Key Takeaways

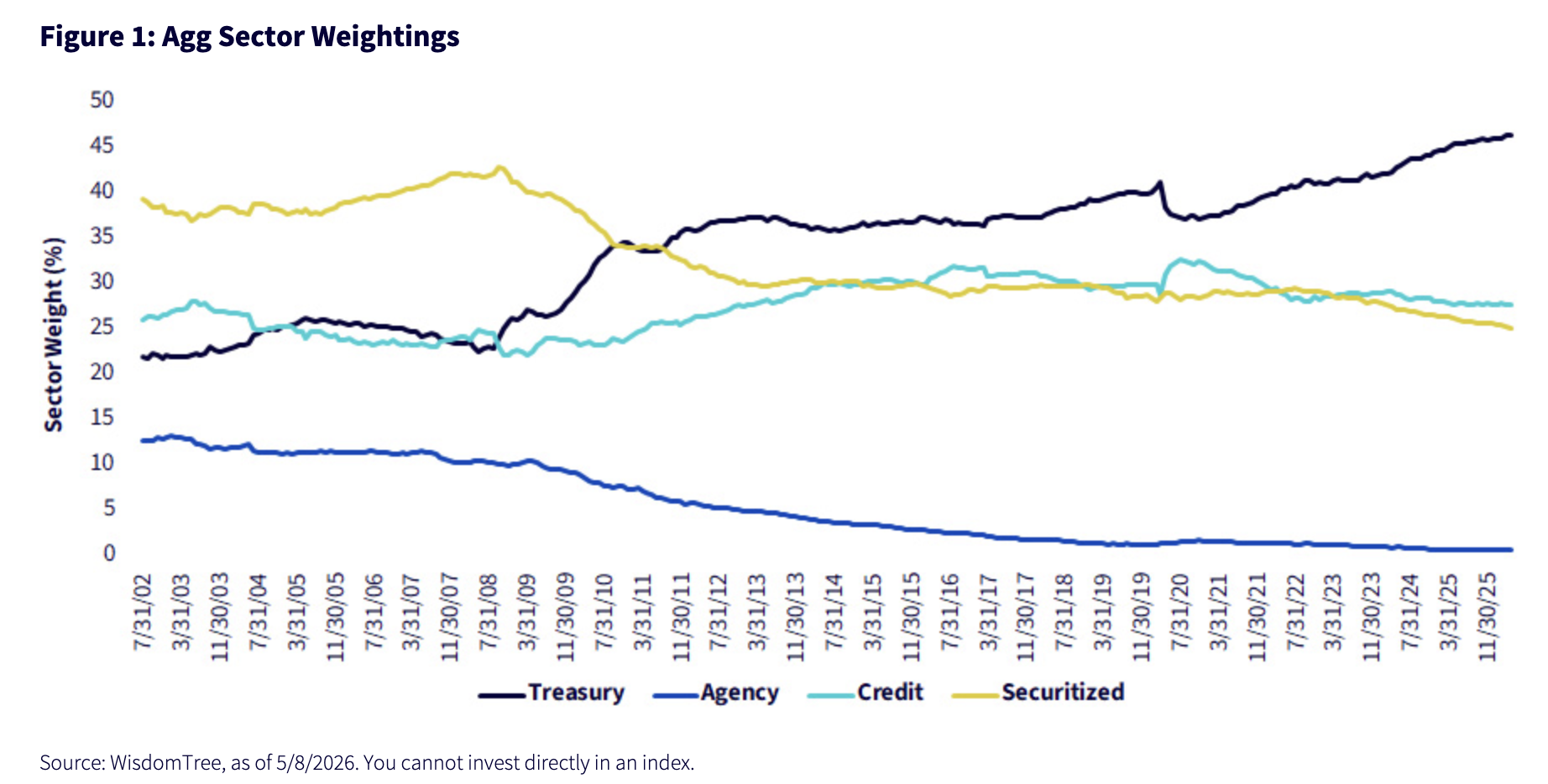

- With Treasury securities now comprising roughly 47% of the Bloomberg U.S. Aggregate Bond Index ("the Agg")—up from 22% in 2002—core bond investors may be taking on too much concentration in U.S. government debt than they realize.

- Persistent fiscal deficits nearing $2 trillion and potential increases in Treasury coupon issuance in FY2027 could push the Agg’s Treasury weighting above 50%, further reshaping the risk and yield profile of traditional core fixed income allocations.

- Investors seeking a more balanced core bond exposure may consider the WisdomTree Yield Enhanced U.S. Aggregate Bond Fund (AGGY), which uses a rules-based approach to reduce Treasury concentration while maintaining familiar investment-grade risk characteristics and enhancing yield potential.

Typically, an investor’s traditional bond portfolio begins with a cornerstone, or core holding of some sort. From either a strategic or tactical perspective, a core fixed income position provides the investor with some ballast to help anchor any other strategies that may be included. However, the term ‘core’ gets thrown around a lot, and when you look ‘under the hood’, you may be surprised with what you discover on how this position could actually be allocated.

For many fixed income investors, their bond portfolio utilizes the Agg as their core holding. The Agg has been utilized as the benchmark for the U.S. bond market for 40 years and is a market-cap based index. In other words, in the market cap-based approach, the more debt an entity has outstanding, the higher relative weighting it receives in the index.

With the U.S. budget deficit standing at close to $1.8 trillion and projected to increase to just under $2.0 trillion for fiscal year 2026, the amount of Treasury marketable public debt outstanding has, and more importantly, will continue to rise if the deficit does not reverse course in coming years. As a result, the Treasury weighting in the Agg has continued to move higher and higher and currently stands at about 47%. Translation: almost one-half of the Agg consists of Treasuries.

Let’s compare that to the weightings for the Agg over the last twenty to twenty-five years. The enclosed graph underscores how the four major sectors have evolved over this timeframe. As I highlighted earlier, the Treasury weighting has surged to roughly 47% from 22% in 2002. On the other side of the ledger, the weighting for Federal Agency securities has declined from roughly 13% down to its current reading of below 1%. Securitized credit was the top weighting back in 2002 at just under 40% but has now dropped down to 25%. Rounding out the slate, investment grade corporates have remained relatively steady, straddling the 25% threshold.

With budget deficits expected to remain elevated, outstanding Treasury supply will also remain high and could very well increase. Thus, the Agg’s weighting for Treasuries could arguably pierce the 50% mark looking ahead. In fact, while Treasury recently signaled no changes/increases to coupon auction sizes “for at least the next several quarters”, the minutes for the Treasury Borrowing Advisory Committee (TBAC) did reveal “that increases in coupon issuance could be warranted in FY2027 and discussed potential changes to the forward guidance for Treasury to consider.”

Read more: A Resilient Labor Market Delays Fed Cuts

Potential Solution

So, how can a bond investor invest in core fixed income without such an overweight to Treasuries? The answer: the WisdomTree Yield Enhanced U.S. Aggregate Bond Fund (AGGY). AGGY is designed to amend the counter intuitive nature of market cap-based strategies, by applying a rules-based approach that reweights the subcomponents of the Agg, while broadly maintaining familiar risk characteristics. As a result, this investment grade solution seeks to enhance yield while achieving the goal of anchoring one’s bond portfolio with a core holding.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner, or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. Investing in mortgage- and asset-backed securities involves interest rate, credit, valuation, extension and liquidity risks and the risk that payments on the underlying assets are delayed, prepaid, subordinated or defaulted on. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit. The Fund does not attempt to outperform its Index. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Kevin Flanagan, Head of Investment and Fixed Income Strategy

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Alejandro Saltiel, Andrew Okrongly, Behnood Noei, Bradley Krom, Brendan Loftus, Brian Manby, Christopher Gannatti, David Graichen, Hyun Ku Kang, Jeff Weniger, Jeremy Schwartz, Jonathan Steinberg, Joseph Grogan, Joseph Tenaglia, Kara Dombroski, Kevin Flanagan, Lauren Pfendt, Liqian Ren, Lonnie Jacobs, Matt Wagner, Rick Harper, Ryan Krystopowicz, and Vanya Sharma are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© WisdomTree, Inc.

Read more commentaries by WisdomTree, Inc.