One of the most important decisions anyone will make in their lives is whether, and whom, to marry. A well-chosen partnership can lead to a happy steady state and help to weather downturns. But even the best long term partnerships can have their ups and downs. For currencies that are wedded to the U.S. dollar, the war in Iran has put some stress into their relationships.

A fundamental support for the U.S. dollar (USD) comes from the market for oil. When demand for crude oil first ascended in the 20th century, the U.S. was the world’s leading oil producer. As U.S. wells depleted, nations in the Middle East came to dominate energy markets. In 1974, the U.S. made an agreement with Saudi Arabia to sell its oil in U.S. dollars, offering a security agreement in exchange for oil revenues being reinvested in U.S. assets. All other OPEC nations followed suit, and the petrodollar was formed.

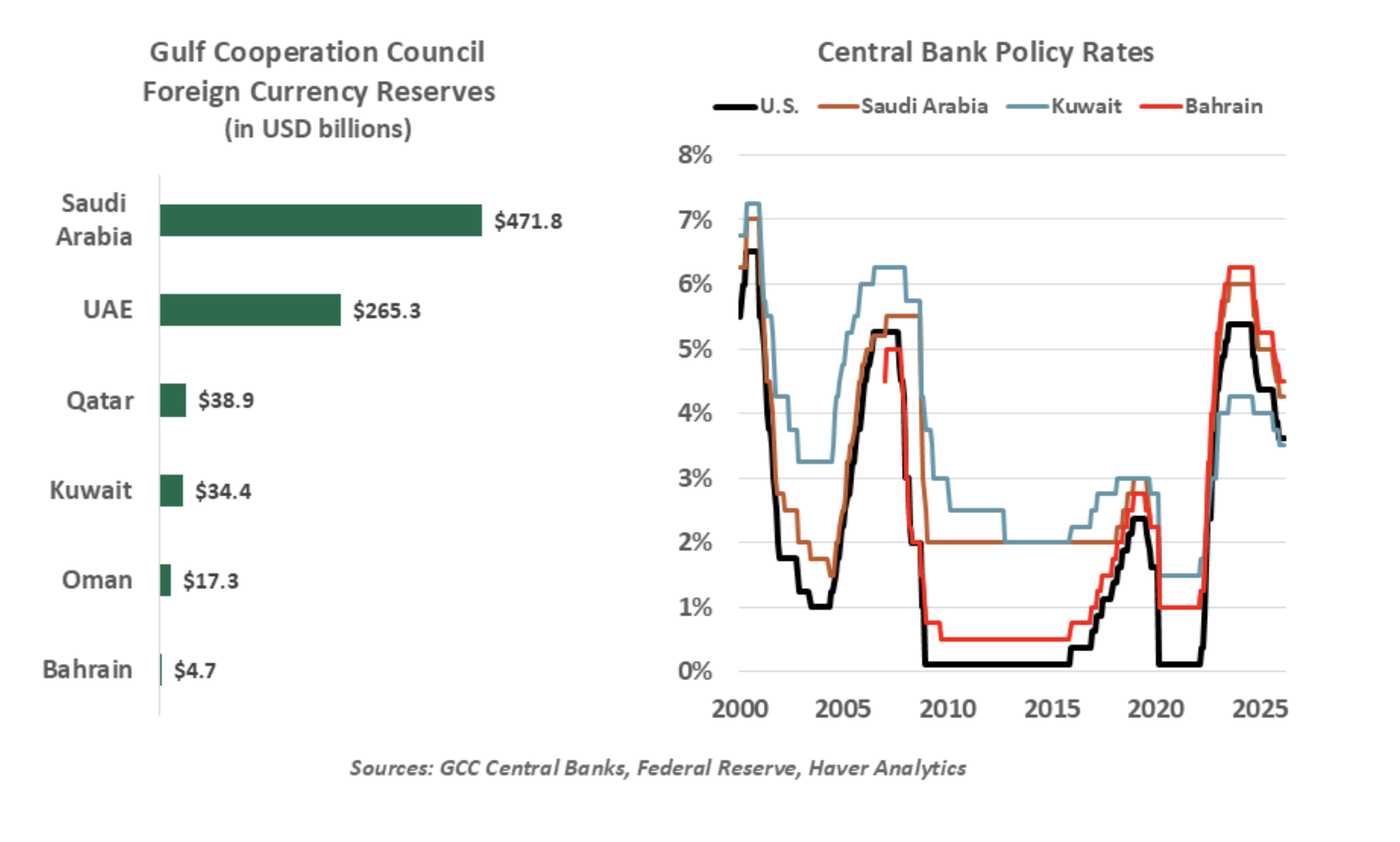

Many oil-exporting nations, including Saudi Arabia, the UAE, Qatar, Bahrain and Oman, found the arrangement sufficiently workable to fix their currency’s value to the dollar. They are not outliers: more than 20 nations keep a fixed, or hard pegged, exchange rate with the USD. Others have a soft or managed peg, targeting a value within a range of the USD. Pegged nations benefitted from a more stable and predictable currency, which secures international purchasing power. Global commerce became easier as exchange rate risk was eliminated for these nations.

The petrodollar helped to cement dollar’s status as the world’s reserve currency, even as greater domestic production made the U.S. less dependent on oil imports. Now, that arrangement has created a vulnerability. U.S. actions against Iran have had rapid spillover across Middle Eastern nations. Many are unable to export oil (or any other goods) at their usual volume. Near-term recessions are likely for many. Policymakers may wish to have wider discretion to manage their economies, but the tie to the dollar has limited their monetary toolkits.

Read more: The Outlook From, and For, the IMF

A currency peg leaves a nation effectively adopting the host country’s monetary policy. Nations in the Middle East that are tied to the U.S. are in this position. Supporting their economies in the wake of the war might call for lower interest rates, but the current inflationary challenge has put off prospects of easing by the Federal Reserve. The dollar had a strong run recently and has held its value amid the crisis, also elevating the value of its pegged currencies.

The petrodollar need not persist forever; the security arrangement was not a formal treaty. Reliance on the U.S. security umbrella has been called into question worldwide. Sanctioned oil producers would welcome an alternative to U.S.-controlled payment systems.

The current hostilities are adding to the case for diversification. China has emerged as a willing broker for oil transactions. India has taken receipt of Iranian oil, paid in Chinese renminbi. The UAE has called out its dwindling dollar reserves as a warning that it may need to move more transactions away from dollars.

We view these sentiments as aberrations, not a change to the world order. The U.S. is an important oil producer and a willing importer of all products. The push to restore oil production in Venezuela will modestly add to the market for petrodollars. Any challenges to the dollar’s position may be met with a strong response, especially as new tariff policies loom.

Partners in a marriage have an incentive to try to work through issues, and we are confident that will be the case with pegged currencies. In this case, separation is not an option.

Ryan James Boyle is the Chief U.S. Economist within the Global Risk Management division of Northern Trust.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Northern Trust

Read more commentaries by Northern Trust