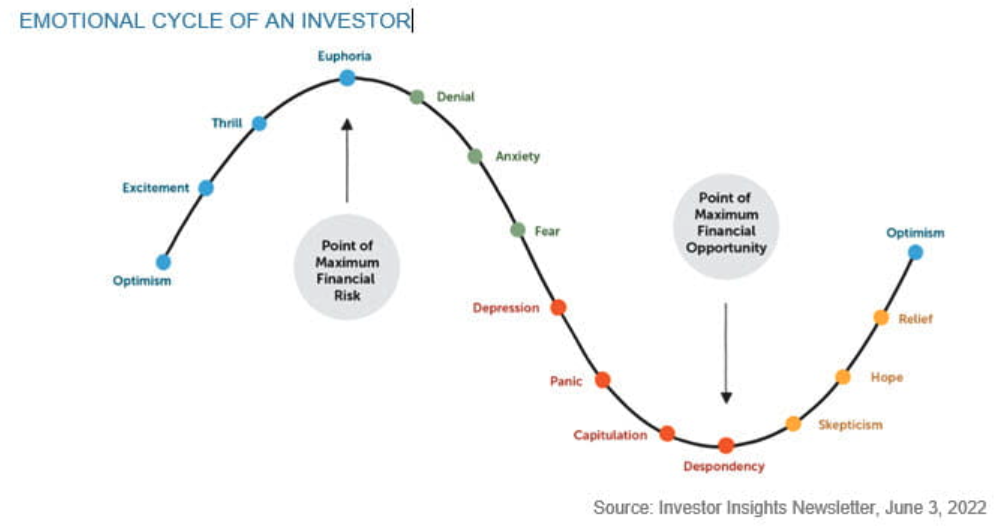

Psychology plays a larger role in our investing lives than many of us care to admit. Often, when investing, we would be better off being a bit more robotic and a bit less human. The reason behind this is often our feelings influence our decisions in ways that are not always to our advantage. Today we are going to focus on the emotional cycle of the investor. None of us are the same, but we all need to recognize how it influences us.

In six of the past seven years the S&P 500 has seen double digit returns. That recency bias makes us feel like we can take on more risk as it has been a minute since we felt the sting of a significant downturn. Most of us tend to overreact in both directions. When things look bleak, we tend to become too conservative at a time that we are supposed to add to riskier assets. When things look great, we tend to take on more risk when we are supposed to sell some of the “winners” to add to the conservative side of the allocation. Let’s look at what some of us should recognize and take advantage of in the current environment.

EMOTIONAL CYCLE OF AN INVESTOR

For those investors at or near retirement the opportunity to create income stability can give great control and confidence going forward. First, let’s remember what it feels like when things look bleak. Pick your memory, the “Tech Wreck” in 2001, the “Great Recession” of 2008-2009, or the market upheaval during COVID in 2020. Any of these events may bring back scary memories. When these market declines began, most investors did not sell riskier investments as they figured it was just a small move. After all, the markets had just been at or near all-time highs and recency bias made us “feel” secure that it would continue. As the markets continued to decline, investors tended to still hold on as they chose not to want to sell during the peaks. It is not until panic sets in that investors sold in mass, driving the markets even lower. At the moment of panic, the markets, of course, were at or near the price bottom. The exact moment we were supposed to buy, right? Yet our emotions were pushing us to do the opposite. Maybe this time we can set up our portfolios to provide positive results during the next downturn, and there will be one. When investing in individual investment grade bonds, you can take control of your outcome by designing custom cash flows to meet your annual lifestyle needs and isolate known dates when your principal is returned. If the cornerstone of your investment portfolio provides the income to live your lifestyle, then hopefully during the next downturn your emotions are tempered as you make decisions from a place of confidence. This may also help to take on risk exactly when you are supposed to instead of selling out of fear.

At Raymond James, your financial advisor’s team of experts can work to create bond portfolios designed specifically around your individual objectives to ensure that you can weather the next downturn. Just a few years ago, interest rates were well below where they are now. Take advantage of the very attractive rates offered today to ensure you are investing from a place of financial confidence.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.