Key takeaways:

- Much of the conversation around private credit versus public high yield focuses on yield levels, default expectations and headline volatility. But we think what matters most is how each market lets investors measure, manage and reprice risk as conditions change.

- Public high yield’s advantages—transparent pricing, broad issuer access and an active secondary market—can be especially valuable late in the cycle, when fundamentals can shift quickly and refinancing outcomes can become path dependent. Just as importantly, high yield’s structure can create opportunity; technical driven moves, index and flow effects, and episodic dislocations can reward experienced, well resourced fundamental investors with longer time horizons. In that context, the question is not simply which market offers more investment carry today, but which structure offers better tools for credit selection, relative value and downside mitigation as dispersion rises.

Stability versus flexibility

Private credit has benefited meaningfully from the sustained retrenchment of banks, allowing private lenders to step into senior positions with stronger controls over documentation and, often, attractive all in yields. For many portfolios, the appeal is straightforward: floating rate income, structural seniority, and a smoother reported return profile. The tradeoff is that the same features that create stability can also delay valuation adjustment and reduce flexibility. Price discovery tends to move more slowly, and periods of stress are often addressed through amendments, maturity extensions, and in some cases, payment in kind features—where interest is paid by adding to the loan balance rather than in cash—rather than immediate market clearing. Outcomes can therefore be highly dependent on underwriting quality, documentation terms, borrower concentration and a manager’s workout capability. Public high yield, by contrast, supports continuous issuer level credit work, sector rotation and relative value decisions across a broader, more diversified opportunity set as fundamentals evolve.

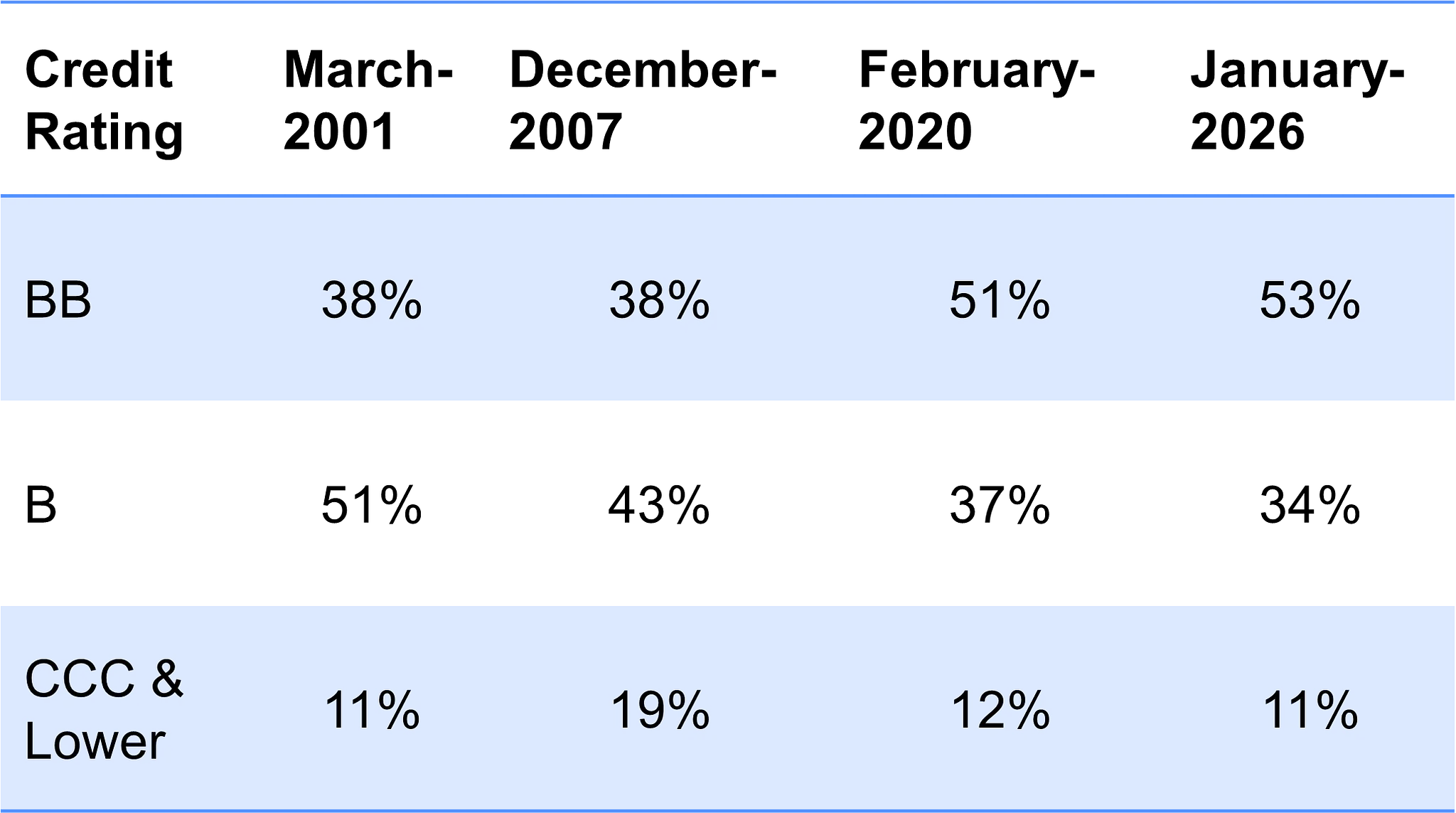

High Yield Credit Quality Has Improved

January 31, 2026

The growth of private credit has influenced the public high yield market at the margin, particularly in sponsor‑backed financings where private, floating‑rate solutions can be attractive to issuers. Since the global financial crisis, the high- yield universe has generally improved in overall credit quality, with a larger share of BB and higher‑quality single‑B exposure than in prior cycles. The market’s evolution is better described as increased dispersion—a smaller cohort of CCC/distressed issuers alongside a substantial base of larger, repeat issuers with improving balance sheets and established capital markets access. For investors, that breadth is a feature. Public high yield provides a deeper opportunity set for issuer selection, capital structure and recovery analysis. And it offers relative value across sectors and structures with multiple pathways to refinancing (bonds, loans, equity, and liability management options) as conditions evolve.

Liquidity as a source of alpha, not just optionality

Liquidity is often described as the defining advantage of public high yield—and it is a meaningful one. In practice, liquidity and transparent pricing provide investors with two things private credit cannot consistently replicate: the ability to actively manage exposure and the ability to see risk reprice quickly when new information emerges. That speed is not the same as “perfect efficiency.” High yield can be technical‑driven and episodically inefficient, with flows, market structure and risk‑off episodes creating overshoots in both directions. For long‑term, fundamental investors, those dislocations can be a source of alpha—enabling rotation into improving credits, allowing disciplined reduction of deteriorating issuers, and adding selective risk when spreads over‑compensate for fundamental risk. By comparison, illiquidity in private credit can be appropriate when terms and protections are strong, but the loss of flexibility can be costly if fundamentals weaken faster than documentation can protect.

Sector Diversification: Public High Yield and Business Development Company Ownership

Portfolio implications in a more dispersed credit cycle

Across both markets, manager skill plays an important role—but public high yield gives skilled managers a broader toolkit. In private credit, return dispersion is widening as origination standards, covenant packages, and workout experience drive outcomes, with limited ability to adjust exposures quickly. In public high yield, alpha increasingly comes from proactive credit work, including issuer selection, capital structure analysis, recovery math and relative value across sectors and ratings, supported by ongoing engagement with management teams, lenders and industry counterparts. As refinancing walls approach and fundamentals diverge, simply owning broad market exposure is unlikely to be sufficient; the ability to continuously reassess credits, test assumptions against new information, and reposition where the risk/reward is most attractive can be a differentiator.

For portfolio construction, we believe the implication is not that private credit has no role—but that public high yield offers distinct advantages when transparency and active risk management matter most. Public markets can provide diversification, a broad investable universe, and the ability to express issuer‑level views as dispersion creates both risk and opportunity. Private credit can be additive when investors are being paid for illiquidity with meaningful structural protections and when manager underwriting and workout capabilities are demonstrably strong. In today’s environment, many portfolios may benefit from pairing public exposure with selective private allocations where terms are compelling—seeking to capture income while maintaining resilience as the credit cycle evolves.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls.

Investment strategies involving Private Markets (such as Private Credit, Private Equity and Real Estate) are complex and speculative, entail significant risk and should not be considered a complete investment program. Such investments should be viewed as illiquid and may require a long-term commitment with no certainty of return. Depending on the product invested in, such investments and strategies may provide for only limited liquidity and are suitable only for persons who can afford to lose the entire amount of their investment. Private investments present certain challenges and involve incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity. There also can be no assurance that companies will list their securities on a securities exchange, as such, the lack of an established, liquid secondary market for some investments may have an adverse effect on the market value of those investments and on an investor's ability to dispose of them at a favorable time or price.

Diversification does not guarantee profit or protect against risk of loss.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton

Read more commentaries by Franklin Templeton