Rethinking US Equity Exposure Through Sectors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsUS equities continue to march higher in 2026 despite geopolitical uncertainties, supported by resilient economic data and strong corporate earnings. Much of the market narrative remains focused on mega-cap technology and artificial intelligence (AI). Yet increasingly uneven performance across sectors suggests that the opportunity set is wider, and more complex, than the headline index return may imply.

Looking beyond broad market exposure, investors are increasingly attracted to sector strategies as a complement to their core US equity allocations or to better align portfolios with the macroeconomic forces shaping returns.

US labor market data recently exceeded expectations, while unemployment held steady, reinforcing a risk-on tone. That, in turn, has helped drive one of the S&P 500 Index’s strongest monthly gains in recent years.

Read more: Meatloaf and the Evolution of ETF Thinking

Some uncertainty may reflect a familiar disconnect, however, between headlines and fundamentals, Main Street and Wall Street. US consumer confidence recently hit record lows even as spending remains somewhat resilient and markets have climbed. This gap highlights a key dynamic in today’s environment—one where differences beneath the surface are playing a larger role in shaping outcomes.

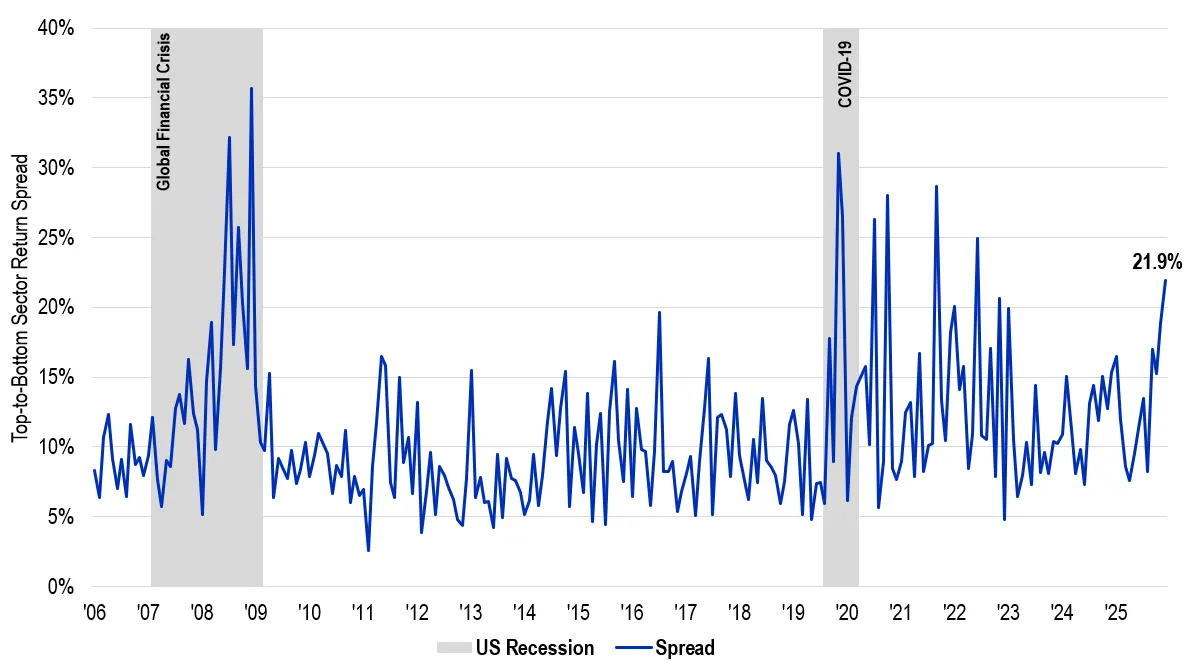

A market defined by dispersion, not direction

Rather than moving in lockstep, sectors have recently diverged in response to economic forces. In fact, sector dispersion—the spread between the best- and worst-performing sectors—has widened meaningfully in recent years and remains elevated.

The widening reflects the uneven impact of higher interest rates, shifting consumption patterns and rapid technological change, and highlights how much sector positioning can influence outcomes.

S&P 500 Sector Return Spread

May 2006 to April 2026

Over the past year, the communication services and information technology sectors have delivered returns in the mid-20% range, while financials have been mostly flat. Over a three-year horizon, communication services returned roughly 35%, compared to about 14% for financials. Even over five years, the spread remains notable, with technology delivering close to 20% annualized returns versus high single digits for more cyclical areas.1

This growing divergence suggests that equity investors may want to take a more tactical approach. As dispersion rises, the difference between sector exposures can be more impactful.

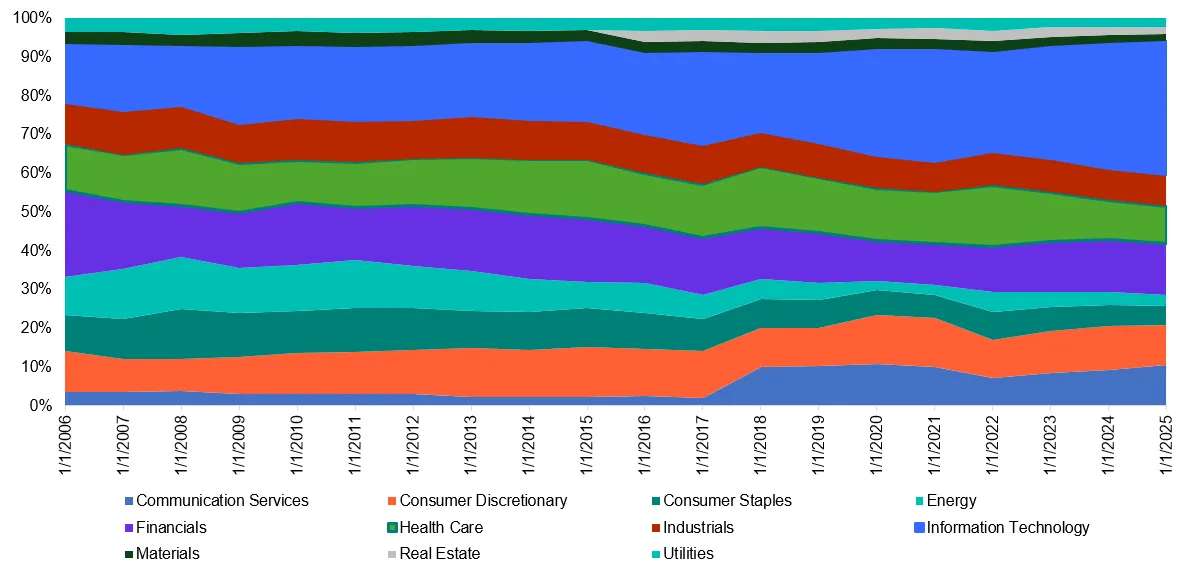

The US market has structurally changed

Another important consideration is how much the US equity market itself has evolved. Two decades ago, sectors such as financials and energy played a much larger role in driving index returns. Today, information technology and communication services dominate, reflecting the rise of digital platforms, software-driven business models and asset-light growth companies.

GICS Sector Allocations: 2006 to 2025

Sector allocations within S&P 500 index have changed significantly in the past 20 years

Market weights are not the only thing shifting. We have also increasingly seen earnings growth resulting from certain digital transformations. This has particularly been the case with business models that benefit from scale—where larger platforms can serve more users at lower cost, and where growing user bases reinforce their competitive advantage. Communication services are a clear example. Today, nearly 70% of the global population uses social media, and close to 90% of adults are connected in some form. Digital advertising has become the primary channel for reaching consumers, while streaming, gaming and the broader creator economy are still rapidly expanding. Rather than viewing these as short-term trends, we believe they reflect deeper shifts that are shaping where growth and market leadership come from.

Macro forces are playing out at the sector level

In this environment, sectors can be considered a transmission mechanism for macroeconomic forces. Higher interest rates, for example, have supported bank profitability through stronger margins, but have also weighed on loan growth and valuations. Meanwhile, innovation cycles, particularly around AI, have continued to support technology and communication services. On the consumer side, spending patterns have become more selective, with US households cutting back in some discretionary categories while continuing to prioritize experiences such as travel, entertainment and live events. Recent surveys suggest Americans are seeking value rather than simply reducing spending, opting for shorter trips, discount retailers or fewer non-essential purchases to preserve spending on experiences and convenience. At the same time, online retail continues to gain share, accounting for roughly 17% of total US retail sales late last year, up meaningfully from pre-pandemic levels.2

These crosscurrents mean that different sectors can perform very differently, even within the same overall market. For investors, this raises an important question: How should portfolios adapt?

Broad US equity exposure remains a core building block for many portfolios. However, given the growing importance of sector-level dynamics, investors are increasingly looking to complement that core with more targeted exposures. Sector strategies can offer a more precise way to express views—whether leaning into structural growth, adjusting rate sensitivity or balancing cyclical and defensive exposures. For investors already holding broad US equity exposure, sector strategies may be used not only to increase exposure to specific structural themes but also to offset areas where the broad index may already be heavily concentrated.

Importantly, this is not about short-term timing. Instead, it reflects a shift from simply “owning the market” to more intentionally accessing the drivers of the market.

The dynamics we see today suggest a one-size-fits-all approach to US equities may be less effective, with opportunity lying in looking beyond the index and using sector-level exposures to complement core allocations and better align portfolios with the forces shaping returns.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnotes

1Source: Bloomberg. Net performance of S&P 500 Capped 35/20 Indices in US dollars as of February 27, 2026. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future results.

2Source: KPMG Consumer Pulse: Memories Over Materials – Americans Slash Non-Essential Spend to Fund Summer Experiences. Kpmg.com. April 23, 2026.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

ETFs trade like stocks, fluctuate in market value and may trade at prices above or below their net asset value. Brokerage commissions and ETF expenses will reduce returns. ETFs may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All