45 Million Americans Hit the Road This Weekend Despite $4.50 Gas

Membership required

Membership is now required to use this feature. To learn more:

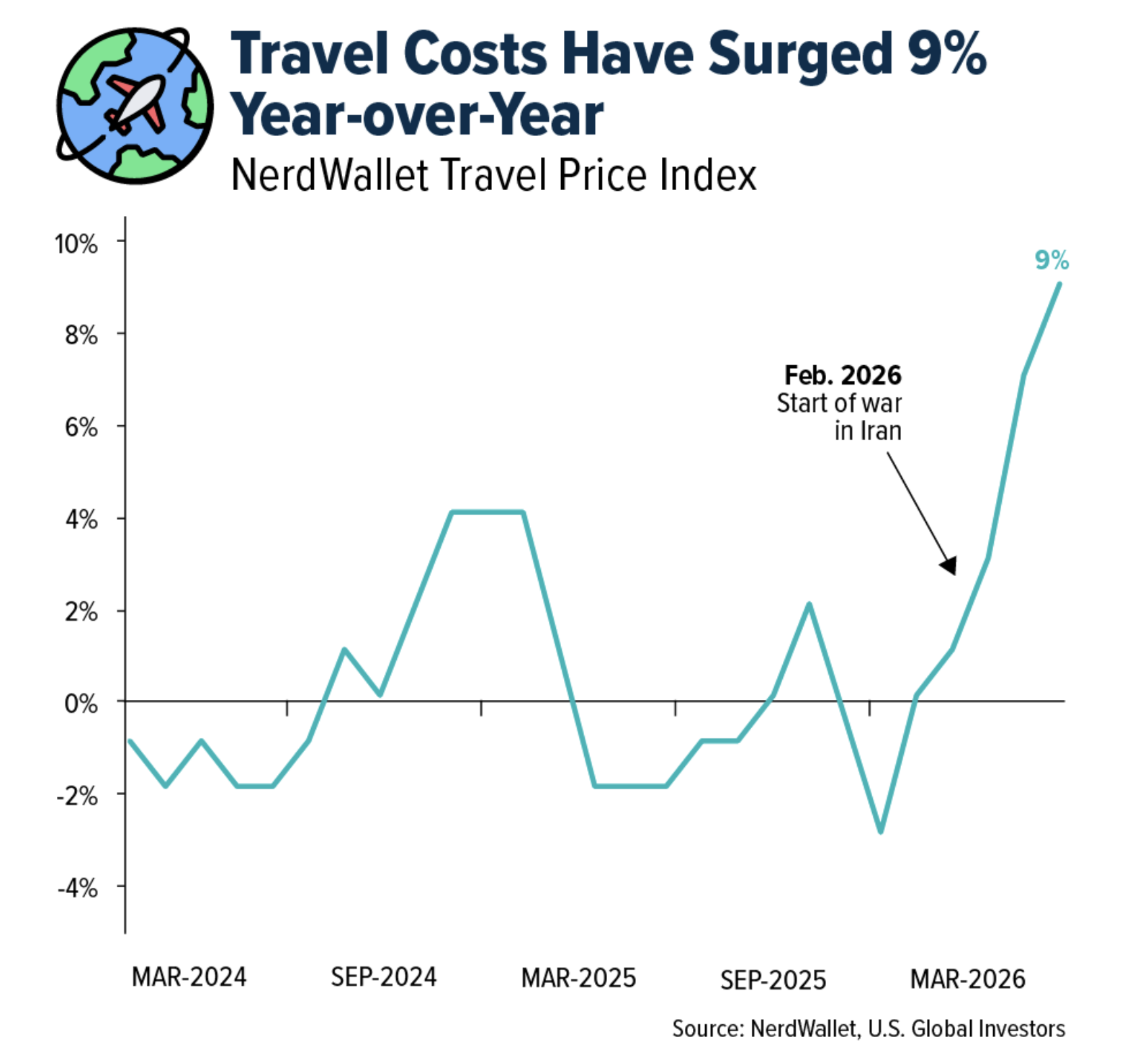

View Membership BenefitsWith the busy Memorial Day travel weekend upon us, the average price of gas in the U.S. is approaching $4.50 per gallon, a four-year high. Travel costs in general—including flights, lodging, food, car rentals and more—have increased 9% year-over-year, according to NerdWallet’s proprietary index based on Bureau of Labor Statistics data.

Despite these higher costs, a projected 45 million Americans are expected to travel at least 50 miles from home this weekend, setting a new record. Close to 40 million will drive while some 3.7 million will fly.

Bank of America’s summer survey found that 77% of Americans are planning to travel this summer, up from 74% last year and 72% in 2024.

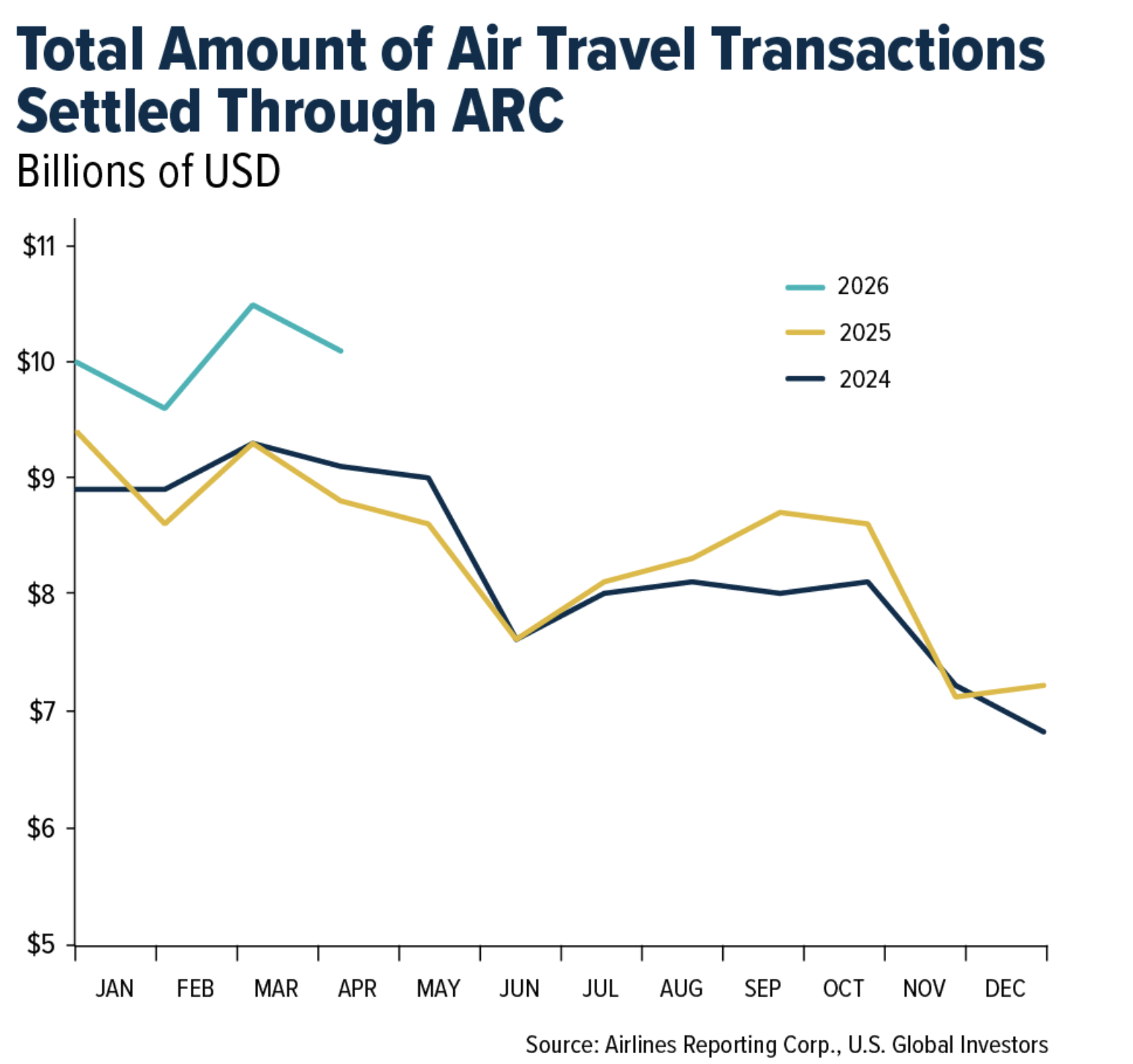

Meanwhile, data from Airlines Reporting Corporation (ARC), which settles airline ticket transactions, shows that April travel agency ticket sales topped $10 billion, a 15% increase from the same month last year. Total passenger trips settled through ARC hit 26.4 million.

Those are more than domestic numbers. The International Air Transport Association (IATA) reported that Asia-Pacific carriers posted an 11.5% jump in demand in March, while European carriers grew 7.7% and Latin Americans airlines surged 12.1%. Traffic between Europe and Asia alone skyrocketed more than 29% as travelers rerouted around the conflict in Iran.

The TSA, meanwhile, is gearing up to screen 18.3 million passengers in the week ahead. And that’s before the FIFA World Cup kicks off on June 11, an event expected to draw some 6 million visitors.

Read more: The Game Theory Behind Taiwan

Cruise Lines Are Effectively Sold Out

I want to mention the cruise industry because the momentum there is extraordinary. According to the Cruise Lines International Association (CLIA), global cruise passengers hit a historic 37.2 million last year, and the projection for this year is 38.3 million, an increase of 4%. Nearly 90% of cruisers say they plan to sail again.

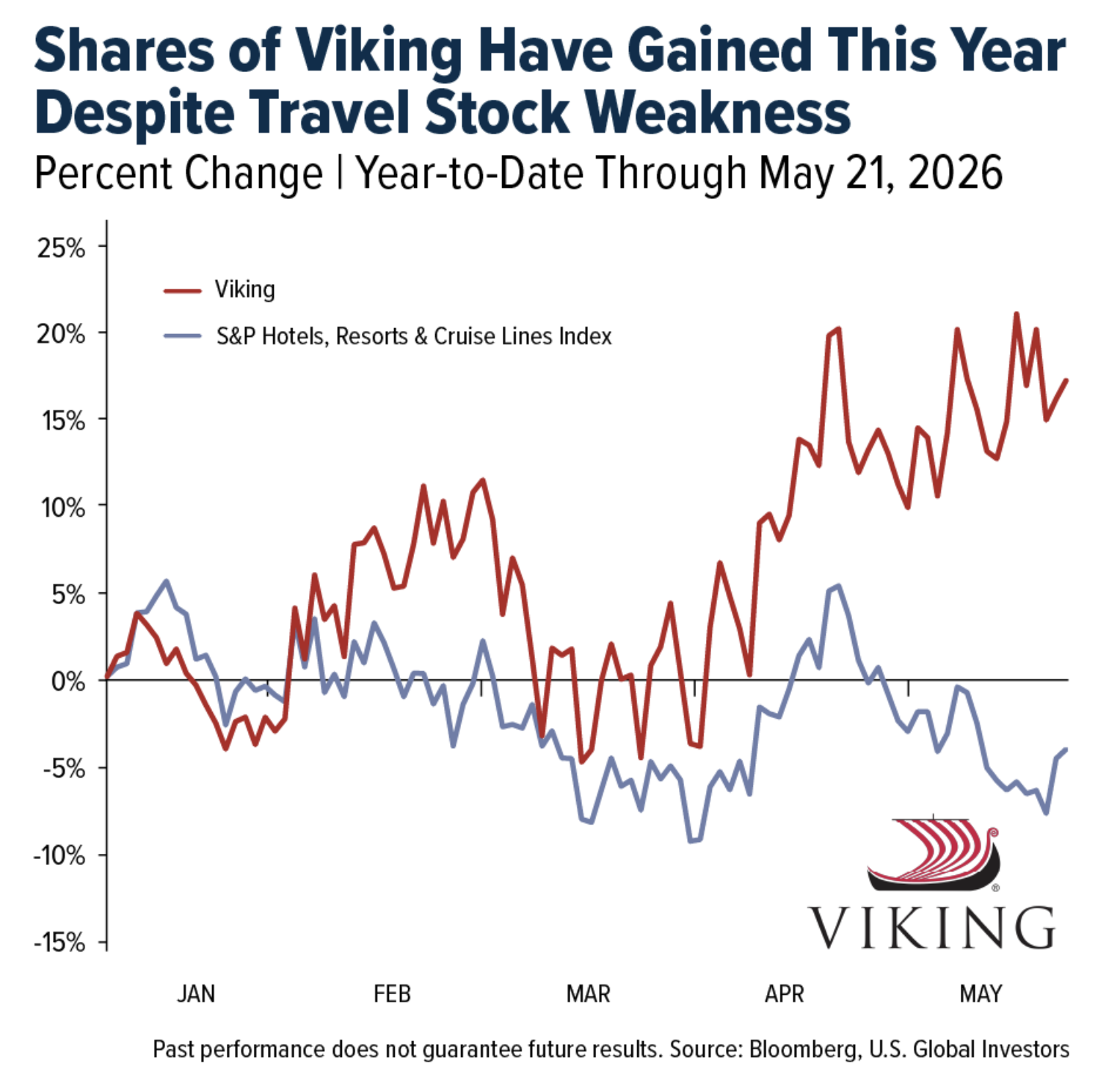

Viking is a good case study. The Switzerland-based company reported first-quarter revenue of $1.05 billion, up 17.5% from the same period last year. Its 2026 sailings are 92% booked. Effectively, it’s sold out. And 2027 is already 31% ahead of last year in advanced bookings.

We’ve been very pleased with Viking’s performance this year. Amid weakness in the broader leisure travel industry due to higher fuel costs, shares of Viking have gained more than 17% as of May 21.

What I find remarkable is that demand persists despite the hantavirus and Ebola headlines that would have torpedoed bookings just a few years ago. The Associated Press recently reported that outbreaks on cruise ships are making news, but they’re unlikely to slow the industry’s growth. Indeed, Bank of America’s survey found that over a third of Americans plan to take a cruise in the next 12 months, with Gen Z leading at 57%.

Your Health on Travel

I’ve always believed that travel is one of the best investments you can make… and not just financially, but in your own health and well-being.

A recent study found that each additional vacation a person takes reduces their risk for metabolic syndrome—high blood pressure, blood sugar and cholesterol levels—by nearly a quarter. Participants who vacationed more frequently had a lower risk of contracting heart disease and diabetes.

When you combine this science with data showing that younger Americans are prioritizing travel, you get a demand profile that looks far more resilient than traditional consumer spending. PwC’s summer spending survey found that close to half of Gen Z and 43% of millennials are planning Memorial Day trips, far outpacing other generations. On average, Americans expect to spend more than $2,800 on travel this summer.

The Headwinds Are Real

I’m not dismissing the challenges. GasBuddy is forecasting a national average of $4.48 a gallon Memorial Day, up sharply from $3.13 just a year ago, with the possibility of all-time records if the Strait of Hormuz remains closed for an extended period. That’s already shifting consumer behavior: the share of Americans planning a road trip of two or more hours dropped from nearly 70% to 56%.

Hotel rates are climbing too. HotelHub data shows the global average rate per night rose over 7% to $189, with U.S. rates hitting $226. Bookings to the U.S. from abroad dropped nearly 12%.

Sadly, the hotel industry’s own outlook on the FIFA World Cup is cautious, with roughly 80% of respondents in one survey saying bookings are tracking below expectations, partly due to visa barriers and geopolitical concerns.

The Rise of Digital Nomads

Consumers don’t appear to be canceling plans, though.

Instead, the lines separating work and leisure travel are beginning to blur. The Deloitte summer travel survey found that a third of travelers plan to work during their longest trip, up from 23% last year. Mastercard reports that 81% of business travelers have extended an international work trip for personal reasons.

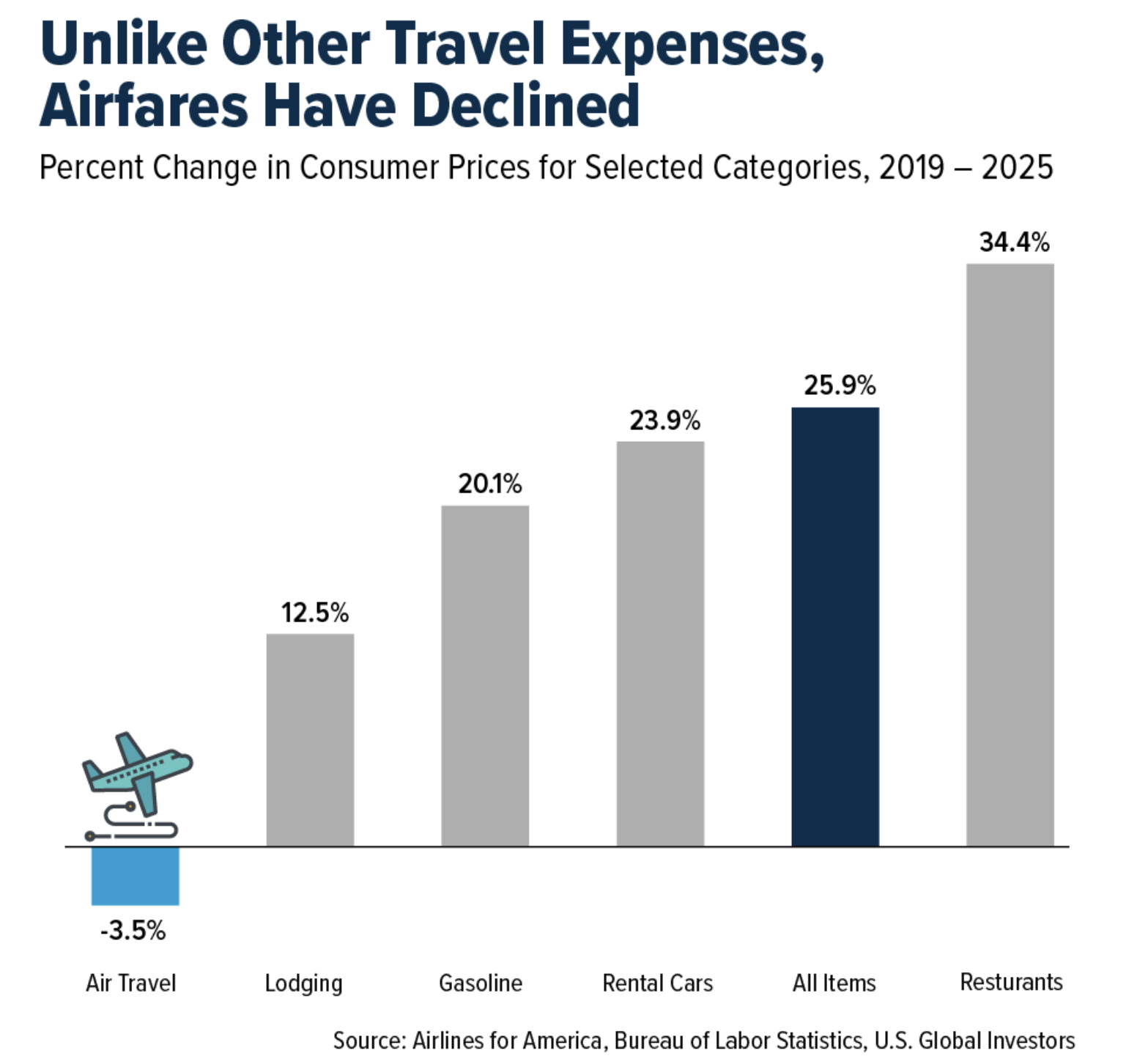

The Airlines for America data reinforces this adaptability. While the consumer price index (CPI) for airline fares actually fell 3.5% from 2019 to 2025 in real terms, low-cost carriers like Breeze, Frontier and JetBlue are aggressively adding capacity in markets vacated by Spirit Airlines, keeping competitive pressure on pricing even as demand grows.

The Investment Case Write Itself

Right now, airlines, cruise operators and travel-adjacent companies are operating in an environment where consumers are telling us, through their wallets, that they will pay more, adapt their plans and blend their work with their vacations before they’ll give up the trip entirely.

Both the tailwinds (infrastructure investment, America 250 celebrations, FIFA) and the headwinds (visa restrictions, energy costs, geopolitics) are shaping a travel landscape that rewards companies with scale and pricing discipline.

Americans—and, increasingly, travelers worldwide—are voting with their feet. Smart investors should pay attention.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was American Airlines, up 13.4%. According to Morgan Stanley, strong ANA Holdings Inc. results were driven by: (1) approximately ¥10.0 billion of special demand related to the Middle East; (2) stronger-than-expected passenger demand on both domestic and international routes; (3) firm air cargo pricing; (4) no visible signs of deterioration in passenger demand based on current forward-booking trends; and (5) international fuel surcharges.

- UBS notes continued rate increases for departures over the next seven days, following last week’s 10% increase in shipping rates. Current futures rates for July and August stand 50% to 60% above the latest shipping-rate levels.

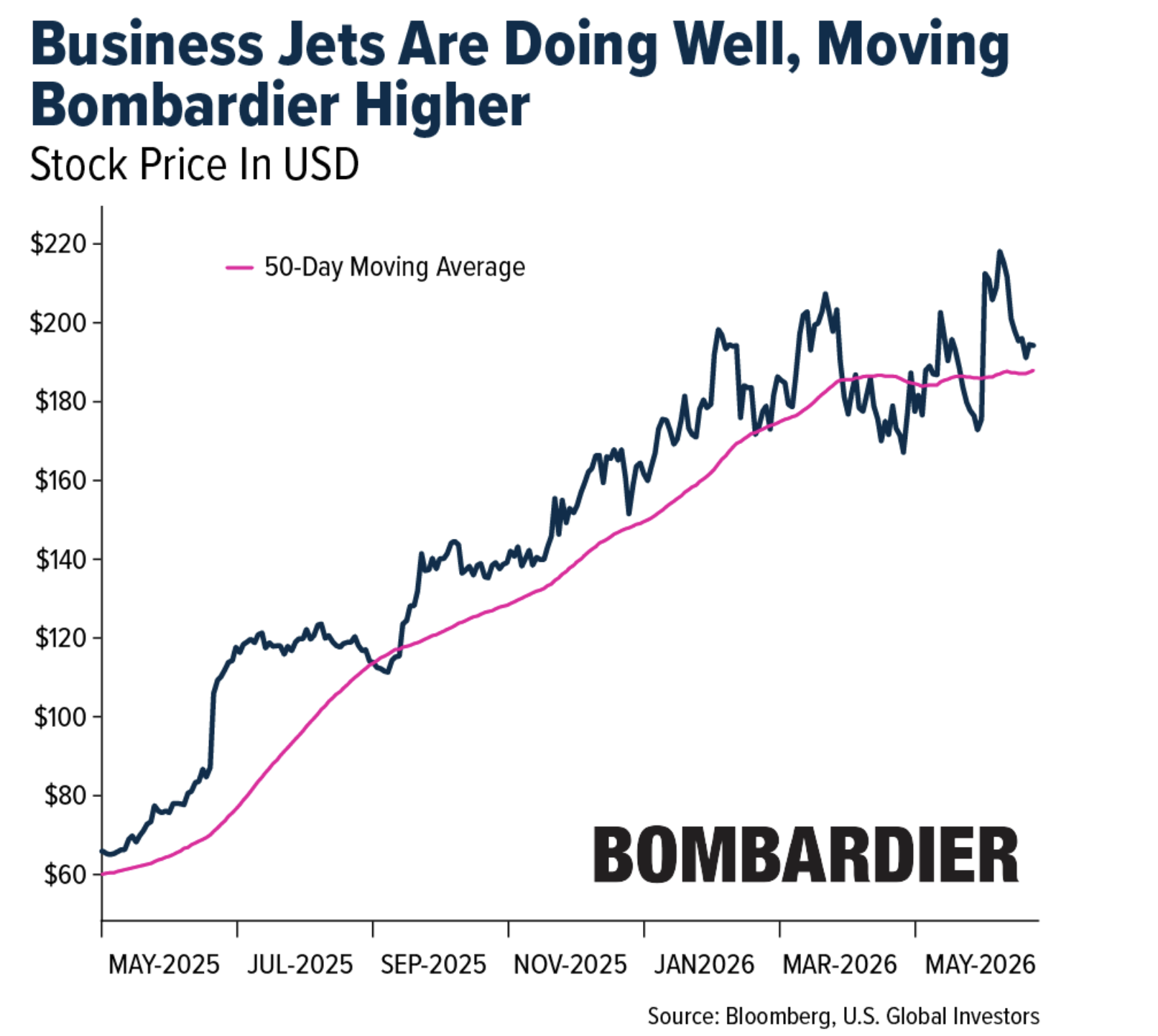

- According to RBC, Bombardier management noted that conditions across the business aviation market are materially exceeding original expectations, consistent with the record backlog the company saw in the first quarter. The depth of buyer appetite is perhaps best illustrated by the fact that used Bombardier jets under 10 years old are attracting multiple offers. Flight-hour utilization is running approximately 6% to 8% above prior-year levels, while used aircraft inventory has trended to all-time lows, dynamics that continue to tighten pricing conditions across the platform.

Weaknesses

- The worst-performing airline stock for the week was Tongcheng Travel, down 10.9%. Japan inbound demand fell to 3.74 million visitors, down 3.2% year-over-year, marking the first drop since January 2022. By region, China was down 48% YOY, while the U.S. and Europe turned negative, according to Morgan Stanley.

- Yangzijiang Shipbuilding released a business update and reported total new order wins year-to-date of $1.03 billion, representing 23% of management’s fiscal year 2026 target of $4.5 billion. Second-quarter-to-date new order wins totaled $0.03 billion per month, materially slowing from the monthly averages of $0.21 billion in 2025 and $0.33 billion in the first quarter of 2026, according to Goldman Sachs.

- After a disappointing Labor Day holiday in China, the number of domestic flights was cut further, down 7% YOY. Although demand was largely maintained, with ex-fuel ticket prices up 5.3% YOY and load factor at 84%, demand in the second half of May is likely to face greater pressure given further fuel-surcharge increases, according to Bank of America.

Opportunities

- Price is still the most important consideration for airline travel, with 77% of respondents citing price as the key factor when purchasing airline tickets for leisure purposes. Destination (55%) and airline brand (49%) were also important elements. Airline brand was meaningfully more important than three years ago, up 600 basis points (bps), as was seat class, up 900 bps versus three years ago, according to UBS.

- ZIM management is more optimistic about full-year unit profit improvement. A positive feedback loop has resumed: market share gains, followed by better pricing power and a more efficient cost structure versus peers, leading to better-than-expected unit profitability and earnings growth, according to Morgan Stanley.

- The Federal Aviation Administration (FAA) announced a new air traffic controller workforce plan to address longstanding staffing shortages, promote high safety standards and prepare for future demand by improving the operational efficiency of the National Airspace System (NAS). The FAA’s 2026 Air Traffic Controller Workforce Plan is based on three pillars: improving its robust hiring process, optimizing controller efficiency and modernizing the NAS, according to Morgan Stanley.

Threats

- According to Flight Master, a 20% YOY increase in domestic China airfares weighed on demand, driving a 9% decline in passenger traffic last week, worse than the prior week. Overall, domestic passenger revenue grew 9% YOY, slower than the previous week.

- This past week, laden vessels from China to the USA were down sequentially, falling 3.5% week-over-week (WoW), and slowed on a YOY basis, rising 9% YOY. Data suggests containers coming into the Port of Los Angeles will turn negative next week, down 14%, according to Goldman Sachs.

- According to JPMorgan, Brazilian airlines are cutting flights, with a reduction of 93 daily flights in May, a 4.3% decrease representing a loss of 14,000 seats per day. Aviation fuel has doubled in price since February and accounts for approximately 30% of the sector’s operating costs.

Luxury Goods and International Markets

Strengths

- According to the National Association of Realtors, sales of homes priced above $1 million rose 9.3% year over year in April, while overall home sales remained flat. This highlights continued strength in the luxury segment. Reflecting this trend, Toll Brothers reported strong earnings last quarter, slightly exceeding management’s guidance.

- According to S&P Global, the U.S. Manufacturing Purchasing Managers’ Index (PMI) rose to 55.3 in May 2026, up from 54.5 in April and well above the 50-point threshold that separates expansion from contraction. The latest reading reflects stronger production activity and improving domestic demand.

- Salvatore Ferragamo was the best-performing stock in the S&P Global Luxury Index over the past five days, with shares rising 16.5%. The stock rebounded after a sharp correction last Friday.

Weaknesses

- Year to date, luxury equities continue to lag the broader market. The S&P Global Luxury Index is down almost 20%, while the Standard & Poor’s 500 (S&P 500) Index is up 8%, the STOXX Europe 600 Index is up 4%, and the Shanghai Shenzhen China Securities Index (CSI) 300 Index is roughly flat.

- The eurozone reported a smaller seasonally adjusted trade surplus of €3.5 billion in March, compared with €7.0 billion in the prior month, indicating softer underlying trade momentum. The decline was driven in part by higher import costs, particularly energy, which continued to weigh on the region’s trade balance.

- Li Auto was the worst-performing stock in the S&P Global Luxury Index over the past five days, with shares falling nearly 18.3%. The decline was driven by weaker investor sentiment toward Chinese EV makers amid intensifying price competition.

Opportunities

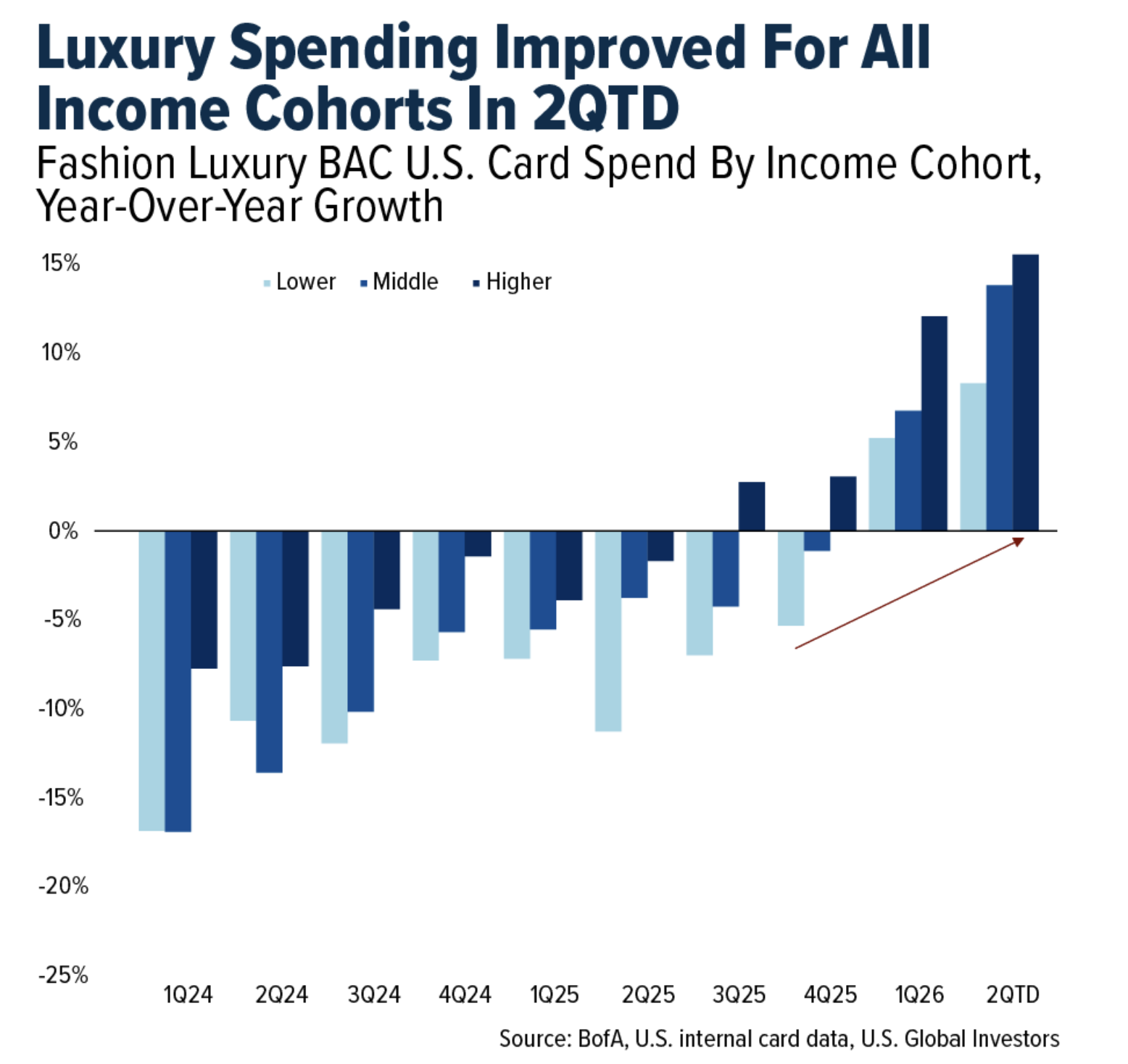

- According to Bank of America (BofA) research, luxury spending has shown a broad-based recovery year to date in 2026, with all income groups contributing to the improvement. High-income consumers continue to lead the trend, with spending growth accelerating to 16% year over year in April, up from 12% in the first quarter of 2026. Meanwhile, middle-income consumers posted the strongest improvement, with spending growth rising 7 percentage points to 14% year over year. Lower-income consumers also increased spending, improving 3 percentage points to 8%.

- After President Donald Trump met with President Xi Jinping in China and agreed that the Strait of Hormuz must remain open without Iranian control, President Vladimir Putin is also visiting China this week to discuss key issues affecting global markets. These high-level meetings among major global powers present an opportunity to address outstanding geopolitical tensions and find common ground, supporting efforts toward greater economic stability and improved global cooperation.

- Luxury stocks remain in oversold territory, having corrected sharply in March due to rising tensions in the Middle East, higher oil prices, and travel disruptions. A swift resolution of the Middle East conflict and the reopening of the Strait of Hormuz could trigger a rapid rebound in the sector.

Threats

- Bond yields have risen sharply in recent weeks as investors grow increasingly concerned about inflation. Markets are now pricing in a higher probability that the Federal Reserve could raise interest rates again by year-end rather than cut them, marking a significant shift from earlier expectations of multiple rate cuts. Higher Treasury yields increase borrowing costs across mortgages, auto loans, and credit cards, which could pressure consumer spending by reducing disposable income.

- In the U.S., Home Depot reported weaker profits, reflecting broader softness in consumer sentiment rather than weakness in the luxury segment specifically. Chief Financial Officer Richard McPhail noted that homeowners are increasingly delaying or canceling home improvement projects due to economic uncertainty. Consumers remain concerned about rising costs and mortgage rates, which have started moving higher again after declining throughout much of 2025.

- The Bank of America research team lowered its second-quarter growth forecast for the luxury sector by 1% to 3%. The broker noted that demand trends in China appear weaker in the second quarter than in the first quarter, while the Middle East is expected to remain a headwind. In contrast, the U.S. is expected to continue outperforming as the strongest regional market.

Energy and Natural Resources

Strengths

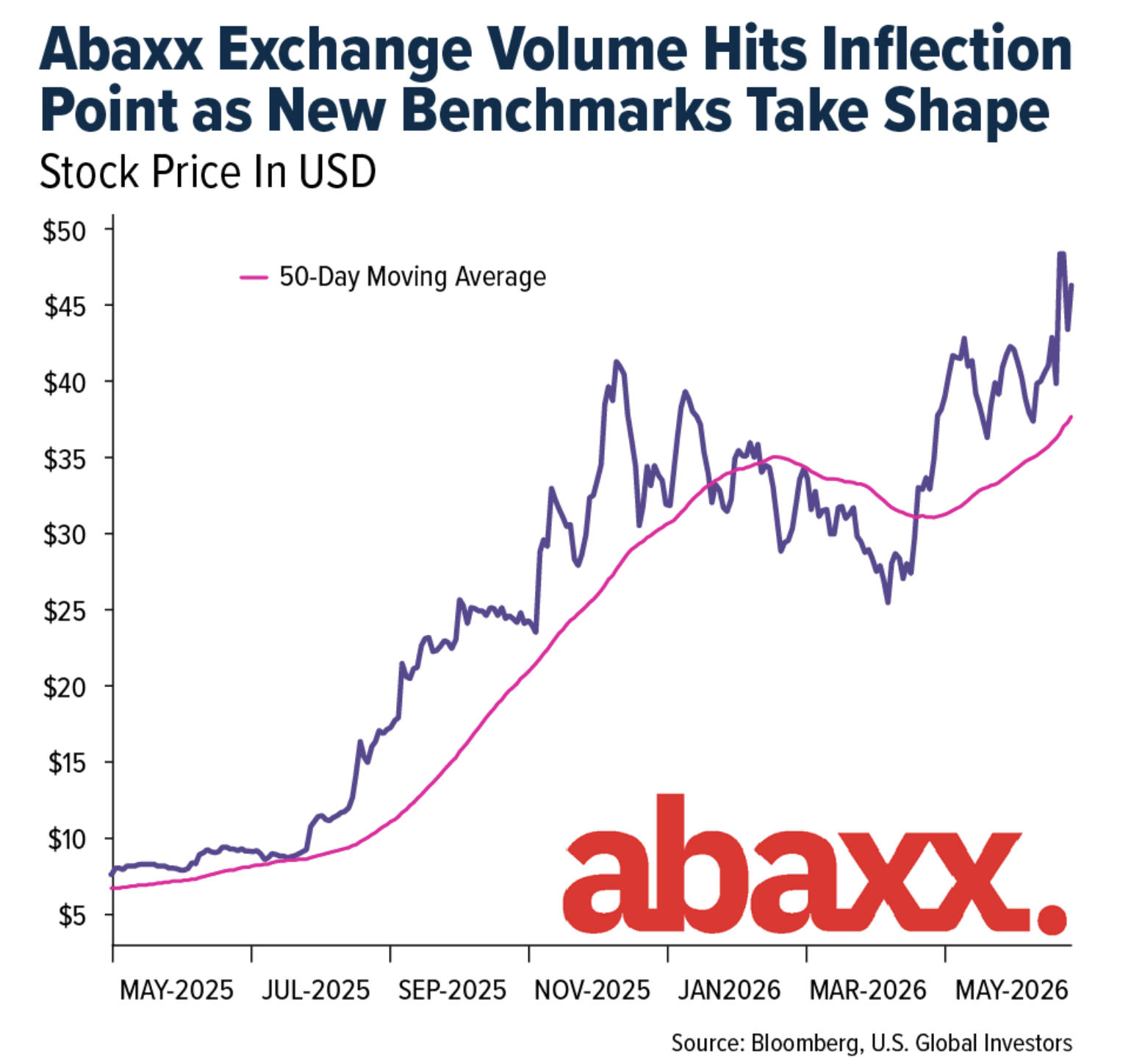

- The best performing commodity for the week was lead, which rose approximately 2.18%. Abaxx Technologies Inc.’s exchange volume surged 145% quarter-over-quarter in Q1 2026 with April alone exceeding the entire quarter’s total, culminating in a single-day record of 50,277 contracts on May 14 — roughly one-third of COMEX gold volume that day. Canaccord raised their price target to C$80.50 on the back of accelerating ADV growth, new product launches in silver and renewables futures, and the company’s uplisting to the TSX.

- NextEra Energy’s announced $66.8 billion all-stock acquisition of Dominion Energy creates a combined entity valued at over $400 billion, strategically merging the nation’s largest renewable energy developer with the operator of Northern Virginia’s electric grid — home to the world’s highest concentration of AI data centers. The deal underscores the thesis that energy infrastructure has become the critical bottleneck for AI expansion, with key metrics to watch including new data center power contracts exceeding 500 MW and transmission utilization rates approaching 90% capacity.

- Copper at $6.67/lb has now pushed 75 mines above $1 billion in annual revenue from copper alone — up 23 from the prior count — underscoring just how dramatically the AI and data center buildout is reshaping mining economics. Despite producing assets with tangible, auditable cash flows, mining still cannot attract the speculative capital that once valued a dog-walking app at $300 million or an NFT marketplace at $13 billion, a disconnect that increasingly looks like an opportunity for investors paying attention to fundamental value.

Weaknesses

- Lithium was the weakest performing commodity of the week, declining approximately 6.07%. Australian lithium miners are restarting mothballed operations as spodumene prices hit two-year highs — Core Lithium resuming blasting at Finniss and Mineral Resources restarting Bald Hill — while traders also weigh China’s announcement of new mining controls on strategic minerals taking effect June 15, which would allow Beijing to cap output and restrict foreign investment in the sector. Prices remain well below the late-2022 record, but the combination of supply restarts, new development plans like the Rinehart-SQM joint venture, and potential Chinese production controls is reshaping the lithium supply picture heading into the second half.

- The virtual blockade of the Strait of Hormuz has removed 28% of global naphtha flows in just three weeks, with the critical Abadan-Yokohama route down 41%, crashing Japanese and South Korean storage capacity from 72% to 41% and forcing Yokohama refineries to cut throughput by 30%. The supply shock is rippling into real manufacturing disruptions including a 35% production cut at Japanese food packaging plants due to plastic packaging shortages.

- Geely becoming the first Chinese automaker to manufacture in Europe — via Ford’s Spanish plant — is a direct response to EU tariff barriers, and the 18-month retooling timeline is the key variable to watch since any slippage beyond 24 months risks meaningful competitive loss in a European EV market growing 30% annually. The deeper signal is that factory reactivation speed is becoming the critical metric for industrial competitiveness — it is no longer about production cost but about how fast legacy ICE infrastructure can be converted into an operational EV asset, a dynamic that could reshape demand patterns for copper, aluminum, and battery metals across the European supply chain.

Opportunities

- Mineral Resources is restarting its Bald Hill lithium mine in Western Australia after an 18-month care-and-maintenance pause, targeting first spodumene concentrate production in July and full capacity in Q2 FY27 — making MinRes the only company globally operating three hard rock lithium mines with dedicated processing facilities. The restart is underpinned by a 50%+ surge in lithium carbonate prices this year driven by supply uncertainty from Chinese mine suspensions and Zimbabwe’s raw mineral export ban.

- The EU has shortlisted tungsten, rare earths, and gallium for its first coordinated critical minerals stockpile, with discussions underway at the Port of Rotterdam for storage, as the bloc moves to reduce reliance on China which supplies 93% of its wind turbine permanent magnets. Ten member states led by Italy, France, and Germany are participating in the initiative, which follows Beijing’s recent export restrictions on strategic minerals and reflects a broader Western shift toward interventionist industrial policy for critical resources.

- Barclays’ 2026 Equity Gilt Study draws a direct parallel between the coming AI infrastructure buildout and the China-led commodity supercycle of the early 2000s, arguing that metals-rich emerging markets — particularly Chile and Peru (copper), Indonesia (nickel), and China (rare earths) — will see rising exports, improving terms of trade, and increased investment as AI-driven demand for electrification, data centers, and robotics feeds through to commodity prices. This is a significant macro call from a major bank that validates the structural demand thesis for copper and battery metals, suggesting the current tightness isn’t cyclical but the early innings of a multi-year AI-driven supercycle.

Threats

- Chile’s state copper commission Cochilco slashed its 2026 production forecast by 300,000 tons to 5.3 million tons, with 2027 cut even more sharply from 5.97 million to 5.5 million tons, citing lower ore grades and operational constraints — a significant supply-side headwind from a country producing nearly a quarter of the world’s mined copper. Cochilco simultaneously raised its average price forecast to $5.55/lb from $4.95/lb, yet copper is already trading above $6/lb in New York, meaning even the upgraded official forecast lags the market by nearly 10%.

- Australia’s government has ordered six major shareholders — five based in China or Hong Kong — to divest their combined roughly 27% stake in rare earths miner Northern Minerals within two weeks, escalating a national security effort that began with a similar 2024 directive. The move reflects broader Western efforts to limit Chinese investment in critical minerals, particularly significant given Beijing’s near-monopoly on rare earth production and Northern Minerals’ undeveloped Browns Range heavy rare earth deposit, which has strategic military and electronics applications.

- U.S. drill bit manufacturers are shifting to steel-based products to cut costs after tungsten prices surged to approximately $3,000/metric ton from around $600/metric ton in October amid trade restrictions, tighter supplies, and stronger military demand. Average-sized PDC drill bits have risen 20% to 38% over the past seven months, and with North American producers expected to ramp up drilling following Middle Eastern oil supply disruptions, higher drill bit and equipment costs are raising the price of new wells and threatening to compress producer margins.

Bitcoin and Digital Assets

Strengths

- Coinbase announced the launch of new perpetual-style futures tied to major equity themes, including artificial intelligence (AI), U.S. national security and Chinese companies listed in the United States. The new products, which will trade under the oversight of the U.S. Commodity Futures Trading Commission (CFTC), include exposure to companies such as NVIDIA, Microsoft, Amazon and Chinese technology firms, including Alibaba Group. The move highlights how crypto exchanges are increasingly expanding beyond digital assets into broader financial markets, offering investors around-the-clock access to thematic trading products tied to some of the world’s most important economic and geopolitical trends.

- London-listed trading platform IG announced plans to expand cryptocurrency trading services across Europe through a partnership with crypto exchange Bitpanda, highlighting the growing integration between traditional finance and digital assets. IG, one of Europe’s largest retail trading platforms with more than 1.3 million global clients, introduced spot crypto trading in the United Kingdom (U.K.) last year and reported that digital assets generated £2.4 million ($3.2 million) in quarterly revenue. The expansion will leverage Bitpanda’s Markets in Crypto-Assets (MiCA)-compliant infrastructure, including liquidity and trading connectivity, reinforcing how clearer regulation in Europe is accelerating institutional participation and mainstream adoption of crypto services.

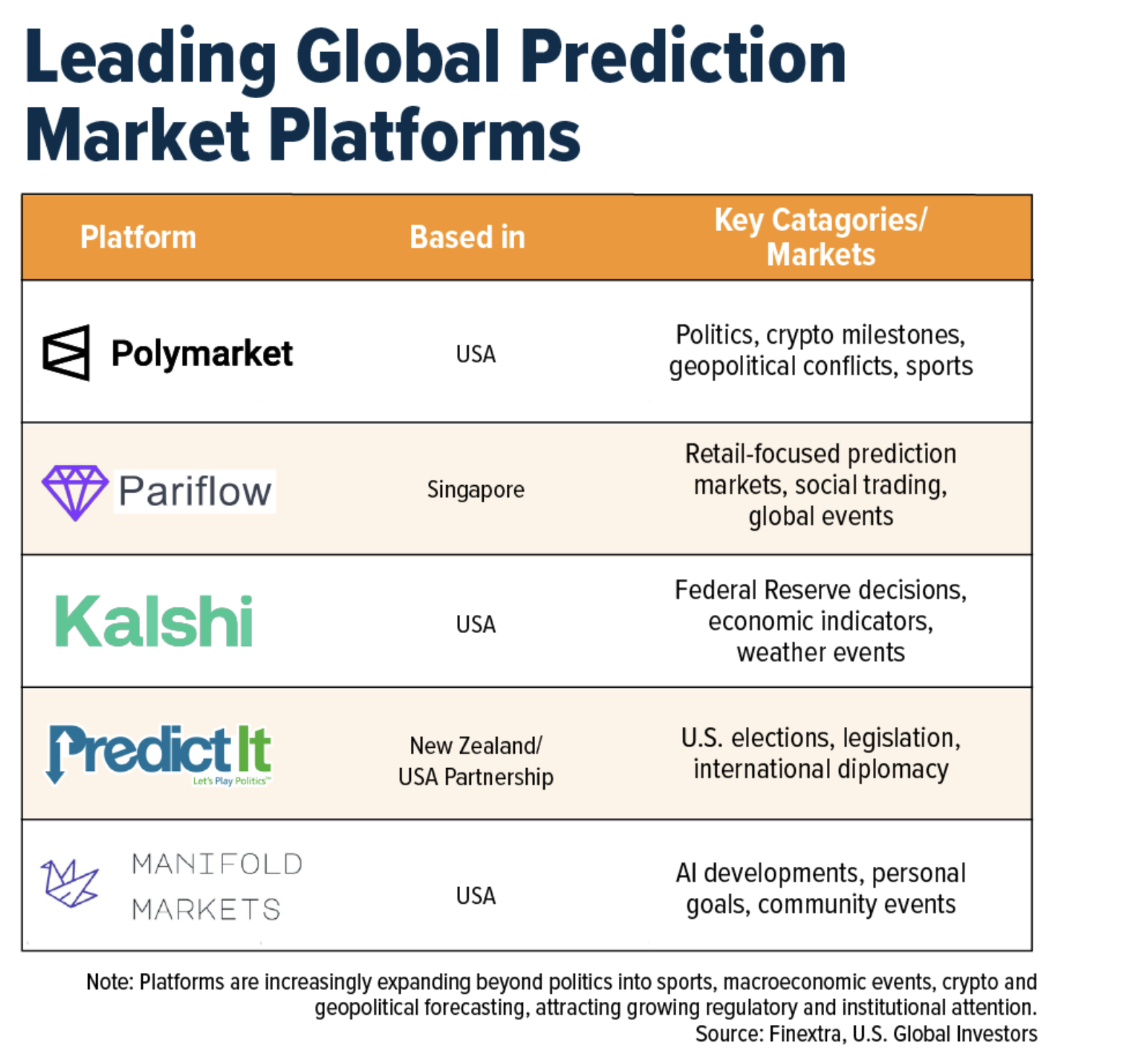

- The CFTC signed a new oversight agreement with the National Hockey League to monitor event contracts tied to professional hockey games, following a similar arrangement recently established with Major League Baseball. The agreement aims to strengthen safeguards against insider trading, fraud and market manipulation as prediction markets continue experiencing rapid growth. The development signals increasing institutional acceptance of regulated event-based trading markets, with the CFTC positioning itself as the primary regulator overseeing the sector rather than seeking outright bans. The collaboration also reflects broader efforts to integrate prediction markets into traditional regulatory and sports governance frameworks while improving market integrity and investor confidence.

Weaknesses

- Despite positive regulatory developments in the U.S., including progress around the Clarity Act, Bitcoin has struggled to attract strong investor interest, remaining near the $77,000 level with little movement over the past week. Instead, markets have been more focused on geopolitical tensions, oil prices near $100, inflation concerns and continued enthusiasm around AI-related stocks. The weaker sentiment toward crypto is also reflected in U.S. spot Bitcoin exchange-traded funds (ETFs), which recorded about $1.15 billion in outflows this week after losing another $1 billion the previous week. The trend suggests that, for now, global macroeconomic and geopolitical narratives are attracting more investor attention and capital than Bitcoin and the broader crypto market.

- Security problems continue to be one of the biggest weaknesses for decentralized finance (DeFi), making many institutional investors question whether the risks are worth the returns. According to JPMorgan, DeFi bridges have already suffered eight major hacks in 2026, with losses totaling more than $328.6 million. Following the recent exploit involving KelpDAO, a DeFi platform focused on generating yield through Ethereum-based restaking strategies, total value locked (TVL) across DeFi fell from nearly $100 billion to around $86 billion in just a few days, showing how quickly investors can pull money out after security incidents. At the same time, DeFi yields are becoming less attractive, with some stablecoin lending rates now below the returns offered by short-term U.S. Treasury bills, reducing one of the sector’s key advantages for investors.

- Trump Media & Technology Group, the parent company of Truth Social, transferred another 2,650 Bitcoin (BTC), worth about $205 million, to Crypto.com as losses tied to its Bitcoin strategy continue increasing. The company purchased more than 11,500 BTC at an average price above $118,000 per coin, leaving it with an estimated unrealized loss of roughly $455 million, with Bitcoin now trading near $77,000. The company also recently withdrew its spot Bitcoin ETF application and reported a quarterly net loss of nearly $406 million on less than $1 million in revenue. The situation highlights how large crypto positions can create significant financial pressure for public companies during periods of market weakness and volatility.

Opportunities

- Onchain derivatives platform Variational raised $50 million in a funding round led by Dragonfly to accelerate the development of perpetual futures tied to real-world assets (RWAs) such as gold, silver, copper and crude oil. The company has already processed more than $200 billion in trading volume since launching in 2025 and plans to expand liquidity infrastructure connecting traditional financial markets with decentralized finance. The move highlights the growing opportunity for RWAs within crypto, as firms increasingly tokenize and bring traditional commodities and financial products onchain. Industry participants believe RWA perpetuals could become one of the largest segments in DeFi, potentially surpassing trading volumes of major cryptocurrencies over time.

- Binance launched perpetual futures tied to SpaceX’s anticipated initial public offering (IPO) valuation, marking another step in crypto’s expansion into traditional financial markets. The new product allows retail traders to gain synthetic exposure to private companies before public listings, an opportunity historically limited to venture capital and institutional investors. Interest has been strong: similar SpaceX pre-IPO contracts on Trade.xyz generated more than $33 million in first-day trading volume, while Polymarket traders assign more than a 70% probability that SpaceX debuts above a $2 trillion valuation. The trend highlights how crypto infrastructure is increasingly being used to democratize access to previously exclusive investment opportunities, potentially driving new trading activity, user growth and institutional relevance for the digital asset ecosystem.

- MoonPay, a crypto infrastructure company known for enabling users and institutions to access digital assets and blockchain-based financial services, announced the launch of MoonPay Trade, a new platform designed to connect banks, financial technology (fintech) companies and enterprises to tokenized assets, decentralized finance protocols and stablecoin liquidity across more than 200 blockchains. The expansion reflects growing institutional demand for blockchain-based financial infrastructure as the tokenized RWA market has already surpassed $33 billion in value, tripling over the past year. Boston Consulting Group projects the sector could reach $18.9 trillion by 2033, while major firms including BlackRock, Franklin Templeton and JPMorgan Chase continue launching tokenized investment products, highlighting the growing convergence between traditional finance and blockchain-based capital markets.

Threats

- U.S. lawmakers are moving to restrict crypto-based prediction markets after investigations uncovered suspicious trading tied to geopolitical events and military operations. Bubblemaps analysts identified 80 Polymarket bets with a 98% win rate, described as statistically impossible, while onchain data revealed that several traders placed high-conviction wagers ahead of U.S. actions involving Iran, generating more than $2.4 million in profits. The controversy has intensified calls for regulation, with members of Congress introducing the “DEATH BETS Act” to ban war-related contracts. The situation highlights mounting concerns that prediction markets could be exploited for insider trading, misinformation campaigns or even national security manipulation, potentially increasing regulatory scrutiny across the broader digital asset industry.

- South Korean lawmakers are set to review the country’s planned crypto tax after a national petition opposing the measure surpassed 50,000 signatures, forcing the issue into the legislative process. Under the proposal, South Korea would impose a 22% tax on crypto gains above roughly $1,650 starting next year, despite ongoing criticism that the market lacks sufficient investor protections and regulatory infrastructure. The tax plan has already been delayed three times, highlighting continued uncertainty around how governments should regulate and tax digital assets. The situation underscores how changing regulatory and fiscal policies in major crypto markets can create uncertainty for investors, trading activity and long-term industry growth.

- Binance is facing renewed scrutiny following reports that an alleged Iran-linked financial network may have used the platform to facilitate hundreds of millions of dollars in transactions tied to sanctions-sensitive activity. According to reports, the network processed roughly $850 million over two years, while U.S. authorities continue investigating whether the exchange was used to help evade sanctions. The controversy comes as Binance remains under heightened regulatory monitoring following its 2023 guilty plea agreement with U.S. authorities. The situation highlights how anti-money laundering (AML), sanctions compliance and geopolitical risks continue to represent major threats for the broader digital asset industry, especially as regulators increase oversight of global crypto exchanges.

Defense and Cybersecurity

Strengths

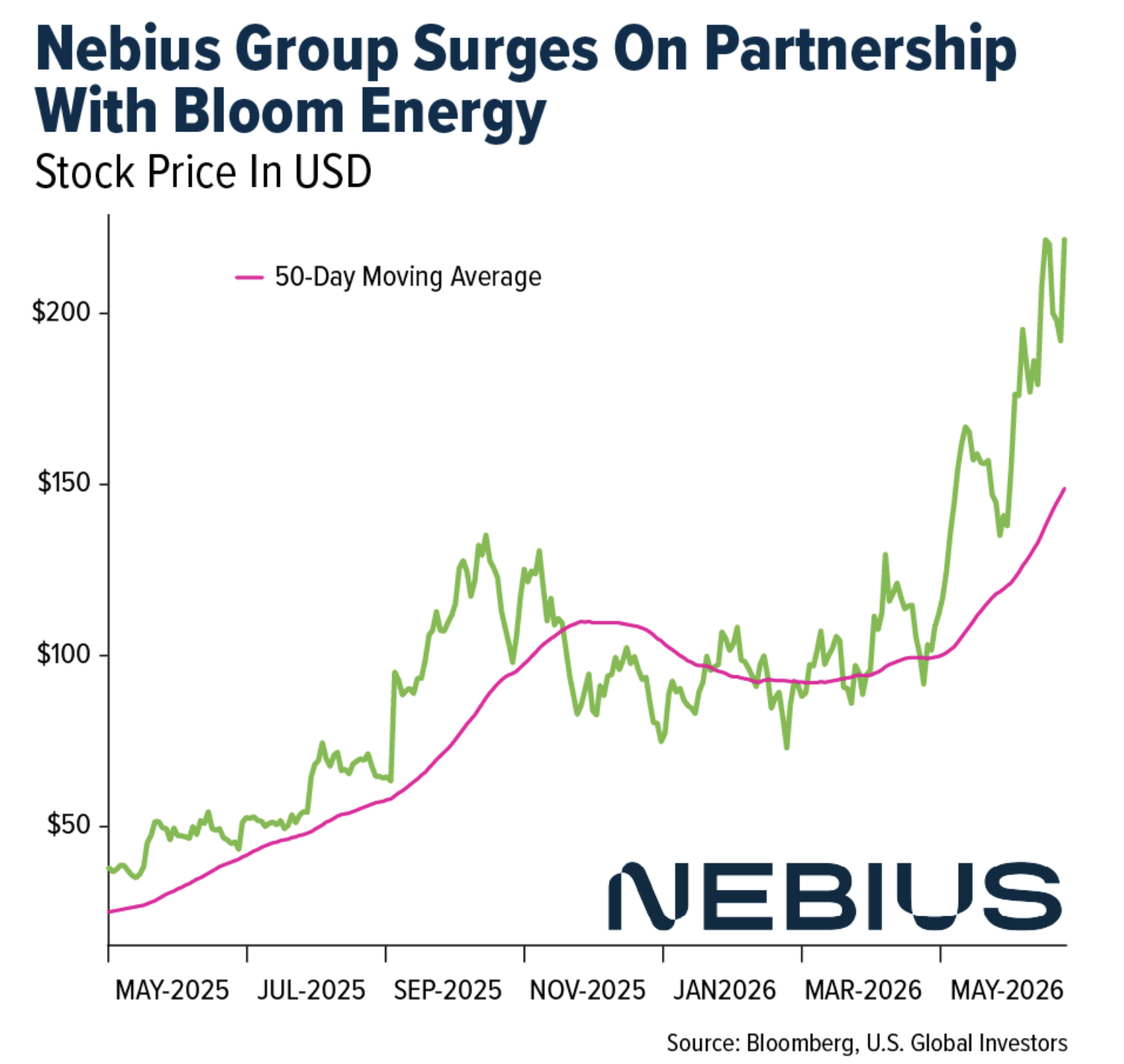

- Nebius Group’s stock surged following a large $2.6 billion partnership with Bloom Energy, which will deploy 328 megawatts of fuel-cell power this year to accelerate its artificial intelligence (AI) data center expansion independently of local electrical grids. This deal highlights Nebius’s significant growth momentum, backed by a recent 684% year-over-year revenue increase and strong validation from major Wall Street analysts.

- The U.S. government committed $1 billion to IBM to build a quantum computing chip foundry as part of a broader $2 billion program involving nine quantum companies funded by the 2022 CHIPS and Science Act, with the government taking equity stakes to bolster U.S. tech competitiveness.

- Poland is set to receive its first F-35s from Lockheed Martin as part of a $4.6 billion deal for 32 aircraft, emphasizing the F-35’s increasing presence in NATO fleets and pressuring Boeing’s competitive standing with its F-15EX and F/A-18 offerings.

Weaknesses

- Lockheed Martin and RTX Corporation are facing a critical inability to scale up production of Patriot missile systems and Patriot Advanced Capability-3 (PAC-3) interceptors, leaving U.S. and allied stockpiles dangerously depleted during ongoing conflicts with Iran and in Europe. Years of peacetime supply chain optimization have created a fundamental weakness, as defense contractors are physically unable to manufacture these systems at the surge capacity required by real, high-intensity warfare.

- The U.S. suspended cooperation with Canada in an 86-year-old joint defense advisory body, marking the latest disruption in ties between the two neighbors.

- The marquee F-35 program, critical to Lockheed Martin’s revenue, is experiencing major delivery halts and financial penalties due to persistent software and hardware integration failures in the Technology Refresh 3 (TR-3) modernization package. This failure underscores the operational weakness inherent in relying on single, hyper-complex programs, where persistent technical defects can freeze deliveries, trigger penalties and severely erode the company’s operating margin.

Opportunities

- The U.S. Navy has approved the MQ-25A Stingray unmanned tanker for Milestone C, allowing the drone to move into low-rate initial production. Boeing is expected to win an initial contract for three aircraft this summer, with options for eight more across two future batches.

- Quantum Cyber has launched a new U.S.-based subsidiary focused on autonomous warfare and drone defense programs as competition intensifies for Pentagon unmanned systems contracts.

- AeroVironment launched an expansion of its AV Halo mission platform with two new software offerings aimed at enhancing unmanned systems operations for defense customers.

Threats

- The United States and Iran remain in a tense standoff under a fragile ceasefire, with negotiations stalled over nuclear disarmament and control of the blockaded Strait of Hormuz. Despite the ongoing diplomatic deadlock, Washington has extended the truce but warned that military options remain on the table if a permanent agreement is not reached.

- President Donald Trump halted the signing of a planned AI oversight executive order, introducing regulatory uncertainty that could affect AI product launches and future compliance costs for companies such as Microsoft.

- U.S. Secretary of State Marco Rubio announced that the United States has halted its mediation in the trilateral peace talks, calling previous diplomatic efforts not fruitful. However, Rubio noted that Washington remains willing to resume its role in the future if a productive breakthrough becomes possible.

Gold Market

This week gold futures closed the week at $4,509.20, down $52.70 per ounce, or 1.16%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.99%. The S&P/TSX Venture Index came off 1.77%. The U.S. Trade-Weighted Dollar rose 0.1%.

Strengths

- The best relative precious metal for the week was gold, although it was down 1.16%. Gold slipped to approximately $4,500 per ounce, down nearly 15% since the Iran conflict erupted, as traders shifted focus from safe-haven flows to the risk that a prolonged Strait of Hormuz closure keeps energy prices elevated and forces central banks to hike rather than cut rates. This marked a reversal from the rate-cut consensus that prevailed before late February. Silver has shown relative strength through the selloff, holding its 50-day moving average at $75.42, supported by dual tailwinds of industrial demand from solar and electronics, as well as its monetary-metal bid. This setup could allow silver to outperform gold if the macro regime tips toward the stagflationary outcome Citi flags as historically strong for precious metals.

- SSR Mining announced the sale of its 20% ownership stake in Hod Maden to Lidya Mines. In exchange, SSR Mining will receive a 4.0% net smelter return (NSR) royalty. Royal Gold has the option to purchase 2.0% of this royalty for $160 million until 12 months after commercial production, according to RBC.

- Net gold ETF inflows turned positive for the first time since early April, driven by North America ($824 million) and Europe ($180 million), according to BMO. Silver ETF inflows also surged to their highest level since late February, led by Europe, at 6.2 million ounces.

Weaknesses

- The worst-performing precious metal for the week was palladium, down 4.77%. The U.S. imposed combined duties of more than 240% on Russian palladium, effectively shutting Nornickel’s approximately 40% global market share out of American supply chains. Meanwhile, China absorbed record imports of 8.6 tons in April, nearly triple the seasonal average, as traders arbitraged the spread between Guangzhou futures and global spot prices rather than responding to any pickup in industrial demand.

- The latest first-quarter 2026 Platinum Quarterly highlights a shift back into surplus, with the market recording its first surplus in six quarters at 268,000 ounces. This was driven by an 18% year-over-year increase in total supply to 1.736 million ounces, with mine supply rebounding 22% YOY, recycling rising 7% YOY and total demand declining to 1.468 million ounces, driven by softer investment demand.

- Northern Star Resources CEO Stuart Tonkin will step down in the third quarter of 2026 after 10 years as CEO. Bank of America does not view the timing of the announcement, ahead of the company’s multi-year outlook, as positive for investor sentiment. Bank of America expects the company to make an external appointment.

Opportunities

- Perpetua Resources secured a $2.9 billion loan from the Export-Import Bank of the United States (EXIM) under EXIM’s “Make More in America” initiative, the largest loan yet under the program. The loan is intended to help the U.S. secure domestic access to critical minerals such as antimony from the Stibnite project, reducing reliance on Chinese exports and helping meet domestic demand.

- Johnson Matthey notes that “platinum is forecast to remain in deficit this year, despite the surplus recorded in the first quarter. Combined primary and secondary supplies are set to contract, with moderate growth in auto catalyst recoveries outweighed by lower jewelry recycling and weaker mine supply from South Africa. On the demand front, platinum has a broader base of applications than the other platinum group metals (PGMs), making it less vulnerable to downturns in any single sector.”

- Agnico Eagle Mines is approving development of Hope Bay. Capital expenditures are estimated at $2.4 billion, and the project generates a 26% internal rate of return (IRR) at $4,500 per ounce. The project will add 400,000 to 435,000 ounces per year starting in 2030, according to BMO. The initial 11-year mine life is based on 50% of the resource, which BMO expects to grow considerably. BMO sees this as a positive step in Agnico Eagle Mines’ push to deliver 20% to 30% production growth over the next decade.

Threats

- Ghana asked large-scale gold miners to sell 30% of annual output to the central bank as part of a revamped reserve-building drive, Reuters reports. The amount producers would be asked to set aside compares with 20% currently.

- Johnson Matthey says that “demand for palladium is forecast to decline by 9% this year, with automotive use shrinking in line with a drop in internal combustion engine (ICE) vehicle production, industrial consumption flat and investment turning negative. Supplies are also expected to fall, as a sharp drop in Russian shipments more than offsets growth in auto catalyst recycling, but this may not be enough to prevent palladium from moving into a small surplus.”

- India has placed most silver imports under the “restricted” category with immediate effect, including silver bars, according to Reuters, as the government looks to curb imports and support the rupee. India meets more than 80% of its silver consumption through imports, with the newly restricted categories accounting for more than 90% of silver imports last fiscal year. The move follows last week’s increase in gold and silver import duties to 15% from 6%.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2026):

Viking Holdings

Nebius Group

Lockheed Martin

Boeing

AeroVironment

Toll Brothers

SSR Mining

Royal Gold

Perpetua Resources

Agnico Eagle Mines

ANA Holdings

Bombadier

American Airlines

Tongcheng Travel Holdings

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The S&P Hotels, Resorts & Cruise Lines Select Industry 15% FMC Capped Index is float-adjusted market capitalization weighted, with a single company cap of 15%, and comprises stocks in the S&P Total Market Index that are classified in the GICS Hotels, Resorts & Cruise Lines sub-industry.

The STOXX Europe 600 Index is a broad European equity benchmark that measures the performance of 600 large-, mid- and small-cap companies across developed European markets.

The Shanghai Shenzhen CSI 300 Index, commonly known as the CSI 300 Index, is a capitalization-weighted equity index designed to measure the performance of 300 large- and mid-cap A-share stocks listed on the Shanghai Stock Exchange and Shenzhen Stock Exchange.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All