Roth Conversion Strategy for High Earners: When It Makes Sense and When It Does Not

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- It’s about tax timing, not tax avoidance: A Roth conversion is a deliberate choice to pay tax today in exchange for potential tax-free growth later, and the strategy only works when the rate you pay now is likely lower than the rate you would pay in the future.

- The window matters more than the intent: The most attractive conversion opportunities appear during temporary income drops, such as early retirement before Social Security and RMDs begin, or the years after a business sale when earned income disappears.

- Model the full picture: For high earners, the Roth conversion decision intersects with RMD projections, Medicare surcharges, state income taxes, estate planning, charitable goals, and heir-level tax exposure. Modeling only the current-year tax return is the most common way this strategy goes wrong.

Most high earners approach Roth conversion strategy with the wrong question.

The instinct is to ask “Should I convert?” The better question is: what tax rate am I paying today, and what am I trying to avoid later? A Roth conversion is a deliberate choice to recognize ordinary income now in exchange for potential tax-free growth and withdrawals later. The strategy can be powerful. It can also be expensive.

Peak earning income tends to stack. Wages, RSUs, K-1 income, bonus compensation, deferred comp, and business distributions can collide in the same year. Add a large conversion and the result is a transfer taxed at the highest marginal federal rate, plus state income tax, plus potential Medicare surcharges. That is acceleration, not planning.

This does not mean high earners should avoid Roth conversions. It means the decision has to be modeled, not assumed. Plus with tax law uncertainty still shaping planning conversations, that modeling matters more than ever.

Below, we cover what a Roth conversion actually is, how it works differently for high earners, when the strategy makes sense (and when it does not), and how to think about the decision across your full financial picture rather than just the current year’s tax return.

Read more: New Highs, $100 Oil, and the AI Bet That’s Splitting Tech in Two

What Is a Roth Conversion?

A Roth conversion moves money from a pre-tax retirement account into a Roth IRA. The converted amount is included in ordinary income for that year, reported on Form 8606, and taxed accordingly. The account then has the potential to grow and be withdrawn free of income tax on qualified distributions.

This is different from a Roth IRA contribution, and the distinction matters for high earners. Direct Roth contributions are income-limited. Roth conversions operate under separate rules. A high-income executive who cannot contribute to a Roth IRA may still be eligible to convert traditional IRA assets. The contribution door can be closed while the conversion door stays open.

How this plays out in practice depends on how each client’s full tax picture is structured.

Why Roth Conversions Are More Complex for High Earners

The higher the current tax bracket, the higher the hurdle rate for a conversion to produce a better outcome than deferring. For a moderate-income retiree, the decision can be clean: income is low today, future RMDs will be large, converting now captures available bracket space. For a high-earning executive or business owner, the same logic rarely applies cleanly. The real question is not whether Roth accounts are attractive. They usually are. The question is: at what tax cost am I buying this account, and is that cost worth it given what I expect to pay later?

For high earners, that cost is shaped by several compounding factors that a simple bracket comparison will miss:

- Peak earning years create high hurdle rates: Converting during high-income years means the conversion itself may be taxed at the top federal rates, which means the future tax savings need to be correspondingly large to justify the current cost.

- Multiple income sources crowd out bracket space: RSUs, K-1s, bonuses, deferred comp, and business income can all land in the same year, leaving little room for an efficient conversion before hitting an unattractive bracket.

- State tax changes the math: A 5% to 13% state income tax layered on top of a federal conversion dramatically changes the hurdle rate in ways that federal-only modeling misses entirely.

- Medicare IRMAA adds a hidden layer: For retirees, conversion income increases modified adjusted gross income, which can push Medicare Part B and Part D premiums into higher tiers. CMS updates IRMAA thresholds annually, and the surcharges can be meaningful enough to change whether a conversion clears the bar.

Understanding these factors is what makes Roth conversion planning fundamentally different for high earners than it is for everyone else, and shapes when the strategy makes sense.

When a Roth Conversion Strategy Makes Sense

The answer depends heavily on where you are in your income cycle. Certain situations create genuinely attractive conversion windows, and the most important skill in this planning is recognizing them when they appear.

During Low-Income Windows

The most attractive conversion opportunities appear when income temporarily drops. Early retirement before Social Security and RMDs begin is the classic window. Sabbaticals, business transition years, the gap after a company sale, years with unusually low K-1 or bonus income. These are all potential openings.

Business owners frequently ask whether the year they sell is the right time to convert. Usually, it is not. The sale year tends to be overloaded with gain recognition, deal expenses, and deferred compensation payouts. The better opportunity is typically in the years that follow, once business income disappears and the overall tax picture normalizes. This is a theme we explore in depth in our business exit tax planning for founders.

The key is bracket management: how much income can be added before the next dollar becomes inefficient? A married couple with $140,000 of taxable income who can add $80,000 more before hitting a major bracket threshold may have an efficient conversion window. Converting $500,000 in that same year almost certainly does not. Getting this right requires knowing the full income picture for that year, not just the IRA balance.

Low-income windows are the most opportunistic entry point, but they are not the only one.

Roth Conversion Before RMDs Begin

A second powerful window opens in the years between retirement and age 73, when required minimum distributions have not yet begun. Traditional IRAs, SEP IRAs, and most qualified plan accounts require minimum distributions starting at age 73. For affluent households that do not need those distributions for living expenses, the problem is that RMDs create forced taxable income whether they need it or not, stacking up in years they would rather keep clean.

There is an additional wrinkle that often goes unaddressed: the surviving spouse problem. When one spouse dies, the survivor files as single. The IRA does not shrink. RMDs continue. But the brackets compress significantly. A systematic conversion program during the couple’s early retirement years can reduce future RMD exposure and improve the surviving spouse’s tax position considerably, as illustrated in our case study on tax-optimized retirement planning for a surviving spouse.

Roth Conversion and Estate Planning for High Net Worth Families

A third situation worth modeling carefully is when the family does not expect to spend down the IRA in their lifetimes. At that point, a Roth conversion stops being purely a retirement decision and becomes an estate planning one. And that’s because the question is no longer what tax you pay in retirement, but what tax your heirs pay when they inherit.

Pre-tax IRA assets can be a difficult inheritance. Most non-spouse beneficiaries must empty inherited accounts within 10 years under post-SECURE Act rules. If those heirs are high earners, drawing down a large inherited traditional IRA during their own peak income years can mean paying tax at rates that rival what the original owner would have owed. The family effectively ends up paying full freight twice: once in the estate, again in the heirs’ income tax returns.

Three factors make this especially consequential for high-net-worth families:

- Heir tax exposure: Inheriting a large traditional IRA during peak earning years creates a compressed 10-year distribution window that stacks ordinary income at the worst possible time.

- Estate reduction through tax payment: Paying the conversion tax from outside taxable assets reduces the taxable estate directly while moving future growth into a Roth structure.

- Beneficiary coordination is non-negotiable: Roth conversions should be coordinated with trust language, beneficiary designations, and estate documents. Treating the conversion as an isolated account decision while the estate plan is handled separately is one of the most common ways this strategy fails. Our guide on estate tax planning for business owners covers how these pieces connect in practice.

When a Roth Conversion is the Wrong Move

Not every situation calls for a conversion, and for high earners the wrong timing can mean accelerating a significant tax bill with nothing to show for it. The clearest signal to wait is when the current tax cost is too high to justify the future benefit, but cost is not the only reason to hold off. There are four distinct circumstances where a conversion is likely the wrong move.

- Peak income stacking: If wages, bonuses, RSUs, K-1 income, and business distributions already fill the top brackets, a conversion accelerates tax at the worst possible rate. In most of those years, the answer is to wait.

- Liquidity is the constraint: Conversions work best when the tax is paid from outside assets. Withholding taxes from the IRA reduces the amount entering the Roth and limits the compounding benefit. If wealth is concentrated in a business, real estate, or appreciated stock, the conversion may be impractical regardless of how attractive the model looks.

- Charitable giving is the more efficient path: For families with meaningful charitable intent, pre-tax IRA assets often belong to charity rather than to the conversion schedule. Charities generally do not pay income tax on inherited IRA assets. If a significant portion of the traditional IRA is heading toward a donor-advised fund or charitable bequest, converting it first is solving a problem that does not exist. For a deeper look at how these structures compare, see our overview of charitable remainder trusts vs. charitable lead trusts.

- Retirement income will be materially lower: A corporate executive in the final years of peak W-2 earnings may be in a much higher bracket today than they will be in retirement. Converting now at the top rate to avoid a lower future rate is the opposite of the intended strategy.

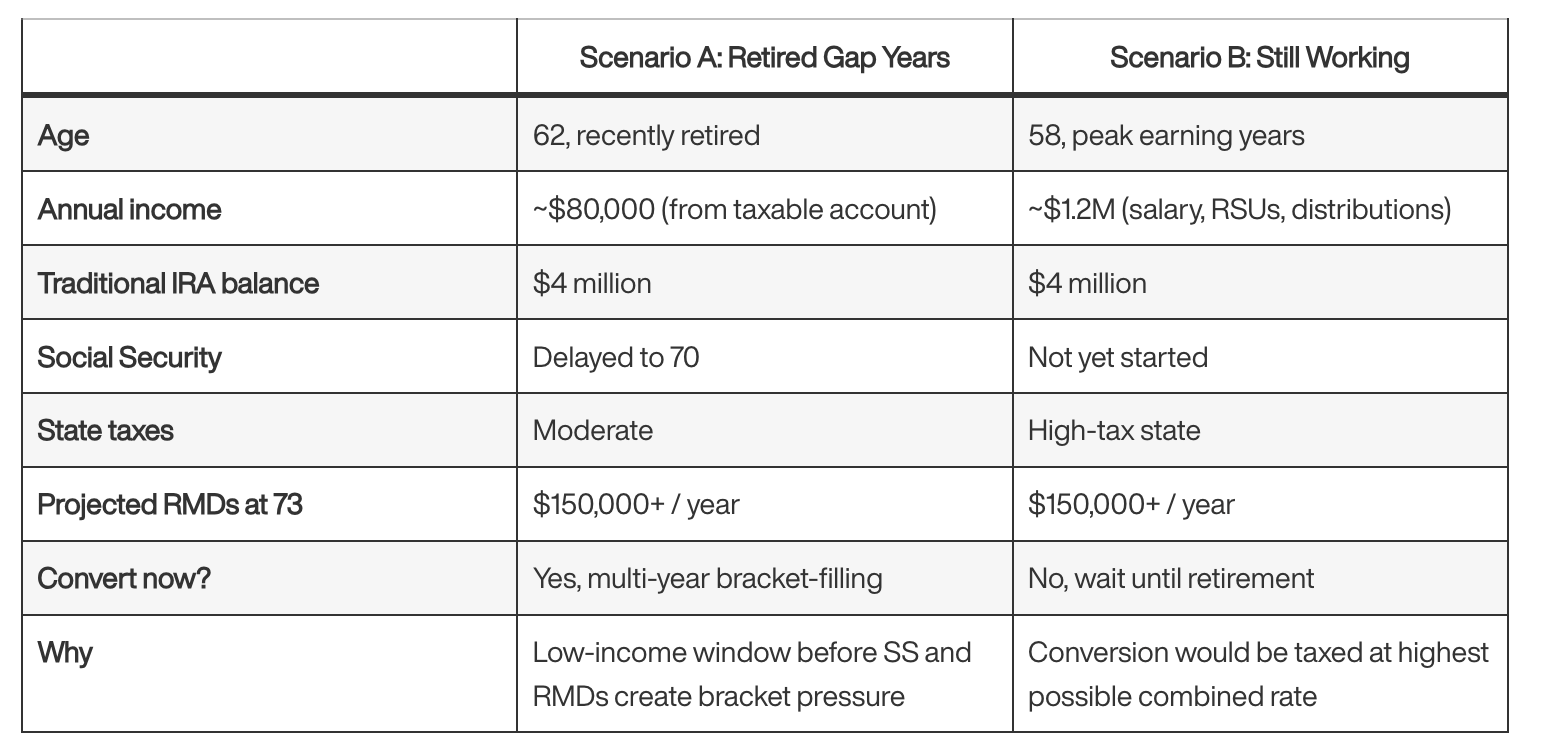

A Real-World Roth Conversion Example

Consider two versions of the same couple to illustrate why timing changes everything.

In Scenario A, the couple has a clean multi-year window to convert systematically, filling available bracket space each year while monitoring IRMAA thresholds and portfolio liquidity. In Scenario B, doing the same conversion today simply accelerates tax at the worst possible rate. Waiting two or three years for retirement produces the same Roth assets at meaningfully lower cost.

Same strategy. Different timing. Very different answer. For a real-world look at how integrated tax planning changes outcomes at scale, see our case study on developing a $20 million tax-optimized investment strategy and estate plan.

Roth Conversion Decision Framework for High Earners

None of what we have covered above leads to a universal answer. That is the whole point. Whether a conversion makes sense in any given year comes down to several variables that interact with each other — and need to be modeled together, not evaluated one at a time. Here is how we frame the decision in practice.

- Convert more when: current income is temporarily low, future RMDs will force excess taxable income, heirs are likely to be high earners, estate planning is a priority, and outside liquidity exists to pay the tax.

- Convert less or wait when: current income is at or near peak levels, liquidity is limited, Medicare surcharges are a concern, charitable planning is more efficient, or retirement income will be materially lower.

- Revisit annually: Income changes. Markets move. State residency changes. Family goals shift. A conversion that made no sense last year may be right this year, and a strategy that looked attractive in January may look inefficient by December after a large bonus or capital event.

The goal is not to convert the largest amount possible. The goal is to convert the right amount, in the right year, at the right tax cost. That is what integrated wealth management and advisory looks like in practice.

FAQ: Roth Conversion Strategy for High Earners

Can high earners do Roth conversions if they cannot contribute directly to a Roth IRA?

Yes. Roth IRA contribution eligibility is income-based and applies only to new contributions. Roth conversions operate under separate rules. A high-income taxpayer who is phased out of direct contributions may still be able to convert traditional IRA assets. The two rules are distinct and should not be conflated.

Does a Roth conversion make sense if I am already in the top federal tax bracket?

Sometimes, but the hurdle rate is significantly higher. A conversion at the top bracket needs a compelling reason: future RMD pressure, estate planning objectives, surviving-spouse bracket compression, or heir-level tax exposure. In most peak-income years, waiting for a lower-income window produces a better outcome.

Should I do a Roth conversion before RMDs begin?

For many affluent retirees, the years between retirement and age 73 represent the strongest Roth conversion window available. If projected RMDs would force substantial taxable income you do not need, converting during the gap years at lower rates can reduce future tax burden and improve the surviving spouse’s long-term flexibility.

Do Roth conversions affect Medicare premiums?

Yes, for retirees. Conversion income increases modified adjusted gross income, which determines Medicare IRMAA calculations. Crossing a threshold can significantly increase Part B and Part D premiums. IRMAA also uses income from two years prior, so a large conversion today may affect premiums two years forward.

Is a Roth conversion effective for estate planning?

It can be, particularly when heirs are likely to be high earners and IRA assets are not needed for lifetime spending. Roth assets may reduce income tax exposure for beneficiaries who would otherwise inherit a large pre-tax account and face a compressed 10-year distribution window during their own peak earning years.

What is the biggest Roth conversion mistake high earners make?

Converting at the wrong tax rate, typically during peak income years. The second most common mistake is treating the conversion as a single-year decision rather than a multi-year bracket management strategy. Conversions work best when executed systematically, coordinated with RMD projections, estate planning, charitable intent, and available liquidity.

Jonathan Dane, CFA, CFP®

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All