Global risks have tilted against both growth and price stability. The ceasefire in the Middle East has brought a measure of calm to financial markets, but it has not resolved the underlying economic shock. With the Strait of Hormuz effectively shut, supply constraints continue to ripple through energy markets and are increasingly spilling over into downstream sectors.

The result is an uncomfortable mix: weakening growth momentum combined with stubborn price pressures, exposing some of the major markets to stagflation risk. The fiscal and monetary policy tradeoffs are becoming more challenging as the disruptions drag on. Elevated energy costs are inflating subsidy bills, widening deficits, and complicating debt dynamics. Central banks face a familiar dilemma: easing policy to cushion growth risks exaggerating inflation, while tightening policy could deepen the slowdown.

Even if the Strait were to reopen tomorrow, normalization would not be immediate; disruptions would linger for months. The longer the closure endures, the larger and more persistent the economic pain.

Following are our outlooks for the world’s major markets.

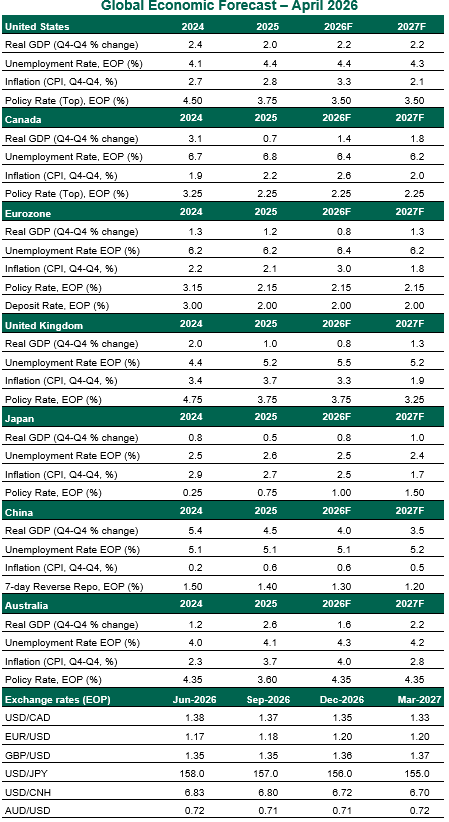

United States

- The primary U.S. economic risk from the war remains inflation. Supply‑chain disruptions could push up prices for food and manufactured goods, adding to the impact on energy. Persistently higher costs would weigh on real purchasing power and could gradually restrain overall spending. That said, we do not anticipate a material slowdown in activity. The U.S. economy has shown notable resilience this decade; supportive financial conditions continue to underpin demand, and AI‑related investment remains a powerful tailwind. A quicker reopening of the Strait of Hormuz would materially reduce the risk of more adverse outcomes.

- The most recent inflation cycle reinforced a clear lesson: once inflation rises, it can take time to bring it back down. The Fed now faces the added challenge of distinguishing temporary disruptions from more durable shifts in price dynamics. With inflation pressures emerging and the labor market still tight, there is little justification for near‑term rate cuts. We continue to see one cut later in the year, but the risk of an extended policy hold is increasing.

Read more: Currency Pegs Raise Dollar Tensions

Japan

- Recent surveys raise cautionary signals for the Japanese economy. Government measures to cap gasoline prices should help limit downside risks to consumption, but Japan remains vulnerable to energy supply disruptions stemming from the Middle East conflict. Elevated energy prices will drain global growth, dampening external demand for Japanese goods. And despite another round of robust outcomes from this year’s Shunto wage negotiations, higher inflation will leave real incomes under pressure again this year.

- The Bank of Japan kept its policy rate unchanged at this month’s meeting. While we continue to see scope for a rate hike later in the summer, policymakers are likely to proceed cautiously. The combination of rising cost pressures, weakening sentiment, and softening external demand raises the risk of stagflation, reinforcing the case for a gradual and measured normalization path.

China

- The Chinese economy continues to demonstrate a high degree of resilience, with real GDP growth surprising to the upside at 5% year over year in the first quarter, up from 4.5%. That headline strength, however, masks a fragile domestic economy. Momentum was driven by exports and industrial activity rather than household demand. Large petroleum reserves should help cushion the economy from immediate war‑related energy shocks. Even so, second‑round effects from sustained disruptions to global supply chains and softer external demand are likely to exert increasing downward pressure on growth in the near term.

- Imported inflation will ease a largely deflationary domestic environment, but weak underlying demand will limit a durable reflationary impulse. Instead, higher costs for imported energy and raw materials, combined with limited pricing power, will lead to narrower profit margins for corporations. Policymakers are expected to remain focused on steering the economy toward “high‑quality” innovation and high-tech led growth, rather than pursuing aggressive demand‑led stimulus.

Australia

- Australia’s economy posted its fastest annual growth in nearly three years in the fourth quarter of 2025, but that momentum is unlikely to be sustained. The conflict in the Middle East is adding to price pressures at a time when capacity constraints have yet to fully ease. Higher inflation, and the associated tightening in monetary conditions, will continue to erode real household incomes. Businesses will also feel the strain, caught between rising input costs and softer demand. That said, spending in areas like data centers should provide some offsetting support.

- With diplomatic efforts to end the war and reopen the Strait of Hormuz at an impasse, upward pressure on costs alongside supply concerns are likely to persist. Against this backdrop, we expect the Reserve Bank of Australia to deliver at least one additional rate hike before shifting to a prolonged pause.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Northern Trust

Read more commentaries by Northern Trust