What Would The Merton Model Say About AI Capital Spending?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways:

- AI-driven spending is benefiting stocks more than bonds: Equity investors are leaning into growth from AI investments, while credit markets are demanding more compensation for rising leverage and uncertainty.

- Not all credit is equal: Software and private-equity-backed borrowers are under more pressure, highlighting the need for careful issuer selection in below-investment-grade portfolios.

- Senior structured credit remains resilient – for now: High quality exposures such as AAA rated collateralized loan obligations (CLOs) continue to hold up, supported by diversification and their position in the capital structure, but would be tested in the unlikely event of a severe downturn.

Read more: Daily Pricing Is Not Daily Liquidity

Hyperscalers: Volatility helps the call and hurts the put

Fifty-two years ago, economist and future Nobel laureate Bob Merton published a seminal paper on the valuation of corporate bonds. The Merton model has plenty of shortcomings that the financial literature has spent decades trying to address, but its central intuition is rock-solid: Shareholders are long a call on the company’s assets and bondholders are short a put on those same assets. In other words, equity investment centers on upside potential, while credit is about downside mitigation.

That single insight explains much of what we are seeing recently across the capital structures of hyperscalers – the massive providers of cloud computing and networking resources essential to the AI buildout.

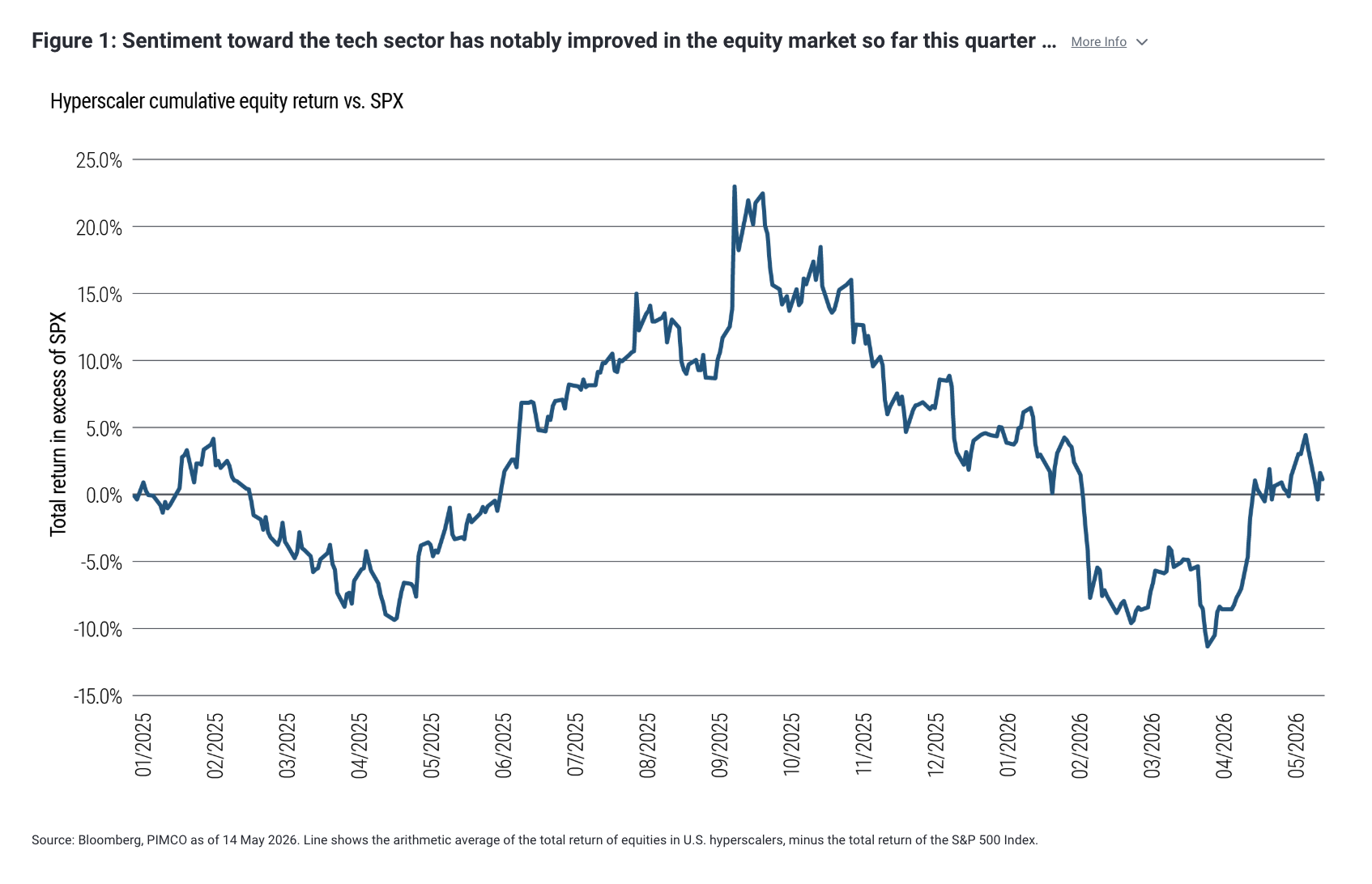

Quarter-to-date, sentiment toward the tech sector has notably improved in the equity market (with the exception of the weakness late last week), buoyed by a decent first-quarter earnings season that calmed investor nerves over the risk of capex overspending. The relief has been visible across the entire AI ecosystem: semiconductors, hyperscalers, and even software, which had been the laggard for much of the prior quarter (see Figure 1).

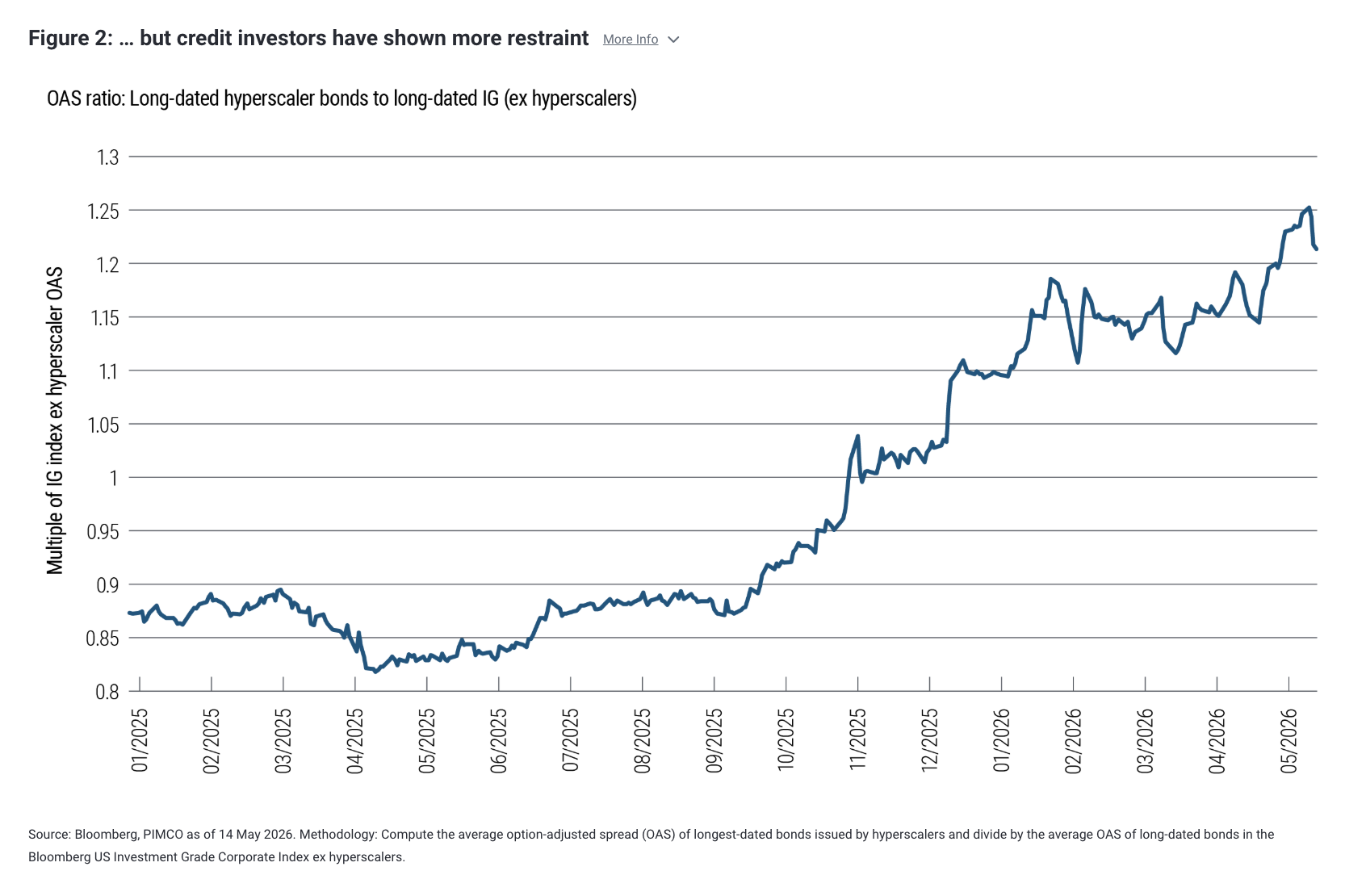

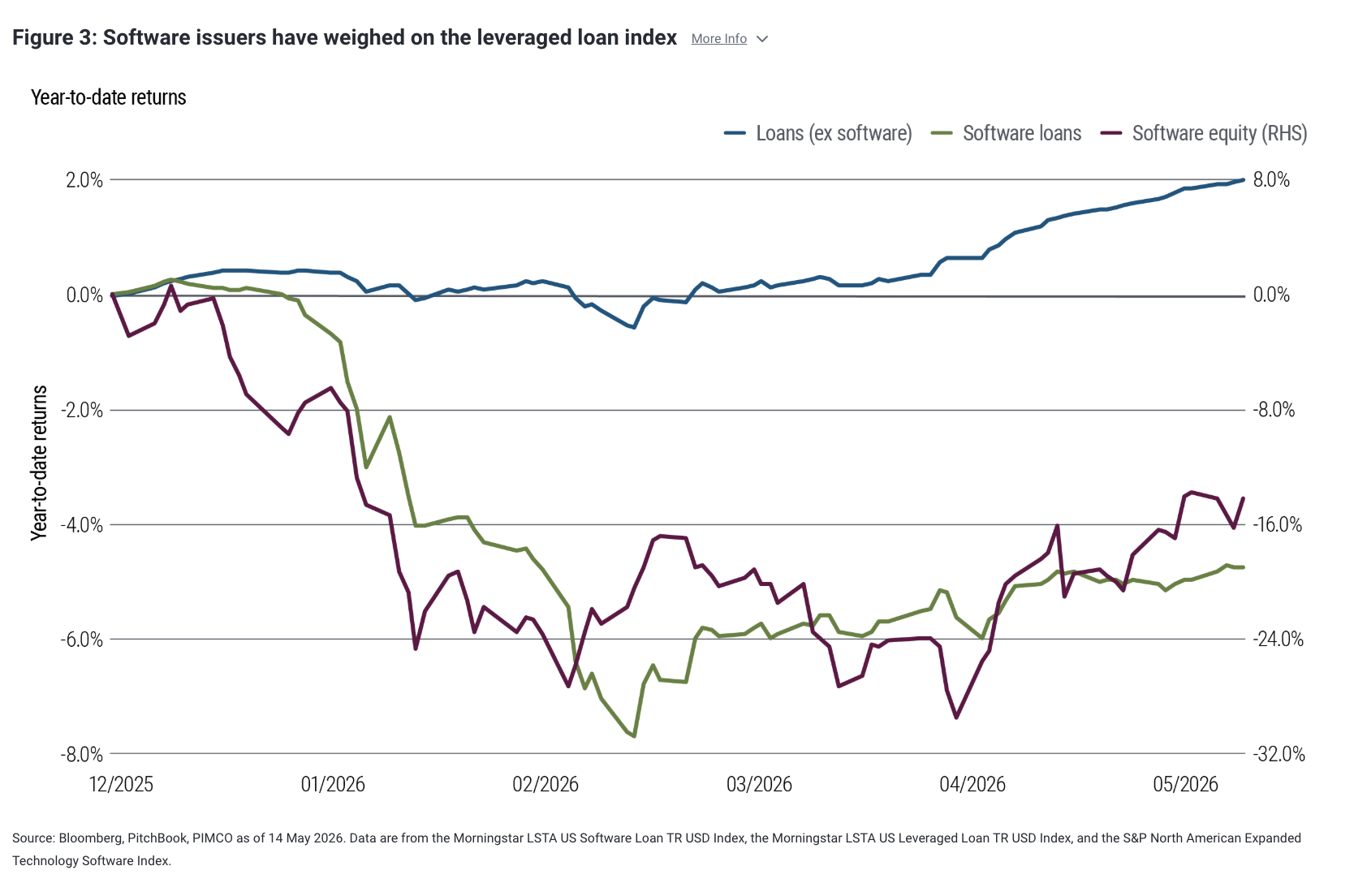

The credit market has shown more restraint. Hyperscalers have underperformed the broader investment grade market in recent weeks (see Figure 2) as investors digest the implications of a multi-year, debt-funded capex cycle. Software, meanwhile, has yet to catch a bid in the leveraged loan market, where AI disruption risk remains priced in (more on this below).

The Merton framework helps explain the bifurcation between equity and credit price moves. A leveraged bet on AI infrastructure with uncertain and potentially volatile payoffs tends to raise the value of the equity call even as it makes the bondholders’ implicit put more risky. In Merton terms, asset values may be increased, but so is the strike price of the put.

For shareholders, the upside justifies the gamble. For bondholders, the downside is real and the upside belongs to someone else. That wedge – the classic asset substitution problem – is what credit investors are increasingly pricing, and until the re-leveraging impulse shows signs of reaching a plateau, the divergence across the capital structure is likely here to stay.

Leveraged loans: The sponsor put is no longer working

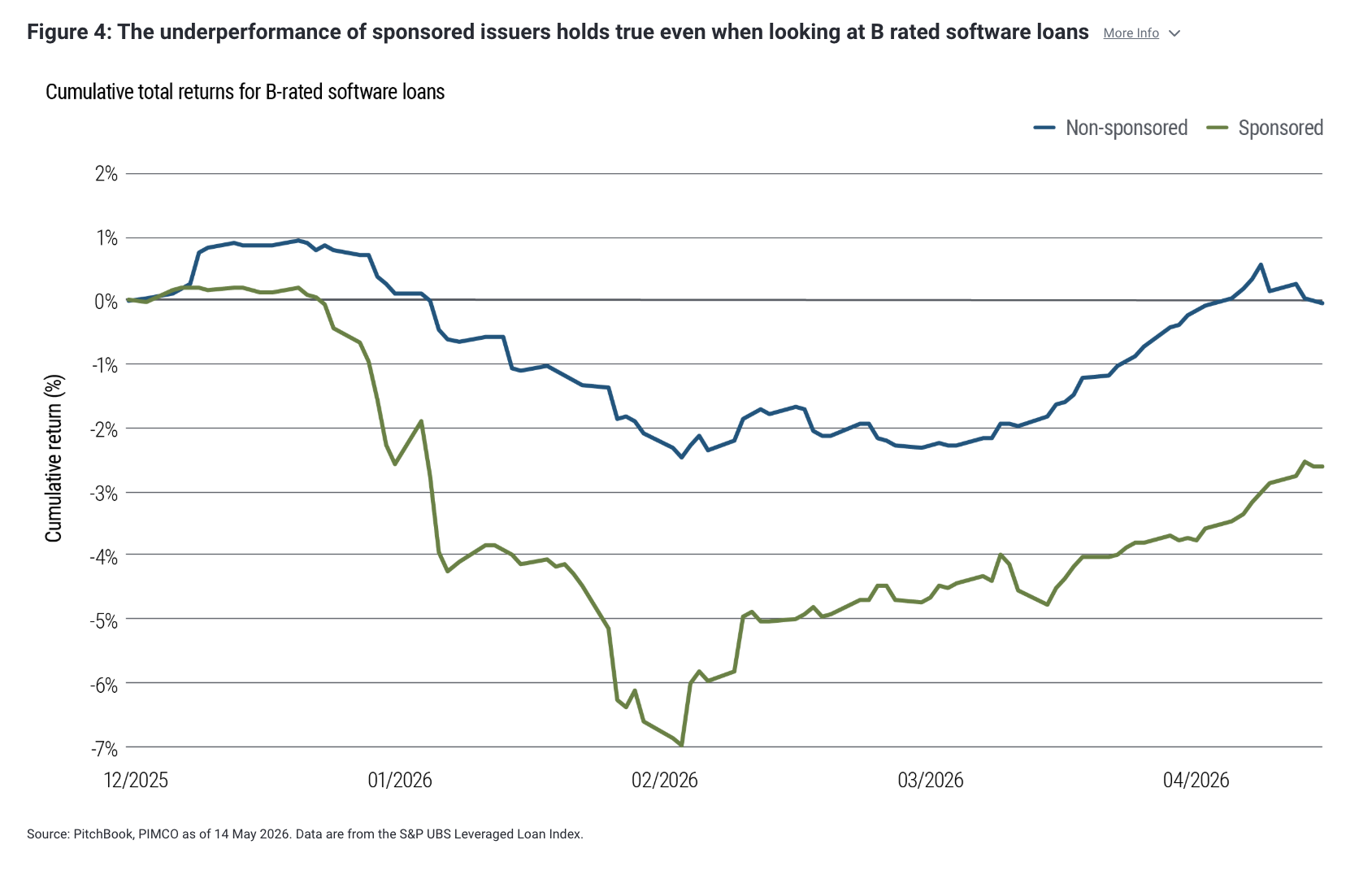

Within the software sector, there has also been clear bifurcation between sponsored and non-sponsored issuers. Although private equity (PE) ownership/sponsorship had been viewed favorably during past periods of weakness, such as the COVID-19 pandemic, this is no longer the case. Loans issued by PE portfolio companies have been materially underperforming those issued by non-sponsored firms. Of course, at the index level one could cite differences in quality and sector composition as the driver of this performance differential, rather than just PE sponsorship. Therefore, to address this critique, we go deeper to show the result in two more robust ways.

First, we conduct a like-for-like comparison by focusing on B rated software loans in the S&P UBS Leveraged Loan Index, constructing one portfolio of sponsored issuers and another of non-sponsored ones. These portfolios control for differences in both credit quality and sector. Figure 4 shows that even within this tightly controlled subset, PE ownership has been a drag on performance.

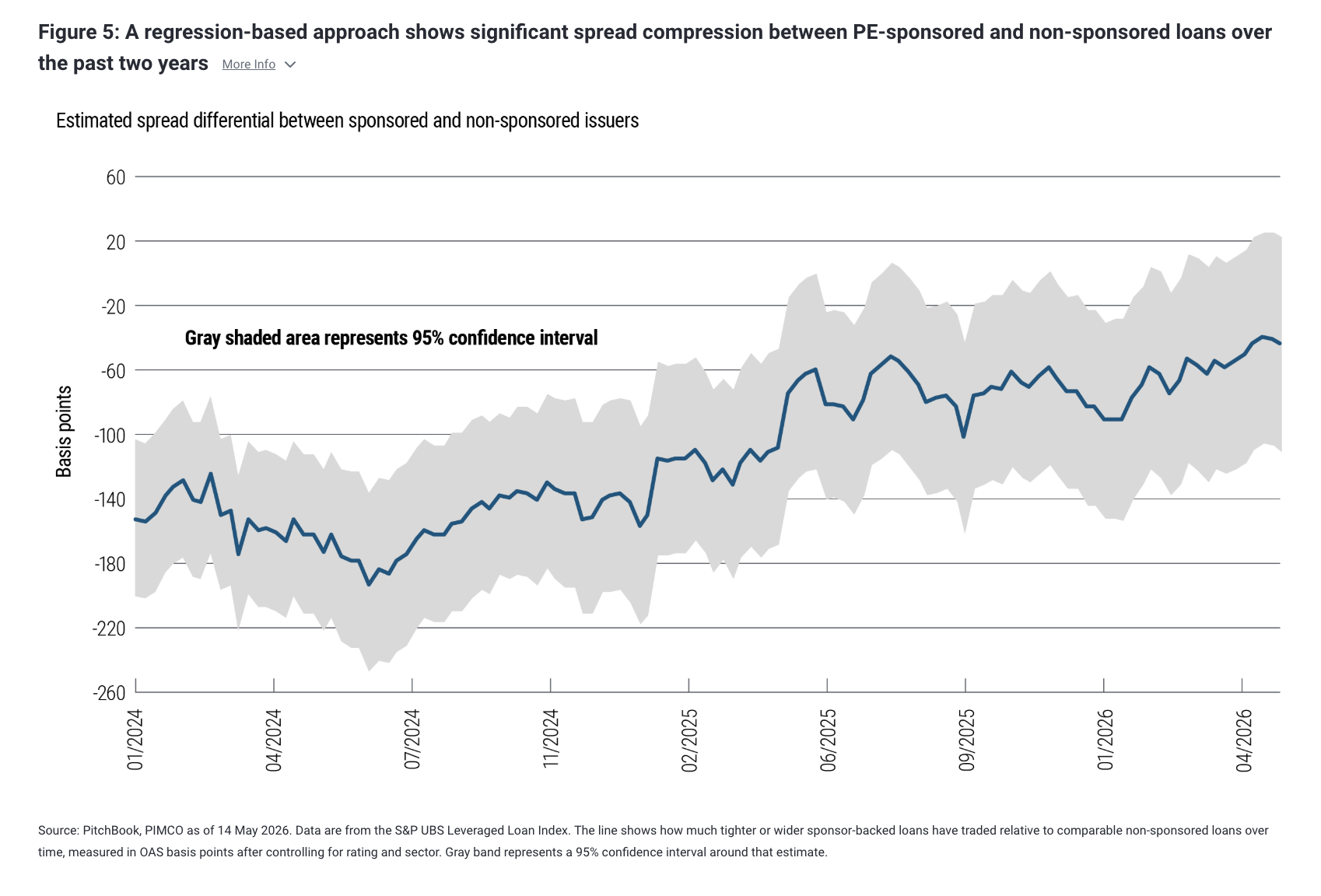

In the second approach, we use a regression-based framework. This method effectively compares two hypothetical portfolios of sponsored and non-sponsored loans in the same index that are otherwise identical in terms of industry and rating composition (see Figure 5). Here again, the result holds, suggesting that the underperformance is not simply a function of compositional differences, but rather reflects a more fundamental shift.

AAA CLO performance: No spillovers yet from the software sector

While software loans have repriced, the broader leveraged loan market has largely succeeded in isolating this weakness and hasn’t been dragged down in a meaningful way. This containment helps explain the striking resilience of spreads in AAA collateralized loan obligations (CLOs).

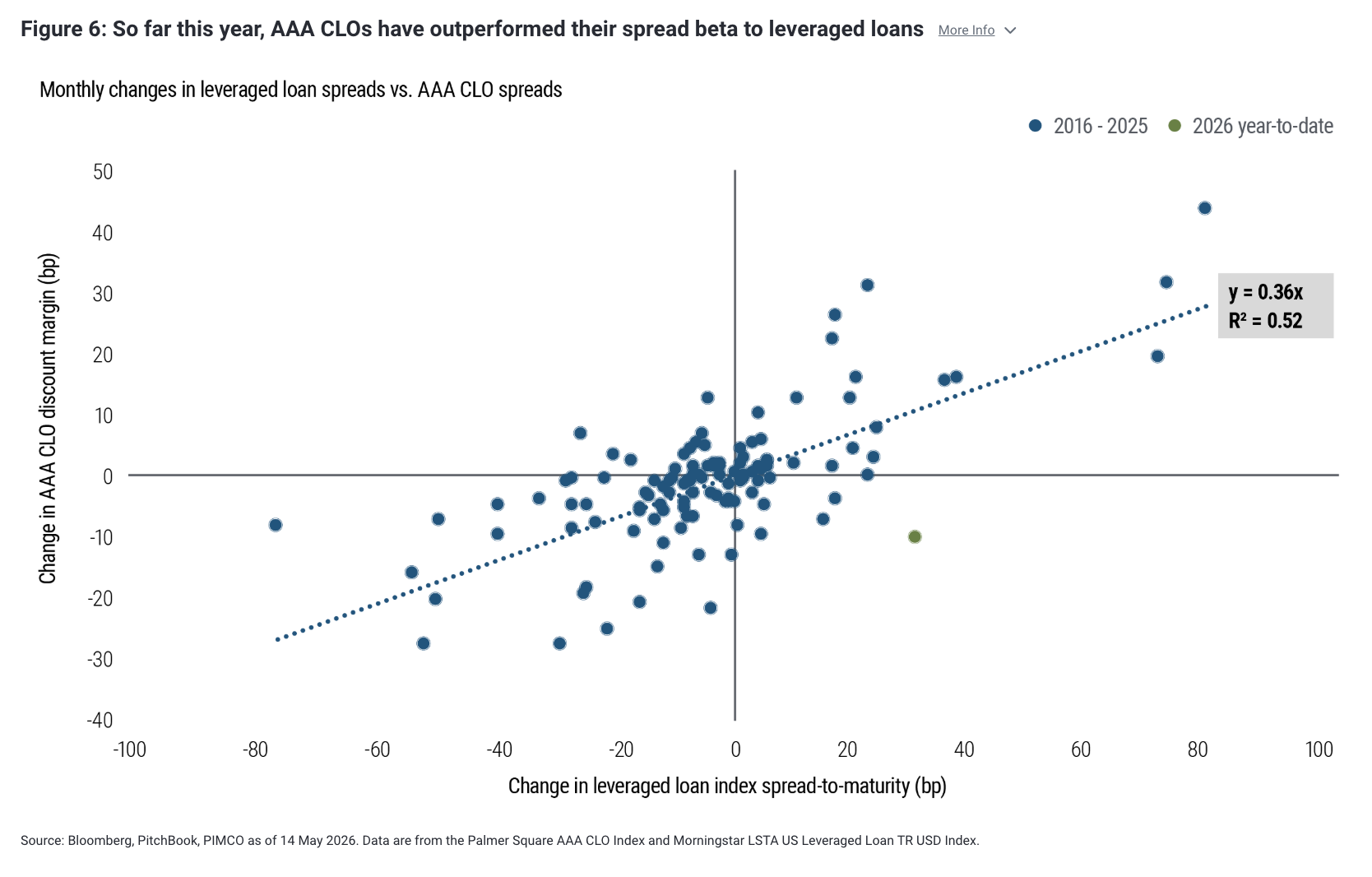

So far this year, AAA CLO spreads have outperformed their historical beta to leveraged loans by a wide margin. If the past empirical relationship had held, the 30 basis points (bps) of year-to-date widening in leveraged loan spreads should have pulled AAA CLO discount margins wider by roughly 11 bps. Instead, AAA CLO spreads are actually tighter by 10 bps (see Figure 6).

Aside from the index-level containment, another main reason for the AAA CLO outperformance is structural subordination – that is, the order in which claims are contractually repaid, with senior tranches coming before junior ones. Even where software exposure exists within CLO portfolios, the deep subordination cushion at the AAA level means the bar for losses to reach the senior tranche is exceptionally high. AAA attachment points are deeply out of the money, and CLO portfolios tend to be diversified across hundreds of issuers and dozens of sectors.

Therefore, for AAA CLO spreads to reprice meaningfully wider, the stress would need to extend well beyond a single sector – it would require a systemic credit event producing default losses far above historical norms. That scenario remains firmly outside the baseline, particularly given the continued resilience of U.S. economic growth.

Michael Puempel and Gabriel Cazaubieilh contributed to this report.

Disclosures:

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. It is not possible to invest directly in an unmanaged index.

Past performance is not a guarantee or a reliable indicator of future results. All Investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Collateralized Loan Obligations (CLOs) involve a high degree of risk and are intended for sale to qualified investors only. Investments in subordinated tranches of CLOs often represent highly leveraged investments in the underlying assets, and may lose all or a significant portion of their value, even if other tranches of the CLO do not. CLOs are typically illiquid, and holders may not be able to sell these securities at an attractive time or price, or at all. CLOs are also exposed to risks such as credit, default, liquidity, management, volatility, interest rate and credit risk. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0515-5497575

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All