Commodity Supercycle: The Enemy Of The Bull Thesis (Part 1)

Membership required

Membership is now required to use this feature. To learn more:

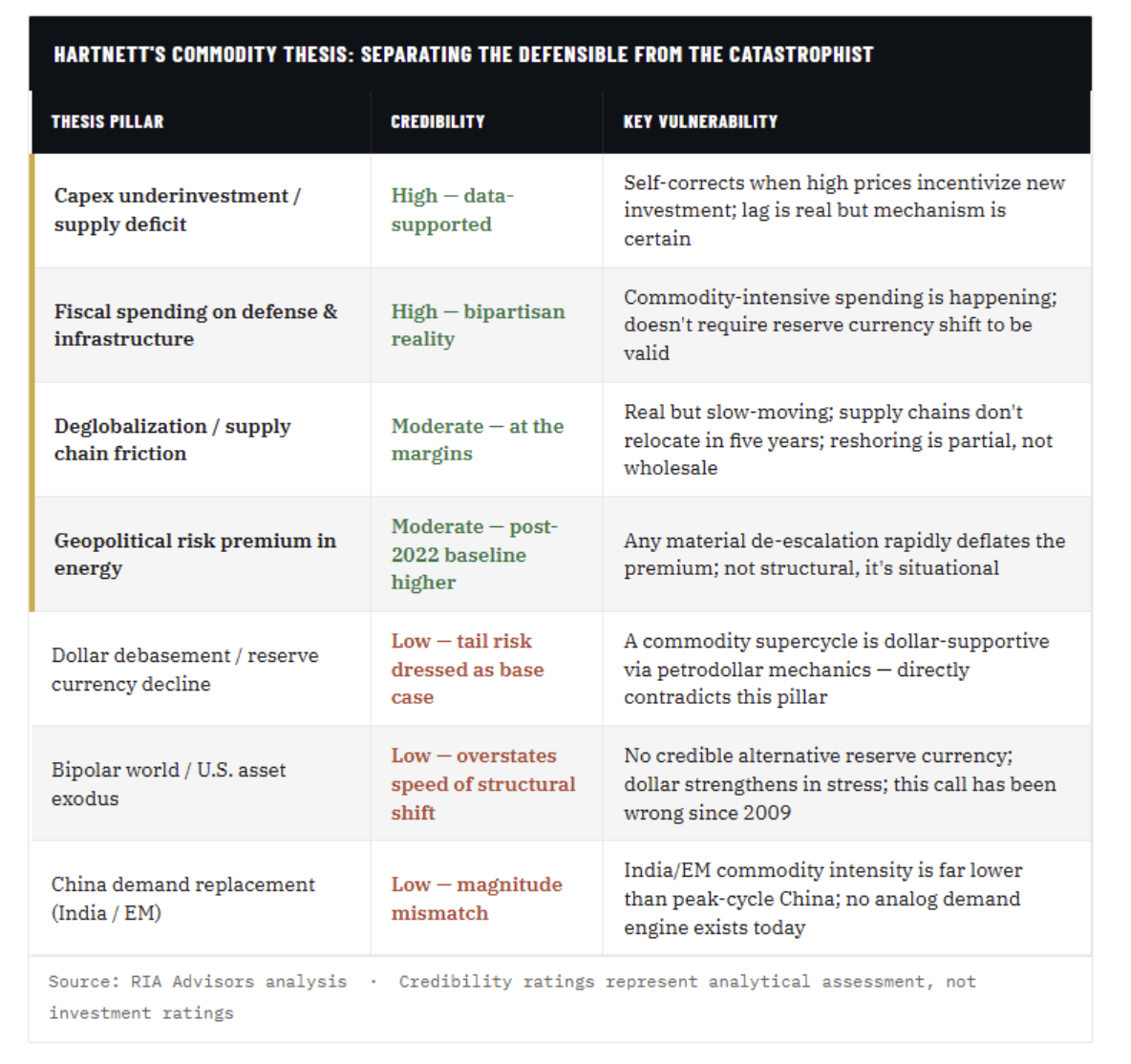

View Membership BenefitsThe commodity supercycle thesis is everywhere right now. Bank of America’s Michael Hartnett, one of the most widely read strategists on Wall Street, recently declared “commodities the biggest trade of the next five years,” anchoring the call on deglobalization, chronic capital underinvestment, and a world drifting away from dollar dominance. As is often the case, the narrative is extremely compelling. However, it’s also internally contradictory in ways that most investors aren’t stopping to examine.

After three decades of managing money, I have learned to be THE most skeptical of the trades that feel the most inevitable. That skepticism isn’t contrarianism for its own sake, but rather the recognition that when a thesis achieves consensus, the crowd has usually already priced the easy part of the move, and the hard part is what comes next. The commodity supercycle argument has real structural legs. But it also carries a reflexivity problem, a dollar mechanics problem, and a catastrophist assumption problem that, taken together, make the clean “go long commodities” conclusion far messier than the headline suggests.

Let’s work through each one carefully, and as always, with the data.

The Reflexivity Problem: When the Trade Defeats Itself

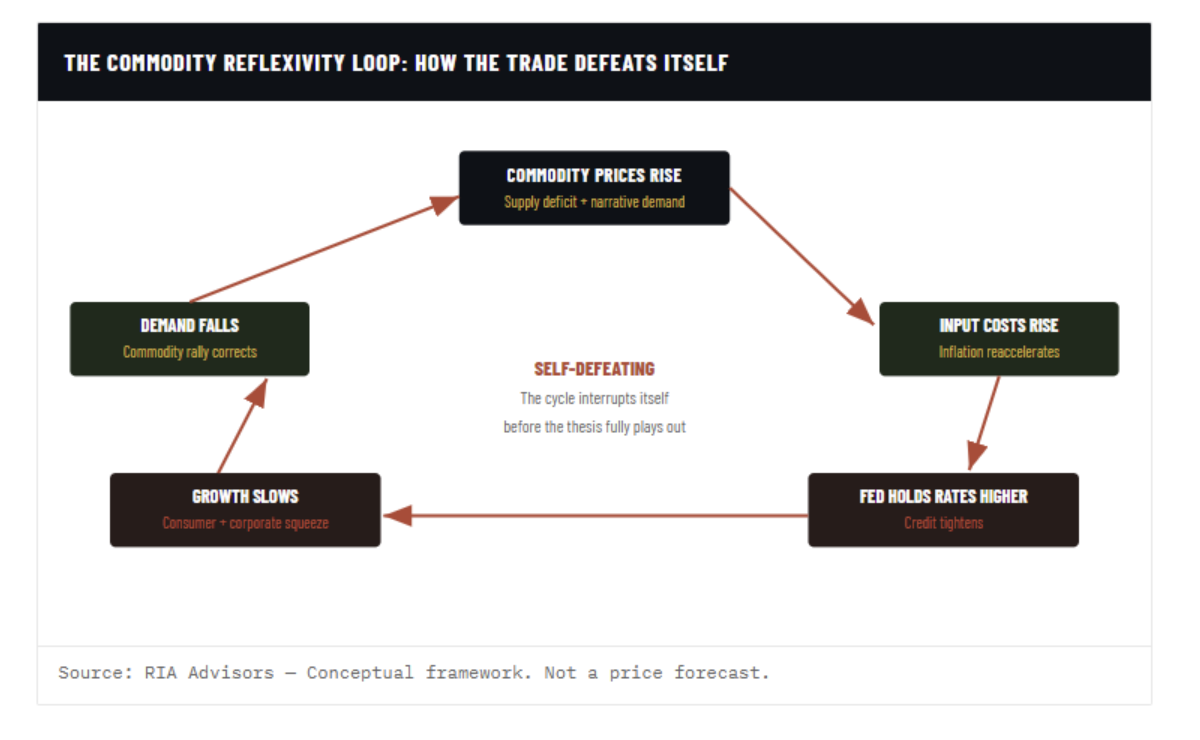

The most straightforward critique of any commodity supercycle thesis is that a sustained commodity rally is, by definition, inflationary. And sustained inflation is demand destruction. Before we get to the counterarguments (there are legitimate ones), it’s worth mapping out the feedback loop precisely, because the mechanism is more complex than the simple “inflation is bad for growth” headline suggests.

Read more: Market Correction Risk: Why Summer 2026 Looks Risky

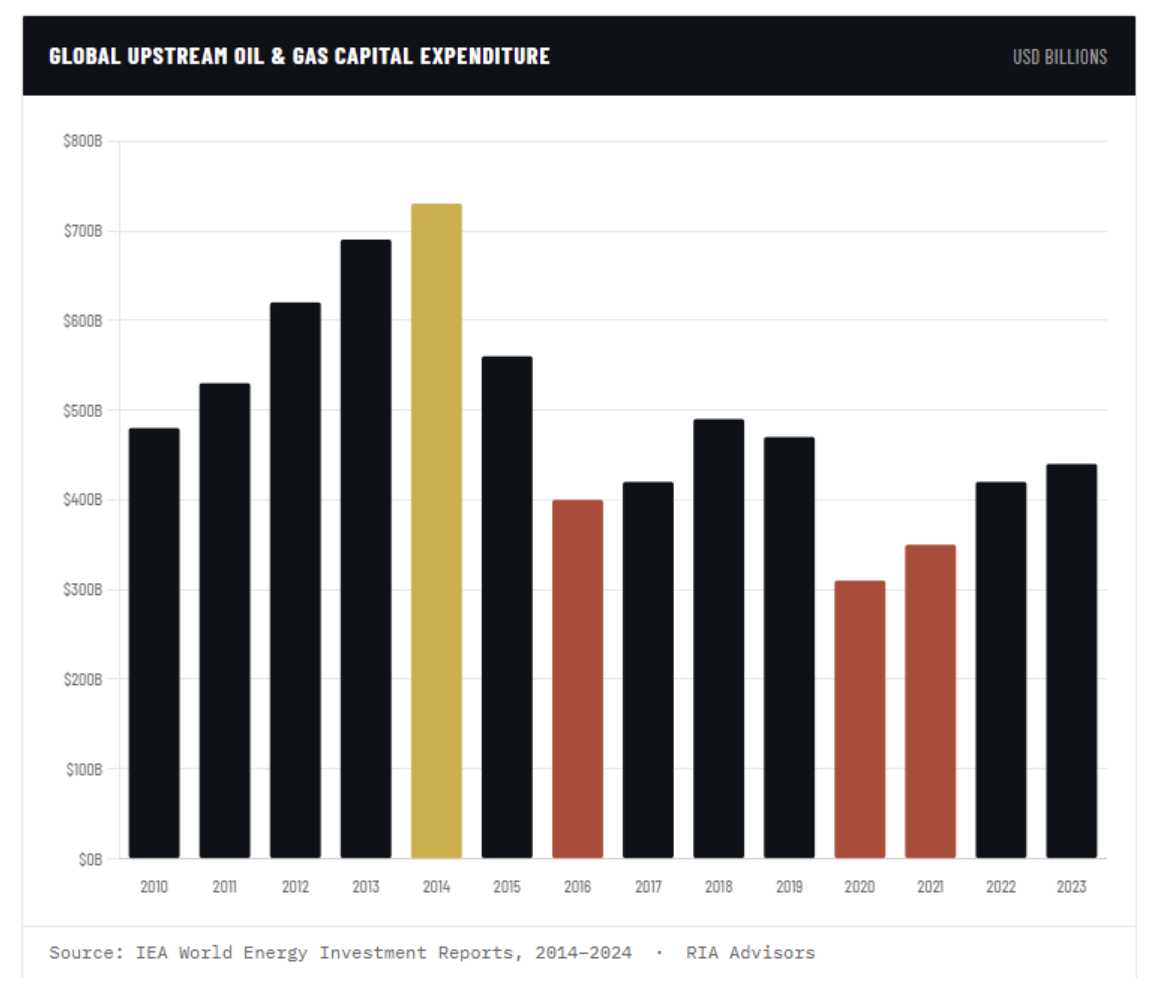

Commodity bulls offer a legitimate counterargument here. First, they distinguish between demand-pull inflation, where a hot economy bids up prices, and supply-constrained inflation. The latter is where chronic underinvestment means the world can’t produce enough regardless of demand levels. Hartnett’s case leans heavily on the supply side, and that’s the more defensible version of the argument. A decade of ESG-driven capital withdrawal from energy and metals, combined with the shale revolution’s diminishing returns, has created real supply deficits in several commodity markets.

The data below illustrates the scale of that underinvestment. Global upstream oil and gas capital expenditure peaked around 2014 and remained roughly 40% below that level as recently as 2023, even as demand returned to pre-pandemic levels. That is a genuine structural story, and certainly is worth paying attention to.

But even granting the supply-side framing, the reflexivity problem doesn’t disappear. This is a point that is often forgotten in the “heat of the moment” of a profitable trade. The markets are not static, but dynamic, and, as the old saying goes, “high prices are a cure for high prices.” There are two reasons why that is true.

First, high commodity prices are a tax on growth by transferring wealth from consumers and manufacturers to producers. That transfer compresses the demand on which commodity producers depend. Governments and central banks respond asymmetrically to commodity inflation by releasing strategic reserves, imposing windfall taxes, or accelerating substitution. The 2022 oil spike is a perfect case study: WTI briefly hit $130 per barrel, the Biden administration released over 180 million barrels from the Strategic Petroleum Reserve, and demand destruction combined with a Fed tightening cycle broke the trade within months of the initial spike.

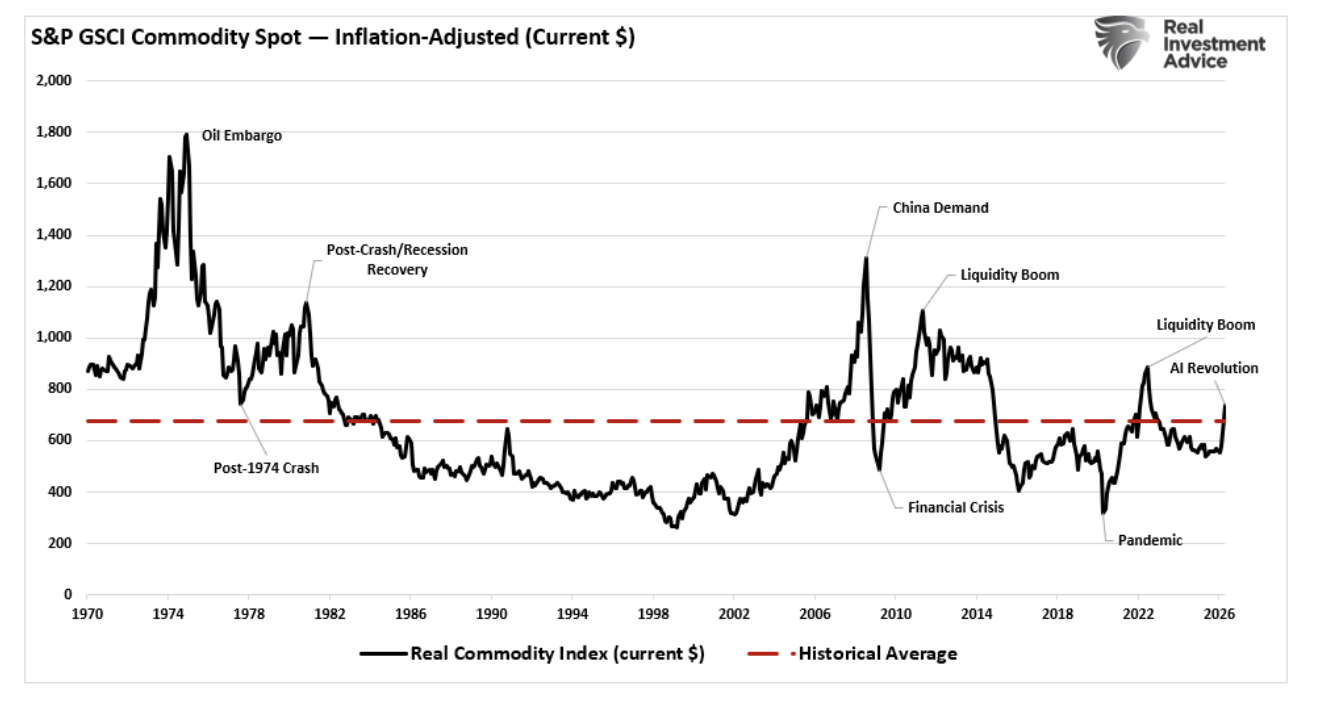

Secondly, high prices bring more supply online. When prices rise, producers are incentivized to produce more products. When that increase in supply collides with the collapse in demand, the cycle reverses quickly due to the supply glut. As shown in the chart below, the commodity market is notorious for booms and busts precisely because of this.

The 2022 episode compressed in real time what would normally take years to play out, but we also saw a similar episode from 2000 to 2007, as China consumed commodities in a push to rapidly grow its economy. That episode crashed in 2008 as the Financial Crisis crushed global demand. The policy/producer response isn’t hypothetical; it’s a documented reflex, and the more dramatic the commodity rally, the more certain the policy response becomes.

The Dollar Contradiction at the Heart of the Thesis

Here’s the fault line that most commodity bulls don’t address directly, and it’s the one I find most analytically significant: virtually all commodities are priced and settled in U.S. dollars in global markets. That’s not incidental; it’s the structural backbone of the petrodollar system that has anchored dollar demand since the 1970s. When oil prices rise, petrodollar recycling intensifies. Commodity exporters accumulate dollar surpluses and recycle them into U.S. Treasuries and dollar-denominated assets (including U.S. equities, gold, and other commodities). More commodity volume at higher prices means more dollar-denominated transactions, more dollar liquidity needs, and more dollar reserves held by commodity-importing nations.

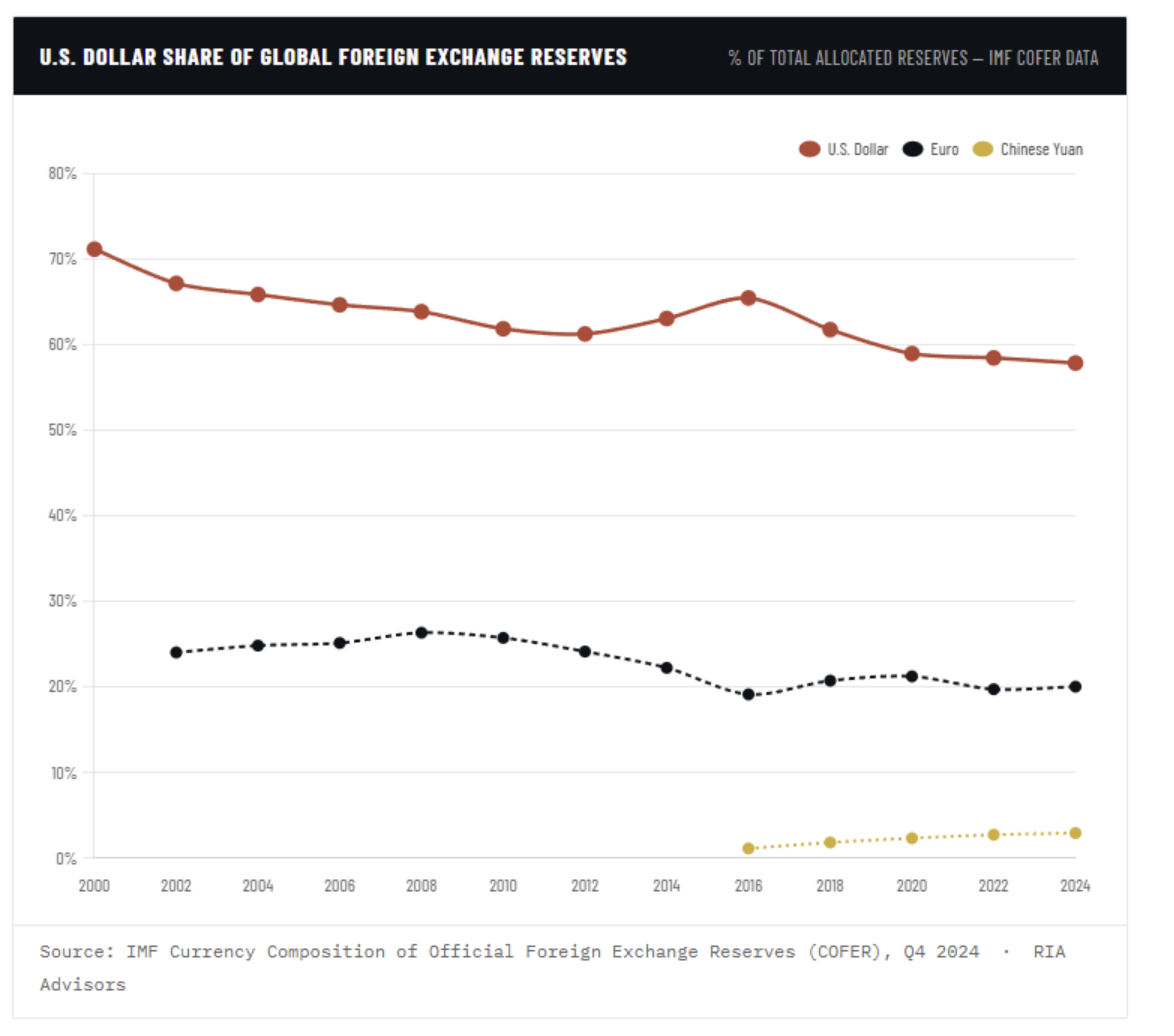

A commodity supercycle, properly understood, is structurally dollar-supportive, not dollar-negative. As shown, many point to the decline in the US dollar’s “share” of global foreign exchange reserves as “proof” of its declining dominance.

The chart above tells a story the catastrophist crowd loves to cite, and they’re not wrong that the dollar’s reserve share has declined from its 2000 peak of roughly 71%. But look carefully at the actual level: as of late 2024, the dollar still accounts for approximately 57-58% of global reserves. The next closest competitor, the euro, sits around 20%. The Chinese yuan, despite years of de-dollarization rhetoric, accounts for less than 3%. The decline is real, but only because the Euro did not exist before 1999, and the Yuan only became accepted for trade on a limited basis a few years ago. However, a crisis it is not, and a commodity cycle only strengthens the dollar position.

This creates a direct contradiction with the other major pillar of the commodity bull narrative: the dollar debasement story. If the thesis requires dollar weakness to fully materialize, and many versions of it explicitly do, then a successful commodity cycle works against that by generating incremental dollar demand. The two arguments pull in opposite directions, and that tension is almost never acknowledged in the thesis presentations.

The only scenario in which both the commodity bull and the dollar bear cases work simultaneously is one in which U.S. fiscal excess debases the dollar faster than commodity-driven dollar demand can offset it. That requires a genuine crisis of fiscal confidence, a level of sovereign stress that isn’t currently visible and isn’t probable within a five-year investment horizon. Yes, the U.S. deficit is running approximately $1.8 to $2 trillion annually, interest expense has eclipsed defense spending, and the CBO projects no credible stabilization path under current policy. That is a real long-run problem over the next 30-50 years. But it’s not a five-year catalyst.

The China Problem: No Replacement for the Original Engine

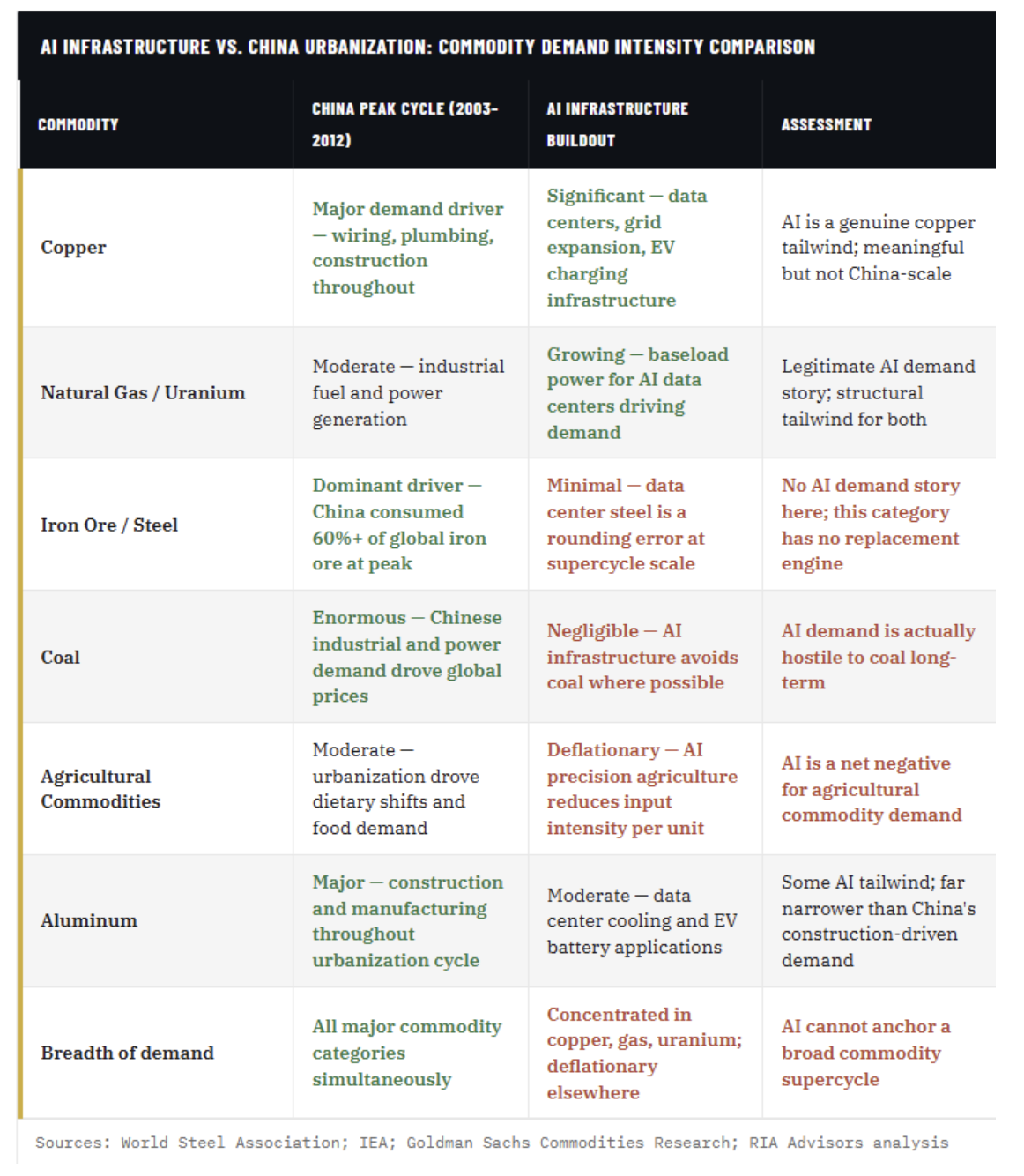

China is the most critical lynchpin to the commodity supercycle. The 2000s commodity supercycle, the one this thesis is implicitly invoking as its template, was not primarily a supply story. It was a demand shock of historic proportions, and it had a name: China’s urbanization and industrialization. Between 2000 and 2012, China accounted for roughly half of all incremental global demand growth for steel, copper, aluminum, and coal. Its share of global iron ore consumption grew from under 20% to over 60% in that same period. That’s not a supply-deficit story. That’s a billion people building cities that no one lived in, which have now become an economic anchor.

That engine is now structurally impaired, and the table below illustrates why the India- and emerging-market “replacement demand” narrative falls significantly short of the original.

India’s commodity demand growth is real, and the broader emerging market infrastructure buildout adds genuine incremental demand. But there’s no single country or bloc that replicates the concentrated, high-velocity demand shock that China delivered between 2000 and 2012. The 2000s supercycle had a demand engine of historic scale running underneath it. Hartnett’s version relies on supply-side logic. In the absence of a comparably powerful demand driver, the supply/demand imbalance will not be as significant.

Meanwhile, as noted, China’s property sector collapse has removed the world’s single largest commodity demand driver. At its peak, Chinese real estate accounted for roughly 25-30% of GDP when the full construction supply chain is included. That’s not recovering in five years. The commodity demand that China generated during its construction boom was effectively borrowed from the future. Now that the borrowed “future” is arriving, it came as a demand vacuum.

Tail Risk Dressed as Base Case: The Catastrophist Problem

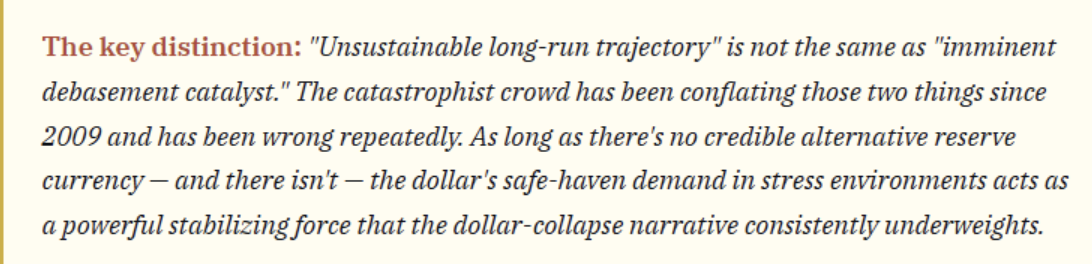

The “dollar demise / U.S. asset exodus / bipolar world” framing has been a persistent feature of bearish macro commentary since at least 2009. Every round of quantitative easing was supposed to be the moment dollar credibility broke. Every geopolitical fracture, the European debt crisis, Russia’s annexation of Crimea, the U.S. credit downgrade, and the rise of the BRICS payment alternatives, was supposed to accelerate de-dollarization beyond the margin.

None of it happened on the timeline or at the magnitude the catastrophist crowd predicted. And yet the narrative keeps resurfacing and gets refreshed with new catalysts because the old narrative failed. That is why those castraphosists always have a key statement: “just not yet.”

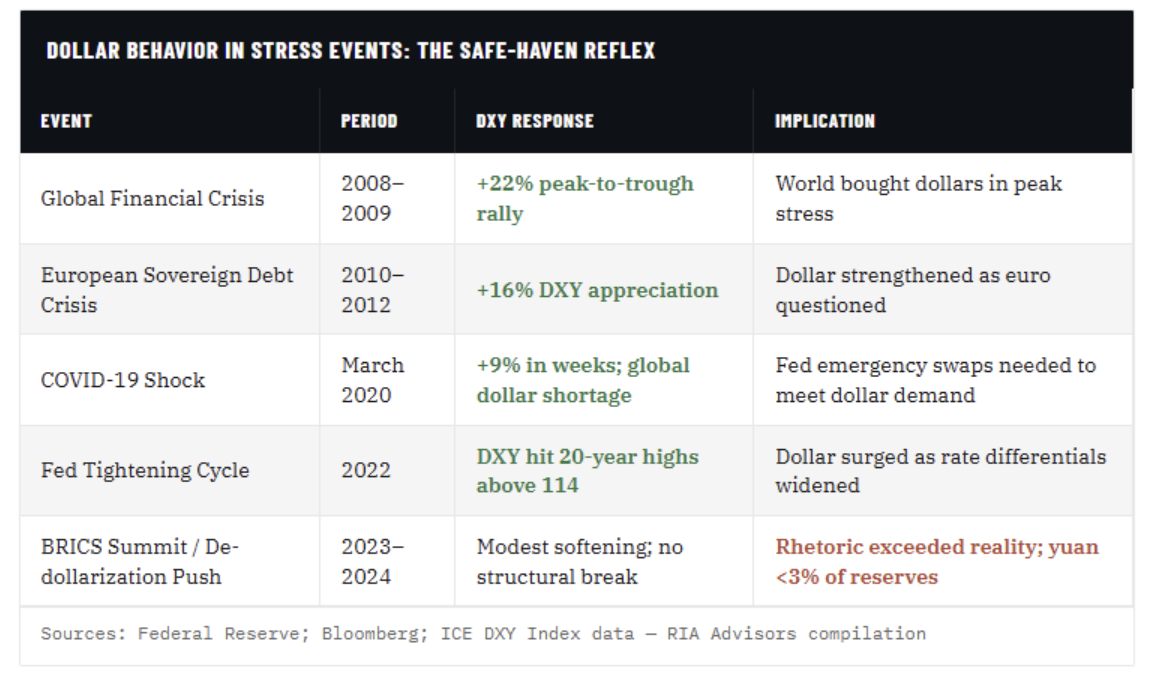

The table above makes a straightforward point. In every major crisis of the past 20 years, the world’s response has been to buy dollars, not sell them. The de-dollarization that Hartnett and others embed in their commodity bull thesis requires the world to do the opposite. Rather, the world would shift away from dollar-denominated reserves and transactions in a sustained, structural way. There’s no evidence that’s happening at the pace or scale the narrative requires.

This doesn’t mean the dollar is invulnerable. The fiscal trajectory is genuinely concerning over a multi-decade horizon. A term premium reset in U.S. Treasuries is already underway, driven by foreign buyers demanding more compensation for duration risk. These are real and worth monitoring. But they’re 10 to 15-year dynamics, not five-year catalysts. Hartnett is packaging a legitimate long-run concern as an imminent trade driver, and that’s where the analytical rigor slips.

What This Means for Investors

I want to be precise about what I’m arguing and what I’m not. I’m not saying commodities are a bad investment or that the structural supply-deficit case is wrong; it’s not. Energy, select industrial metals, and agricultural commodities face real, medium-term supply constraints. Those constraints should support prices above the levels they traded at in the 2010s deflationary decade. The capex destruction of the prior cycle created a genuine deficit. That deficit will take years to close, and that story is worth holding exposure to in a diversified portfolio.

What I’m arguing is that the clean, multi-year commodity supercycle narrative, particularly the version built on dollar collapse and a wholesale shift away from U.S. assets, overstates the probability of its own enabling conditions. And more importantly, it contains a logical fault line: the commodity supercycle itself is dollar-supportive, not dollar-negative. The two main pillars of the thesis pull in opposite directions.

But What About The AI Boom?

Here is the real question. Can the artificial intelligence infrastructure boom replace China’s urbanization as the demand engine underneath a new commodity supercycle? The short answer is no, and understanding why clarifies exactly what kind of commodity opportunity we’re actually dealing with.

AI infrastructure does generate real commodity demand. Data centers require significant copper for power distribution and cooling systems. The grid expansion needed to support hyperscaler compute loads is driving demand for steel, aluminum, and transformers. Natural gas and nuclear power are being positioned as the baseload energy sources for facilities that can’t tolerate renewable intermittency. Goldman Sachs estimated that data center power demand could grow by roughly 160% by 2030, a figure worth taking seriously. Copper in particular has a legitimate AI demand tailwind, and uranium’s renaissance as a clean baseload energy source is directly tied to this infrastructure buildout.

But here’s where the China comparison breaks down completely. China’s urbanization moved roughly 500 million people from subsistence agriculture into cities over 20 years. It required building entire urban ecosystems. That boom required everything from roads and bridges to apartment towers, factories, ports, and railways. All scratch, simultaneously, across every commodity category at once. That was broad-based, high-intensity demand across iron ore, coal, copper, aluminum, cement, and energy, running in parallel. A true commodity supercycle requires that kind of breadth. AI infrastructure demand is concentrated almost entirely in copper and electricity. It doesn’t move the needle on iron ore, agricultural commodities, coal, or the dozens of other categories that a genuine supercycle requires.

There’s an irony here that rarely gets discussed.

“AI is simultaneously the most compelling new source of commodity demand and one of the most powerful long-run deflationary forces for commodity consumption.“

AI-driven efficiency gains in manufacturing, logistics, energy management, and precision agriculture reduce the per-unit economic output intensity of commodities. Predictive maintenance reduces equipment replacement cycles. Smart grid management reduces transmission losses. The same technology driving data center copper demand is also optimizing the systems that consume commodities everywhere else in the economy. Over a five-year horizon, those efficiency gains compound. The net commodity impact of the AI revolution is almost certainly positive. However, it is far more modest than the bull case narrative implies.

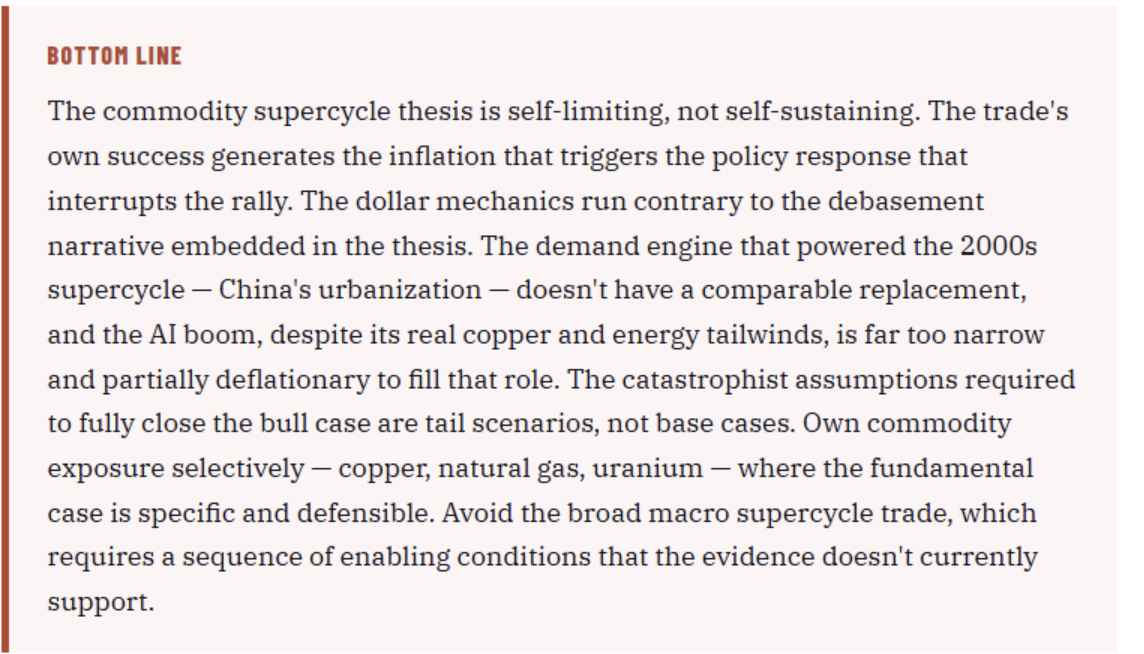

Conclusion

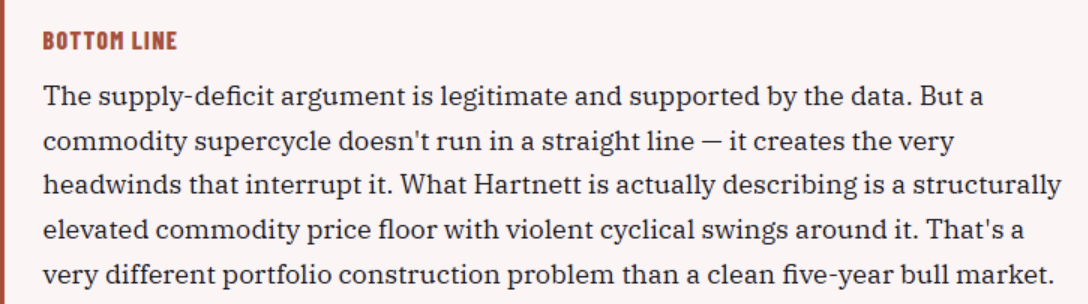

The highest probability scenario, a structurally elevated commodity price floor with significant cyclical volatility, doesn’t support a set-it-and-forget-it long commodity position. It supports tactical, rules-based exposure management. The investors who generated the most alpha during the 2000s commodity bull weren’t the ones who correctly read the structural thesis in 2001 and held through 2008. They were the ones who managed position sizes through the cyclical interruptions and had predefined frameworks for when to add and when to reduce.

That discipline is exactly what the current “biggest trade of the next five years” framing discourages. When a thesis gets packaged as a multi-year certainty, it creates complacency about the cyclical risks embedded in the trade. Those risks — recession-driven demand destruction, Fed policy response, dollar strength in stress events — are precisely the ones that cause the most damage to investors who sized positions based on narrative conviction rather than risk-adjusted analysis.

Sources & Endnotes

1 International Energy Agency, World Energy Investment 2023 & 2024 — upstream oil and gas capex data 2014–2024.

2 U.S. Department of Energy, Strategic Petroleum Reserve Release Data, 2022; EIA crude oil price history.

3 IMF, Currency Composition of Official Foreign Exchange Reserves (COFER), Q4 2024 — U.S. dollar share approximately 57.8%.

4 Congressional Budget Office, The Budget and Economic Outlook: 2024 to 2034 — deficit and interest expense projections.

5 World Steel Association, Steel Statistical Yearbook, various years; BP Statistical Review of World Energy 2023.

6 IMF Working Paper, “The Decline of China’s Real Estate Sector,” 2023 — real estate and construction share of Chinese GDP at peak cycle.

7 Goldman Sachs Equity Research, “AI Data Centers and the Coming Electricity Surge,” 2024 — data center power demand growth projections through 2030.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube Customer Relationship Summary (Form CRS)

Join RIA Advisors and elevate your career within a deeply experienced team focused on innovation. Our collaborative environment is built on a foundation of advanced technology and effective investment models, designed to enhance your ability to serve clients and grow your practice. Benefit from a supportive culture that encourages professional development and fosters a forward-thinking approach. By joining our team, you’ll be part of a group dedicated to excellence and continuous improvement, empowering you to focus on building meaningful client relationships and pursuing your business ambitions. Discover the advantages of working with our accomplished advisory team by starting your conversation today.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All