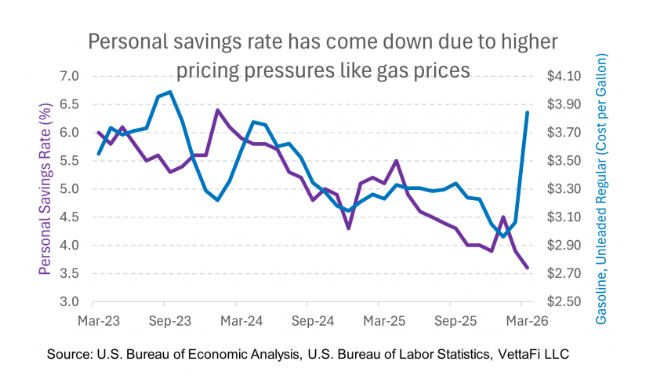

The consumer is still spending, but with a higher level of caution. Inflation remains a persistent pressure point, particularly for lower- and middle-income households. This has caused the U.S. personal saving rate to fall to 3.6% as of March 2026, leaving significantly less breathing room for discretionary purchases.

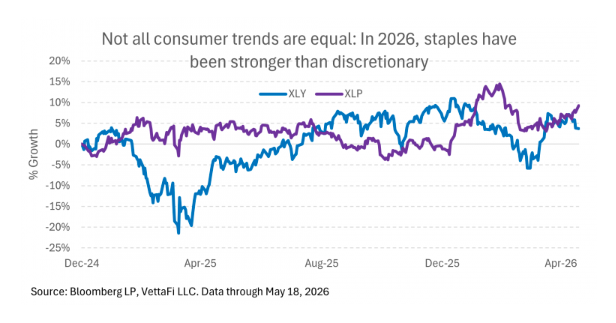

Against this environment, consumer staples continue to look highly attractive relative to more cyclical consumer discretionary categories. This isn’t because staples are completely immune to macroeconomic pressures, but because many of these businesses sell everyday goods, emphasize value, and have revenue streams that tend to be stickier in uncertain environments. Retailers, including staples companies, are also shifting toward e-commerce which has widened its reach from select discretionary items to broad consumer needs.

The consumer is still spending, but with a higher level of caution. Inflation remains a persistent pressure point, particularly for lower- and middle-income households. This has caused the U.S. personal saving rate to fall to 3.6% as of March 2026, leaving significantly less breathing room for discretionary purchases.

Against this environment, consumer staples continue to look highly attractive relative to more cyclical consumer discretionary categories. This isn’t because staples are completely immune to macroeconomic pressures, but because many of these businesses sell everyday goods, emphasize value, and have revenue streams that tend to be stickier in uncertain environments. Retailers, including staples companies, are also shifting toward e-commerce which has widened its reach from select discretionary items to broad consumer needs.

While e-commerce has been integrated into traditional retail, the standalone theme remains compelling

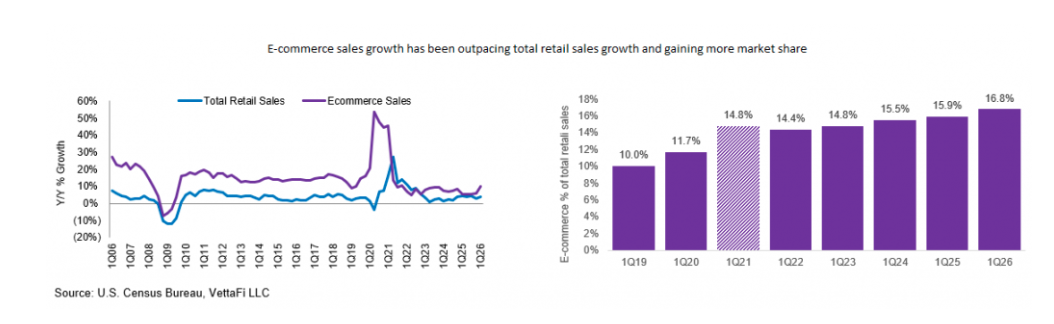

E-commerce remains one of the strongest growth drivers in retail. According to the U.S. Census Bureau, U.S. retail e-commerce sales reached an estimated $326.7 billion in 1Q26, up 2.7% from 4Q25 and 9.8% from 1Q25. That compares with total retail sales growth of 1.5% quarter over quarter and 3.9% year over year. E-commerce accounted for 16.9% of total retail sales in the quarter, showing that online sales continue to gain share even as the broader consumer environment remains uneven.

That is significant because e-commerce is becoming less about discretionary spending and more about convenience, value, and repeat purchases. Online retail was often tied to higher-growth discretionary categories like apparel, electronics, and home goods. But today, many of the strongest e-commerce platforms are tied to everyday spending categories, including grocery, household essentials, health and beauty, and club retail. This is one reason the e-commerce theme now overlaps more closely with the staples story in addition to the discretionary story. Consumers may be cautious, but they are still buying necessities and increasingly using digital tools to compare prices, find discounts, schedule pickup, or order delivery.

Large retailers with greater scale are especially well-positioned. Walmart and Costco show how e-commerce is becoming part of the broader retail story including staples, rather than a separate business line. Walmart’s latest quarter showed 27% growth in Walmart U.S. e-commerce, supported by store-fulfilled pickup and delivery, marketplace, and advertising. Costco’s most recent quarter showed 22.6% growth in digitally enabled comparable sales, well above its total comparable sales growth of 7.4%. In both cases, digital growth is being supported by existing store networks, membership models, and loyal customer bases.

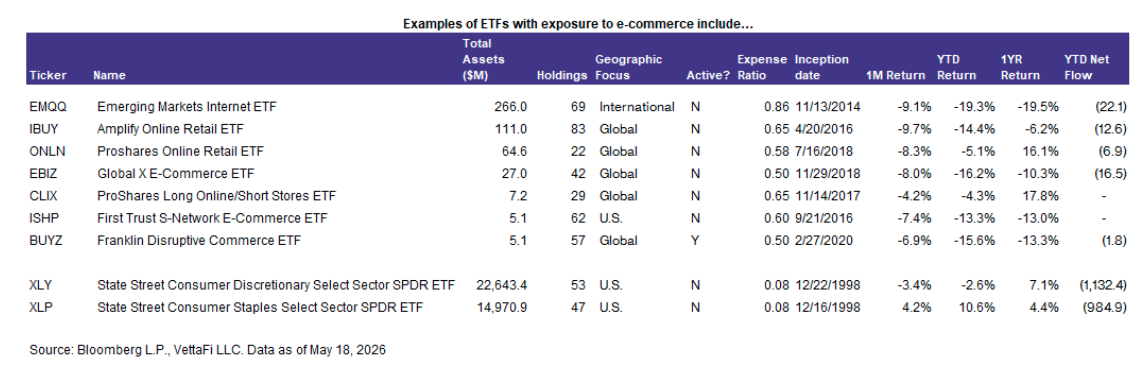

Other ETFs focus strictly on e-commerce

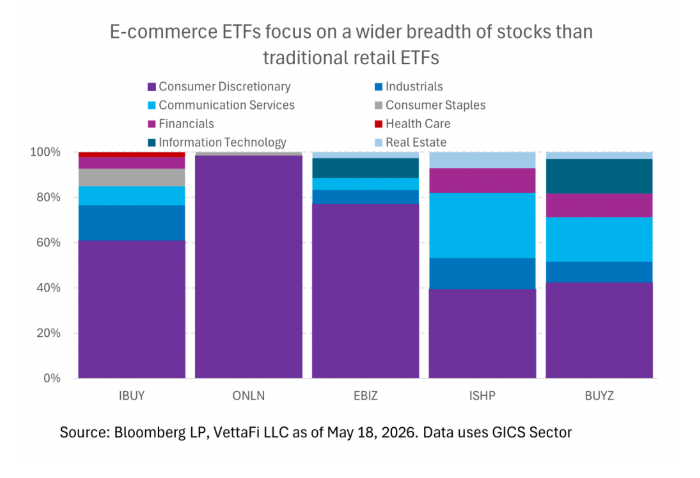

E-commerce is now embedded across the retail ecosystem, including broad retail ETFs, consumer discretionary ETFs, and even staples-oriented funds with exposure to companies like Walmart and Costco. But for investors who want a more focused look at e-commerce, including exposure to internet companies (technology), financials (payment systems), and industrials (logistics and delivery companies), several ETFs exist that specifically follow that theme. A few are listed below

-

Amplify Online Retail ETF (IBUY): This ETF is the largest global e-commerce ETF with around $110 million in assets. It holds companies in online retail, online travel, online marketplace, and omnichannel retail that have at least 70% of revenues or a minimum of $100 billion in annual retail sales in online transactions. For omnichannel retailers, online sales must be at least 10% of total annual retail sales and more than $2 billion in revenue or in the top five of global online retail market share. Equally-weighted, these stocks have a 10% aggregate cap on omnichannel. While a global ETF, IBUY is mostly U.S. stocks with non-U.S. domiciled stocks are capped at a 25% total weight. Holdings include eBay (EBAY), Spotify Technology (SPOT), Maplebear (CART), Peleton Interactive (PTON), and Affirm Holdings (AFRM).

-

ProShares Online Retail ETF (ONLN): Holdings include online retailers, e-commerce retailers, or internet retailers. Unlike IBUY, ONLN excludes online travel companies. Holdings are weighted based on market capitalization, with non-U.S. companies limited to a total of 25%. While its peers have smaller exposure to Amazon (AMZN), ONLN has a 25% weight to this stock. Amazon, Alibaba Group (BABA), and eBay (EBAY) make up around 50% of the ETF’s weight.

-

First Trust S-Network E-Commerce ETF (ISHP): ISHP invests in the top 15 companies by market cap in four business segments: content navigation, online retail, online marketplace, and e-commerce infrastructure. These companies are then equal-weighted. This ETF holds some unique stocks not included by many of its peers, including internet stocks like Reddit Inc (RDDT)and Meta Platforms (META) in addition to logistics/delivery companies like AP Moller-Maersk (MAERSKB DC) and United Parcel Service (UPS).

For more news, information, and analysis, visit VettaFi | ETF Trends.

VettaFi LLC (“VettaFi”) is the index provider for IBUY and ISHP, for which it receives an index licensing fee. However, IBUY and ISHP are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of IBUY or ISHP.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Read more commentaries by VettaFi