Key Takeaways

- Oil prices are set to move meaningfully lower by year-end

- Once the Strait of Hormuz reopens, production should ramp up quickly

- Higher energy prices pose a headwind, but the economy and markets can absorb it

With two months having passed since shipping through the Strait of Hormuz was effectively shut down, the world is now facing the largest oil supply disruption in history, driving prices well north of $100 per barrel. The key question we’re getting from investors is: Where does oil go from here? Despite ongoing uncertainty around potential US‑Iran escalation or de‑escalation, we expect prices to move meaningfully lower over time, converging toward our recently updated $70 per barrel forecast by year‑end. This view assumes shipping traffic recovers to pre‑war levels by mid‑July, though we acknowledge the diplomatic path and its timing remain uncertain. Importantly, our oil outlook still does not imply a recession; while higher energy prices pose an economic headwind, particularly for inflation, we still expect the path of oil prices to trend lower into year‑end for four key reasons.

Four reasons why oil prices should move lower by year-end

Despite currently elevated oil prices, we remain confident that oil prices can decline meaningfully towards $70 per barrel by year-end for the following reasons:

Both the US and Iran need a durable off-ramp

The Iran conflict has proven deeply unpopular, with approval averaging around 30%. With the midterms just over six months away, political considerations are likely to factor into how the White House charts its path forward. The longer $4.00+ per gallon prices at the pump persist, the more downward pressure it will place on Republican approval ratings, raising the likelihood of a Democratic sweep of Congress. At the same time, Iran also has a strong incentive to reach a deal. The US blockade of Iranian ports has effectively cut off its oil exports, severing a key source of export revenue for its economy. Iran is facing an estimated GDP decline of nearly 10% this year. With both sides motivated to strike a deal, an offramp appears likely. The key uncertainty is the timing.

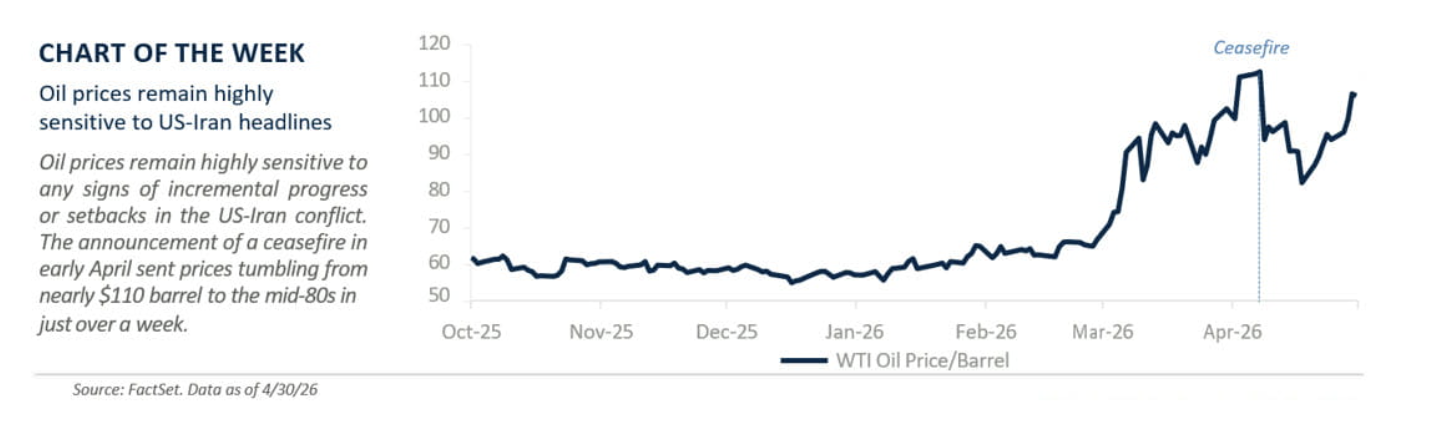

The supply disruption is primarily a shipping issue

The good news is that oil infrastructure, unlike LNG infrastructure, has suffered only limited damage from recent military actions. Once US-Iran negotiations reach a settlement, shipping traffic through the Strait of Hormuz should normalize relatively quickly. With safe transit restored, countries around the Persian Gulf would be able to resume oil production at pre-war levels. While the timing of a diplomatic breakthrough remains uncertain, our base case assumes that shipping gradually normalizes by mid-July. More important, markets are highly sensitive to any signs of incremental progress. Case in point: WTI oil prices dropped from ~$110 to ~$80 per barrel as reports of a ceasefire made news headlines in early April.

Read more: Wars, Markets and Economic Growth

There is already evidence of oil demand weakening

Over the past two months, we estimate that over 800 million barrels of global oil supply has been lost. Under our base case, cumulative losses could rise to an estimated range of 1.2 to 1.5 billion barrels. With the International Energy Agency’s (IEA) 32 members committing to release 400 million barrels from emergency stockpiles, this offsets no more than one-third of the supply loss. The remaining adjustment will most likely come through what the industry calls demand destruction, and it is already happening.

In developed economies and China, impacts have been modest, including suspension of select airline routes and changes in individual travel plans. The Eurozone economy also saw a sharp slowdown in growth to just 0.1% QoQ in Q1, as elevated energy prices weigh on economic activity. Meanwhile, in lower-income countries, the impacts may be more serious, with fuel rationing and remote-work mandates for government employees being implemented. Putting all that together, the IEA projects global demand to decline in 2026, for the first time since COVID. In essence, higher oil prices are often the “cure” for higher oil prices.

New supply is coming onstream

As important as the Persian Gulf is, other sources of oil supply are set to contribute as 2026 progresses. This includes oilfield projects that are scheduled to be completed in Brazil, Canada, Norway, Uganda and the US. As these oilfields come onstream in the coming months, the incremental supply (roughly 1.1 million barrels per day in aggregate) should mitigate the impact of the Mid-East disruption. In addition, the United Arab Emirates (UAE) decision to end its membership with the Organization of the Petroleum Exporting Countries could further bolster supply once war-related disruptions cease and the strait fully reopens. Over time, these factors should place additional downward pressure on oil prices even though the market remains focused on near-term supply tightness. Energy stocks have benefited from higher oil prices but remain ~5% below their recent peak and have lagged the S&P 500 by over 10% since the April 7 ceasefire, as investors question how long elevated prices can last.

Bottom line

While oil prices are likely to remain elevated in the near term, we do not view the current disruption as a lasting supply shock. A diplomatic resolution, or even progress toward one, should help bring prices lower by year-end. Although higher oil prices are a headwind, we believe both the economy and equity markets can absorb the impact with limited damage, as underlying fundamentals remain strong.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success.

Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.

The S&P 500 Total Return Index: The index is widely regarded as the best single gauge of large-cap U.S. equities. There is over USD 7.8 trillion benchmarked to the index, with index assets comprising approximately USD 2.2 trillion of this total. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization.

Sector investments are companies focused on a specific economic sector and are presented here for illustrative purposes only. Sectors, including technology, are subject to varying levels of competition, economic sensitivity, and political and regulatory risks. Investing in any individual sector involves limited diversification.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition - September 2025 (PDF)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Raymond James

More Fixed Income Topics >