Key takeaways:

- Bond benchmarks are useful but not investable: Because fixed income indices are essentially impossible to replicate in a portfolio, investors should consider more relevant comparisons to evaluate passive and active bond performance.

- Active management has tended to benefit bonds: When measured against passive portfolios investors can actually own – rather than theoretical bond indices – most actively managed bond portfolios have outperformed their passive peers, especially over longer time periods.

- Private credit has no true benchmark: In the absence of a standard yardstick, direct lending can appear to perform well by default; however, alternative measures of relative performance suggest excess returns versus adjacent public credit markets have narrowed in recent years.

Despite the move lower late last week, U.S. Treasury yields are still holding well above recent lows and close to highs not seen in more than a year. By contrast, risk assets are firmly bid: U.S. equities have been routinely touching new historical highs, and credit spreads over Treasuries remain tight.

Read more: Key Takeaways From PIMCO’s Sustainable Investing Report 2025

The playbook is unchanged: Risk assets continue to price a resolution of the Iran conflict and are willing to look through some inflation reacceleration so long as growth holds and fundamentals stay supportive, both of which have been the case thus far. Bonds will likely keep discounting a wider range of potential monetary policy outcomes, and also embed a higher war-related risk premium that, if tensions further de-escalate, has room to compress.

This is only one example of the many fundamental differences between risk assets – and equities in particular – and fixed income.

Measuring what matters: Active versus passive

The debate about active versus passive management in fixed income has never been resolved, and the reason is structural, not empirical. Any comparison between the two faces three distinct hurdles. First, performance must be measured on a like-for-like basis, which requires controlling for survivorship bias by including merged and liquidated funds, rather than implicitly treating them as underperformers or excluding them altogether. Second, selecting the appropriate benchmark is inherently more complex in fixed income. Third, and most critically, the comparison should be against an investable passive strategy, not a theoretical benchmark that no investor can actually own.

This last point is where most comparisons break down. Bond indices, while useful as broad measures of an investable universe, are not portfolios anyone can hold. Aggregate and corporate indices, and especially securitized, bank loan, and emerging market bond indices, are closer to accounting constructs than tradable, observable portfolios. They assume month-end rebalancing at the mid price, costless absorption of new issues, real-time treatment of rating migrations, and full inclusion of thousands of line items that trade “by appointment” rather than in liquid, transparent markets. Replicating this universe in a portfolio is simply not possible. As a result, measuring active fixed income performance against these paper indices conflates the cost of investability with manager skill.

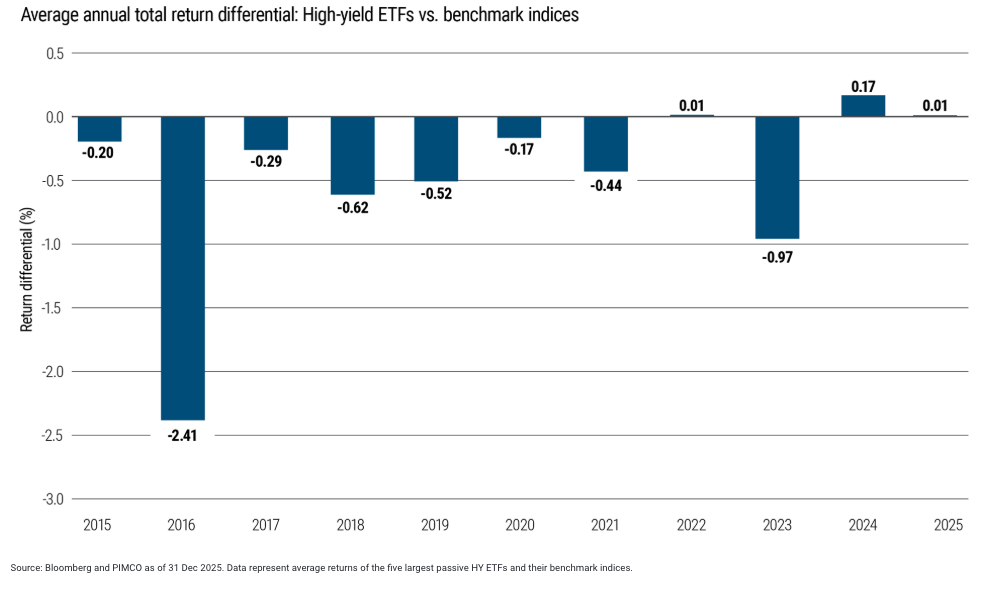

Index ETFs make that cost visible. A passive vehicle has no selection mandate, yet it persistently lands below the benchmark – dragged down by fees, transaction costs, and sampling discrepancies. Figure 1 illustrates this by plotting the average annual total return differential relative to the benchmark for the top five passive ETFs in the high yield (HY) market (measured by assets under management) over the past 10 years. The pattern is predominantly negative, meaning that when judged by the same benchmark-relative logic applied to active managers, passive essentially underperforms itself.

Figure 1: On average, passive HY ETFs have lagged their benchmark indices

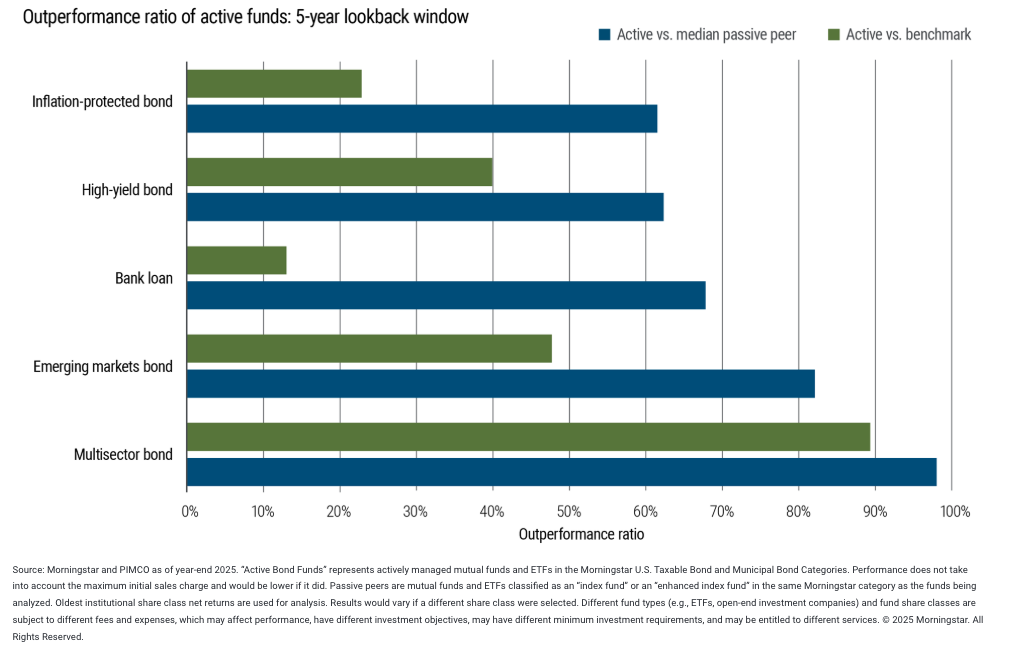

The real test, then, is not active return against a theoretical index but against what an investor could actually have earned in a passive vehicle, fees included and ideally risk-matched. Measured that way, the evidence is clear: Active fixed income beats passive most of the time. Figure 2 illustrates this by showing the fraction of active fixed income funds and ETFs that outperform their benchmark indices versus those that outperform their median passive peers.

Figure 2: The empirical evidence shows that a majority of active bond funds outperform their median passive peers over a five-year period

The comparisons in Figure 2 are performed net of fees, using a five-year lookback window as of year-end 2025 (the results are similar when using a 10-year lookback period). Our universe also includes merged and liquidated funds and therefore corrects for any potential survivorship bias. As the chart shows, across various styles, the fraction of active funds that outperform their median passive peers is quite high. The ratio of outperformers also increases over longer horizons. The evidence shown in Figure 2 is consistent with a large body of academic literature.Footnote1

With spreads at historically tight levels, the compensation for indiscriminate exposure is thin and the asymmetry unattractive. At the same time, dispersion is rising. When valuations are rich, managing downside risk is first and foremost about avoiding positions the index forces on a passive holder. When dispersion is high, doing the credit work in both public and private markets can pay off to capture the upside. These are precisely the conditions where passive replication is most costly and active management may be most valuable.

No benchmark, no problem? Not quite.

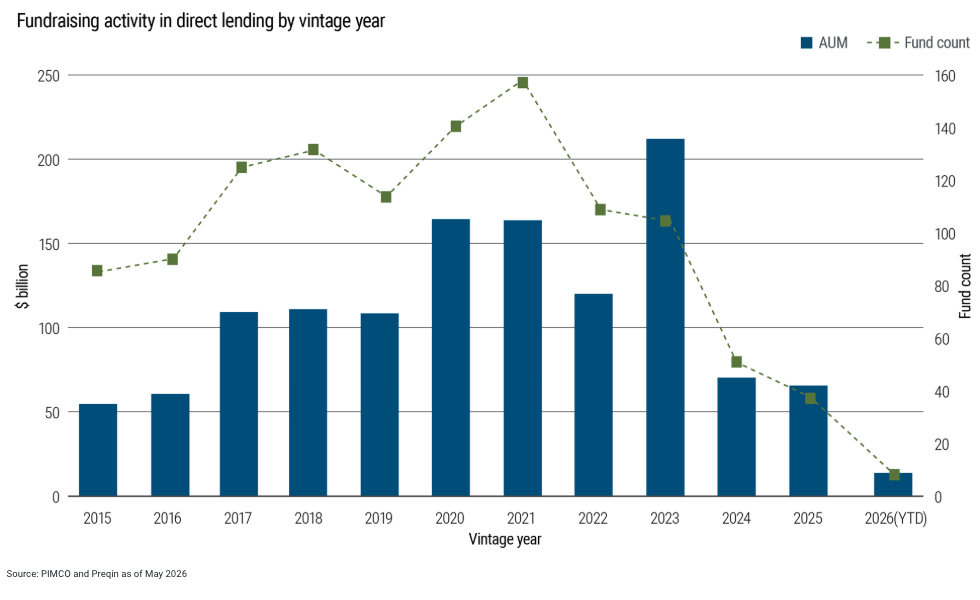

Much of the attention in private credit has focused on redemption pressure in non-traded business development companies (BDCs). But five months into the year, fundraising in drawdown funds looks mixed at best. The number of newly launched direct lending funds – on a run-rate basis – remains very low, while the number of funds reaching a final close has also declined materially. Further, the time from launch to close continues to set new highs. These figures will likely be revised, but the direction is clear: Institutional appetite for direct lending has cooled, and financing conditions for borrowers are tightening at the margin as a result (see Figure 3).

Figure 3: Fundraising activity in direct lending has further cooled this year

Beyond the fundamental headwinds facing direct lending portfolios, the shrinking excess premium over comparable public markets has also weighed on demand. This brings into focus a deeper issue: how to measure that excess premium. And in private markets, the problem runs in the opposite direction of public markets. There is no benchmark at all, and that absence invites the comfortable illusion of costless outperformance.

But the lack of a yardstick does not mean direct lending consistently outperforms a viable alternative. A more appropriate comparison exists: a modestly leveraged exposure to the broadly syndicated loan market. Viewed through that lens, private credit is not benchmark-free.

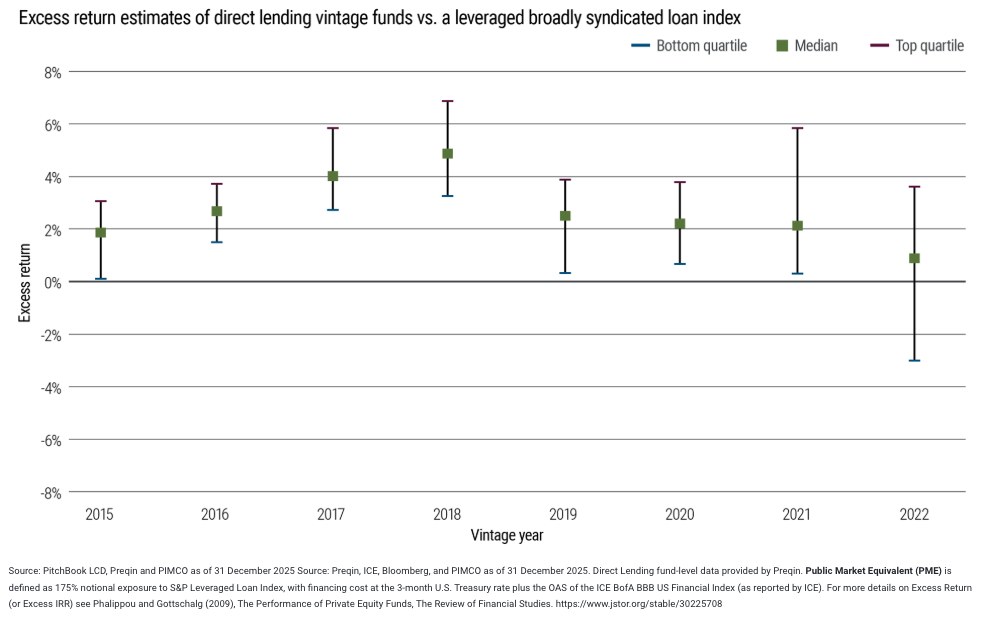

This is illustrated in Figure 4, which plots the excess return (net of fees) generated by direct lending vintage funds versus a leveraged broadly syndicated loan index, using a public market equivalent (PME) framework. Stripping away technical details, the PME approach estimates the excess return that must be added to the leveraged broadly syndicated loan index so that the net present value of the fund’s cash flows equals zero. Intuitively, this measures how much additional return the fund has generated relative to what investors would have earned by investing the same cash flows in the leveraged public broadly syndicated loan index. These results capture both investors’ compensation for illiquidity as well as any additional benefit from manager selection.

Figure 4: The extra compensation provided by direct lending vintage funds versus the broadly syndicated loan market has been declining in recent years

The takeaway from Figure 4 is straightforward. The pre-COVID vintages delivered solid compensation relative to public market equivalents, reflecting stronger underwriting discipline and greater scope for manager skill. By contrast, recent vintages have seen a steady decline in excess returns.

Put differently, recent vintages of direct lending portfolios appear to increasingly resemble a beta product, with returns driven more by broad credit conditions than by manager skill, much like a passive exposure.

Michael Puempel, Gabriel Cazaubieilh, Helen Guo, and German Ramirez contributed to this article.

Footnotes:

1 See Jaewon Choi, K. J. Martijn Cremers, and Timothy B. Riley. “Active versus Passive Management of Bonds (and why passive bond management is an oxymoron).” SSRN paper 3557235 (revised April 2026). See also K. J. Martijn Cremers, Jon A. Fulkerson, and Timothy B. Riley. “Benchmark Discrepancies and Mutual Fund Performance Evaluation.” Journal of Financial and Quantitative Analysis (2022).

Return to content

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Read more commentaries by PIMCO