The Cost of Being Too Liquid

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey points

- Private markets (private equity, private credit and real estate) have historically delivered an “illiquidity premium”

- Institutions and family offices have recognized this illiquidity premium and have historically allocated significant capital to capture it

- Advisors should consider developing an “illiquidity bucket”

- Allocating a portion of a client’s portfolio to illiquid investments helps in maintaining a long-term approach

Legendary investor David Swensen famously stated that the “intelligent acceptance of illiquidity, and a value orientation, constitutes a sensible, conservative approach to portfolio management.”1 What Swensen, and so many other sophisticated investors recognized is the illiquidity premium available by allocating capital to illiquid investments like private equity, private credit and private real estate.

In fact, throughout Swensen’s tenure as the chief investment officer of the Yale endowment, he often allocated between 70%–80% of his portfolio to alternative investments broadly, with illiquidity budgets of up to 50% of the total allocation. The illiquidity bucket is a technique institutions use to identify the amount of capital that they are willing to tie up for an extended period of time (7–10 years). As of the end of fiscal year 2025,2 Yale had a roughly US$44 billion in assets under management, with about 55% in the illiquidity bucket.

Of course, endowments are very different than individual investors, and Yale has certain built-in advantages, including unique access to private markets, dedicated resources to evaluate opportunities and long-time horizon. If Yale needs capital, it has the ability to reach out to well-heeled alumni and donors for additional capital.

Most high-net-worth (HNW) investors would be uncomfortable locking up so much capital—but the concept of an illiquidity bucket would certainly apply. While high net-worth-investors may not have donors to call upon, they often do share something with Yale—a long time horizon for some of their goals.

What does the data show?

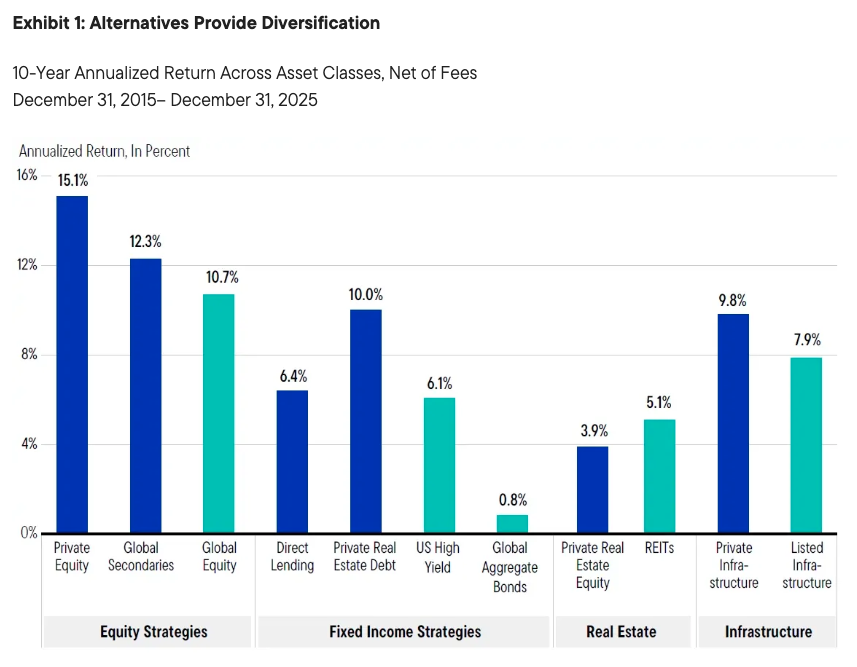

Academic research has shown the historic persistence of an illiquidity premium3—the excess return received for tying up capital for an extended period of time. This makes intuitive sense because the private fund manager has ample time to source opportunities and unlock value. The fund manager isn’t beholden to investors and shareholders, like their public market equivalents, who are viewing results over shorter intervals.

While the magnitude of the illiquidity premium will vary over time, depending upon the market environment and the fund, the data show that private equity, private credit and private real estate have historically delivered a substantial illiquidity premium relative to their public market equivalents. Note, private markets will not outperform their public market equivalent over all time periods.

Historically, the US equities has delivered an annualized return of about 10% over the past century. In recent years, US equities have exceeded its historical average. While this recent outperformance is notable, it is important for investors to maintain a long-term perspective when evaluating both public and private investments across different market environments.4

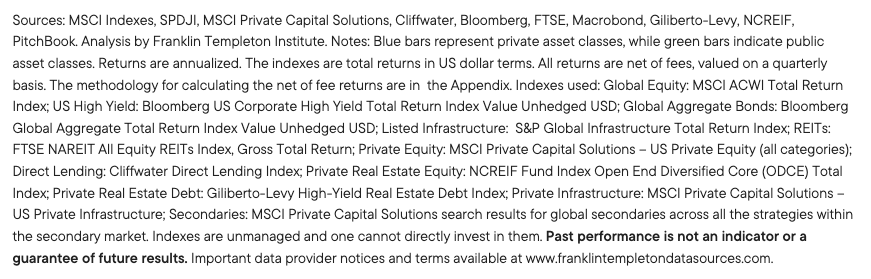

Institutions and family offices have long recognized this illiquidity premium and consequently have historically allocated significant capital to private markets. In fact, according to the UBS Global Family Office Report, Family Offices have allocated roughly 44% of their portfolios to alternative investments, with private equity and real estate representing the largest allocations at 21% and 11%, respectively (see Exhibit 2).

The report notes that such families are comfortable allocating capital for the long-run in order to capture the illiquidity premium. The average illiquidity bucket for this cohort is approximately 37% (private equity, real estate, private credit (debt) and art).

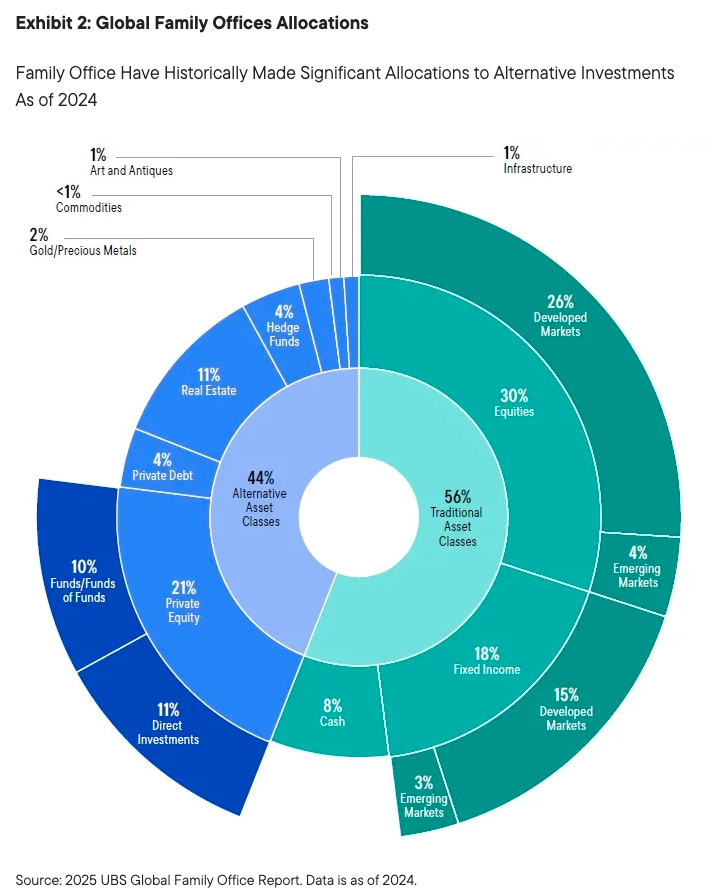

The report also notes that many of these global family offices are looking to increase their allocations to the private markets, notably private equity, real estate and private credit.

High-net-worth demand

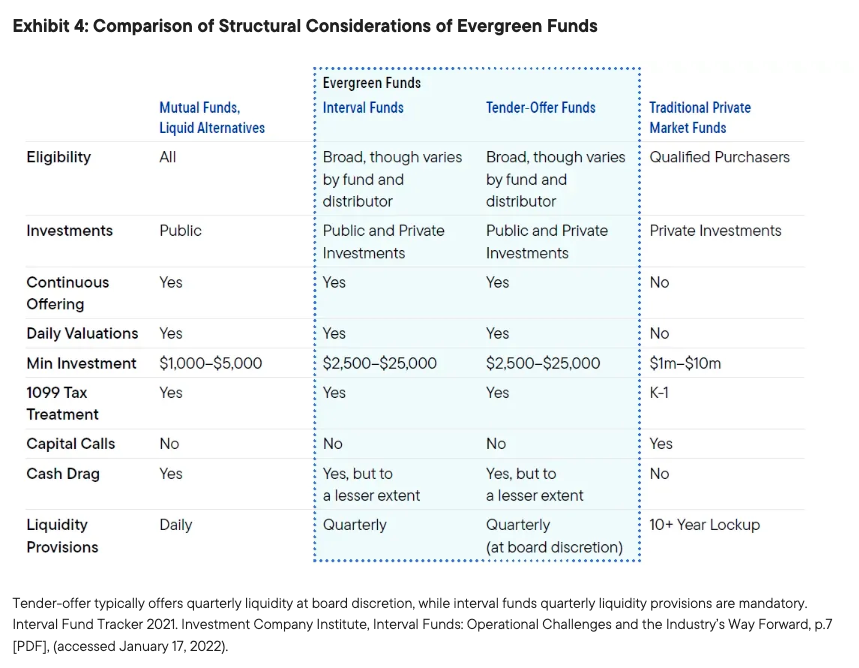

Up until recently, HNW investors had limited access to these elusive investments due to HNW investor eligibility and high minimums. However, due to product innovation and a willingness of institutional-quality managers to bring products to the wealth management marketplace, HNW investors now have a broad array of options to select from.

As the table below illustrates, the first generation of private market funds were only available to qualified purchasers (individuals with US$5 million or more of investable assets) and had high minimums and limited liquidity. This structure was fine for institutions and family offices who could comfortably commit capital for the long run, but not an ideal structure for most investors who would not even meet the minimum or accreditation requirements.

Interval funds and tender-offer funds are available to a broader group of investors and have lower minimums and more flexible features. Like traditional mutual funds, they are continuously offered, provide daily valuations and 1099 tax reporting. Unlike traditional mutual funds, they can hold illiquid investments, and their liquidity provisions are quarterly, not daily.

The growth of evergreen funds has expanded the access of private markets to HNW investors and allowed advisors to scale their allocations across their practices. While interval funds and tender-offer funds offer more flexible liquidity provisions than the first generation of fund structures, they should be viewed as long-term investments to potentially capture the illiquidity premium noted above. There may be a cost for offering greater liquidity—a “cash drag”—the cost of holding more liquid assets to meet periodic redemptions.

How much should advisors allocate to illiquid investments?

The amount of capital to allocate to illiquid investments varies by investor and their underlying liquidity profile. Many investors believe that they should be 100% liquid, but there is an opportunity cost, especially in today’s market environment. Traditional liquid market investments may continue to deliver returns below their historical averages, and advisors may need to consider private markets to help investors achieve their goals.

One way of determining the appropriate percentage to allocate to private markets is to develop an illiquidity bucket. Similar to the Yale example covered earlier, the illiquidity bucket should represent the amount of capital that an investor is willing and able to tie up for 7–10 years. It can be determined via the discovery process and advisors should designate these investments as long-term in nature.

As the advisor is determining the family’s needs and requirements, they should inquire about their short- and long-term liquidity needs. Do they have significant capital expenditures in the next couple of years (college funding, purchasing a second home, boats, etc.)? How much of their portfolio needs to be short-term in nature to meet these needs? What portion are they comfortable putting aside for the next 7–10 years?

For many HNW investors, a 10%–20% illiquidity bucket may be appropriate given their wealth, income and cash flow needs. Once the advisor has determined the illiquidity bucket, they can then define which asset classes are appropriate to achieve their client’s goals.

Allocating to private markets

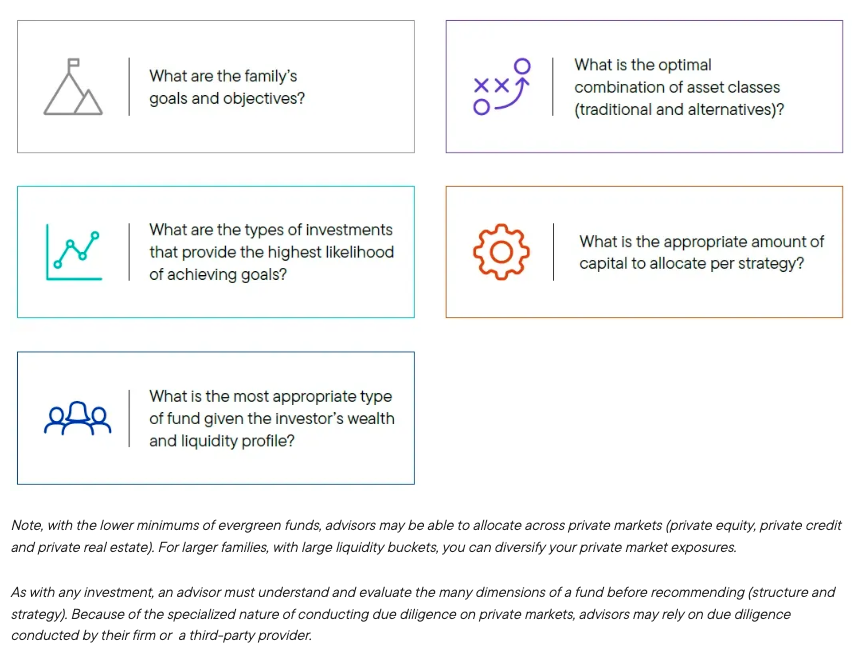

Once the illiquidity bucket for long-held assets has been established for a particular client, an advisor can then determine the appropriate allocation to private markets. There are several factors to consider before allocating.

As with any investment, an advisor must understand and evaluate the many dimensions of a fund before recommending (structure and strategy). Because of the specialized nature of conducting due diligence on private markets, advisors may rely on due diligence conducted by their firm or a third-party provider.

The behavioral benefits of illiquidity

While many consider the Altair 8800 the first personal computer (1974), the original personal computer was the human brain. The brain is capable of complex computations, processing information rapidly, and it has extended storage capacity. The human brain processes information in seconds and is capable of learning history, math, science, literature, philosophy and the arts.

However, unlike the personal computers that we use today, the human brain also responds to all sorts of emotional stimuli, including fear, greed, euphoria, grief, pain and pleasure. While the modern-day PC processes information in nanoseconds, in a logical and rational fashion, the human brain often responds to emotional stimuli in an irrational manner.

Daniel Kahneman was awarded the Nobel Prize for his research of behavioral finance, how the brain responds to certain stimuli and the biases that we all exhibit. One of the behavioral biases that Kahneman studied was “loss aversion.” In his book, Thinking, Fast and Slow, Kahneman suggested that investors will go to great lengths to avoid losses.

In fact, his research concluded that for the average investor, the ratio of avoiding losses to seeking gains is roughly 2:1. Consequently, investors may fall short of their goals by being too conservative or leaving the market in times of volatility. While loss aversion is well known, and advisors often coach investors to refrain from these irrational responses, it is still very challenging to act rationally in volatile times.

Of course, there is a built-in benefit of allocating a portion of a client’s portfolio to illiquid investments—it removes the emotional impulse to sell at the wrong time or switch strategies midstream. By utilizing an illiquidity bucket for a portion of a client’s portfolio, an advisor can instill discipline to their investment approach.

For this portion of their portfolio, investors can’t sell at the first signs of volatility or the temptation to chase returns elsewhere. These assets are truly long term in nature and will require patience to reap the full potential benefit. With that said, evergreen funds (interval and tender offer funds) do offer more flexible liquidity features, which may provide some level of comfort that investors can redeem if necessary.

Conclusion

The bottom line is there is a potential illiquidity premium for allocating capital to private markets. The illiquidity premium is the reward for giving the fund manager ample time to execute their strategy and unlock value. There is an opportunity cost for being too liquid, especially in today’s market environment.

Advisors should help investors in determining their illiquidity bucket. The illiquidity bucket should be determined based on each investor’s ability to allocate capital for an extended period of time (7–10 years). An illiquidity bucket can help instill a long-term disciplined approach that can remove the impulses to respond to emotional stimuli.

Definitions

Accredited investors are individuals with gross income of $200,000, or with joint income with a spouse or partner of $300,000 or more, in each of the two most recent years.

Bloomberg US Aggregate Bond Index is an unmanaged index that reflects the performance of the investment-grade universe of bonds issued in the United States, including US Treasury, government sponsored, mortgage and corporate securities.

Capital calls are mandatory demands made on an ad hoc basis by private investment vehicles for additional capital from investors to support the original investment.

Closed-end funds are a type of investment company created by the Investment Act of 1940 in which money is pooled for deployment in a specific set of assets. Many closed-end funds raise capital at their inception and issue shares to investors which can be traded on public exchanges.

CPI (Consumer Price Inflation) is a measure of inflation calculated by the US Bureau of Labor Statistics based on price changes for a hypothetical basket of goods and services.

Distribution rate expresses the income and capital distributed to investors as a percentage of the total investment capitalization.

Family offices are private financial advisors employed by very wealthy families or individuals to provide customized planning and investment management services tailored to their specific needs.

40-Act funds are investment vehicles authorized by the Investment Company Act of 1940, including open-end mutual funds, exchange-traded funds, closed- end funds, and unit investment trusts.

FTSE NAREIT All Equity REITs Index is an unmanaged index of public US equity REITs that reflects the performance of the public REIT market overall.

K-1 is a US tax return schedule used to report an investor’s share of the profits and losses from a business partnership.

NCREIF property index (NPI) is an unmanaged index of institutional property investments that reflects the performance of the real estate market in general.

NFI-ODCE (NCREIF Fund Index—Open End Diversified Core Equity) is an unmanaged index of open-end commercial real estate funds that reflects the performance of investment real estate in general.

Private real estate is an asset class composed of pooled private and public investments in the property markets which are not traded publicly.

Qualified purchasers are individuals or family-owned businesses with $5 million or more in investments, or which invest $25 million or more for others, such as a professional investment manager.

A REIT (Real Estate Investment Trust) is a specialized type of company designed to own and/or invest in real estate properties which required by law to distribute at least 90% of its taxable income to shareholders.

Shares in public REITs are tradable on public exchanges; non-traded REITs are privately held and may be very illiquid.

S&P 500 is an unmanaged index of 500 US stocks that reflects the performance of large-cap US stocks in general.

Standard deviation is a statistical measure of the variation from the average (mean) in a set of data commonly used to assess the volatility of investment returns over a given time period.

Yield to worst (YTW) is the lowest potential yield that can be received on a bond without the issuer actually defaulting.

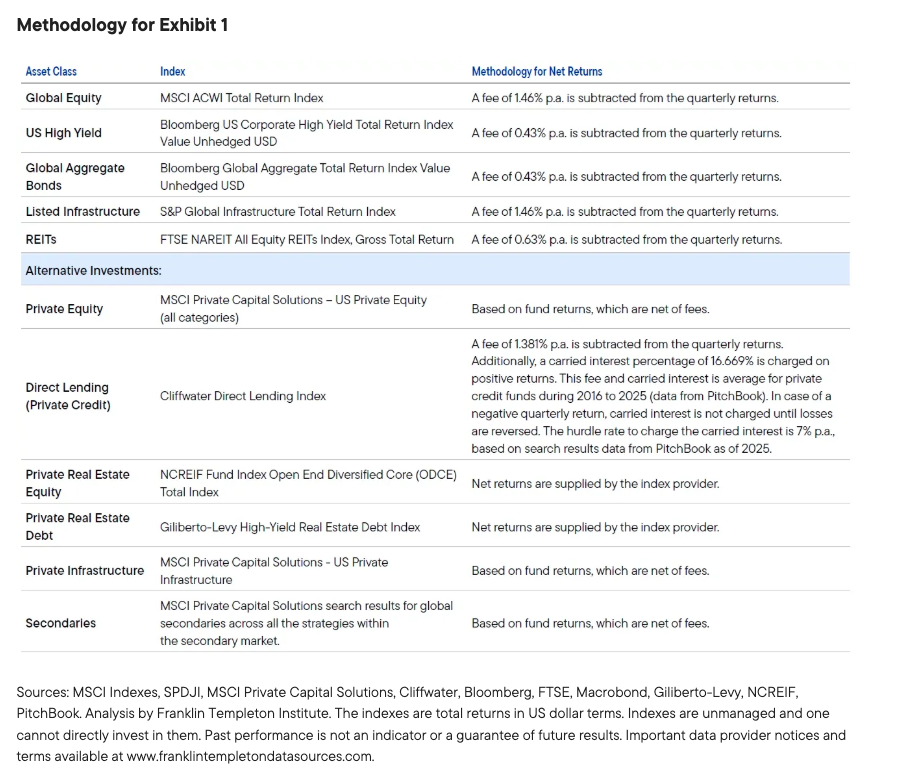

Sources: MSCI Indexes, SPDJI, MSCI Private Capital Solutions, Cliffwater, Bloomberg, FTSE, Macrobond, Giliberto-Levy, NCREIF, PitchBook. Analysis by Franklin Templeton Institute. The indexes are total returns in US dollar terms. Indexes are unmanaged and one cannot directly invest in them. Past performance is not an indicator or a guarantee of future results. Important data provider notices and terms available at www.franklintempletondatasources.com.

“Cliffwater,” “Cliffwater Direct Lending Index,” and “CDLI” are trademarks of Cliffwater LLC. The Cliffwater Direct Lending Indexes (the “Indexes”) and all information on the performance or characteristics thereof (“Index Data”) are owned exclusively by Cliffwater LLC, and are referenced herein under license. Neither Cliffwater nor any of its affiliates sponsor or endorse, or are affiliated with or otherwise connected to, Franklin Templeton Companies LLC, or any of its products or services. All Index Data is provided for informational purposes only, on an “as available” basis, without any warranty of any kind, whether express or implied. Cliffwater and its affiliates do not accept any liability whatsoever for any errors or omissions in the Indexes or Index Data, or arising from any use of the Indexes or Index Data, and no third party may rely on any Indexes or Index Data referenced in this report. No further distribution of Index Data is permitted without the express written consent of Cliffwater. Any reference to or use of the Index or Index Data is subject to the further notices and disclaimers set forth from time to time on Cliffwater’s website at https://www.cliffwaterdirectlendingindex.com/disclosures.

Endnotes

1Source: David F. Swensen, “Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment.” 2009.

2Source: Yale University. FY 2025 Financial Report.

3Source: “The Iliquidity Premium and the Market for Private Assets. Portfolio for the Future.” CAIA.

4As of May 12, 2026. Sources: SPDJI, Bloomberg, Macrobond. Analysis by Franklin Templeton Institute. Index used: S&P 500 Index. Notes: The return expressed is the Compounded Annual Growth Rate (CAGR) in USD over the period Jan 1928 to May 2026 for the S&P 500 Index. Returns have been calculated assuming dividend reinvestment and monthly average prices of the S&P 500 Index. Returns are for i lustration only and exclude fees, expenses, and taxes. Indexes are unmanaged and one cannot directly invest in them. Past performance is not an indicator or a guarantee of future results. Important data provider notices and terms available at www.franklintempletondatasources.com.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Investments in many alternative investment strategies are complex and speculative, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative strategies may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity. Diversification does not guarantee a profit or protect against a loss.

Risks of investing in real estate investments include but are not limited to fluctuations in lease occupancy rates and operating expenses, variations in rental schedules, which in turn may be adversely affected by local, state, national or international economic conditions. Such conditions may be impacted by the supply and demand for real estate properties, zoning laws, rent control laws, real property taxes, the availability and costs of financing, and environmental laws. Furthermore, investments in real estate are also impacted by market disruptions caused by regional concerns, political upheaval, sovereign debt crises, and uninsured losses (generally from catastrophic events such as earthquakes, floods and wars). Investments in real estate related securities, such as asset-backed or mortgage-backed securities are subject to prepayment and extension risks.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks, and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Equity securities are subject to price fluctuation and possible loss of principal.

An investment in private securities (such as private equity or private credit) or vehicles which invest in them, should be viewed as illiquid and may require a long-term commitment with no certainty of return. The value of and return on such investments will vary due to, among other things, changes in market rates of interest, general economic conditions, economic conditions in particular industries, the condition of financial markets and the financial condition of the issuers of the investments. There also can be no assurance that companies will list their securities on a securities exchange, as such, the lack of an established, liquid secondary market for some investments may have an adverse effect on the market value of those investments and on an investor’s ability to dispose of them at a favorable time or price. Past performance does not guarantee future results

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All