In a way, this same concept is what draws me to investing. While we are currently in a particularly grueling climb (including the war in Iran – a situation in which we will provide an update at the end of this piece), we cannot lose our long-term perspective. We want to take this piece as a summit in the middle of our hike; one where we can see a path through the trees and hills and clearly see four potential paths from here. The details of how things actually unfold will not match our scenarios exactly, but we believe having a framework helps us know what to look for as earnings and economic data come in over the months ahead.

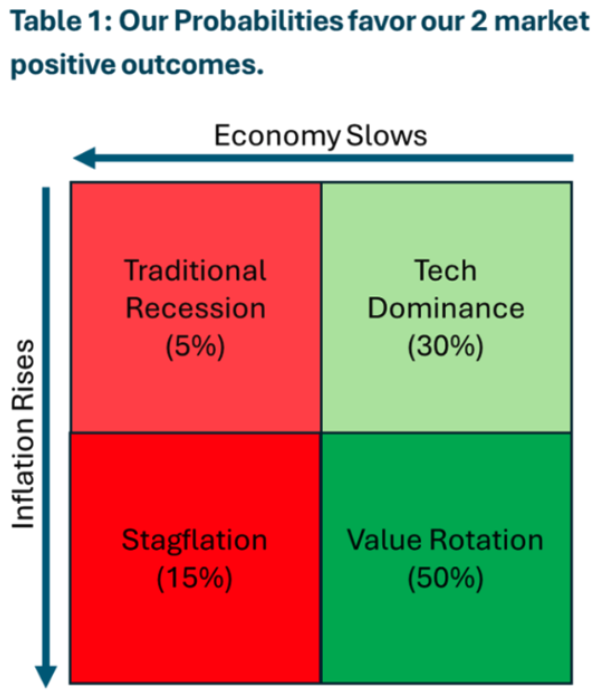

Four Paths Ahead: They Depend on Two Key Economic Variables

We see four likely outcomes for markets over the next one to three years, differentiated by the trajectory of long-term economic growth and inflation.

Path #1: Traditional Recession Scenario (Low Inflation / Low Growth) – 5%: This scenario involves a significant demand collapse and disinflation, prompting the Federal Reserve to shift quickly toward accommodation. While anything is possible, we view this outcome as unlikely given the current strength of corporate earnings and resilient employment data.

Path #2: Stagflation (High Inflation / Low Growth) – 15%: Stagflation would put the Fed in a difficult bind — unable to come to the market’s aid without allowing inflation to spiral. This scenario could materialize if tariff-driven price pressures from last year are compounded by supply chain disruptions stemming from the Iran conflict and Strait of Hormuz instability. For this probability to rise meaningfully, we would need to see the Fed cutting short rates against a backdrop of rising inflation, with long-term core inflation exceeding 3%.

Path #3: Tech Dominance (Low Inflation / High Growth) -30%: The AI-driven advances of recent years, combined with the valuation reset of the past six months, could allow technology to sustain a prolonged run – provided earnings continue to grow at elevated levels for longer than the market currently expects. While we expect positive returns from Technology, we believe a return to narrow technology leadership is less likely than a broad value rotation. Paradoxically, the market’s own fear of an AI bubble may be its best defense against one forming, at least in the near term.

Path #4: Value Rotation (Moderate Inflation / High Growth)-50%: This is our base case, and it would bear some resemblance to the post-Korean War period (1950s-60s) or the 2004–2007 cycle. In this scenario, inflation settles in the 2.5–3% range, the 10-year Treasury finds equilibrium between 4.25–4.75%, and the Fed can lower short rates against a backdrop of strong nominal growth. This combination is also favorable for indebted governments, as it allows them to gradually inflate their debt down to more manageable levels over time.

We call this a value rotation because the asset classes that tend to benefit — US value, small-caps, international, and emerging markets — share the classic characteristics of traditional value investing: lower multiples and higher sensitivity to nominal economic growth. The specific mechanisms differ – lower short rates are the primary tailwind for small-caps, dollar weakness for international equities, and operating leverage for cyclicals. But they share a common driver — nominal growth strong enough to lift all boats without triggering a Fed response that chokes the cycle.

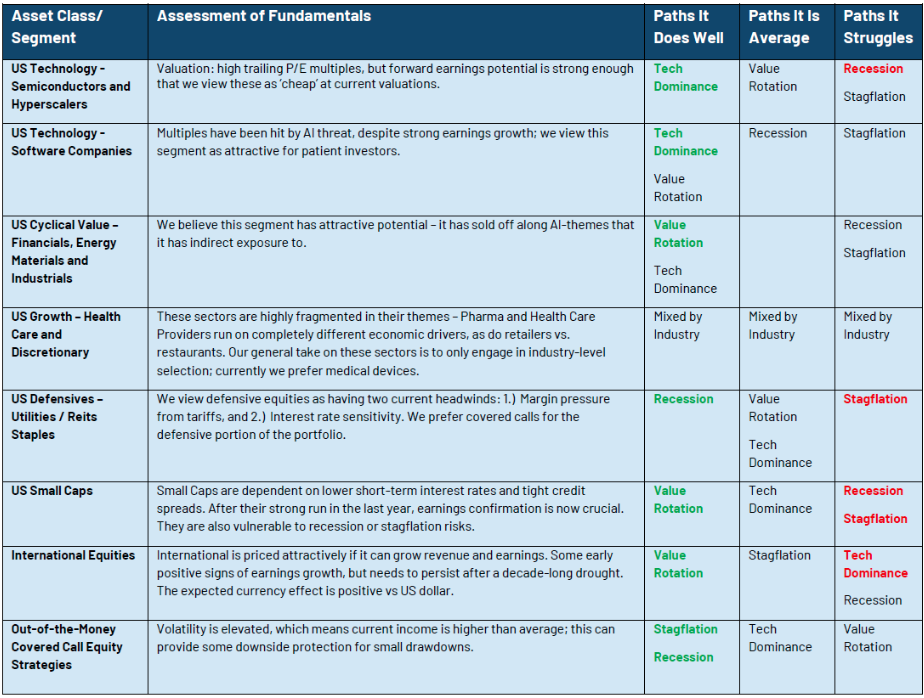

Implications of Different Environments on Select Asset Classes and Sectors

Above is a summary of how some of the major equity segments and other asset classes we are evaluating might hold up if each of the four paths are taken by the market. Red and green highlights emphasize our belief that the asset class will hold up the best (or worst) in each scenario.

Conclusion: Stay Invested and Seek Out Value

After taking this moment of respite from our proverbial market grind, we believe there are 5 major takeaways for our portfolios:

-

Our portfolios remain overweight equity relative to their benchmarks. This positioning reflects the 75% combined probability we assign to our two market-positive scenarios.

-

In the US, we prefer large-cap value over broad small-cap. Small-caps would likely be hardest hit in either of our two downside scenarios, though we see compelling selection opportunities in specific sectors and individual stocks.

-

Internationally, we are currently benchmark-neutral — though the case is becoming increasingly attractive. Cheap valuations, a macro environment that is favorable to US-denominated Investors, and our expectation of moderate dollar weakness driven by tariffs all create strong tailwinds for international assets. The primary risks remain China growth and European political fragmentation.

-

We remain invested in US Technology. Long-term investors should likely see semiconductors grow into their valuations over time, and software valuations have compressed to levels where they may hold their own even in a value rotation environment.

-

From a risk management perspective, it is important to diversify your diversifiers. Risk-protection assets are scenario-dependent. As 2022 reminded us, in a rising rate environment, Treasuries can decline alongside equities. Balancing hedges — such as covered call strategies alongside bonds — is critical, as is maintaining the flexibility to be tactical.

Overall, this analysis reinforces our pro-risk bias and our desire to add to value-oriented positions where opportunities arise. We will look to Q1 earnings season for confirmation — expecting broad resilience, improvement in value-oriented segments, and earnings stability in technology. The key risk we are watching most closely is core inflation: a re-acceleration of long-term inflation above 3.0% would cause us to shift probability from Value Rotation toward Stagflation, with meaningful implications for our asset class preferences. Absent that, our view from the summit is clear — this is not an environment for hiding in cash or defensives, but one that rewards a willingness to lean into economically sensitive assets.

Postscript: Iran War Update – We Believe the Worst for Markets is Behind Us

The recent equity market rally – propelling the S&P 500 to a new all-time high – has been fueled by the hopes the ceasefire between the US and Iran leads to a resolution. While the two sides are still miles apart, we believe that the worst is behind us, and that the likely outcome will be our ‘Muddle Through’ scenario, where the war lasts less than four months. We do not believe the Trump Administration, nor the American people have the appetite for a protracted military engagement. This conflict’s trajectory has followed the same pattern of escalation and de-escalation we have seen play out with tariffs, Greenland, and pharmaceutical negotiations — brinkmanship followed by pragmatic retreat. Consistent with that pattern, we have modestly raised our probability of favorable or non-disruptive resolution to 80% and reduced our probability of further escalation to 20% from our last Iran-focused Weekly View.

We continue to maintain a constructive market outlook so long as corporate earnings remain resilient, and we will continue update our scenario probabilities as the Iran situation develops. To that end, our shorter-horizon balanced portfolios added US and international equity exposure back to the portfolio last week after the ceasefire was announced. We are watching events with humility, but we are not abandoning our constructive market outlook — and we are already sizing up potential opportunities that resolution will eventually present.

Authored by Adam Grossman, CFA

Originally posted on RiverFront Investment Group.

Originally published on ETF Trends

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Risk Discussion: All investments in securities, including the strategies discussed above, include a risk of loss of principal (invested amount) and any profits that have not been realized. Markets fluctuate substantially over time, and have experienced increased volatility in recent years due to global and domestic economic events. Performance of any investment is not guaranteed. In a rising interest rate environment, the value of fixed-income securities generally declines. Diversification does not guarantee a profit or protect against a loss. Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability. Please see the end of this publication for more disclosures.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment

decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

The comments above are subject to change and are not intended as investment recommendations. There is no

representation that an investor will or is likely to achieve positive returns, avoid losses or experience returns as discussed for various market classes.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

In general, the bond market is volatile, and fixed income securities carry interest rate risk. (As interest rates rise, bond prices usually fall, and vice versa). This effect is usually more pronounced for longer-term securities). Fixed income securities also carry inflation risk, liquidity risk, call risk and credit and default risks for both issuers and counterparties. Lower-quality fixed income securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Foreign investments involve greater risks than U.S. investments, and can decline significantly in response to adverse issuer, political, regulatory, market, and economic risks. Any fixed-income security sold or redeemed prior to maturity may be subject to loss.

Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Dividends are not guaranteed and are subject to change or elimination.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by Riverbend Investment Management