Key takeaways

- The extended closure of the Strait of Hormuz is pushing global oil inventories toward critical lows, where the market’s “balancing mechanism” could quickly give way to operational stress.

- Markets may be looking through the crisis because excess inventories, strategic petroleum reserve releases, sanctioned barrels and China’s strategic reserves could extend the runway before shortages become severe, but they do not eliminate the risk of a bullwhip effect.

- We are raising our energy overweight and modestly reducing our materials exposure, seeking to use energy stocks as a relatively inexpensive asset that may serve as a hedge against a surge in oil prices and the reality of a tighter energy market.

Energy shock absorbers under strain

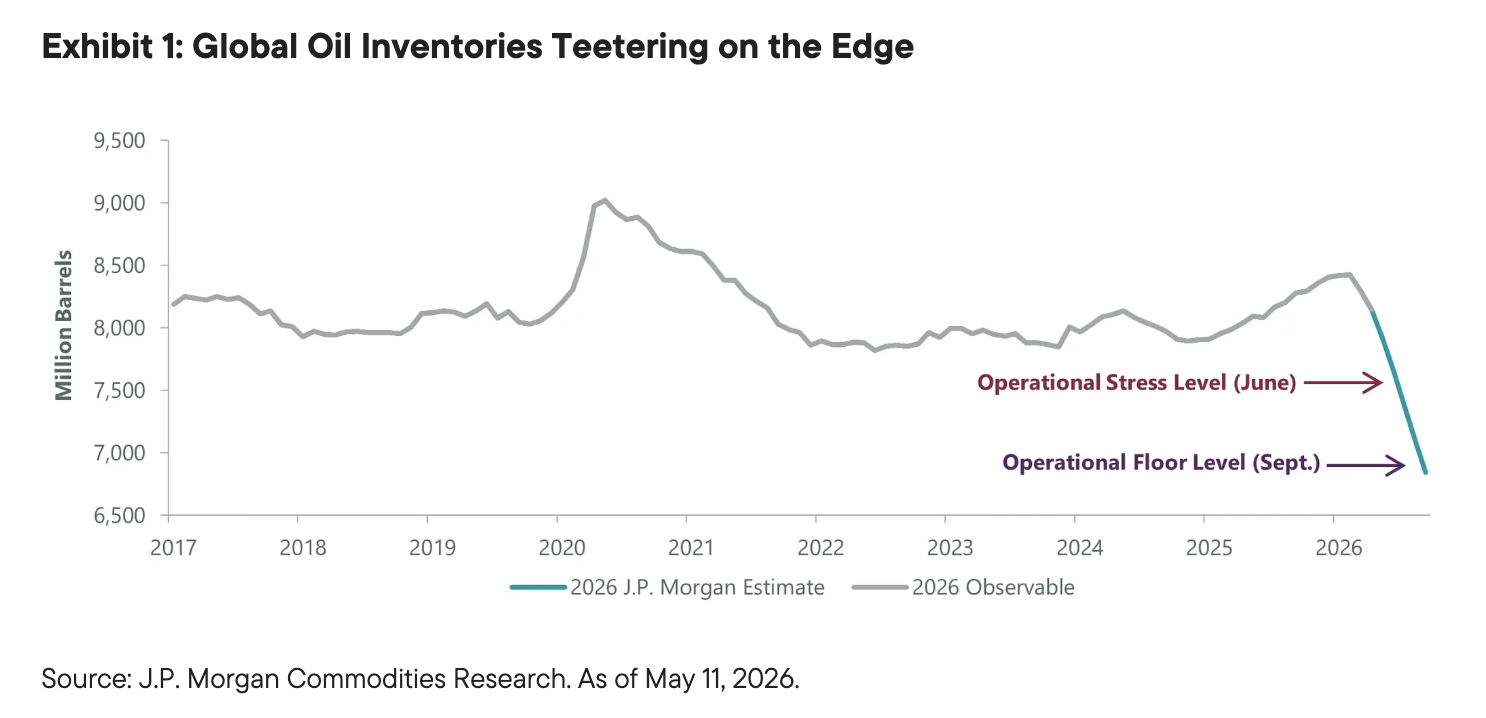

The extended closure of the Strait of Hormuz has created one of those rare moments in markets when something both knowable and important appears to be underappreciated. In this case, we know with a greater degree of certainty that the ongoing energy crisis is pushing global oil inventories, including many critical product inventories, toward all-time lows—levels that could result in outright stock-outs of critical products like jet fuel in certain markets (Exhibit 1). This is one of the largest supply disruptions we have experienced, and the problem is that it is ongoing. Current estimates are that if the Strait opened today, cumulative unproduced barrels would approach one billion. If this continues until June 1, that estimate jumps to 1.4 billion barrels.

So far, this has been an historic, but still largely linear, time-driven process in which the initial shock has been absorbed by excess oil inventories and strategic petroleum reserve (SPR) releases. The problem is that we are approaching the point where record inventory draws rapidly erode these crisis shock absorbers, creating the conditions for stress to spread quickly across the global energy supply chain. It is practically impossible to model the price per barrel required to force demand destruction, especially in markets that simply run out of product, but we can be quite certain the right price will not be US$100 per barrel—it will likely be significantly higher.

Read more: Most Families Don’t Know the Full Power of 529 Plans

This is not an obscure conclusion; energy experts and analysts see the same intensification ahead1. The core issue is that the “balancing mechanism” of inventories will soon be lost as global oil markets begin to reach the hard floors required to keep the energy supply chain functioning. Like a biological circulatory system that can bleed out, the system can quickly move from manageable stress to operational strain once those buffers are gone.

So why is the market largely looking past this crisis? Beyond those initial shock absorbers, sanctioned cheap barrels, primarily Russian and Iranian, likely boosted oil consumption in key consuming markets like China and India, suggesting there may be more discretionary demand cushion than traditional models assume. China has also spent recent years adding massive amounts of strategic oil storage capacity, which it filled with cheaper sanctioned barrels. If those barrels are released, particularly into targeted Asian markets where shortages could become most acute, it could extend the runway while giving China tremendous strategic leverage.

Another way the market appears to be looking through this crisis is in recession odds, which remain relatively sanguine. We closely monitor these signals and think the current consensus could prove too complacent if the energy crisis intensifies as expected. The risk is that economic stress does not grow in a smooth, linear fashion. As supply chains tighten, product shortages emerge and oil prices rise to force demand destruction, the macro drag could compound quickly, adding another layer of uncertainty to an already fragile energy backdrop.

Ultimately, we do not think markets are fully prepared for the potential bullwhip effects of plummeting oil inventories. One of the cyclical models we are using, due to the magnitude of the inventory shifts, is the DRAM (dynamic random-access memory) inventory cycle, which is prone to extreme booms and busts when inventory buffers disappear, supply cannot respond quickly, and customers begin to pull demand forward. That dynamic has become especially visible recently as AI-driven demand for high-bandwidth memory has tightened supply across the broader memory market, pushing prices higher and reinforcing the power of the inventory cycle. A similar inventory-driven reflexivity could emerge in energy if consumers, refiners or countries begin acting not on the reality of today’s supply availability, but on the fear of tomorrow’s scarcity.

Positioning for reality

The critical portfolio construction question is: How do we position for a risk that appears increasingly knowable, but not yet fully reflected in markets? With equity markets near all-time highs and index valuations historically elevated, we are adjusting our positioning pre-emptively rather than waiting for the energy shock to be fully reflected in prices by raising our energy overweight through the addition of new oil and natural gas companies, as well as increasing our existing positions in diversified oil majors. The most direct reason is that energy is the clearest expression of the risk we see building. If global inventories are approaching hard floors and product stock-outs become more likely, then energy companies should experience materially positive estimate revisions and generate much higher cash flows.

The second reason is that using energy stocks to hedge against a surge in oil prices is still relatively inexpensive. Energy stocks have some of the highest free-cash-flow yields in the market, fortress balance sheets and healthy dividends. Even if this crisis ended today, oil prices would likely remain materially higher than before the crisis, as global inventories will need to be rebuilt over the next couple of years, and rebooting the global energy supply chain will take time.

The third reason is portfolio construction. When energy prices spike, historically, pretty much every other market sector goes down. We saw this negative correlation pattern early in the crisis, and we think the risk is growing that it will reassert itself as oil inventories start to plummet. In an energy-induced volatility spike, we think energy will likely be one of the few truly defensive sectors.

We are funding part of this energy increase by modestly reducing materials exposure. This is not a rejection of the long-term bull market in real assets, which we still think remains intact as the energy crisis creates more ongoing inflationary risks. Rather, it is a near-term portfolio construction decision. Materials stocks, including gold, have recently been among the most negatively correlated areas versus energy, with gold behaving more like a risk-on asset. If the central issue is the risk of hard inventory floors and stock-outs across the global energy supply chain, then energy is the more direct expression of that risk.

We invest in a world where we are constantly dimensioning the probabilistic landscape, pushing that process until we reach the border of irreducible uncertainty. It is extremely rare to know something about the future to a degree that takes us in the opposite direction, toward certainty; however, this is one of those rare times. The unknowable part is how quickly markets will reprice the reality of scarcity if oil inventories continue to plummet. We hope this crisis de-escalates quickly and we are proven wrong. But hope is not a strategy, and we are positioning accordingly.

Endnote

1. Source: "Short-Term Energy Outlook." U.S. Energy Information Administration. May 12, 2026.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal. No assurance can be given that any forecast, projection or prediction regarding economies or financial markets will be realized.

Active management does not ensure gains or protect against market declines.

Commodity-related investments are subject to additional risks such as commodity index volatility, investor speculation, interest rates, weather, tax and regulatory developments.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

The government’s participation in the economy is still high and, therefore, investments in China will be subject to larger regulatory risk levels compared to many other countries.

WF: 10423963

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© ClearBridge Investments

Read more commentaries by ClearBridge Investments