On Friday, the Department of Justice announced it was dropping its investigation of the current Federal Reserve Chair Jerome Powell. Senator Thom Tillis was effectively blocking the nomination process from moving forward while the Department of Justice investigation of Powell was ongoing. With Friday’s announcement, the path forward for confirming Kevin Warsh as the next Chair of the Federal Reserve can proceed. Last week, Kevin Warsh appeared before the Senate Banking Committee, making a statement and taking questions from Senators. While much of the questioning was more politically driven than substantive with regards to how Warsh views the economy and how he may handle the position of Fed Chair, there were a few takeaways that provided some insight into his views and how he may like to steer the Fed going forward.

On measuring inflation

When discussing inflation and how he prefers to measure inflation, Warsh said that he prefers to look at “things that are called trimmed averages” because they “take out the tail-risks, all of the one-off items.” Currently, the preferred measure of inflation for the Fed is Core PCE, which essentially strips out the food and energy components from PCE. The theory is that food and energy are historically volatile (big swings both up and down). Removing those components reduces the short-term “noise” and provides a cleaner picture of longer-term inflation trends. A trimmed average differs from this calculation in that instead of eliminating the same two components (food and energy), it trims both the high and low outlier components for each reading. The components that are trimmed could vary from month-to-month. The idea is that any large swings from month to month are likely one-off items that are not indicative of a longer-term trend.

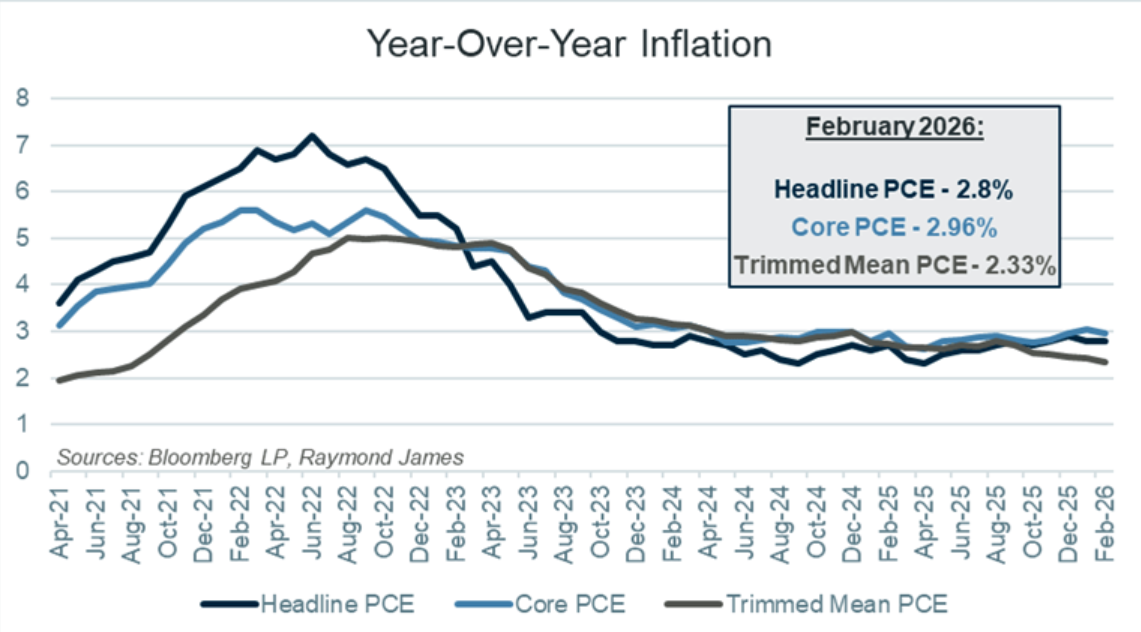

In the role of Fed Chair, Kevin Warsh would not have absolute authority to make changes at the Fed as he is only one voting member, albeit an important voting member. What might a shift towards a trimmed average measure of inflation look like? Conveniently, the Dallas Fed runs a trimmed mean PCE calculation that can provide some insight. The chart shows Headline, Core, and Trimmed Mean PCE over the past five years to provide some context on how they move and relate to each other.

One interesting takeaway from this chart is that trimmed mean PCE is considerably closer to the FOMC’s 2% inflation target than both Headline and Core measures. It is also trending lower, meaning that it is both closer to the target and still trending in the right direction. While Warsh did not provide much insight into what his potential policy decisions might be, his preference for a trimmed average measure means that he might view the FOMC as much closer to its inflation target than a Core PCE analysis might provide. Generally, lower inflation provides more flexibility for the FOMC to lower rates so if (and it is a big IF at this point) the benchmark shifted from Core PCE to some sort of trimmed measure, that could mean a more dovish FOMC in the current environment.

On the balance sheet

Warsh emphasized his preference for using the interest rate decisions as the primary tool for the FOMC to affect markets while relying less on the Fed’s balance sheet. His reasoning was that interest rate decisions have the ability to “get in the cracks” of the economy, effecting the entire economy; whereas the balance sheet’s impact on the economy was less democratic and provides outsized benefits to those at the higher end of the economic spectrum. While he did not provide details, in theory this means considerably shrinking the size of the balance sheet and using open market purchases much less as a tool going forward. Given the sheer size of the Fed’s balance sheet (~$6.7 trillion), any changes with regards to how the balance sheet is used and the effects that those might have on the economy are likely not going to be felt near-term, although how that discussion plays out over the next year could provide some longer-term changes.

On guidance and communication

Warsh has made his opinion clear that less forward guidance and less communication from the Fed would be beneficial. In recent years, the Fed has prioritized communication and transparency concerning their forecasts and views. Notably, the Fed releases their Summary of Economic Projections four times a year. This provides an extensive report on the Fed’s outlook on a range of data points, from inflation to GDP to the Fed Funds rate. Warsh’s argument against this type of communication and transparency is that once views are provided to the public, Fed members are more likely to stick to their prior convictions, even in the face of evolving data. In essence, he thinks that less “public conversation” would make the FOMC more nimble and quicker to react to changing economic conditions. While market participants would likely not greet this change with enthusiasm (more data is always better in the eyes of those trying to predict the future), there are some merits to Warsh’s argument when viewed through the eyes of the FOMC and their objectives.

The next few weeks and months will likely provide much more clarity on specific changes that Warsh might want to implement if/when he becomes Chair of the Fed, but we did get a window into how he approaches a few high-level points. Stay tuned…

A message from Advisor Perspectives and VettaFi: Discover something new! Click hereto register for our upcoming webcasts.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.