Key takeaways:

- Credit risk in the software sector may still be understated, as weaker growth and less reliable sponsor support could push defaults higher over time, even as refinancing pressure remains low.

- If the sector weakens further, history suggests losses could be larger than investors expect, as relevant past periods of heavy stress have led to below‑average recoveries, not just more defaults.

- Private credit valuations may look stable but could reset quickly under stress, as uneven and opaque business development company (BDC) price marks raise the risk of a sharp repricing.

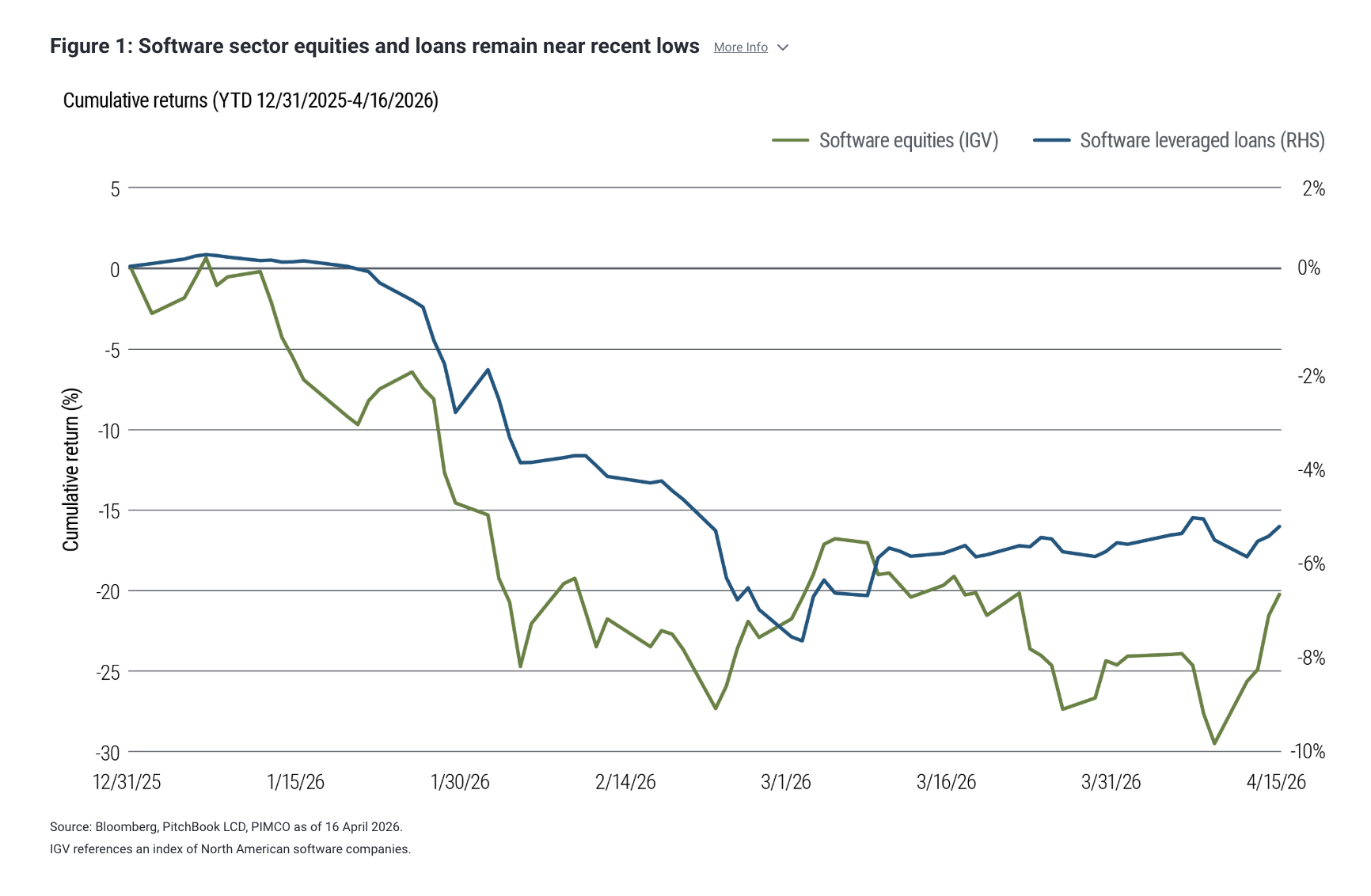

The software sector remains stuck in a trough across the capital structure. Software equities saw a meaningful relief rally last week but remain down about 20% year-to-date, while the modest March recovery in software leveraged loans has stalled (see Figure 1). Despite compositional differences – public equities generally represent larger companies with more scale, liquidity, and financial flexibility than the typically smaller, private-equity-owned issuers that dominate the software loan market – the outcome is the same: Neither market has been able to fully retrace the year-to-date sell-off in a meaningful way.

Public software equities are effectively long-duration assets (they typically pay no dividend and rely more on long-term cash flow expectations than other sectors), so the March backup in interest rates was not particularly helpful.

In credit, investors have historically leaned on the “sponsor put” – i.e., the ability of financial sponsors to support portfolio companies via add-on capital, debt buybacks, and other liability management tools – but that backstop has been less reliable this time.

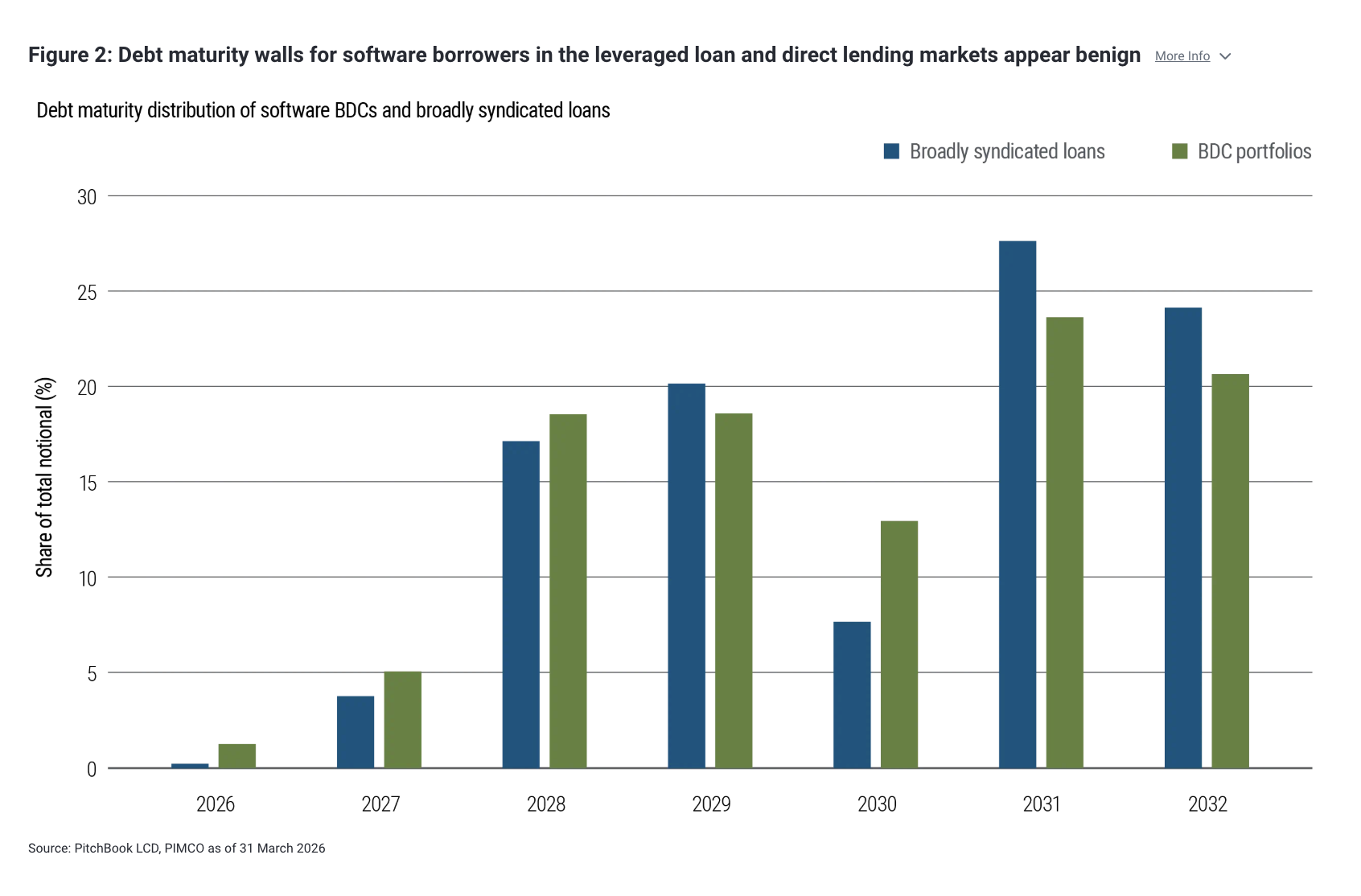

The good news is that relatively benign near-term refinancing needs for software companies limit the risk of an abrupt rise in financial distress (see Figure 2). That said, this is hardly a clean bill of health, and the fundamental challenges around terminal values are unlikely to dissipate anytime soon. An inflection in the broader business cycle would almost certainly turn latent, sector‑specific vulnerabilities into higher defaults over time.

Read more: Why the Fed Could Shrink Its Balance Sheet Again (and Markets Might Not Notice)

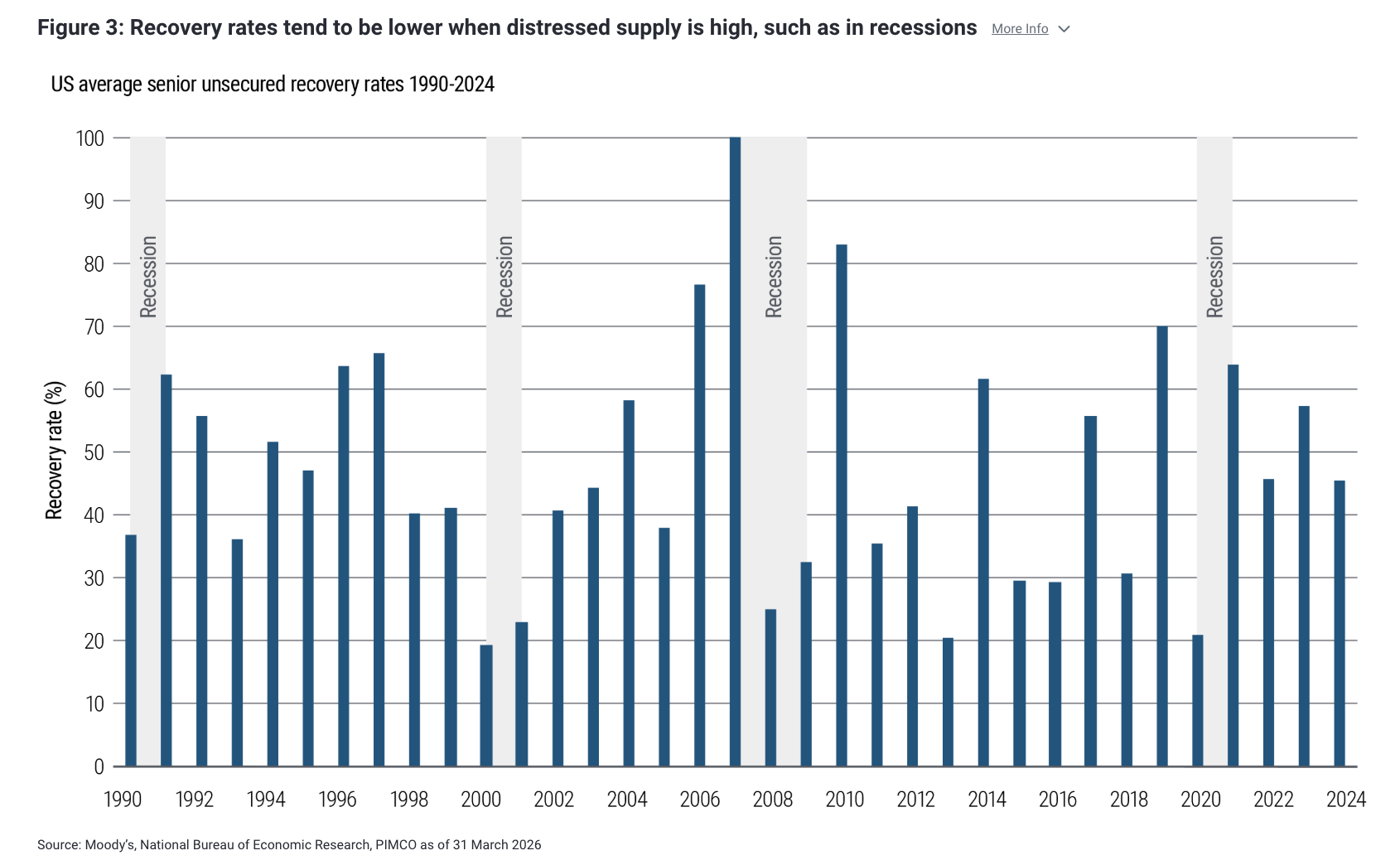

If a software‑led default cycle were to emerge, however, history offers limited direct guidance. The software sector as we know it today, characterized by loan‑heavy capital structures and significant sponsor involvement, has not experienced a meaningful episode of financial distress. As a result, empirical evidence on default intensity and recovery behavior remains scant.

That does not mean history is silent. There are precedents of industry‑specific shocks driven by technological change that resulted in asset obsolescence or excess supply. The rise of the internet and the ensuing print media defaults of the early 2000s illustrate the former, while shale production and the resulting energy sector distress exemplify the latter.

These episodes suggest a common pattern: When depressed residual asset values coincide with a concentration of distressed supply, recovery rates tend to be materially lower than average. Consistent with this, Figure 3 shows that recoveries during such periods, particularly in recessions, are notably lower than in low‑default environments.

Another look at dispersion in BDC portfolios

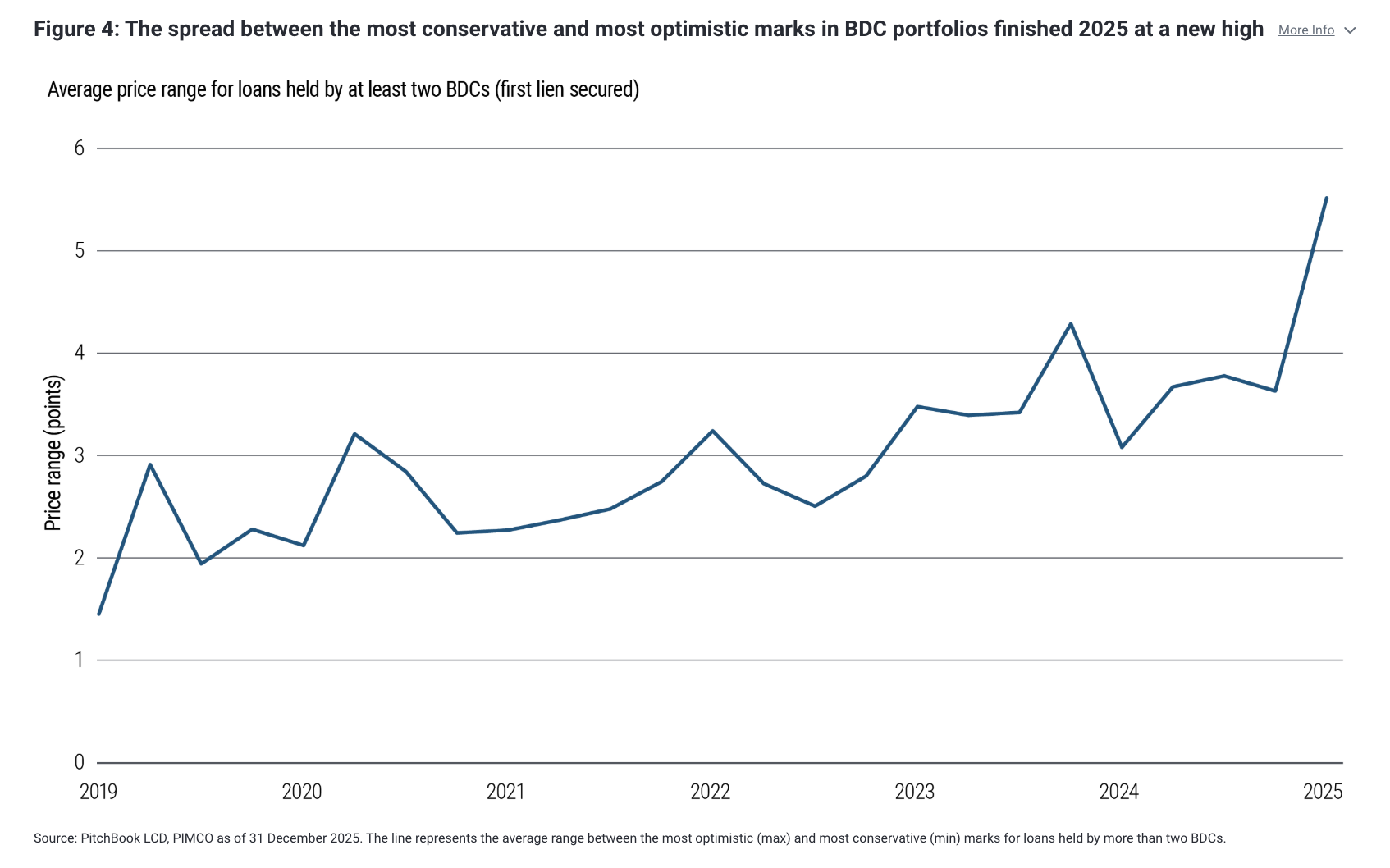

Valuation opacity in corporate direct lending portfolios remains front and center. Investors increasingly recognize that the smoother return profile over the past decade for this subset of private markets largely reflects lower observed volatility, not inherently lower risk. What is less appreciated is the extent to which opaque valuation practices and stale price marks have distorted the cross-sectional distribution of loan prices within BDC portfolios.

These practices have artificially compressed dispersion and created an appearance of stability that is not fully consistent with underlying credit diversity. This stands in sharp contrast to the broadly syndicated loan market, where continuous price discovery produces a wider, more informative range of outcomes across outstanding loans.

Two metrics underscore this gap. First, for loans held across multiple BDCs, the spread between the most conservative and most optimistic marks has widened meaningfully in recent quarters (see Figure 4). This divergence signals growing uncertainty around true valuations and has contributed to recent redemption pressures.

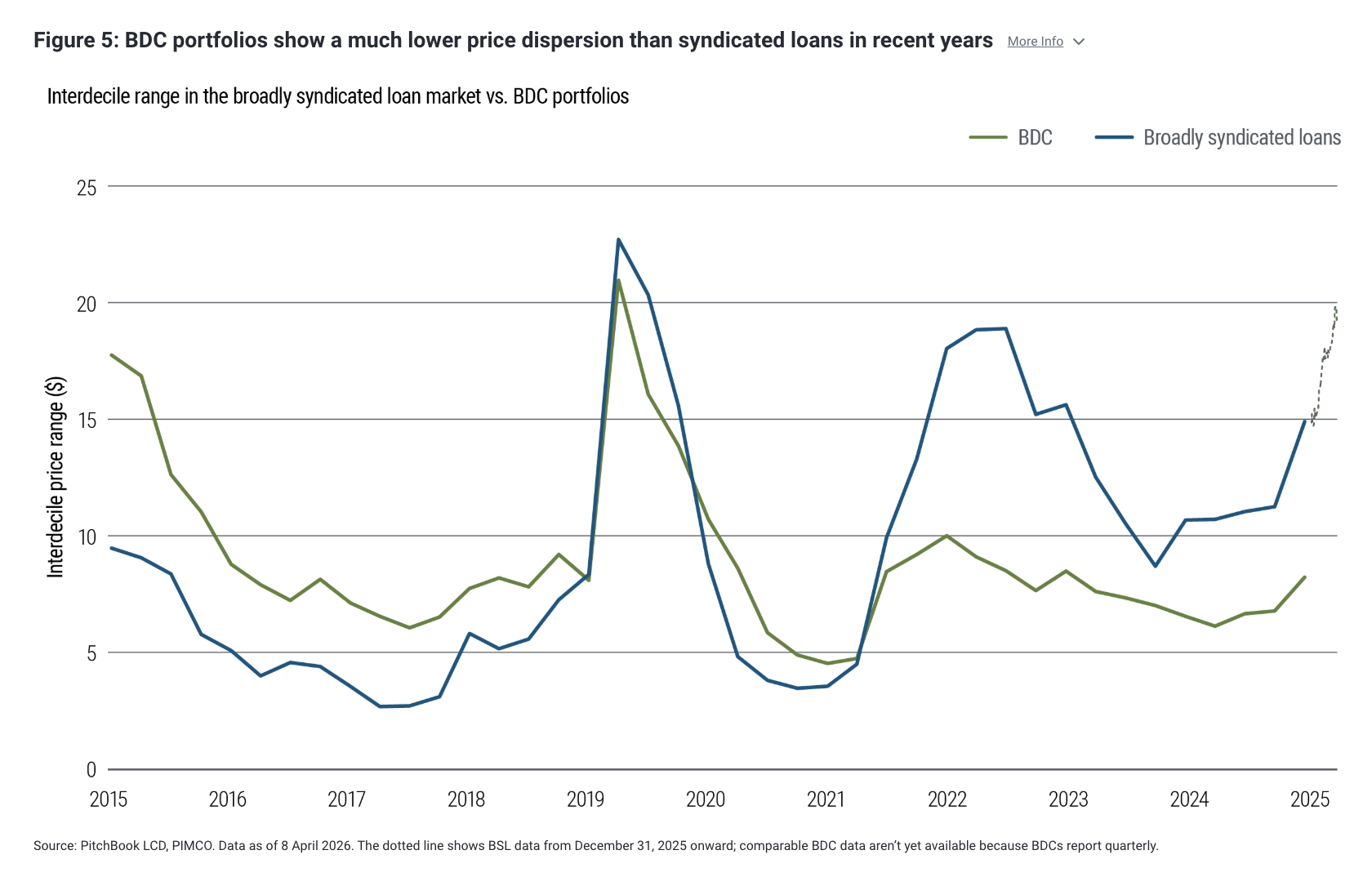

Second, since 2021 the overall price dispersion within BDC portfolios has been an order of magnitude lower than in the broadly syndicated loan market, leading to an implausibly tight range given broadly comparable credit risk (see Figure 5). In a stress scenario in which marks are forced to converge toward realizable value, dispersion would likely widen abruptly.

Taken together, the software credit landscape looks stable on the surface but more fragile underneath. This argues for selectivity, a focus on downside mitigation, and caution toward strategies that rely on smooth reported valuations rather than resilient fundamentals.

Disclosures

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. There is no guarantee that results will be achieved.

Past performance is not a guarantee or a reliable indicator of future results. References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

All Investments contain risk and may lose value. An investment in a BDC is subject to credit and investment risk, leverage risk, market and valuation risk, price volatility risk, liquidity risk, interest rate risk and structural and regulatory risk. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0417-5408039

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO