When Volatility Isn’t the Risk That Matters

For decades, portfolio construction across the advisory industry has been anchored in a simple premise: managing volatility equates to managing risk.

This assumption is embedded in widely adopted frameworks—diversification, mean-variance optimization, risk parity, and volatility targeting. Each seeks to smooth the path of returns, reduce drawdowns, and improve client experience.

However, experience across multiple market cycles suggests that the relationship between volatility and risk is more nuanced. While volatility is observable and measurable, it may not fully capture the outcomes that matter most to long-term investors.

Defining Risk vs. Experiencing Risk

In practice, volatility is often used as a proxy for risk because it is observable, measurable, and easily communicated. Standard deviation, tracking error, and beta offer a structured way to describe how a portfolio behaves under most market conditions.

But investors do not experience risk as a statistical abstraction. They experience it as permanent impairment of capital or disruption to the compounding process. These outcomes are typically not driven by routine market fluctuations. Rather, they tend to occur during severe, episodic dislocations—periods when the assumptions underlying traditional portfolio construction may not hold.

This distinction is important:

- Volatility reflects the variability of returns

- Risk, in a long-term wealth context, reflects exposure to meaningful and lasting drawdowns

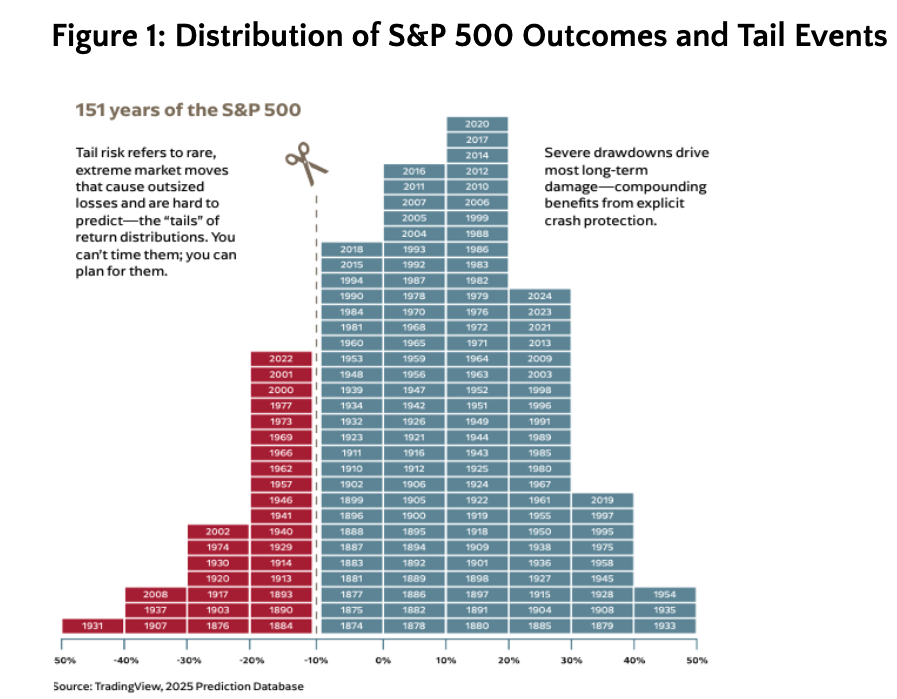

Intra-year declines on the S&P 500 of 10–15% are normal market occurrences. History shows they are frequent and not necessarily detrimental to long-term wealth creation. Yet an expanding array of products and asset allocation models promote protection against exactly these types of drawdowns—often at a meaningful cost to upside market participation.

At the same time, these approaches may offer more limited protection during periods of severe market dislocation, when correlations shift and liquidity conditions deteriorate. When done effectively, risk mitigation should expand the ability to take intelligent risk over time—not simply reduce volatility. While that may appear counterintuitive within traditional portfolio frameworks, it is economically consistent: preserving capital during periods of severe stress can enhance the long-term compounding path.

In practice, many investors allocate to risk mitigation strategies for their intended protective effects, but do not always fully account for the cost required to achieve those outcomes.

Viewed over a full market history, it becomes clear that not all market declines carry the same significance. While moderate drawdowns occur with regularity, the most meaningful impacts on long-term wealth creation have historically been concentrated in a relatively small number of severe dislocations.

The Limits of Traditional Risk Management

Conventional portfolio management techniques are generally designed to perform within a defined set of assumptions:

- Correlations across asset classes remain relatively stable

- Liquidity is available across markets

- Price behavior falls within historically observed ranges

During periods of stress, these assumptions can break down. Correlations may converge, liquidity can deteriorate, and price movements can become more abrupt and less predictable.

In these environments, diversification—while still valuable—may provide less protection than expected.

At the same time, many strategies intended to manage volatility introduce structural trade-offs. Allocations to lower-volatility assets may reduce short-term fluctuations but also dampen long-term expected returns. Risk-targeting approaches can require adjustments during periods of stress that lock in losses rather than mitigate them.

These dynamics suggest that managing volatility and managing severe downside risk are not necessarily the same objective.

A Structural Distinction: Volatility Control vs. Drawdown Protection

It is useful to distinguish between two different portfolio goals:

1. Volatility Control

- Seeks to reduce variability in returns

- Focuses on improving return consistency

- Generally performs well in stable or mean-reverting environments

2. Drawdown Protection

- Seeks to to mitigate the impact of large, episodic losses

- Focuses on preserving capital during extreme dislocations

- Assumes that markets can behave differently under stress than historical averages suggest.

The difference between these objectives is structural.

A portfolio optimized for volatility control may still experience significant losses during periods of market instability. Conversely, approaches designed to address extreme outcomes often accept some cost during normal markets in exchange for resilience during stress.

Implications for Portfolio Construction

Recognizing this distinction has several implications:

1. Risk Should Be Defined by Outcome

Risk measures such as maximum drawdown, recovery time, and exposure to non-linear market events may provide a more complete picture than volatility alone.

2. Diversification Has Boundaries

Diversification remains a foundational principle, but its effectiveness is conditional. Understanding how correlation structures behave under stress can help set more realistic expectations.

3. Portfolio Design May Require Multiple Layers

Managing routine volatility and protecting against extreme outcomes are distinct goals. Addressing both may require complementary approaches rather than reliance on a single framework.

4. Framing Matters in Client Conversations

Advisors increasingly serve as interpreters of risk. Explaining the difference between managing fluctuations and managing potential impairment may become a more important part of that role.

A More Complete View of Risk

None of this suggests that volatility management should be abandoned. Reducing unnecessary fluctuations and maintaining disciplined portfolio construction remain important objectives.

However, a portfolio designed solely around volatility may overlook the events that have historically driven the most significant outcomes for long-term investors.

A more complete framework considers:

- Behavior in both normal and stressed markets

- Trade-offs between efficiency and resilience

- The role of protection against non-linear outcomes

Conclusion

Volatility provides a useful, observable lens through which to view portfolio behavior. But it is not the only lens—and, at times, it may not be the most relevant one.

Over full market cycles, the risk that matters most is often not the frequency of small fluctuations, but the impact of rare, severe dislocations.

For advisors, acknowledging this distinction does not require abandoning established principles. It requires expanding them—so that how risk is measured more closely aligns with how it is ultimately experienced.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.