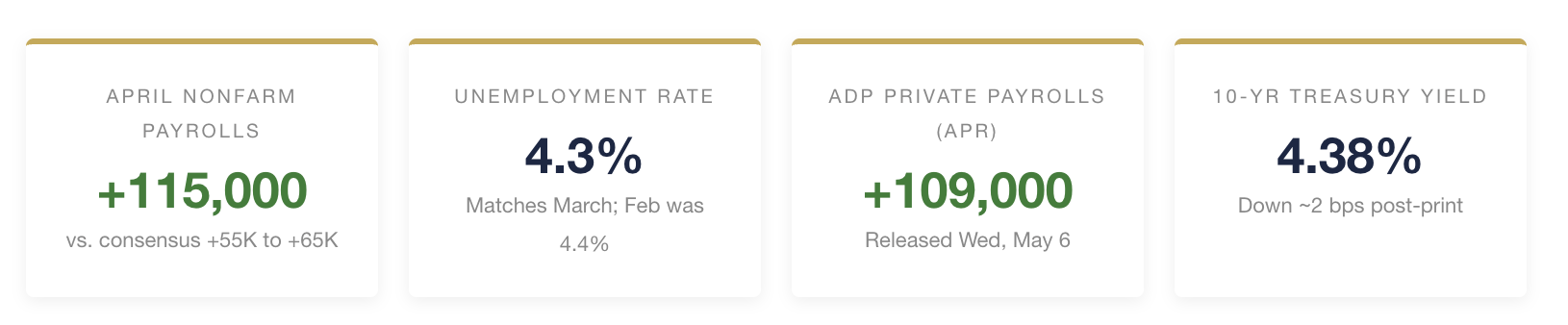

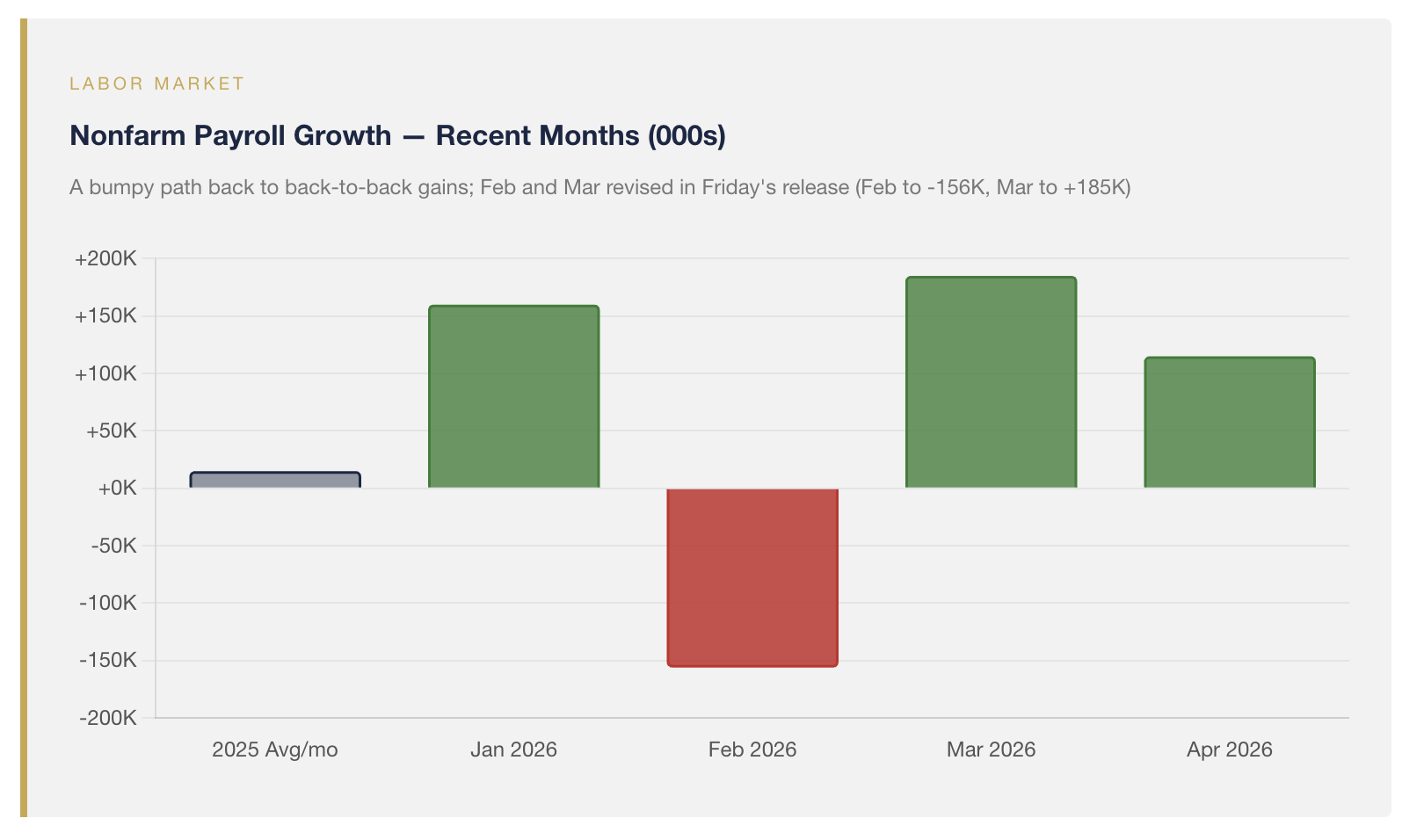

A week dense with data delivered the relief that consensus had been bracing against. The April employment report, released Friday morning by the Bureau of Labor Statistics, showed nonfarm payrolls rising by 115,000 — well above the 55,000 to 65,000 most economists had penciled in — with the unemployment rate holding at 4.3%, matching the March reading after a brief tick up to 4.4% in February. Combined with ADP's May 6 print of 109,000 private-sector additions, the data describes the first back-to-back monthly payroll advance in nearly a year. Treasury yields drifted modestly lower, with the ten-year easing to 4.38% and the thirty-year sitting near 4.95%, and equity markets, which had spent the week swinging on Iran headlines, found a calmer tone. Our reading is that this is a meaningful positive at the surface — a real-time confirmation that the most pessimistic recession scripts written in March can be set aside — but it is also a print that fails to alter the structural calculus we have been describing all year. The labor market is steady. The trajectory of fiscal policy, monetary credibility, and dollar reserve status is not.

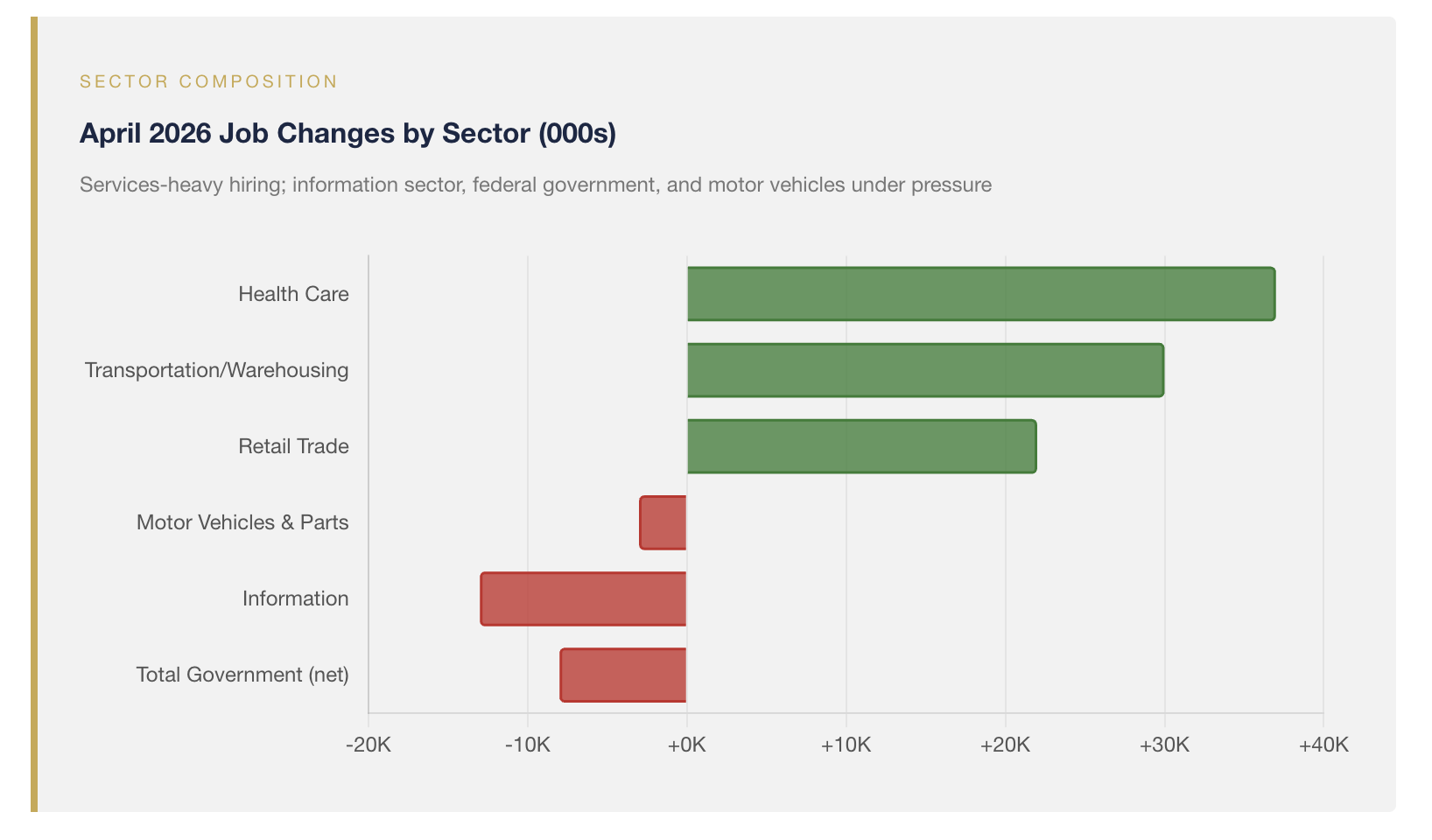

The composition of the April gain matters more than the headline. Health care contributed 37,000 jobs, transportation and warehousing added 30,000, and retail trade added 22,000 — the latter concentrated in warehouse clubs and general merchandise retailers, partially offset by losses at department stores and electronics retailers. Federal government employment continued its DOGE-era decline at -9,000, leaving total government employment down roughly 8,000 on the month even with state and local government roughly flat. Motor vehicle and parts manufacturing slipped by 3,000, and information shed 13,000. The pattern that emerges, as Morningstar described it heading into the print, is the "low-hire, low-fire" labor market: services sectors with structural demand growth absorb workers at a steady rate while interest-rate-sensitive and cyclical sectors flatten or contract at the margin. We do not view this as a discouraging configuration. We view it as a configuration that supports neither the urgent recession case nor the strong-recovery case — and one that gives the Federal Reserve a reason to do exactly what it has been doing, which is wait.

Read more: Looking Through the Energy Cost Shock—Stronger Earnings, Lower Tail Risks

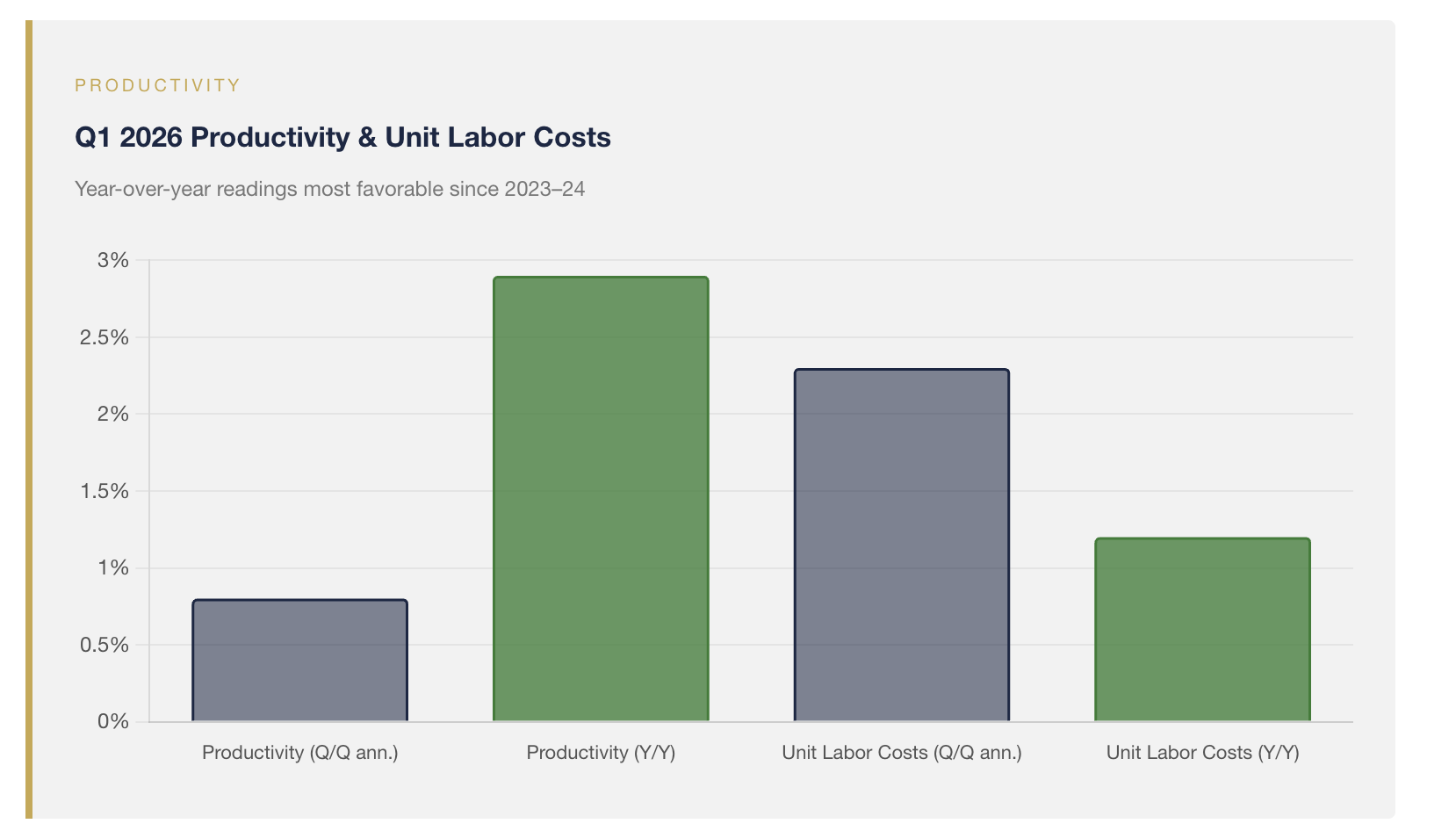

Thursday's preliminary Q1 Productivity and Costs report from the BLS deserves more attention than it received. Nonfarm business productivity rose at a 0.8% annualized rate in the first quarter while unit labor costs rose 2.3%. More instructive were the year-over-year readings: productivity climbed 2.9% over the four quarters ending in Q1 — the strongest annual rate since the third quarter of 2024 — while unit labor costs increased just 1.2%, the slowest annual reading since the third quarter of 2023 and a figure broadly consistent with the Fed's 2% inflation target. Manufacturing productivity registered an even more striking 3.6% quarterly gain with unit labor costs in that sector up 2.4%. We have written for nearly two years that the AI-infrastructure investment cycle is genuinely lifting the productive frontier of the US economy; this report is the cleanest empirical evidence to date that the macro-level numbers are starting to confirm the micro-level capex announcements. We acknowledge it explicitly, and we do not believe the diversification thesis we maintain depends on denying it. But we also note the quieter line in the same release: real hourly compensation fell 0.5% in the quarter, and the labor share of nonfarm business output dropped to 54.1% — the lowest reading in a series that begins in 1947. Productivity gains are accruing to capital, not labor, which is one reason aggregate consumer spending has held up despite cooling hiring, and also one reason the inflation pipeline from tariff pass-through and energy may not encounter the wage-price-spiral resistance that some still expect.

"Productivity gains are accruing to capital, not labor — one reason consumption has held up while hiring has cooled."

For the Federal Reserve, this constellation of data — softer but positive payrolls, moderating unit labor costs, productivity gains — provides material that doves on the Federal Open Market Committee will use to argue for a cut and that hawks will use to argue for patience. We continue to believe patience prevails. The April 30 8–4 hold at 3.50% to 3.75% — the most dissent on a single decision since 1992 — was a snapshot of a committee genuinely divided on the path forward, and Chair-designate Kevin Warsh, whose first FOMC meeting will be the June 16–17 session following Powell's term expiration on May 15, has every institutional incentive to consolidate consensus before moving rates. Markets are now pricing fewer rather than more cuts in 2026 following the week's data, which we believe is the correct read. We expect the policy rate to hold through June, with a single cut still possible later in the year if — and only if — the inflation pipeline from tariffs and energy proves more contained than the cumulative evidence to date suggests.

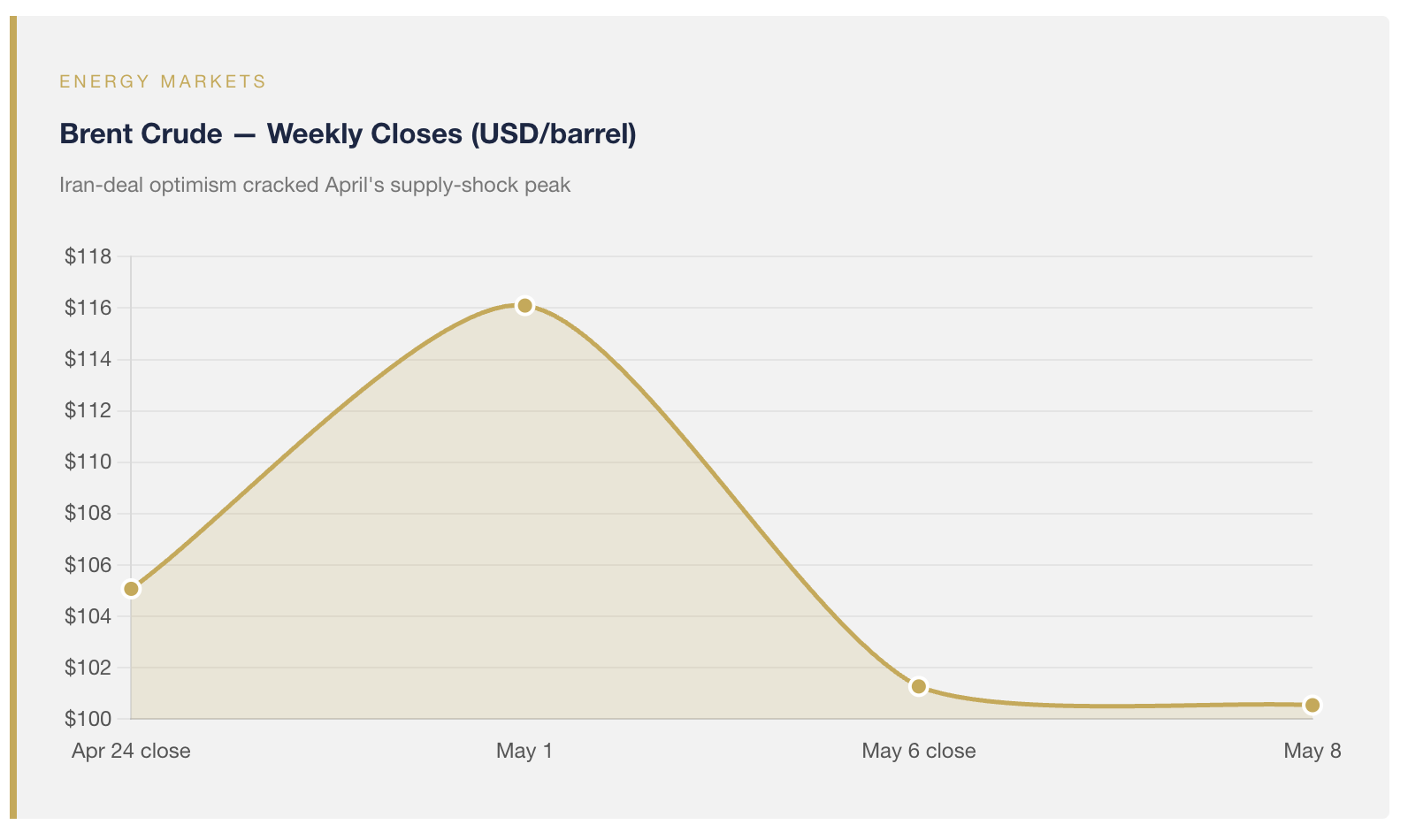

Energy markets delivered the week's most dramatic move. Brent crude fell from above $116 the prior Friday to roughly $100 by Friday May 8, a weekly decline on the order of 13–15%, after President Trump paused the newly launched Project Freedom escort effort in the Strait of Hormuz earlier in the week and US officials confirmed that a fourteen-point memorandum of understanding is under negotiation with Iran. West Texas Intermediate briefly traded as low as $88 mid-week before recovering, and Brent printed an intraday low near $96 on Wednesday before settling around $101 that day. We caution against taking this drop as a durable change in the energy backdrop. The International Energy Agency still characterizes the conflict as disrupting roughly ten million barrels per day of global supply; a fresh exchange of fire in the Strait of Hormuz during the week was a reminder that the ceasefire remains fragile; and OPEC+ shut-ins from earlier in the conflict will not return online overnight even if a final agreement is reached. What is true is that if the deal holds, the disinflationary tailwind into the second half of the year would be meaningful. That is a scenario we want clients prepared for, but not one we want them positioned solely toward.

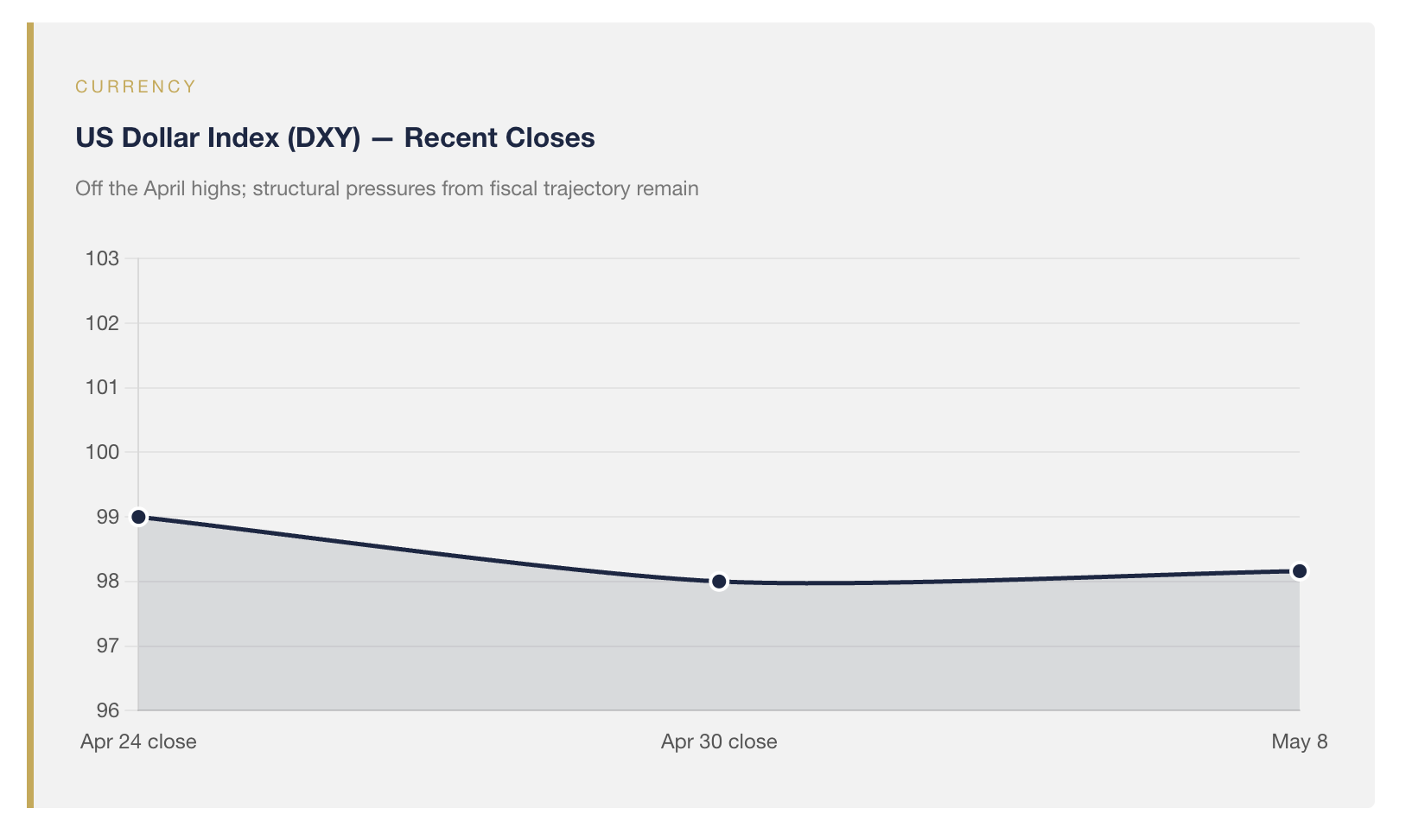

Across the Atlantic, both the Bank of England and the European Central Bank held rates at their April 30 meetings, with their next decisions not due until mid-June — the BoE at 3.75% by an 8–1 vote in which the lone dissent argued for a hike, and the ECB at a 2.0% deposit rate, citing the same supply-and-tariff-shock concerns that have constrained the Fed. Both central banks are now operating in the same macro corridor: inflation pulling from cost-push channels they cannot easily resolve with policy, growth holding near trend, and politically sensitive transitions ahead. This synchrony reinforces a point we have made repeatedly: dollar weakness is not a story about US idiosyncratic failure — it is a story about whether the marginal foreign holder of US Treasury and dollar reserves continues to find the yield premium and credibility worth the concentration risk. The DXY at 98.16, off its April highs, is consistent with that arc.

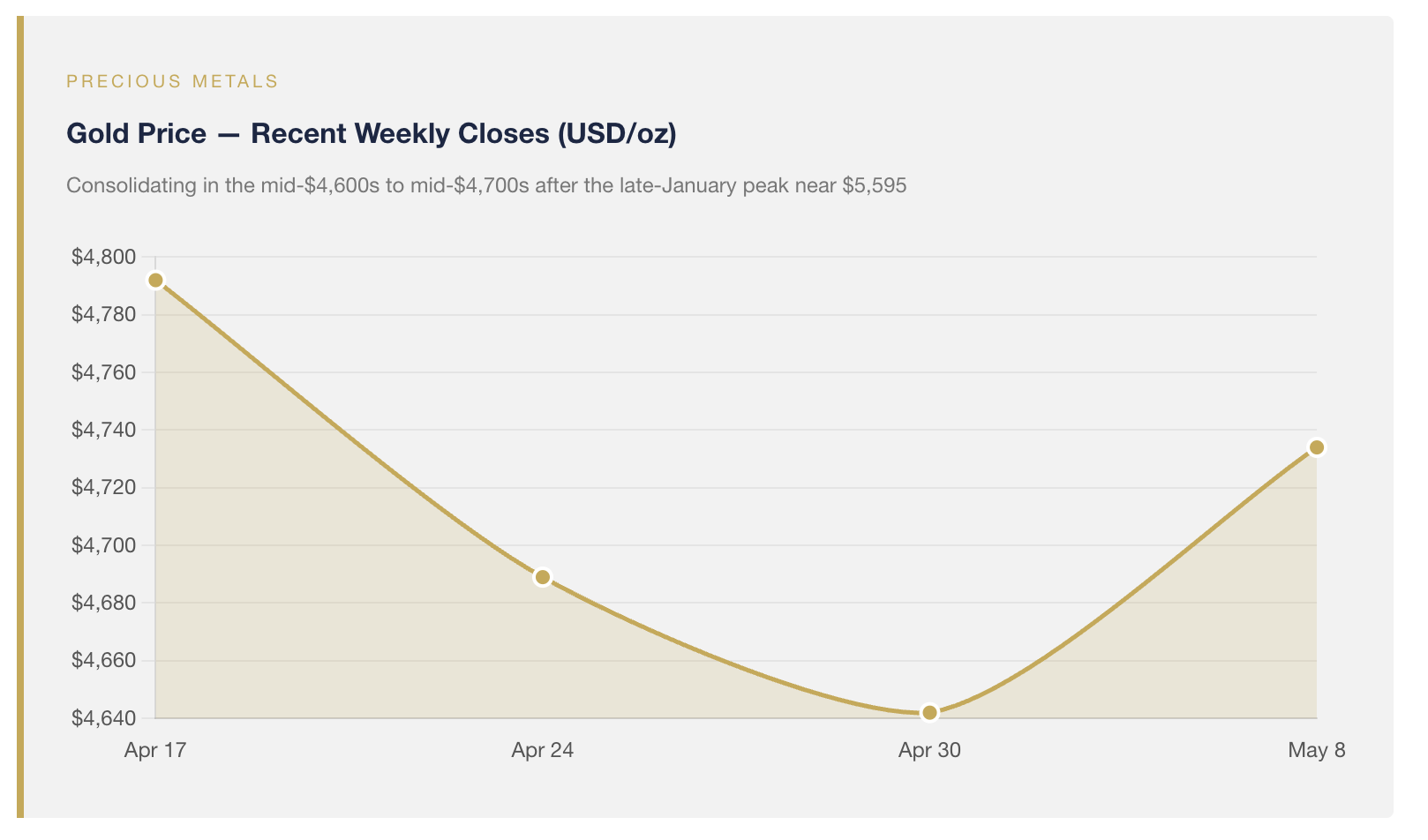

That leaves us where we began the year. The S&P 500 sits in record territory near 7,337 after Thursday's close, gold holds firm near $4,734 per ounce, and our positioning across our Value, Gold, and Emerging Markets strategies remains designed not for any single week's data but for the structural likelihood — not inevitability — that fiscal trajectory, Fed transition under unprecedented political pressure, and progressive de-dollarization by foreign reserve managers continue to reward investors who own assets with return streams that are not tethered to the US policy mix. A 115,000 print on a Friday in May does not retire that view. Nor, in fairness, does it require us to escalate it. The case for diversification, gold, and hard assets is a probability-weighted allocation, not a directional trade — and this was a week in which several of those probabilities moved modestly in different directions, with the structural balance preserved.

This week brings the April CPI release on Tuesday, retail sales on Thursday, and the formal handoff to Chair-designate Warsh on Friday, May 15. We will be writing again at the end of it. In the meantime, if the week's data has prompted you to reconsider how the international and hard-asset portion of your portfolio is built, we would encourage you to reach out to a Euro Pacific Asset Management advisor or visit EuroPac.com to learn more about our Value, Gold, and Emerging Markets strategies. The case for diversification is not a bearish call on America. It is a forward-looking allocation to the world that the week's data, taken together, continues to describe.

investment risk

Please read about the Risks of investing in the Funds. You should carefully consider the Fund’s investment objectives, risk, charges and expenses before investing. Investing involves risk, including potential for loss of principal. The risks of investing in emerging market and foreign securities may be higher than the risks associated with investing other securities. Diversification cannot assure a profit or protect against loss in a down market. Dividends are not guaranteed and may fluctuate. Fund holdings are subject to change and risk. Past performance cannot predict future results.

To obtain a prospectus or summary prospectus that contains this and other information about the Funds, please Click Here or call 1-866-878-2881. Please read the prospectus carefully before investing. Euro Pacific Asset Management Funds are distributed by Distribution Services, LLC (Euro Pacific Asset Management is not affiliated with Distribution Services, LLC).

Disclosure: Any tax or legal information provided is merely a summary of our understanding and interpretation of some of the current income tax regulations and it is not exhaustive. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation. Neither the Funds nor any of its representatives may give legal or tax advice.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Euro Pacific Capital

Read more commentaries by Euro Pacific Capital