S&P 500 Posts Best Month Since November 2020

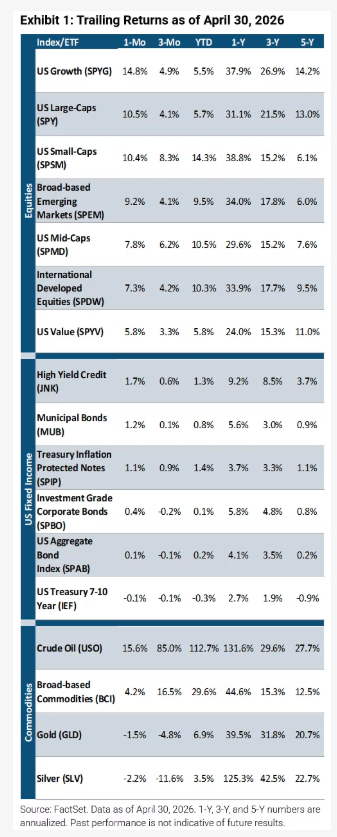

Despite lingering geopolitical tensions, higher oil prices, and renewed inflation concerns, equities moved higher in April, supported by a strong start to the Q1 earnings season and resilient economic growth. After approaching correction territory late last month, the S&P 500 rebounded to post seven record closing highs, gaining more than 10% for its strongest monthly performance since November 2020. The tech-heavy Nasdaq-100 also surged over 15%, marking its best month since April 2020. The rebound was broad-based, with US small-caps (+10.4%), emerging market equities (+9.2%), and US mid-caps (+7.8%) all posting strong gains. Aside from 7-10 year US Treasuries (-0.1%), bonds also fared well as high yield credits increased 1.7%, municipal bonds rose 1.2%, and Treasury Inflation Protected Notes gained 1.1%. Commodities produced mixed returns as both crude oil and broad based commodities rose (15.6% and 4.2%, respectively), while both silver and gold fell (-2.2% and -1.5%, respectively).

Fed Holds Steady; Powell to Stay on as Governor

The Federal Reserve held rates steady for the third straight meeting at its April FOMC, keeping the target range at 3.50%–3.75%. The vote was 8–4, reflecting an unusually high level of dissent, with views split in both directions. Governor Stephen Miran supported a 25 bps cut, while Presidents Hammack, Kashkari, and Logan preferred maintaining a restrictive stance. The macro backdrop has given little urgency to change course, with unemployment at 4.3% and annualized March Core PCE at 3.2%, above the 2% inflation target. Moreover, Chair Powell noted that inflation risks remain present, including from geopolitical developments and supply-chain disruptions, and indicated that policy decisions will depend on clearer evidence that tariff-related price effects are temporary and that inflation pressures linked to the Iran conflict have moderated. Attention is now on the June meeting, when Kevin Warsh is set to assume the Fed Chair role. Outgoing Chair Powell also stated he will remain a Fed Governor, contributing to continuity during the leadership transition. As of May 1, market pricing via the CME FedWatch Tool implies a 91% probability of another hold at the next meeting.

Rising Costs, Falling Confidence

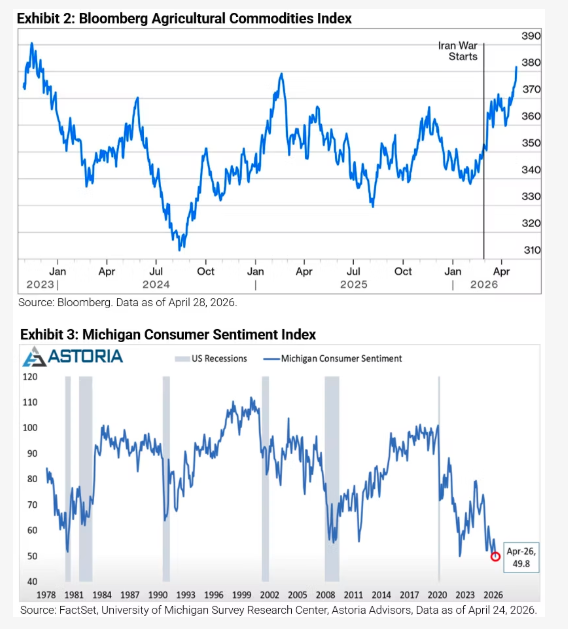

Global equity markets have recouped their recent drawdowns and pushed to new all-time highs, notably without a US-Iran peace deal in place, as the Strait of Hormuz remains effectively closed and negotiations remain stalled. Brent crude has traded above $100 per barrel throughout the end of April, having briefly spiked above $120 amid reports of potential military escalation against Iran and the UAE’s withdrawal from OPEC. Inflationary pressure is also broadening beyond energy, with the Bloomberg Agricultural Commodities Index hitting a 30-month high and signaling stress across the wider commodities complex. Consumer confidence is also weakening, with the University of Michigan Sentiment Index falling to 49.8 in April, its lowest reading on record, while year-ahead inflation expectations surged from 3.8% to 4.7%, the sharpest single-month jump since April 2025. Taken together, these readings suggest consumers are losing confidence while simultaneously bracing for higher prices, a combination that could weigh on discretionary spending.

Forward Earnings Remain Resilient Across Market Segments

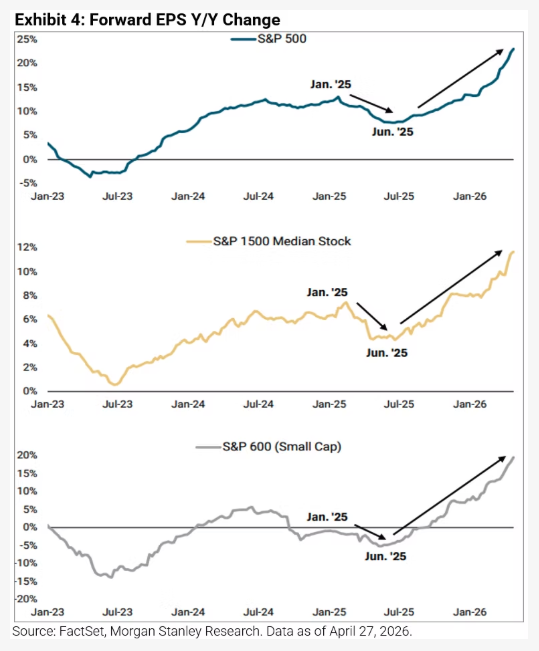

Despite headwinds and risks from geopolitical conflict, forward earnings estimates for the S&P 500 continue to inflect higher. Notably, this earnings resilience is not isolated to large-caps. Forward earnings estimates for both the median stock in the S&P 1500 and small-caps via the S&P 600 have continued to rise into double-digit territory, suggesting the earnings recovery continued to broaden across the market. Morgan Stanley attributes this to tailwinds from a rolling recovery in the earnings and capex cycle, fiscal support via tax cuts, and the ongoing AI buildout and reshoring trend. For Q1 2026, the S&P 500 is on track for its sixth consecutive quarter of double-digit EPS growth, with consensus estimates calling for roughly 12% as of end of March. With approximately 63% of the index now reported as of April 30th, including most of the Magnificent 7, blended EPS growth has surged to around 27%, more than double the March-end estimate.

AI Revenue Now vs. Investment Later

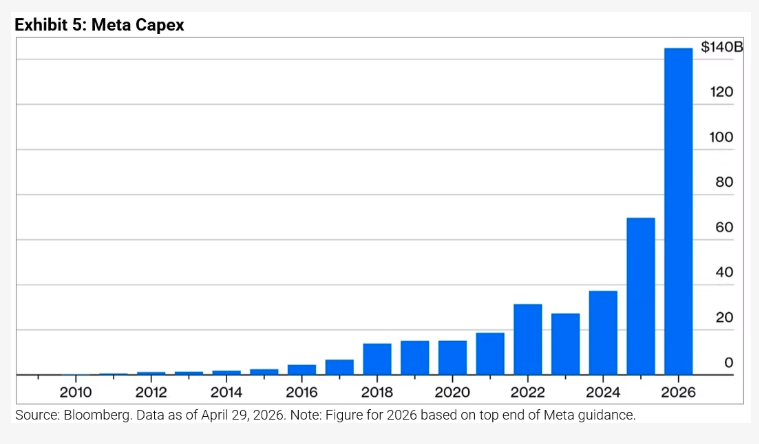

The latest earnings from Alphabet, Amazon, Microsoft, and Meta Platforms reinforce a growing market distinction between near-term AI monetization and longer-dated investment. The divergence was reflected in price action, with Alphabet rising approximately 10% on the day and Amazon modestly higher by ~80 bps, while Microsoft declined roughly 4% and Meta fell about 8.6%. Alphabet grew revenue 20% to $109.9 billion, led by a 63% surge in Google Cloud, which appears to be emerging as a primary growth driver. Amazon reported $181.5 billion in revenue, with AWS growing 28% year-over-year, its fastest pace in 15 quarters, at a 37.7% operating margin. Microsoft delivered 18% revenue growth to $82.9 billion, though Azure’s relative underperformance versus Google Cloud weighed on sentiment. Meta exceeded expectations on both revenue and EPS but increased full-year capex guidance to over $140 billion. Overall, the quarter highlighted a continued divergence in how markets are responding to AI-related spending. Companies demonstrating clearer near-term monetization, such as Alphabet and Amazon, saw more favorable reactions, while those continuing to invest heavily for future returns, such as Meta and Microsoft, experienced more muted or negative price responses despite solid fundamental results.

Click here to view this report as a PDF.

Originally posted on Astoria Advisors

For more news, information, and analysis, visit the ETF Strategist Content Hub.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in SPYG, SPY, SPYV, SPDW, SPMD, SPSM, SPEM, SPBO, SPAB, MUB, IEF, SPIP, GLD, SLV, USO, BCI, META, MSFT, GOOGL, and AMZN on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by Astoria Portfolio Advisors