Quarterly Review and Outlook First Quarter 2026

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOil Shocks

Oil shocks hitting economies with weak demand and strained balance sheets are especially damaging. Firms cannot fully pass on rising costs, so margins shrink, layoffs increase, and investment falls. Tightening monetary and credit conditions would cause inflation to fade faster but job losses, failures, and fragile household finances to be much worse.

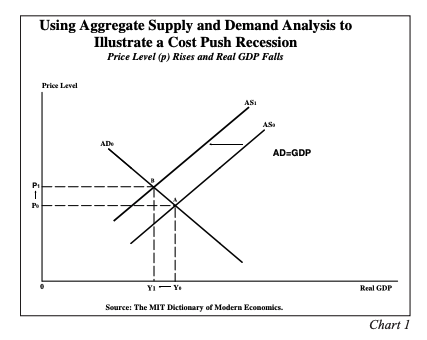

The word “stagflation” is often used to capture the economic consequences of an oil shock, mainly because it gained prominence in the 1970s and serves as a convenient label for the rare mix of inflation and slowing growth. Yet this label misleads, since it implies economic stagnation rather than the actual reduction in real activity that follows oil shocks. More precise terms include “supply-side recession” or “cost-push recession,” which shift the aggregate supply curve inward (Chart 1, from AS0 to AS1), lowering output (real GDP) and increasing prices (P). The Russian invasion of Ukraine did not meet this criterion, since, simultaneously, the aggregate demand (AD) curve was being shifted outward in response massive domestic and global demand stimulants in response to COVID. Without the stimulus, the AD curve remains stationary, as depicted in Chart 1.

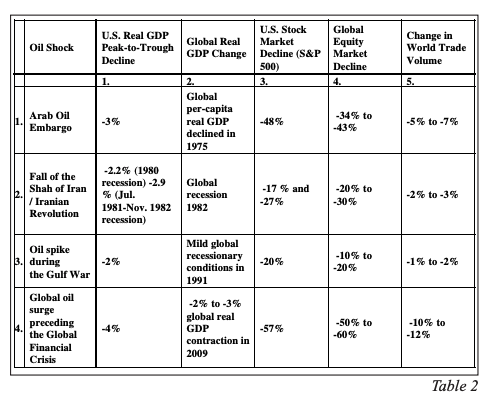

When an economy is already under strain, oil shocks can accelerate downturns more quickly than most typical business cycle lags (Table 1). For instance, just a month after the 1973 Arab Oil Embargo, the U.S. entered a recession lasting into late 1974. The 1979 Iranian Revolution caused a surge in oil prices, and within eleven months, the U.S. entered the 1980 recession, the first of two in three years. In 2007, oil production disruptions in Nigeria and Venezuela, along with rapid Chinese growth, drove prices up, and within five months, the U.S. was in the midst of the Global Financial Crisis. In each scenario, higher oil prices acted as a catalyst for major economic problems already stirring. When Iraq invaded Kuwait in August 1990, a similar effect may have occurred, but a recession had already started a month earlier.

Read more: How to Future-Proof the Global Economy

A Global Event

When oil prices spike in already weak or financially strained economies, negative effects compound domestically and globally. Oil shocks raise production and distribution costs, fueling inflation while reducing output and employment. In debt-burdened economies with slow growth, higher energy costs erode real incomes and profits, prompting households to cut spending and businesses to delay investment or trim payrolls. If other economies are also distressed, global trade and export demand fall, deepening the downturn. The four major cost-push recessions were global events, significantly reducing real GDP, stock prices, and world trade volume in each case (Table 2).

An Ill-Equipped Fed

The Federal Reserve faces a dilemma when an oil or supply shock occurs. Raising interest rates to curb inflation suppresses demand and deepens recession, while cutting rates to support growth risks fueling more inflation as oil price increases spread. In 1973, the Burns Fed first loosened policy, worsening inflation, then imposed prolonged tightening, making the recession deeper and longer. Because monetary policy almost entirely influences demand, not supply, either approach risks aggravating one side of the problem. This trade off becomes even more acute when the economy is already weak, as in past episodes.

Although not an issue in the decision making, the Fed’s choice to hold the policy rate steady in March is backed by economic logic. The Fed's forecast says rates will stay about the same through 2026. This trajectory is also consistent with theory.

Do-Nothing Option

If neither the central bank nor fiscal policy makers choose to intervene and allow a downturn caused by higher costs to play out, the initial burst of price increases from rising production costs tends to subside as the slowdown deepens. As job losses mount and incomes shrink, both households and businesses tighten their belts. This makes it harder for firms to continue raising prices, so upward pressure on costs typically peaks and then fades as overall spending drops. However, output and employment can remain subdued until business expenses ease or the external disturbance recedes. In this way, the slowdown itself eventually reins in price escalation, though at the cost of weaker economic performance and more unemployment in the meantime.

In a classic oil-shock-driven cost-push recession, a restrained policy mix tends to cause the least harm. Broad demand stimulus should be avoided as amplifying inflation poses a significant risk. Fiscal policy can boost oil production through incentives, investment, and reforms that encourage efficiency and output, but these measures often take time to have an effect and face significant political obstacles to implement. This approach helps limit the entrenchment of higher inflation expectations and preserves central bank credibility, allowing the shock to dissipate as markets adjust. However, this strategy requires accepting slower growth and weaker labor markets, which can be politically and socially challenging. Although a completely passive stance is rarely optimal, maintaining a steady, non-accommodative monetary policy can cushion the downturn without reigniting inflation. By contrast, aggressive demand-side intervention would likely worsen the trade off between inflation and output rather than resolve the imbalance.

Economic theory strongly rejects the logic of the phrase “never let a crisis go by without massive new governmental stimulus.” This view may be popular, but for an economy in a supply-side recession, such programs would have a deleterious effect. Such an action would add to the growing list of policy failures, a topic to be discussed later.

Distressed Conditions - Then and Now

The current oil shock is striking an economy already burdened by distressed labor and financial markets. Employment growth slowed sharply entering 2025, with QCEW revisions indicating almost no job gains between the third quarters of 2024 and 2025, highlighting weak labor momentum and constrained household incomes. Financial stress is also rising and both consumer and corporate loan delinquencies are up, bankruptcies are increasing, and over-leverage in real estate is creating vulnerabilities. Business Development Corporations face liquidity and portfolio risk from distressed borrowers, private fixed-income funds struggle with losses on high-yield holdings, and private equity portfolios face declining valuations and higher refinancing costs. Contagion risks are evident: stress in one segment can spill over into credit markets, amplifying systemic risk.

These stresses set the stage for a pattern observed in prior major oil shocks: the 1973 Arab Oil Embargo struck amid rising inflation and slowing growth; the 1979 Iranian Revolution occurred when unemployment was already creeping up; the 1990 Iraq-Kuwait crisis coincided with a cyclical slowdown; and the 2007–2008 multi-factor oil shock hit during severe financial strains tied to the housing and banking sectors. In all cases, oil shocks compounded pre-existing weaknesses. Today, the combination of sluggish employment, downward payroll revisions, fragile household and corporate balance sheets, and heightened financial vulnerabilities leaves the economy unusually susceptible to a contractionary and destabilizing response to even a moderate rise in energy costs.

Past Policy Failures

Structural imbalances and recent policy decisions have heightened the economy’s vulnerability to the current oil shock. Much of today’s instability stems from the coordinated monetary and fiscal response during the pandemic. While these actions kept the economy afloat, they also fueled lasting weaknesses. Ultra-low rates and large-scale relief drove up debt across households, businesses, and alternative lenders, increasing leverage in real estate, private credit, and private equity. Pandemic stimulus spurred a surge in demand for homes and vehicles, pushing prices to record highs and straining affordability for major purchases—key drivers of consumer spending and growth. At the same time, strong demand fed persistent inflation, eroding real incomes and weakening the labor market. By prioritizing immediate relief over long-term resilience, these policies left the economy more exposed to risks from energy shocks, defaults, and financial stress.

Positive Initial Conditions

Unlike during earlier oil shocks, U.S. households are receiving substantial tax refunds, and the country is largely energy self sufficient—a sharp contrast to its past dependence on foreign oil. Both factors could buffer the impact of the current oil shock. As an oil exporter, the U.S. now keeps higher energy spending at home when prices rise. Prolonged disruptions may prompt producers to ramp up output and hiring, but this effect will take far longer than the disruption to household budgets.

Energy Production: Energy Self-Sufficiency: China, Japan, and the EU are highly dependent on oil imports, relying on imports for about 75%, 99%, and 95% of their oil and gas, respectively. In contrast, while the US does import oil, its domestic production of oil, natural gas, and related products exceeds its domestic energy consumption. As a result, US energy costs are likely to rise much more slowly than in the world’s second-, third-, and fourth-largest economies. This energy advantage could encourage globally active businesses to view energy availability as a critical factor in choosing where to locate operations—an important plus for the US economy.

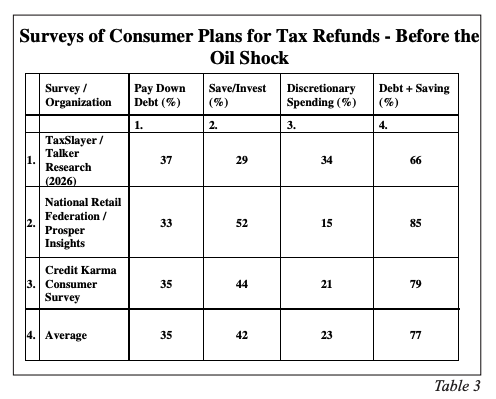

Tax refunds: Before the shock, surveys showed that most Americans planned to save, invest, or pay down debt with their current refunds, prioritizing financial security over immediate spending (Table 3). This mirrors past tax cuts, which initially boosted household balance sheets before eventually boosting consumption and growth over the longer term.

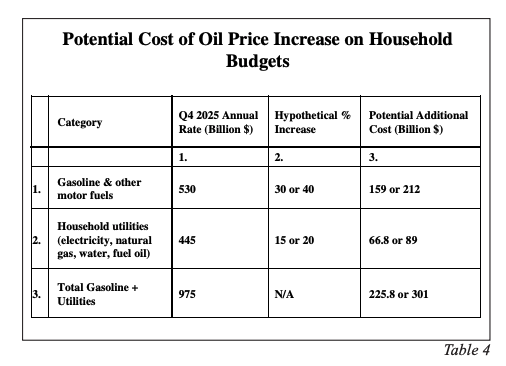

The tax benefit could be wiped out if the oil shock persists (Table 4). A 30% jump in fuel prices plus a 15% rise in utilities would cost consumers an extra $226 billion this year; with a 40% and 20% increase, costs exceed $300 billion—about the size of the 2026 tax cut. In this scenario, households could absorb higher energy bills but lose the chance to strengthen their finances.

Outlook

Oil shocks hitting economies with weak demand and strained balance sheets are especially damaging. Firms cannot fully pass on rising costs, so margins shrink, layoffs increase, and investment falls. Inflation fades faster, but contractions are deeper: job losses mount, failures rise, and fragile household finances and tight credit amplify each shock.

Distressed conditions shape the Fed’s response. With weak demand and fragile finances, the Fed is unlikely to tighten policy against temporary supply-driven inflation, as this could deepen the downturn. Instead, it should tolerate a brief inflation spike, let recessionary forces cool prices while avoiding moves that worsen instability.

While the Fed holds the policy rate steady, long-term Treasury yields are likely to be volatile as news of a recession and inflation play off each other amid markets' reactions to Iran-related news. Prior situations, however, suggest that faster inflation will be reflected more quickly in the widely followed indicators than in the deteriorating real economic measures. Historically, an inflation surge is often slow to reverse as Middle East oil production has not recovered quickly. In this environment, longterm Treasury bond yields are expected to rise, even though the oil shock has further aggravated the already distressed US economy.

Van R. Hoisington

Lacy H. Hunt, Ph.D.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

The information in this market commentary is intended for financial professionals, institutional investors, and consultants only. Retail investors or the general public should speak with their financial representative. Information presented is for educational purposes only and does not constitute an offer or solicitation for the sale or purchase of any securities, investment products or advisory services.

Information herein has been obtained from sources believed to be reliable, but HIMCo does not warrant its completeness or accuracy; opinions and estimates constitute our judgment as of this date and are subject to change without notice. This memorandum expresses the views of the authors as of the date indicated and such views are subject to change without notice. HIMCo has no duty or obligation to update the information contained herein. This material is intended as market commentary only and should not be used for any other purposes, including making investment decisions. Certain information contained herein concerning economic data is based on or derived from information provided by independent third-party sources. Charts and graphs provided herein are for illustrative purposes only.

This memorandum, including the information contained herein, may not be copied, reproduced, republished, or posted in whole or in part, in any form without the prior written consent of HIMCo.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All