Differing Signals in BDCs, and Orderly Defaults in High Yield

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways:

- Sentiment around business development companies (BDCs) has rebounded recently, although stock prices continue to reflect questions about reported net asset values (NAVs), while credit investors have required extra compensation.

- Large gaps in how similar loans are marked across BDCs are a reminder that private credit valuations can lag and shouldn’t be taken at face value.

- In the high yield bond market, defaults are happening but in a managed way, with most issuers opting for negotiated restructurings rather than disorderly bankruptcies.

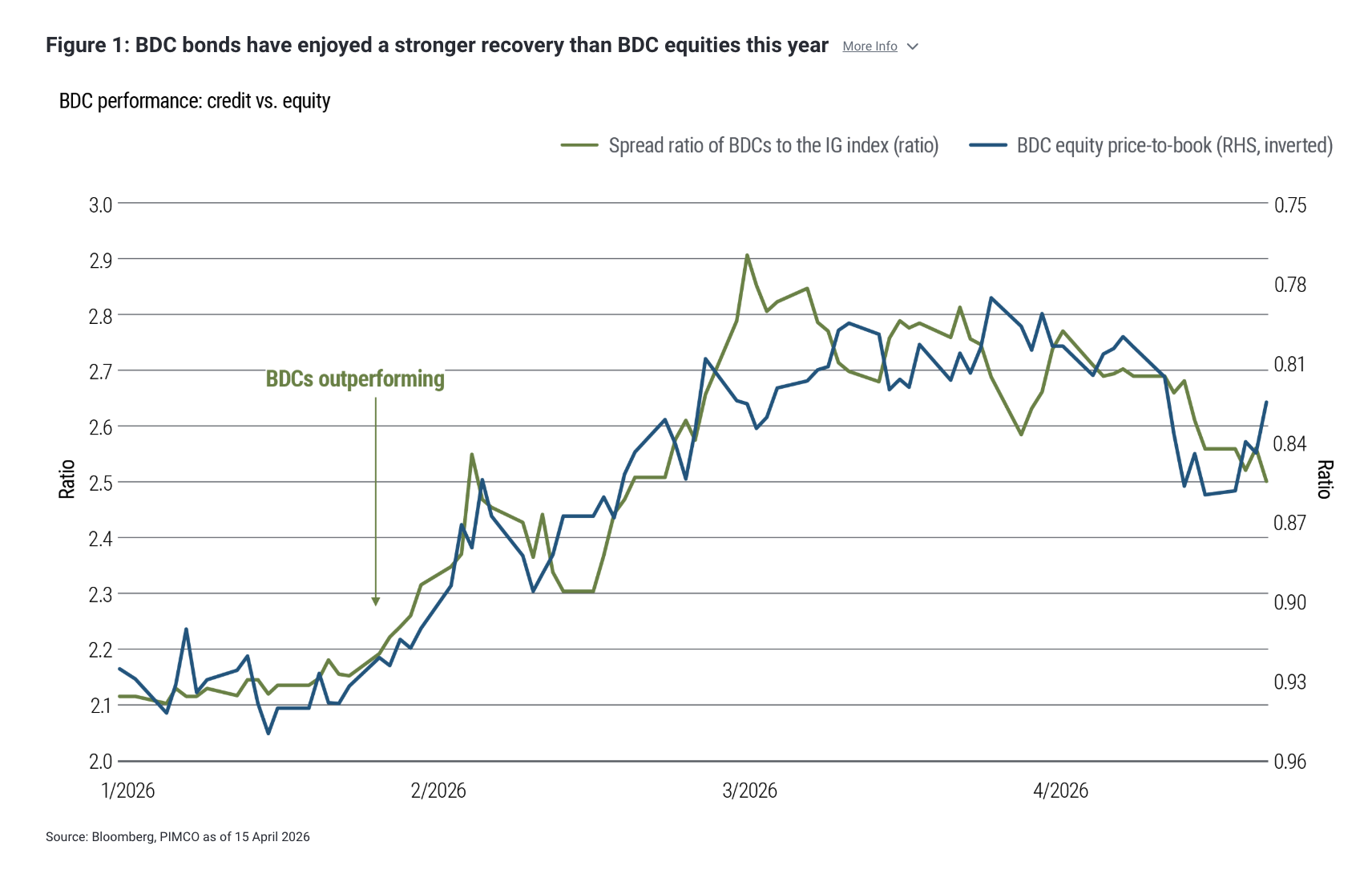

Sentiment toward BDCs – funds that invest in small and midsize private U.S. businesses – has improved since early March. BDC bond spreads have stabilized and outperformed the broader investment grade (IG) index, suggesting credit investors are increasingly comfortable with downside risk. Publicly listed BDC equities have also rebounded (see Figure 1). Despite the strong co-movement in recent weeks, however, the equity and credit narratives differ.

On the equity side, the debate centers on NAV credibility. Investors remain skeptical of where portfolios are marked, and without better price discovery that skepticism is likely to persist.

Read more: When Geopolitics Becomes an Economic Input

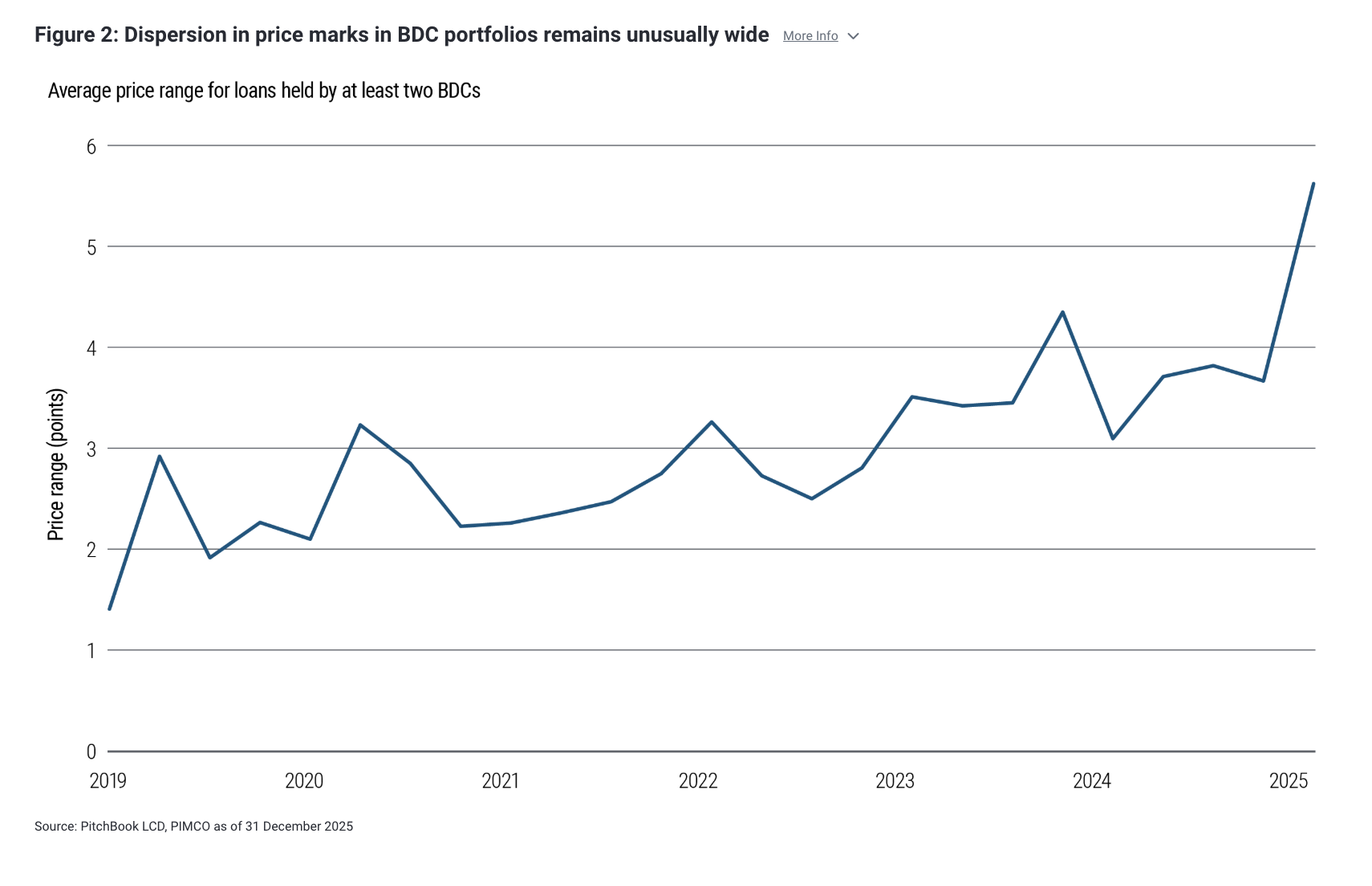

Elevated dispersion in marks is part of the problem: For loans held across multiple BDCs, the gap between the most optimistic and most conservative managers exceeds five percentage points (see Figure 2). Rather than providing comfort, that spread signals uncertainty around true asset values and makes it harder for reported NAVs to serve as an anchor – hampering confidence in dividend sustainability and underlying earnings power.

A parallel in real estate

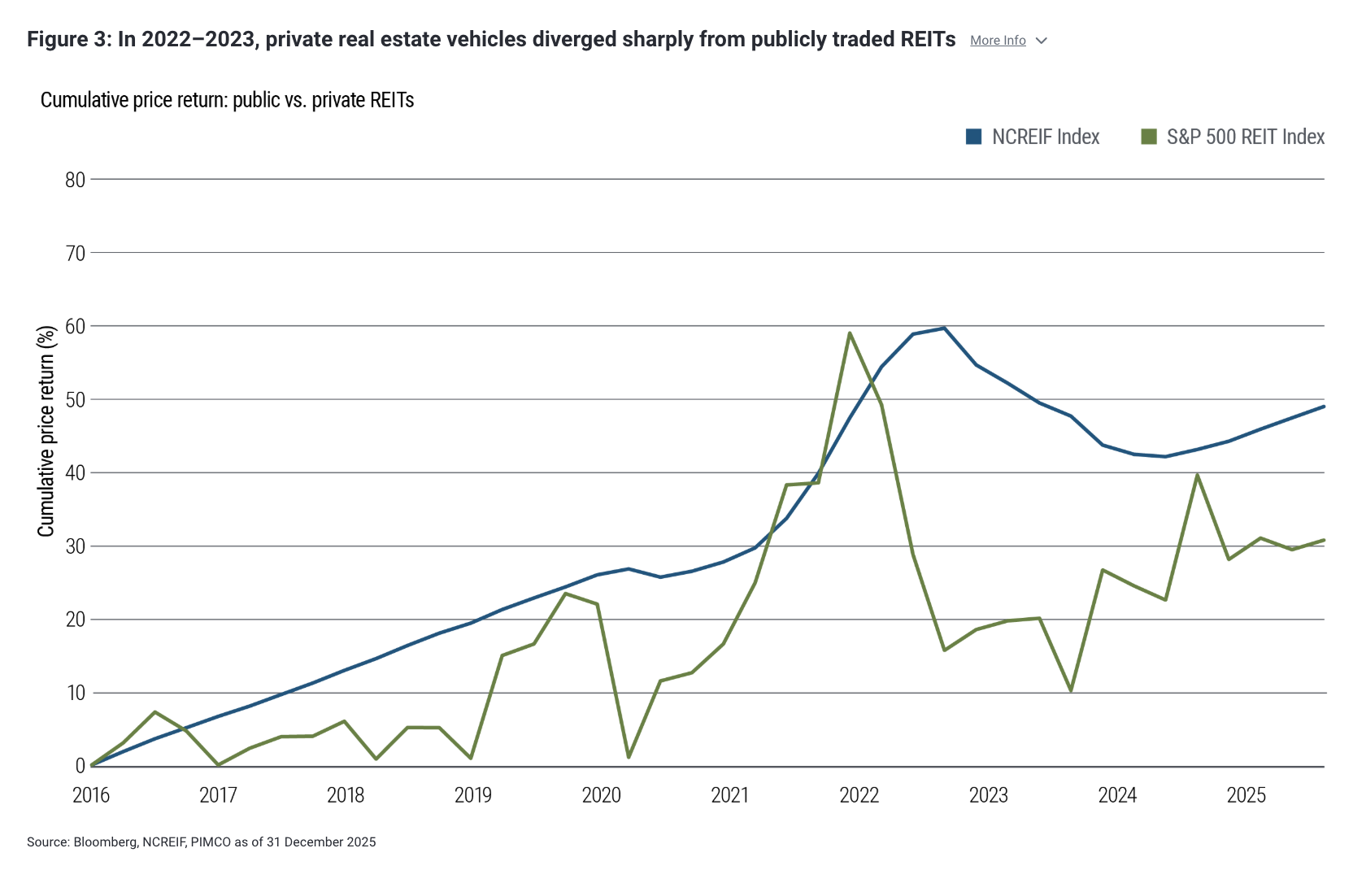

History offers a useful parallel. In U.S. real estate markets, after the rapid rise in interest rates in 2022–2023, private vehicles diverged sharply from publicly traded real estate investment trusts (REITs), with public markets repricing faster and more aggressively before the two ultimately converged about halfway back toward the baseline.

The lesson is not that equities are immediately “right,” but that when marks are opaque and stale, public markets tend to apply a large – and often persistent – discount until clarity emerges. Figure 3 illustrates this dynamic by comparing cumulative price returns for the S&P 500 REIT Index with the National Council of Real Estate Investment Fiduciaries (NCREIF) Property Index, a proxy for unlevered private real estate returns. Public REITs sharply underperformed their private counterparts from the first quarter of 2022 through the third quarter of 2023, but by mid-2024 the two indices had reconverged.

In credit, the story is different. Credit markets can be more anticipatory in some ways, demanding compensation against the risk of asset quality deterioration. To a large extent, this repricing has already occurred, with many BDC bonds trading at spread levels not too far from the index of BB bonds, the top rating tier in the high yield (HY) sector.

From here, further material spread widening would likely require a more acute shock that would most plausibly come from a reassessment of balance sheet liquidity risk, particularly among non-traded BDCs. For now, that risk appears contained and supported by structural guardrails, including fund redemption limits, access to bank credit facilities, the presence of liquid assets in portfolios, and principal payments from maturing loans.

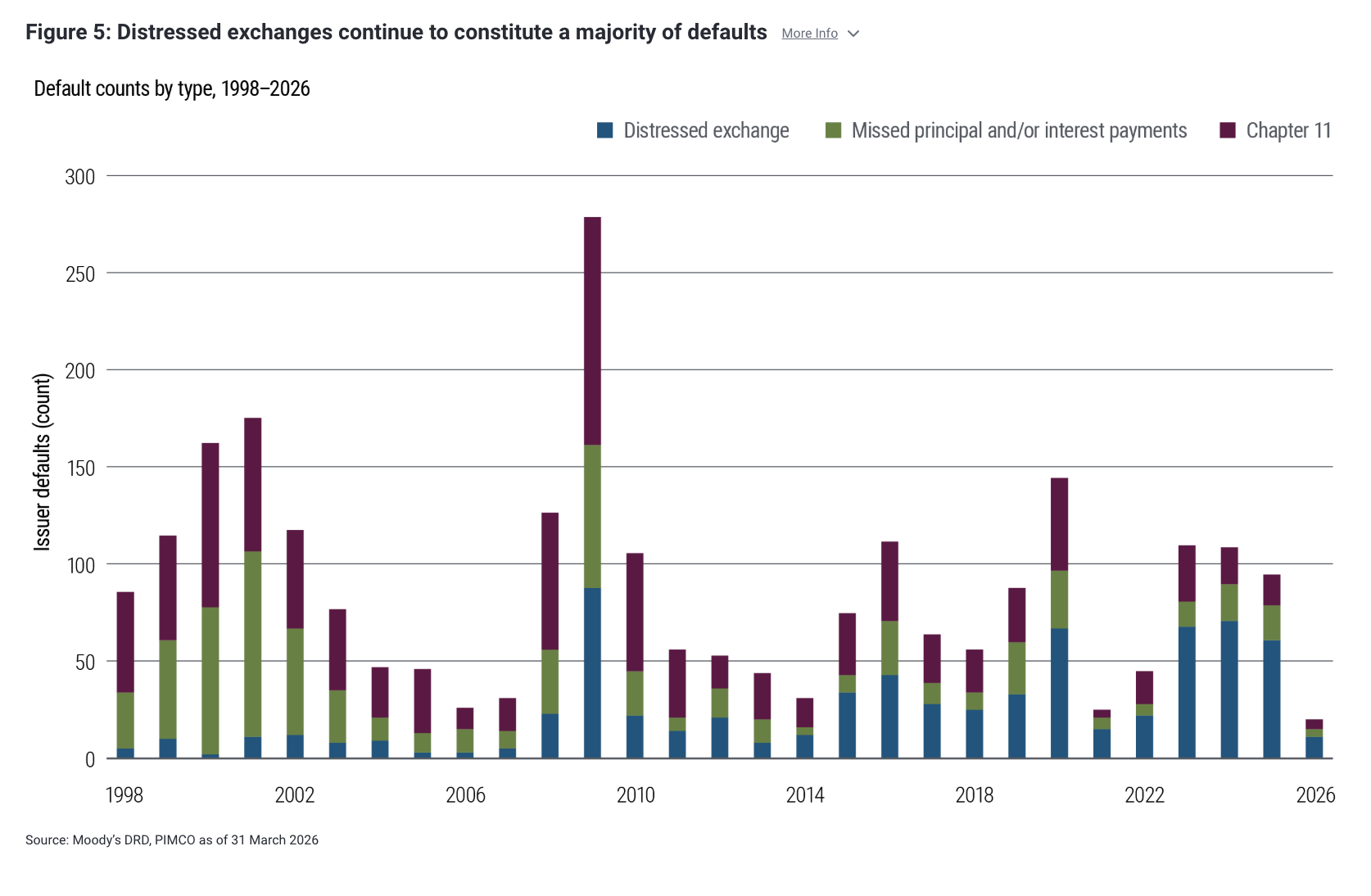

Distressed exchanges remain the norm for U.S. dollar high yield defaults

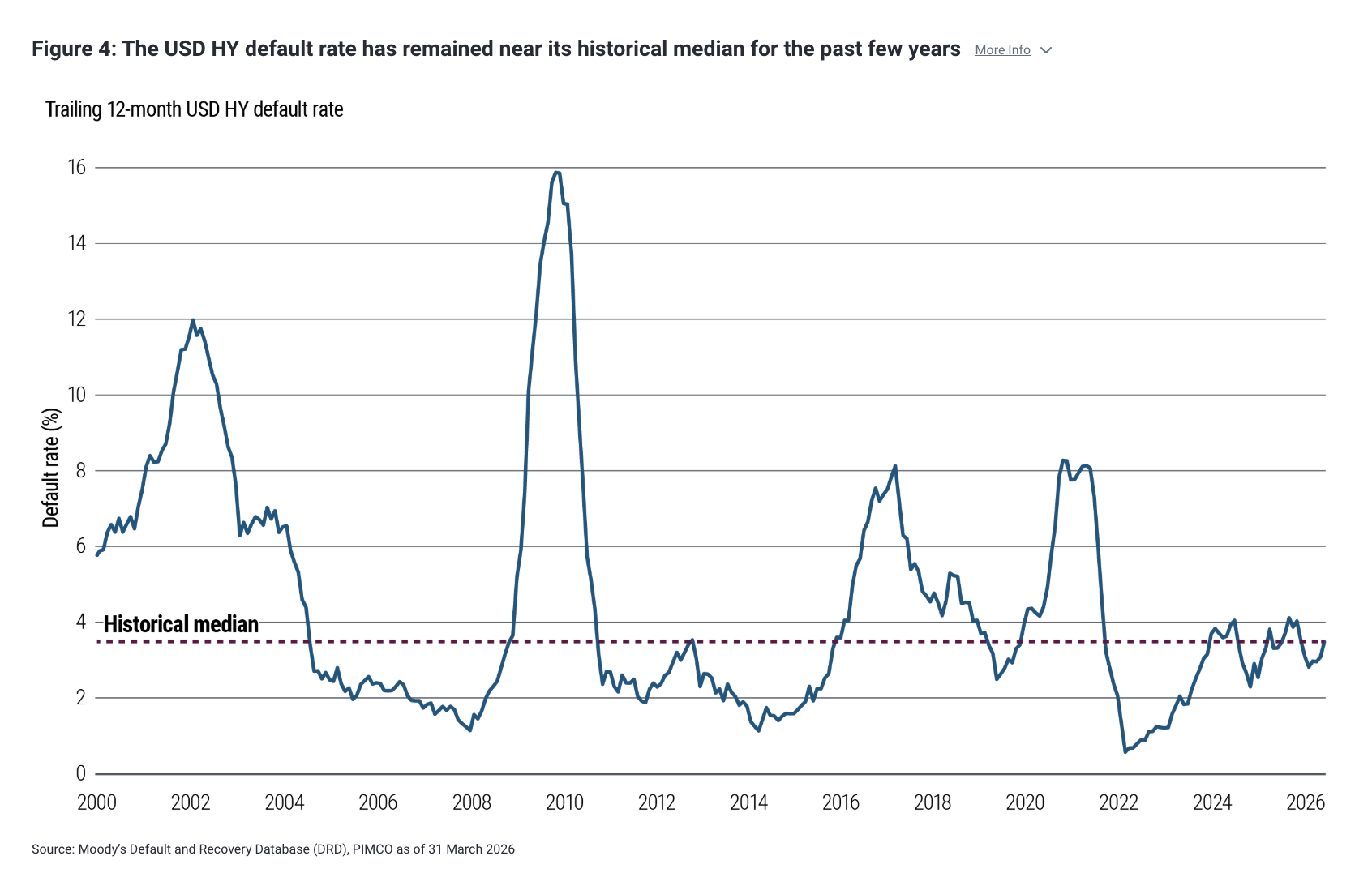

It has been almost 17 years since investors last experienced a true default cycle – an abrupt rise in financial distress that drives 12-month trailing default rates into the double digits. Since the global financial crisis, default rates have instead followed a stop-start pattern, with two notable but shorter-lived humps: the 2014–2015 episode that followed the onset of the shale revolution (and was largely concentrated in oil and gas), and the COVID shock, which was unusual both in its duration and in the magnitude of the policy response that followed. As Figure 4 shows, since defaults bottomed at the end of 2021, the 12-month trailing issuer-weighted default rate in the U.S. dollar (USD) HY market has been range-bound around its long-run median of 4%.

Against that backdrop, there were 20 issuer-level USD HY defaults over the first three months of 2026, according to Moody’s data, broadly in line with first quarter default counts in each of the prior three years. Importantly, distressed exchanges continue to account for the majority of default events (11 of the 20 so far this year) – a pattern that has persisted for roughly a decade (see Figure 5). A distressed exchange is an out-of-court restructuring in which an issuer offers creditors new securities or amended terms that are less favorable than originally promised (for example, a maturity extension, coupon reduction, or principal haircut) to avoid a payment default and a Chapter 11 filing.

The preference for distressed exchanges reflects their typically lower frictions relative to Chapter 11. They can be executed more quickly, with less operational disruption and less headline risk, which can help preserve employee retention and enterprise value.

For investors, these dynamics often translate into higher recoveries than in-court restructurings, although outcomes ultimately depend on the issuer’s capital structure, collateral, and the depth of the underlying business deterioration.

Michael Puempel and Gabriel Cazaubieilh contributed to this report.

Disclosures

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. It is not possible to invest directly in an unmanaged index.

Past performance is not a guarantee or a reliable indicator of future results. References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

All Investments contain risk and may lose value. An investment in a BDC is subject to credit and investment risk, leverage risk, market and valuation risk, price volatility risk, liquidity risk, interest rate risk and structural and regulatory risk. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss. The value of real estate and portfolios that invest in real estate may fluctuate due to: losses from casualty or condemnation, changes in local and general economic conditions, supply and demand, interest rates, property tax rates, regulatory limitations on rents, zoning laws, and operating expenses. REITs are subject to risk, such as poor performance by the manager, adverse changes to tax laws or failure to qualify for tax-free pass-through of income. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0424-5429946

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All