2025 was a strong year for U.S. equity markets, driven partially by large-cap technology stocks exposed to the artificial intelligence (AI) theme. But the market has become more discerning in 2026. As investors reassess where AI creates value versus where it may erode it, we have seen sectors such as software, brokerage platforms, professional services and insurance companies sell off on fears of AI disruption. This has some investors looking to allocate toward businesses viewed as more durable.

As market leadership rotates and recalibrates, a theme we discuss in our Q2 Equity Market Outlook, allocators have sought refuge in parts of the market that may be less susceptible to AI disruption risk. Sectors such as energy, utilities, industrials and materials outperformed the broader U.S. equity market (and the technology sector) in the first quarter of the year.1

This market rotation has led to the coining of a new phrase: HALO, which stands for Heavy Assets Low Obsolescence. HALO refers to companies with capital-intensive physical infrastructure that is difficult or impossible to digitize, such as a barrel of oil or a power plant. While AI can impact these businesses, it is more likely to be leveraged for efficiency gains instead of replacing their core competencies.

Times have changed

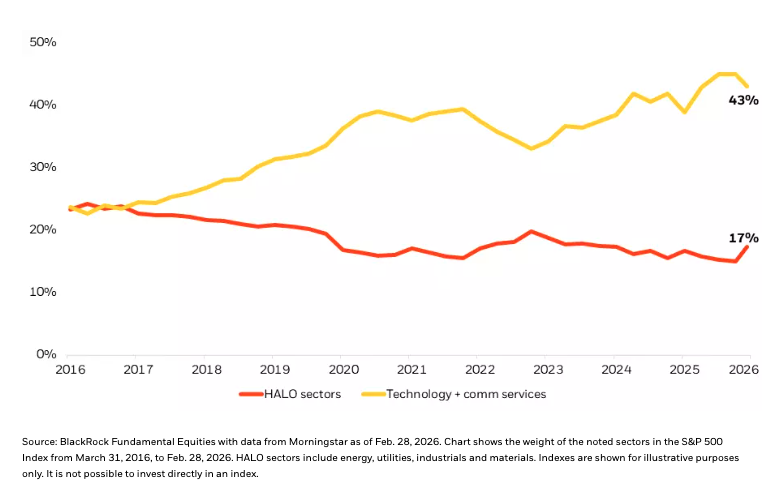

Investors looking to bolster their portfolios with resilience against AI-led disruption need to be more nimble and intentional in their allocations today. The reason: With technology and growth equities leading the U.S. market for the past several years, their weights in core indexes like the S&P 500 have increased, leaving less exposure to companies in sectors like energy, utilities, industrials and materials. HALO sectors represented just 17% of the S&P 500 Index at the end of February, compared to the combination of technology and communication services near a 10-year high at 43%, as shown in the chart below.

Ample imbalance

Weight of selected sectors in the S&P 500 Index, 2016-2026

Equity investing outside of AI

We still see AI as a transformational mega force creating investment opportunities for years to come. Yet its large influence on broad market indexes may have investors seeking equity options that effectively spread their risk. We identify two ways to diversify away from AI while still maintaining equity exposure.

1. U.S. value equities

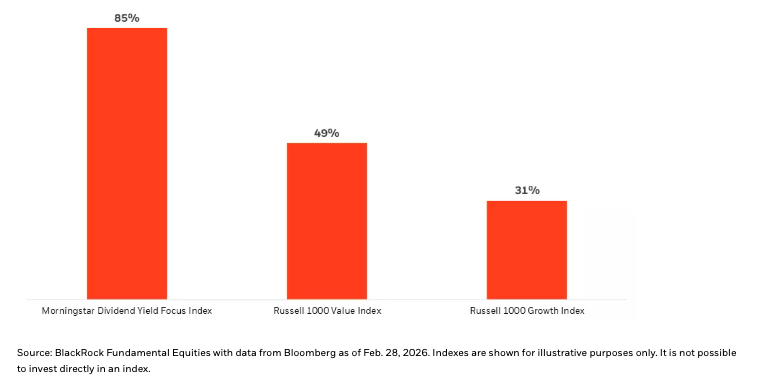

Our analysis finds that commonly used value indexes such as the Morningstar Dividend Yield Focus Index and Russell 1000 Value Index tend to have significantly more weight in HALO sectors than their growth peers such as the Russell 1000 Growth Index. These sectors are home to companies that leverage meaningful physical assets to generate revenue. One example: a mining company that operates intensive machinery to discover metals. One way of understanding this distinction is by looking at property, plants & equipment (PP&E), a common balance sheet metric, as a percentage of revenue. See chart below.

Where HALO sectors carry weight

PP&E as a percentage of revenue, 2026

We are already seeing live examples of companies in these areas leveraging AI to create new revenue-generating ideas and enhance the efficiency of their physical assets.

Case study: PPG, a major paint manufacturer, built a database that captured all of its products, including their chemical properties. With the help of AI, the company used that data to create a fast-drying, clear coat of paint that could be applied by autobody shops after repainting a car. The AI model suggested a combination of chemicals not previously used, and a new product was born for retail sale. The company has dozens more AI-assisted products in its pipeline.2

2. Infrastructure equities

Infrastructure equities offer the dual benefit of being difficult to disrupt by AI as well as benefiting from its continued adoption. As AI growth expands, the energy needs to power data centers will be tremendous, a topic discussed by Tony Kim, Head of the Fundamental Equities Technology team, in Energy and the AI buildout. Infrastructure strategies typically have material exposure to potential beneficiaries such as energy companies and utilities.

Case study: Duke Energy, a major Florida-based utility company, leverages AI to detect outages, isolate the problem and reroute power. The company says this technology helped avoid more than 280,000 outages and saved customers more than 300,000 outage hours.3

Given the market volatility related to AI disruption, we see compelling reasons to apply an active lens to investment decision-making and to consider both value and infrastructure equities as options for diversifying risk exposures.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

1Based on S&P 500 data, sourced from Morningstar, as of March 30, 2026.

2WSJ, John Keilman, Jan. 24, 2026. “Faster-Drying Paint and Better-Smelling Soap: AI Tries Product Development.”

3Duke Energy, Feb. 6, 2026. Duke Energy Florida’s smart, self-healing technology investments help keep customers’ lights on, Duke Energy News Center.

BlackRock does and may seek to do business with companies covered in this content. As a result, readers should be aware that the firm may have a conflict of interest that could affect the objectivity of this content.

Investing involves risk, including possible loss of principal. Stock values fluctuate in price so the value of your investment can go down depending on market conditions. Investment in a specific sector can entail greater volatility given the narrower focus of the investment universe and concentration in sector-specific risks.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of April 2026 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

Prepared by BlackRock Investments, LLC, member FINRA.

©2026 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

© BlackRock

Read more commentaries by BlackRock