Key takeaways

- The market regime is shifting from concentration to competition. The forces that drove U.S. dominance and narrow leadership are evolving, creating a more complex and less stable environment.

- Opportunity is expanding globally and becoming more interconnected. Higher rates, fiscal policy, regionalization, and AI are driving returns in unexpected places.

- Dispersion is rising, making active and portfolio construction critical. Outcomes are diverging across regions, sectors, and companies, while many portfolios remain exposed to legacy concentrations built for a different regime.

- How you go global now matters as much as going global. Capturing opportunity increasingly requires an integrated approach that allocates across markets, not just between U.S. and non-U.S. buckets.

Global equity markets entered 2025 with a familiar narrative. U.S. leadership remained firm, supported by strong earnings, AI-driven optimism, and a market structure increasingly dominated by a narrow group of large-cap companies. For many investors, the path forward seemed clear: stay anchored to what worked.

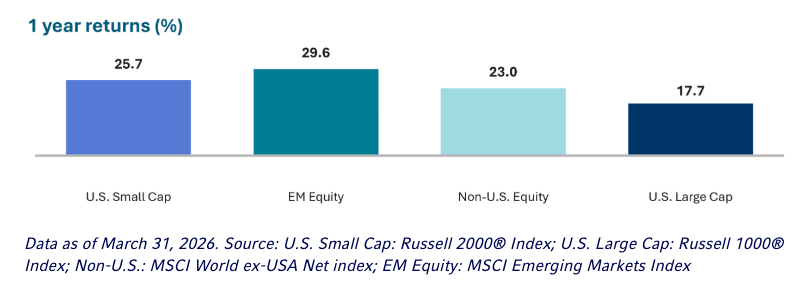

However, over the course of the year, the narrative shifted. Leadership broadened as non-U.S. equities gained traction. More cyclical sectors and smaller companies began to participate more meaningfully. U.S. large cap equities that have long been the dominant force in global portfolios, underperformed global markets on a relative basis.

Read more: Wars, Markets and Economic Growth

In 2026, this shift appears to be accelerating. The market continues to be driven by AI disruption, while geopolitical tensions and the subsequent energy shock, are reshaping returns across regions and sectors.

The environment that defined the last decade — low rates, U.S. dominance, globalization, and concentrated leadership — is evolving. What’s replacing it is less stable, more competitive, and far more dispersed.

Performance across U.S. & non-U.S equities

Why global?

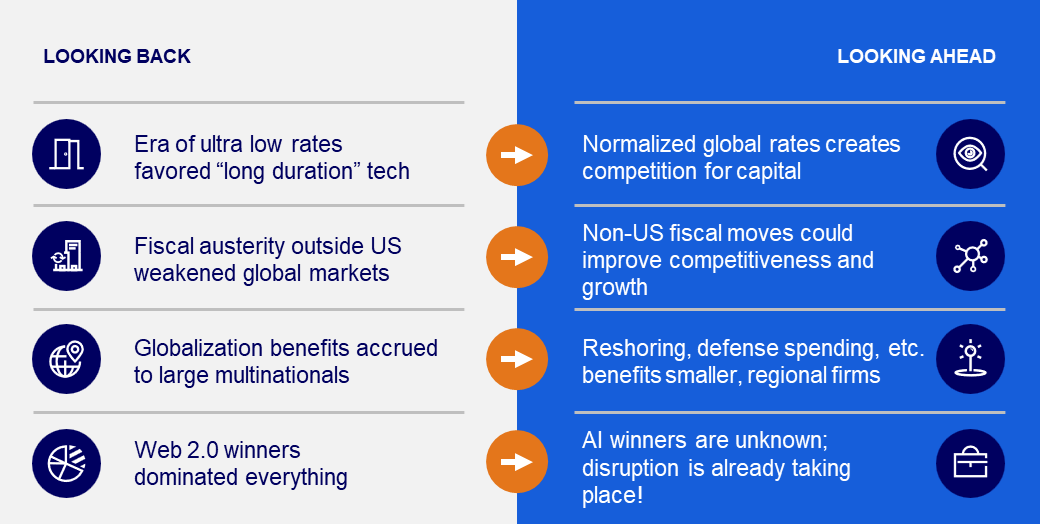

To understand why the opportunity set is broadening, it helps to look at what worked before and what is changing now.

For much of the past decade and beyond, ultra-low interest rates have favored long-duration growth assets. Capital flowed to companies whose earnings were far out in the future, reinforcing the dominance of U.S. technology and internet platforms.

Today, rates have normalized globally, meaning capital is no longer free. More parts of the market can compete for it which is creating a more balanced opportunity set across sectors and regions.

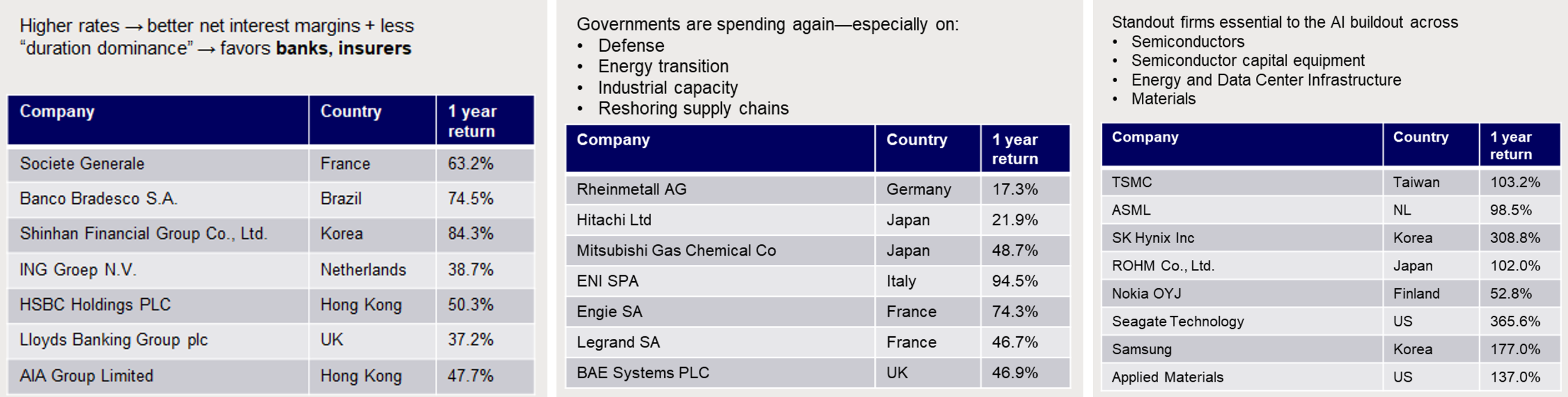

Fiscal policy has changed meaningfully since the early 2010s. Outside the U.S., years of relative austerity weighed on growth and market performance. However, this is changing rapidly, with governments now investing in defense, energy security, and industrial capacity, particularly in Europe and Japan. These investments support a broader range of companies and sectors that were previously overlooked.

The world is shifting from global to regional. In the prior regime, globally integrated supply chains disproportionately benefited large multinational companies. Today, supply chains are becoming more regional and resilient. Reshoring, defense spending, and energy independence are supporting smaller, locally focused businesses and creating more differentiated opportunities across markets.

Finally, technology itself is changing. The Web 2.0 era created clear winners — platform businesses with powerful network effects that came to dominate both the economy and equity markets.

AI is changing the landscape dramatically. It is a powerful theme, but its winners are far less certain. The buildout is global, spanning semiconductors, infrastructure, energy, and materials. The beneficiaries are distributed across regions and industries, not concentrated in a single market.

Taken together, these shifts point to a clear conclusion. Global investing today isn’t about diversification for its own sake. It’s about accessing a broader and more relevant set of opportunities.

Why active management?

As opportunity expands, outcomes are becoming more uneven, which warrants an active approach to portfolio management.

The past year has shown how quickly leadership can shift — from European financials to AI-driven growth to energy and defensives — often within the same quarter. Markets are being driven by multiple forces at once, from structural innovation to geopolitical shocks.

Many portfolios today carry exposures that aren’t always obvious. Over time, allocations have tilted toward growth, technology, and the U.S. While those exposures worked in the previous regime, they can become vulnerabilities as leadership changes, and passive investing can miss meaningful opportunities.

It is no longer simply sector rotation. Outcomes are diverging:

- Across regions (energy exporters vs. importers, fiscal expansion vs. restraint)

- Across sectors (financials vs. long-duration growth, industrials vs. asset-light models)

- Within industries (AI beneficiaries vs. disruption losers)

This creates a more complex opportunity set that cannot be captured effectively through broad index exposure alone.

There are already clear examples of this playing out. Many of the strongest performers over the past year have come from areas that had minimal or no representation in major indices, including non-U.S. financials, beneficiaries of fiscal expansion, and companies tied to AI infrastructure investment.

Past performance does not predict future returns. Source: Russell Investments. Total returns in USD, net of dividend withholding tax. Data as of March 31, 2026

At the same time, risks are increasingly embedded, not explicit. Factor tilts, sector concentration, and regional exposure can accumulate over time, leaving portfolios more dependent on a narrow set of outcomes than they appear on the surface. Active management is critical in this environment, not just for stock selection, but for portfolio construction.

Why an integrated approach is crucial

If the opportunity set is becoming more global, the next question is how that exposure is built. Many portfolios still approach global investing by combining U.S. and non-U.S. allocations, typically managed separately and benchmarked independently. That structure reflects how markets used to behave, but it is less effective in today’s environment.

Capturing today’s opportunities requires coordinated decision-making across regions. This means making relative value decisions between markets, allocating capital efficiently to the most attractive opportunities worldwide, and managing unintended regional or factor exposures as they emerge.

By contrast, simply bolting together separate U.S. and non-U.S. portfolios can create blind spots. It can miss cross-market opportunities, reinforce unintended biases, and limit a portfolio’s ability to adapt as leadership shifts across regions. In a market where opportunity is increasingly global and interconnected, implementation is not just a detail, it is a defining factor.

Why act now?

The past year has shown how quickly markets can change direction. The forces that defined the past 15 years are rapidly evolving and for investors this means rethinking how portfolios are constructed:

- Where are the real sources of opportunity?

- Where are the hidden concentrations?

- And how aligned is the portfolio with the environment ahead?

A global, active approach is no longer just a diversification decision. It is the difference between being positioned for the market that was, and the market that is emerging.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Diversification and strategic asset allocation do not assure a profit or guarantee against loss in declining markets.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The Russell Investments logo is a trademark and service mark of Russell Investments

The information, analyses and opinions set forth herein are intended to serve as general information only and should not be relied upon by any individual or entity as advice or recommendations specific to that individual entity. Anyone using this material should consult with their own attorney, accountant, financial or tax adviser or consultants on whom they rely for investment advice specific to their own circumstances.

Products and services described on this website are intended for United States residents only. Nothing contained in this material is intended to constitute legal, tax, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. The general information contained on this website should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional. Persons outside the United States may find more information about products and services available within their jurisdictions by going to Russell Investments' Worldwide site.

Russell Investments is committed to ensuring digital accessibility for people with disabilities. We are continually improving the user experience for everyone, and applying the relevant accessibility standards.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management, L.P., with a significant minority stake held by funds managed by Reverence Capital Partners, L.P. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

© Russell Investments Group, LLC. 1995-2026. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

© Russell Investments

More Fixed Income Topics >