Contrary to what legal television series portray, verdicts rarely turn on a single moment of drama. They take shape gradually, as evidence accumulates and a broader narrative comes into focus.

Britain’s government bond (gilt) market has been struggling of late, with long-term yields surging to their highest levels since 1998. Investors are reaching a verdict not from one dramatic moment, but by a steady build-up of evidence that forms a troubling narrative.

Politics has played its part. The U.K. has had six prime ministers in a decade, and may soon have a seventh following the Labor Party’s poor showing in recent local elections. The balloting earlier this month has brought the possibility of another leadership contest back into view, and suggests an uncomfortable level of instability.

That said, political turmoil should be seen as an outcome, not the source of the problem. The real story for markets lies beyond Westminster, in an economic backdrop that has shaped and constrained policy choices.

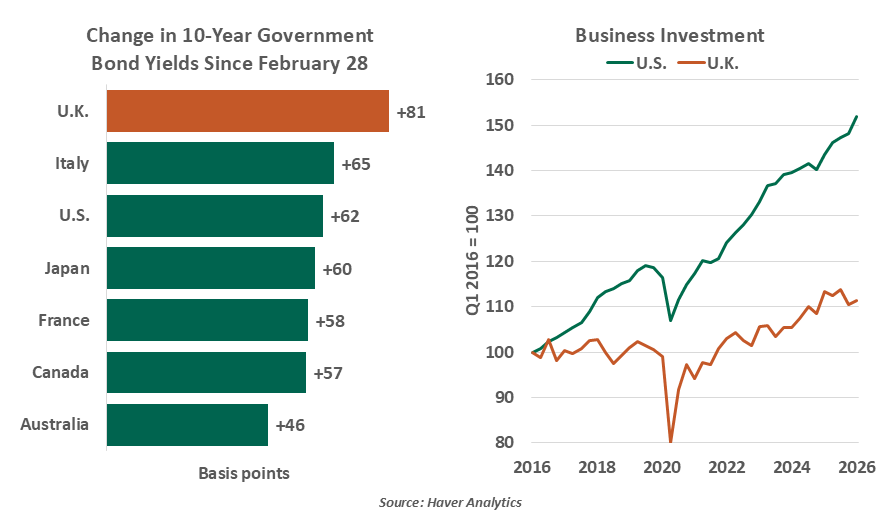

Britain’s economy has struggled for years to escape a pattern of underperformance. U.K. growth has trailed both the U.S. and the wider eurozone in recent years, by a wide margin. Britain’s productivity has fallen short of both its pre‑pandemic trajectory and the performance of its major peers. Since 2016, business investment has risen at less than half the pace seen in the United States. Post‑Brexit frictions and successive shocks from the pandemic and the Ukraine war have weighed on activity and dampened corporate confidence.

While investment picked up modestly in Britain last year, the composition offered little reassurance. Much of the increase was concentrated in utilities, which are essential but which do not generate broader economic dynamism. By contrast, investment in the U.S. has been more heavily skewed toward infrastructure and artificial intelligence (AI).

Though U.K. firms have been quick to adopt AI, the nation still lags far behind the United States and China in both model development and investment. While the U.K.’s capital markets are sophisticated, tech firms sometimes struggle to access them. The U.S. offers a clear contrast: deep capital markets, strong domestic demand, and a focused tech sector are keeping investment in AI flowing. As a result, while adoption is high in the U.K., it is not yet powerful enough to materially lift its weak productivity.

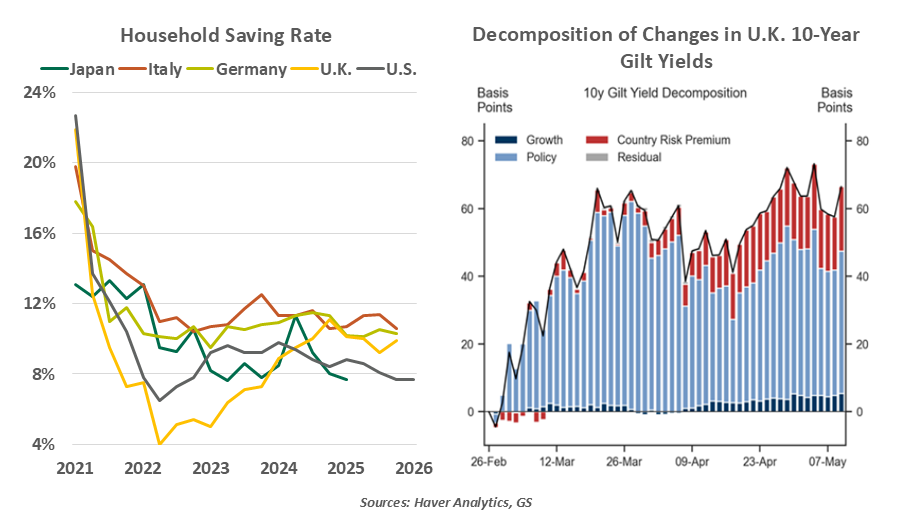

U.K. consumers have been unable to compensate for a disappointing investment environment. British households have remained unusually cautious since the pandemic, as reflected in elevated savings and a softer appetite for credit. Rising prices have eroded purchasing power; inflation was running above 3% even before the latest energy shock. The squeeze on real incomes and spending in Britain is becoming more acute.

A shift in expectations around the path of monetary policy has been the main force behind the gilt selloff this year. Persistent inflation has kept borrowing costs elevated, keeping the Bank of England cautious. Monetary policy will be tighter for longer. The result has been upward pressure on longer-term yields. Structural factors in the gilt market have added to the strain: quantitative tightening from the Bank of England has removed a stabilizing buyer. Defined benefit pension schemes are winding down, reducing another source of demand.

Fiscal dynamics have become central to the market’s calculus. Weak growth has strained public finances, narrowed policy choices, and intensified political fragmentation, leaving the economy exposed to even modest shocks. In times like these, markets are acutely sensitive to any perceived slippage or erosion of fiscal headroom.

As the chart above shows, political risk has played a more secondary role in the recent gilt market turmoil, but the unsettling political backdrop threatens to make matters worse. The ongoing Middle East war could wipe out as much as £16 billion of fiscal headroom, through higher energy costs, rising yields and their knock-on effects on inflation and growth. Leadership changes can open the door to looser fiscal impulses at a time when scrutiny from the bond markets is most intense.

Broadly, the debate among leading candidates to replace Prime Minister Starmer is less about direction than degree. The current front-runner Andrew Burnham advocates a break from austerity-era thinking, favoring higher borrowing to fund infrastructure and housing. He would also like to take defense spending out of existing fiscal rules.

That said, whoever takes the helm will inherit the same constraints: limited fiscal space, market scrutiny, and an economy that has yet to regain momentum. Britain has tried supply-side initiatives; it has tried austerity. Neither has delivered a sustained lift in trend growth. Policy choices may shift at the margin, but the binding nature of these constraints is unlikely to change.

Given this varied and mounting evidence, it is not surprising that the U.K. sits near the top of the Group of Seven for long-term borrowing costs. Markets are serving as a jury, and are finding guilt. A sentence of higher interest rates will be punitive for the U.K. economy, beyond a reasonable doubt.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust