Dispersion Revisited

Membership required

Membership is now required to use this feature. To learn more:

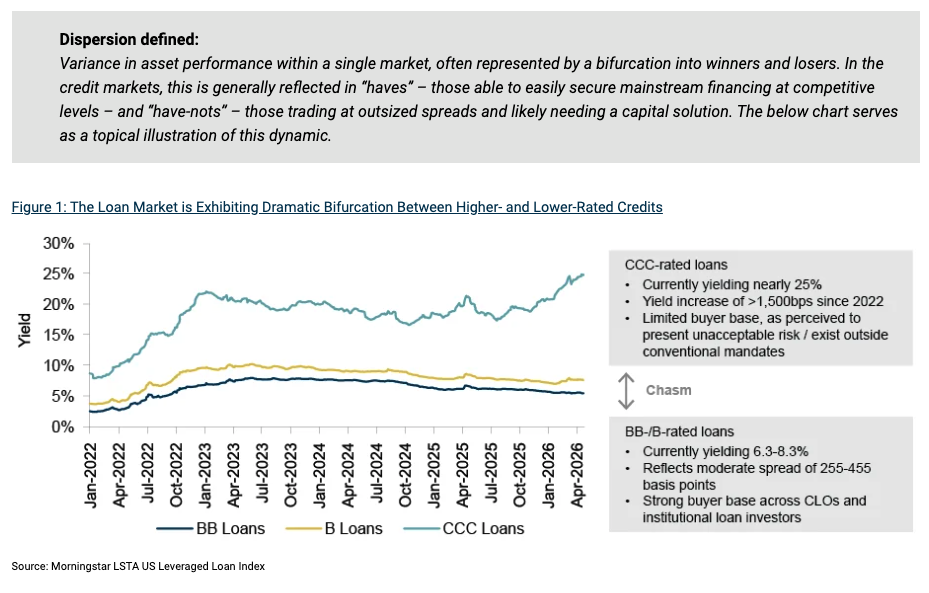

View Membership BenefitsAlthough a lot has changed since our last quarterly, its central theme – dispersion – feels like it’s only become more pronounced. We wrote last time that ‘‘we believe we’re entering a new era of dispersion in the performance of financial assets.’’ We picked out pockets of dislocation that aren’t clearly visible in aggregate metrics, including CCC-rated loans trading at outsized spreads while the overall index presents a sanguine picture.

Three months later, CCCs aren’t looking any healthier but a volley of headlines regarding potential vulnerabilities in the credit markets – chiefly relating to software debt – has impacted investor sentiment. Add in resurgent inflation and stubbornly high interest rates, which compound the pressure on already-struggling borrowers, and we feel dispersion in asset performance is set to accelerate.

The bulk of the credit universe remains in decent health, but there’s a meaningful subset of borrowers under pressure. What does this mean in practical terms? In performing credit strategies, managers must avoid the losers to retain a still-attractive contractual yield. In more opportunistic strategies, there’s a growing potential to selectively pursue pockets of dislocation.

1. No respite for CCCs

There’s been no let-up for CCC-rated loans, with spreads widening by over 300 bps so far this year.1 In contrast, higher-rated credits have shown remarkable resilience: BB-rated loan spreads have marginally tightened this year, making for a yield of just over 6% – about a quarter of the level of CCCs.2 In short, the rating bands are a world apart, with the sort of aggressive bifurcation normally seen in a recession. So, what’s going on?

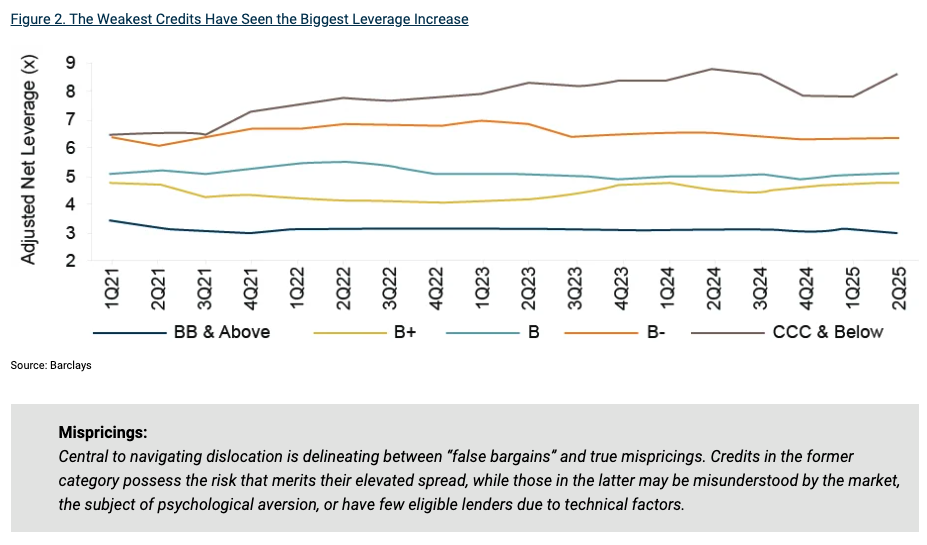

Market participants are expressing a clear view: the weakest credits cannot handle elevated interest rates and will struggle to refinance through mainstream channels. The fundamentals appear to validate this concern: leverage on CCC-rated loans has crept higher while other rating categories haven’t seen such increases. (See Figure 2.)

Given the risk of default and the reality of poor recovery rates, buyers expect to be compensated in the form of an outsized spread. Meanwhile, higher-quality names continue to attract a broad buyer base, particularly from CLOs, thereby keeping spreads tight.

2. Software under the microscope

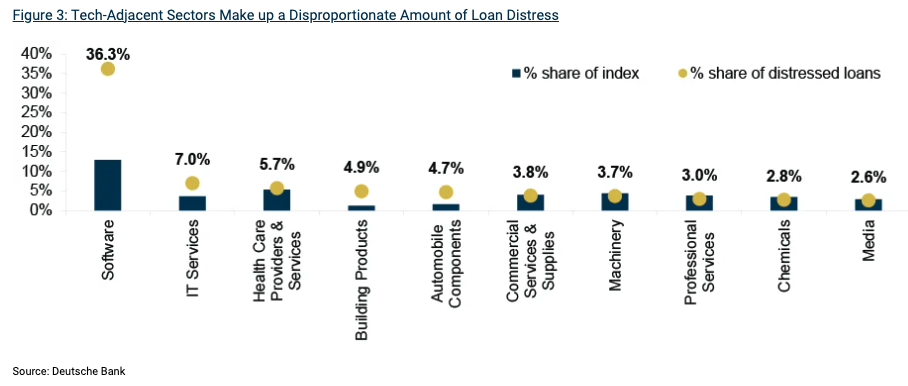

Investors are concerned that AI could rapidly antiquate certain software business models. The shift in sentiment has been abrupt, with a sharp reappraisal of the lofty valuation and leverage multiples that characterized the software LBOs of recent years. The credit market reaction has been significant, with software and IT services together making up over 40% of overall distress in the senior loan market.3 (See Figure 3.) In fact, at our 2026 client conference, Bob O’Leary, Co-CEO of Oaktree, described software’s troubles as ‘‘the swiftest fall from grace of any sector that I have ever seen.’’

Against this backdrop, it is reasonable to expect that managers’ ability to prudently navigate this sector will be a determinant of relative performance. This includes both portfolio weighting to the sector and the selection of individual names within it. While the risks are well broadcast, it’s worth noting that the software sector is currently entirely unloved – meaning certain robust names may be ‘‘thrown out with the bath water’’ and trading at unreasonably depressed levels.

3. Direct lending headlines

Direct lending has been the story of the quarter. The fastest-growing area of private credit appears to be experiencing growing pains. So, what are the major concerns?

- PIK (payment-in-kind) reliance: represents around 10% of total interest for public BDCs, and around 4% for perpetual BDCs, but with dramatic variation among managers.4 While these levels appear stable, it’s reasonable to acknowledge PIK isn’t a long-term solution for a weak borrower. PIK loans are currently marked at 91 cents on the dollar, indicating all isn’t well for this subset of loans.5

- Evergreen funds liquidity mismatch: perpetual BDCs have mostly experienced a one-way street of inflows until this quarter, when most received redemptions above the standard 5% threshold, leading to many BDCs limiting redemptions. This is the structure working as designed – to avoid forced sales – but it undoubtedly impacts investor sentiment.

- Software exposure: software has been a favored sector of the private equity industry, with over $400 billion of deal activity in 2021 and 2022 alone.6 Much of this activity has been funded by private lenders, with software now making up over 20% of the direct lending market.7 For the reasons described in the previous section, investors are now concerned about this level of concentration.

What’s the upshot of this? Firstly, it’s a good reminder of the importance of increased selectivity in direct lending. Secondly, pockets of weakness may create potential access points for opportunistic investors, including through rescue financings for struggling individual borrowers, as well as more esoteric opportunities, such as portfolio sales.

4. Returning inflation?

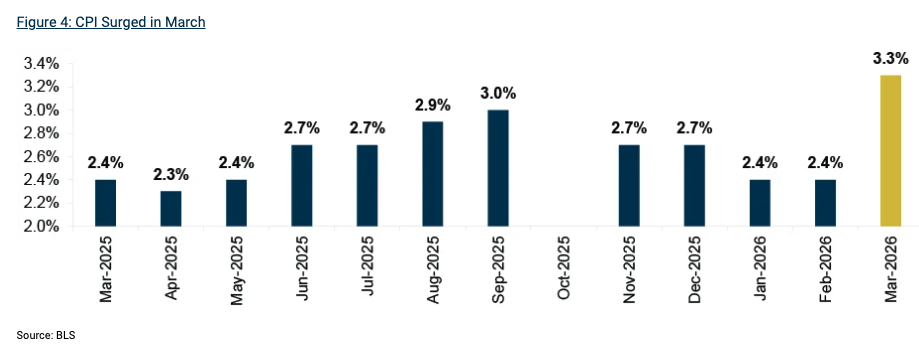

Central banks have been attempting to tame inflation for several years now, with its stubbornness reflected in the federal funds rate still standing at 3.50-3.75%.8 Resurgent inflation, fueled by rising energy costs, won’t help matters. (See Figure 4.) The bond markets are making their thoughts clear: UK gilt yields recently reached a level not seen since the GFC, with the 10-year touching 5%; German bunds – which had a negative yield for much of 2019-2021 – are hovering around 3%; while the U.S. 10-year Treasury rose over 40 basis points between Feb 27 and April 30.9

It would be a foolish endeavor to predict the long-term paths of oil prices or interest rates given the unpredictability of macroeconomics, but it’s clear a surge in energy costs has an immediate impact on corporates and consumers. It presents a particular headwind to an already-pressured lower-income consumer, for whom gasoline makes up 8% of total card spending, while the impact on corporates will be determined by their ability to pass through price increases.10

5. Restructuring outcomes

Recovery rates in the leveraged finance universe remain low overall and uneven across lenders.

The recovery rate on first-lien loans currently stands at around 40%, with high yield bonds closer to 35%, both significantly below their long-term averages.11 This is a function of unitranche structures, weak covenants and limited equity cushions, as well as the value erosion from repeat liability management actions. In fact, repeat default actions comprised a record 41% of default activity last year.12

Much of the unevenness in experience results from liability managements exercises (LMEs), a topic we addressed in depth in a prior quarterly and podcast. As we wrote:

Although historically, with certain exceptions, lenders holding the same debt instrument were generally treated on a pro rata basis, LMEs can disrupt this outcome, creating a significant disparity in recoveries across otherwise similarly situated lenders.

We continue to believe securing superior outcomes in an LME is a function of scale, with the size of holdings (along with strong industry relationships) generally determining a spot in the ‘‘in-group’’ during an LME.

Navigating a new era of dispersion

On April 30, 2021 – exactly five years ago at the time of writing – leveraged loans yielded 4.8%.13 Today that figure is 8.6%.14 This is a boon for income-seeking investors but not for borrowers, who’ve seen their coupon payments jump 70%.15

That means the yields aren’t a freebie. Some borrowers will have a tougher time than during the low-rate era of 2009-2021. This creates opportunities for credit managers to demonstrate skill by avoiding the losers. It also creates the pockets of dislocation pursued by intrepid investors, who can see through volatility to provide complex capital solutions when they’re needed most.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Endnotes

1Morningstar LSTA US Leveraged Loan Index, May 1, 2026.

2Morningstar LSTA US Leveraged Loan Index, May 1, 2026.

3Deutsche Bank, Global Default Monitor, March 3, 2026.

4Oaktree analysis.

5Goldman Sachs, Private Credit Monitor (April 13, 2026), based on average mark of PIK loans within the Cliffwater Direct Lending Index as of 4Q2025.

6PitchBook, Analysis: PE exposure to Software booms amid sector reckoning, February 20, 2026.

7Morgan Stanley, Mapping Software Exposure in Leveraged Credit, February 9, 2026. BDC software exposure estimated at 26% and used as rough proxy for direct lending industry.

8Federal Reserve, April 30, 2026.

9Trading Economics, Federal Reserve Bank of St. Louis. U.S. 10-year Treasury yield of 3.97% on Feb 27 to 4.40% on April 30.

10BofA, Consumer Checkpoint, April 10, 2026.

11J.P. Morgan, Default Monitor, April 1, 2026 (LTM recovery rate of 35.7% for HY bonds and 40.1% for first lien loans).

12J.P. Morgan, Default Monitor, April 1, 2026 (25/61 default actions in 2025 had already experienced a default action).

13UBS LevLoan Index, April 30, 2026.

14UBS LevLoan Index, April 30, 2026.

15UBS LevLoan Index, April 30, 2026.

Originally posted on Oaktree Capital Management

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All