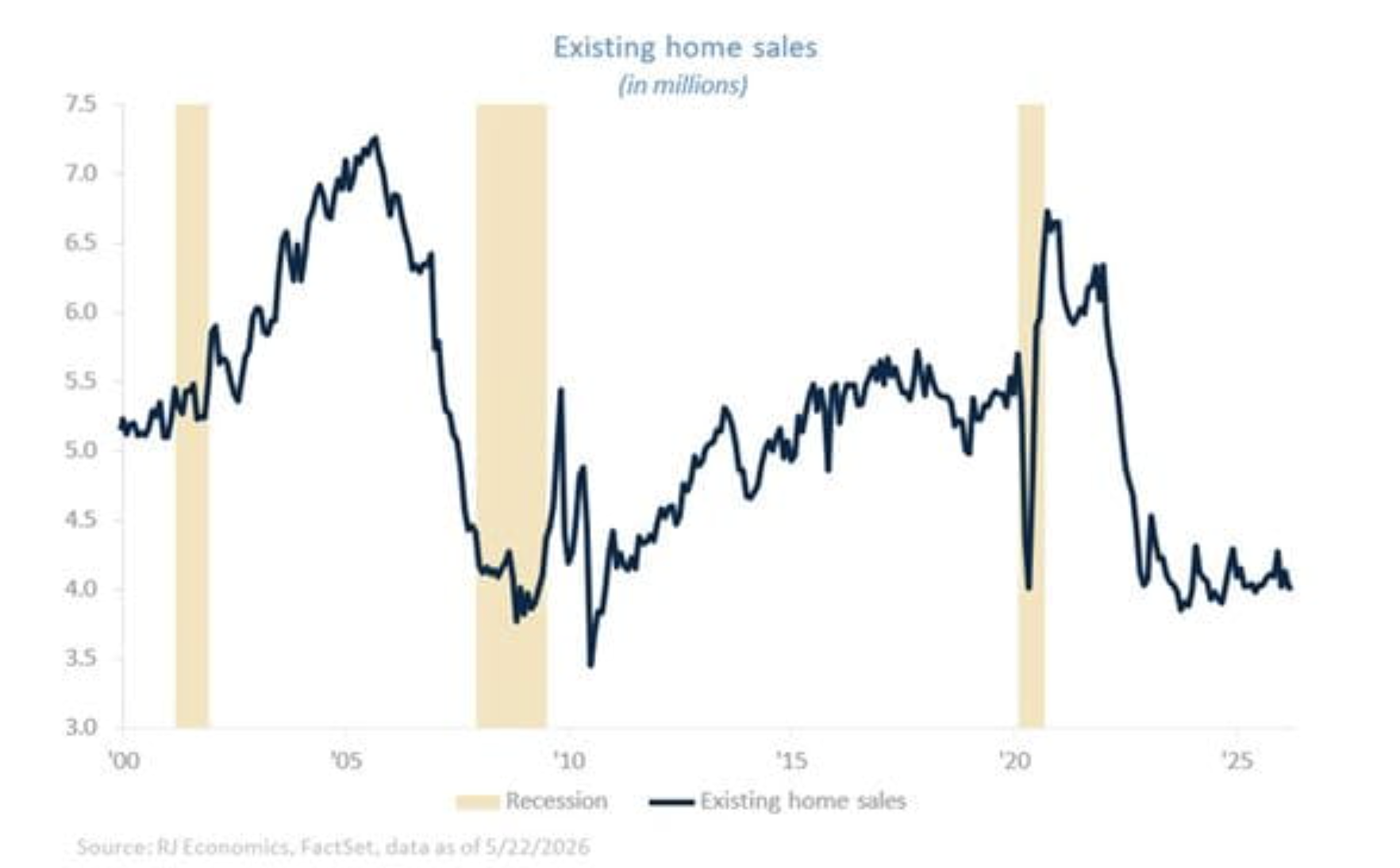

After a slowdown earlier in the year, stronger April and May data support the view that weakness in January and February, followed by a rebound in March, was largely weather-related rather than the start of a broader deterioration in housing demand. Existing home sales rose 0.2% in April, helped by a 0.5% increase in the South, the country’s largest housing region. Even so, existing home sales remain at a seasonally adjusted annual rate of just 4.02 million units, essentially unchanged from a year ago and still hovering near the lowest levels seen since the Great Financial Crisis, excluding the temporary collapse during the onset of COVID-19 in March 2020.

Despite sluggish transaction activity, national home prices have remained surprisingly resilient. The National Association of Realtors (NAR) reported that the median existing home price reached $417,700 in April, up 0.9% year-over-year and marking the 34th consecutive month of annual price appreciation. Inventory has improved modestly, rising to 1.47 million units, or 4.4 months of supply, but that still leaves the market well short of the excess inventory conditions needed for a broad-based price correction. For comparison, during the housing crash of 2008 to 2009, months’ supply was roughly double current levels, which helps explain why today’s market feels stagnant rather than distressed.

Mortgage rates continue to freeze the market

The mortgage rate environment remains the single largest constraint on housing activity. The 30-year fixed mortgage rate remains elevated around 6.51%, only modestly below levels from a year ago and still dramatically higher than the sub-3% rates seen prior to 2022. Fannie Mae’s May forecast projects the 30-year fixed mortgage rate to average 6.3% in 2026 and 6.2% in 2027.

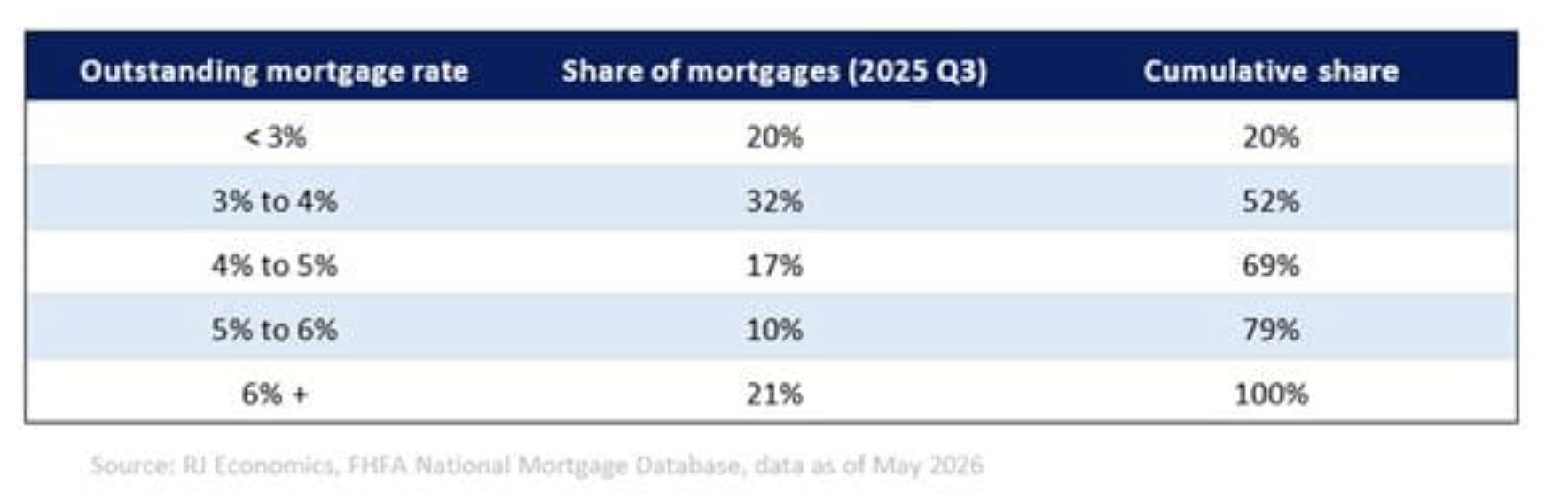

In our view, that would not materially change housing activity, and a sustained move below 6% would likely be needed to meaningfully unlock demand and encourage existing homeowners to list their properties. According to a National Mortgage Professional analysis, roughly 80% of outstanding mortgages currently carry rates of 6% or lower, meaning millions of homeowners remain financially “locked in.”

For many households, selling a home with a 3% mortgage only to purchase another at 6% or higher simply does not make economic sense, particularly given elevated home prices and insurance costs. This lock-in effect continues to suppress resale inventory and is one of the primary reasons the market remains undersupplied despite weak transaction volumes.

Builders face constraints despite stable demand

Builder sentiment reflects this same cautious environment. The NAHB/Wells Fargo Housing Market Index rose three points in May to 37, but any reading below 50 still signals that more builders view conditions as poor. Homebuilders are increasingly relying on incentives to move inventory: 32% reported cutting prices in May, while 61% offered some form of sales incentive, including mortgage-rate buydowns.

This is not a builder recession, but it is far from a confident expansion. Builders retain some competitive advantages over existing homeowners because they can subsidize financing costs and offer incentives directly to buyers. However, their ability to significantly expand supply remains constrained by several structural factors, including elevated financing costs, higher material prices, labor shortages and immigration-related workforce challenges.

Demand is weak, but not dead

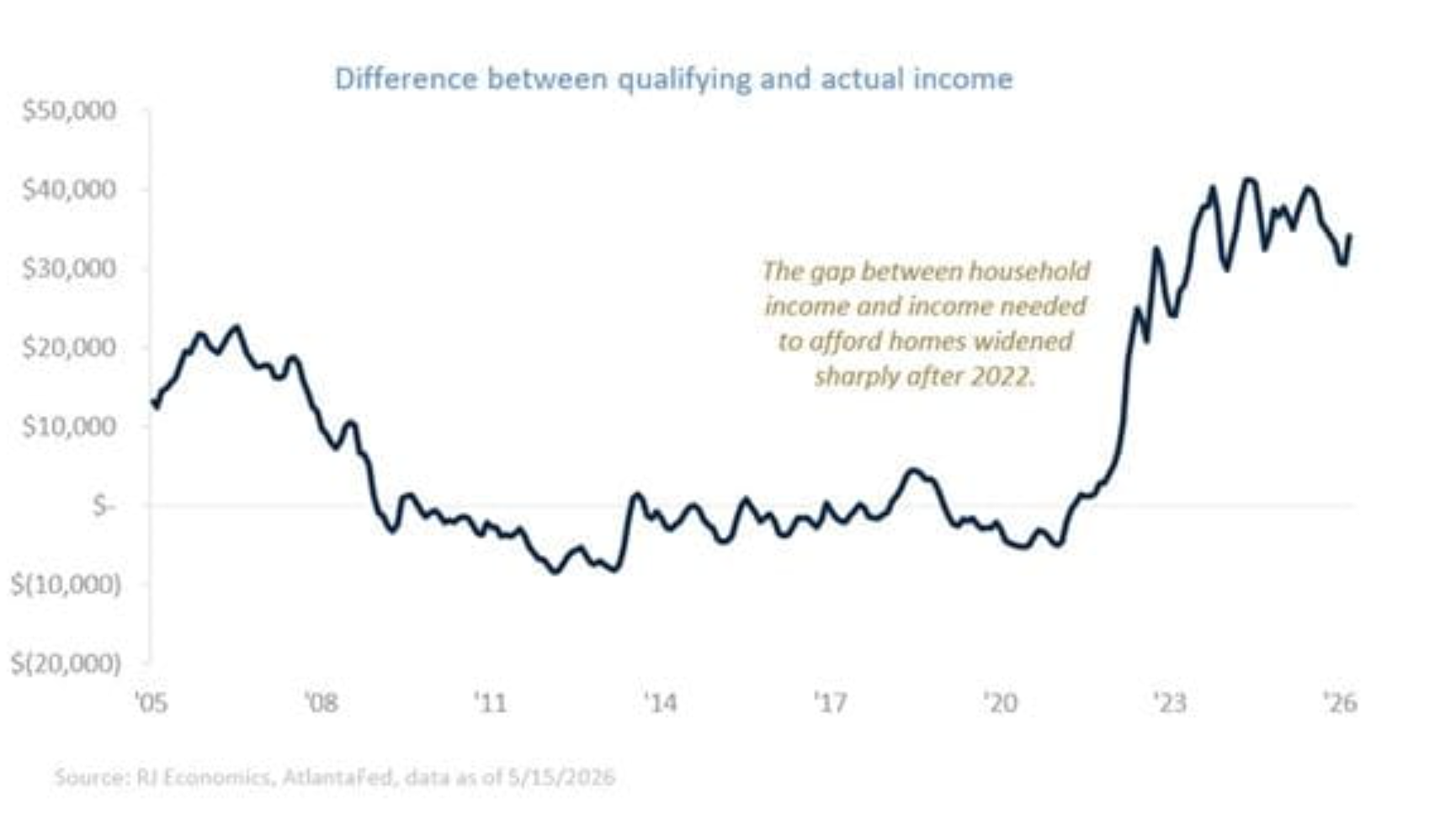

On the demand side, housing activity remains surprisingly resilient given affordability conditions. Pending home sales, a leading indicator for future closings, rose 1.4% month over month and 3.2% year over year in April, according to NAR. The data suggests buyers are still active, though highly selective and extremely payment sensitive. Affordability pressures extend well beyond mortgage rates. Home prices remain significantly higher than pre-pandemic levels, while property taxes, insurance premiums, HOA fees and maintenance costs continue to rise. In many states, buyers of existing homes may also face materially higher property-tax bills than the prior owner because a sale can reset capped assessed values or remove owner-specific tax exemptions. This issue is particularly relevant in states such as Florida and California and further contributes to affordability challenges for move-up buyers. As a result, the market today is best characterized as constrained rather than collapsing. Demand exists, but many buyers are either priced out, unwilling to stretch budgets at current rates or waiting for better financing conditions.

Outlook: a sluggish market, not a housing crash

Overall, the key risk to the housing outlook remains interest rates. If mortgage rates move sustainably toward 6% or below, housing activity could improve meaningfully as affordability pressures ease and more homeowners become willing to sell. However, if inflation keeps mortgage rates closer to 6.5%, the market will likely remain stuck in low gear. Our base case is that rates remain largely unchanged over the next year. Even if the Federal Reserve were to begin lowering short-term interest rates toward the end of 2026, mortgage rates would likely remain at or above 6%, limiting any significant recovery in housing activity. Combined with tight and uneven supply conditions, this environment continues to point toward a sluggish housing market in 2026. The housing market today is neither fundamentally broken nor meaningfully healthy. Instead, it remains frozen between sellers unwilling to give up low mortgage rates and buyers struggling to absorb today’s financing costs. Until rates move decisively lower or supply increases materially, housing activity is likely to remain subdued.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website's users and/or members.

Raymond James & Associates, Inc., member New York Stock Exchange / SIPC, and Raymond James Financial Services, Inc., member FINRA / SIPC, are subsidiaries of Raymond James Financial, Inc.

Raymond James® and Raymond James Financial® and power of personal® are registered trademarks of Raymond James Financial, Inc.

Raymond James & Associates Statement of Financial Condition – March 2026 (PDF)

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Raymond James

Read more commentaries by Raymond James