodollar.” Deutsche Bank. March 2026.

2Ibid.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments.

Currency management strategies could result in losses if currencies do not perform as expected.

The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

There is no assurance that any estimate, forecast or projection will be realized.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton

Read more commentaries by Franklin Templeton