The $13.7 Billion Hedge Fund That’s Betting Big on AGI Infrastructure

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIf you’re not familiar with the name Leopold Aschenbrenner, you should be.

A 24-year-old wunderkind, Aschenbrenner was hired by OpenAI in 2023 to work on the company’s “superalignment” team, essentially trying to figure out how to keep AI systems safe once they become smarter than the people building them. After being let go in 2024, he published a 165-page essay called Situational Awareness that went viral in Silicon Valley, Washington and on Wall Street.

His central argument in a nutshell: AI models could become capable of doing the work of AI researchers by around 2027. If that happens, AI begins improving itself, and the timeline to artificial general intelligence—or AGI—compresses dramatically.

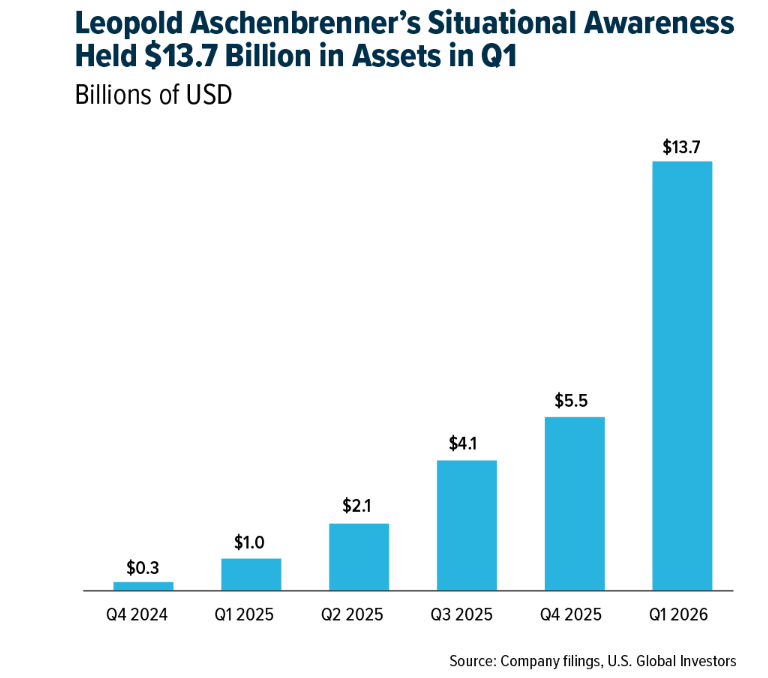

Aschenbrenner also created a hedge fund, Situational Awareness LP, specifically to invest in the AGI growth trend. In its 13F filing for the first quarter of 2026, the company disclosed it held a respectable $13.7 billion in assets. That’s up from just $254 million at the end of 2024, a head-spinning 54x increase.

I’m happy to report that Aschenbrenner’s fund also disclosed a purchase of nearly 3.4 million shares of HIVE Digital Technologies. As many of you know, I serve as executive chairman of HIVE, and on behalf of everyone at the company, I want to express my gratitude in Aschenbrenner and Situational Awareness’s conviction in the HIVE story.

But the bigger story here isn’t the HIVE investment. It’s what’s driving Aschenbrenner’s thesis, and how quickly the rest of the world is catching up to it.

The AGI Consensus Is Building Fast

What’s changed since Aschenbrenner published Situational Awareness is that the voices agreeing with his outlook have only multiplied. And these aren’t fringe figures.

Marc Andreessen, co-founder of venture capital firm a16z and co-creator of some of the earliest web browsers, said he believes AGI is already here. On Joe Rogan’s podcast last week, he claimed that the top AI chatbot platforms (OpenAI, Claude, et al) now give him better answers on any topic than what world-class experts could give him.

Demis Hassabis, CEO of Google DeepMind, claimed at Google’s developer conference this month that humanity is “standing in the foothills of the singularity”—another word for the moment when AI surpasses human cognitive capacity. He now expects AGI to arrive in 2029.

Ambitious forecasts, maybe, but the financial data appears to support this breakneck growth. Microsoft’s AI business alone just surpassed an unbelievable $37 billion run rate, up over 120% year-over-year.

Morningstar reports that AI-focused funds attracted over $16 billion in net inflows in 2025, nearly eight times the prior year. Despite broader market turbulence, flows remained strong in the first quarter of 2026.

The Semiconductor Boom Tells the Story

If you want a single indicator of how fast this industry is moving, just look at the chip sector.

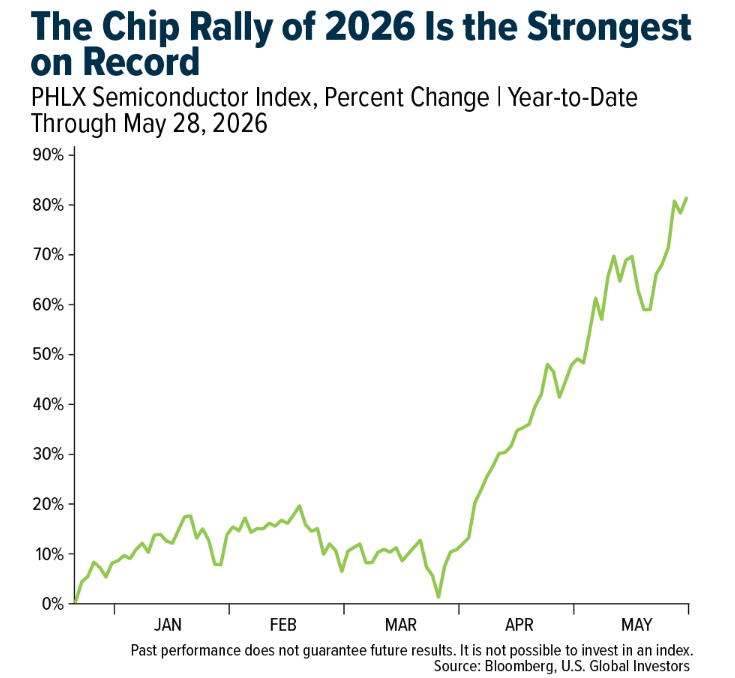

The PHLX Semiconductor Index has climbed 82% so far in 2026, its best-ever performance through the first 100 trading days of any year. The previous record was set in 1995. Believe it or not, companies in the index have added roughly $5.7 trillion in market capitalization this year alone.

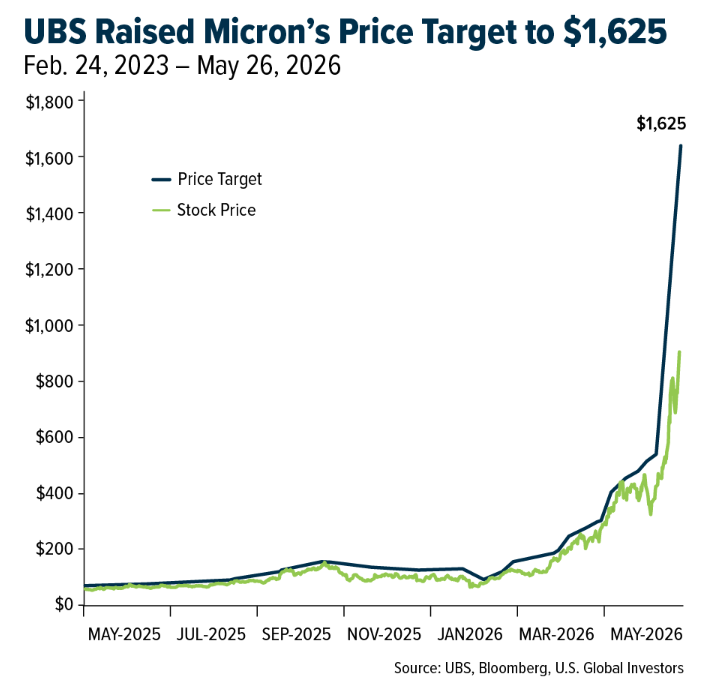

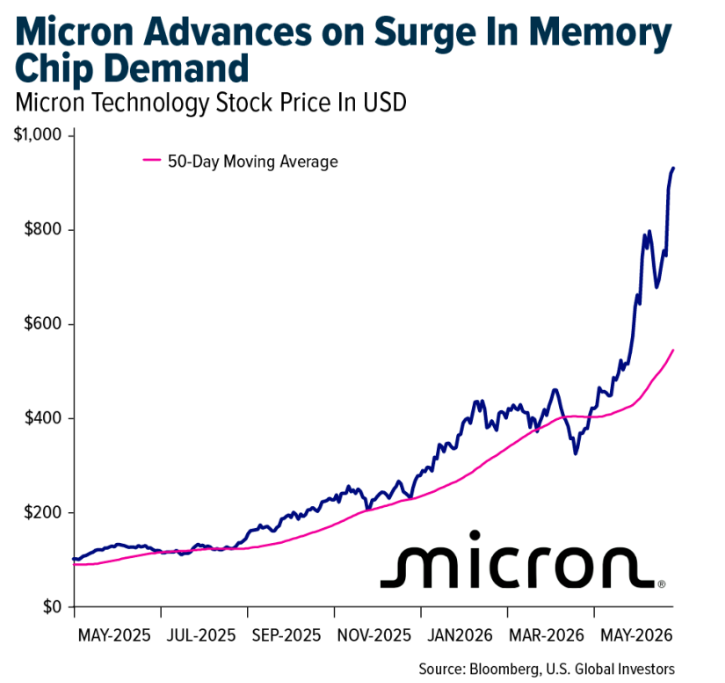

This week, memory chipmakers Micron and SK Hynix both crossed the $1 trillion valuation mark. UBS raised its price target on Micron from $535 to $1,625.

Power, Land and Infrastructure

Despite the breakneck momentum, Aschenbrenner’s fund is actually shorting chipmakers.

Instead, he’s going long on companies that own the electricity, data centers and physical infrastructure that AI requires to scale.

His largest holding is the VanEck Semiconductor ETF, but the filing also disclosed significant stakes in Bitcoin miners and infrastructure firms. Besides HIVE, you’ll find IREN, Core Scientific, Riot Platforms, CleanSpark and others.

Why? Because as Aschenbrenner wrote in Situational Awareness:

“The race to AGI won’t just play out in code and behind laptops—it’ll be a race to mobilize America’s industrial might.”

He’s not wrong. Global AI computing capacity is doubling every seven months, according to Epoch AI.

Training clusters are on track to cost hundreds of billions of dollars individually by 2028, each requiring power equivalent to a small U.S. state.

Put another way, you can design all the chips you want, but without secured megawatts and physical sites, they have nowhere to run.

It takes roughly three years to build a data center from the ground up. But if you already have the infrastructure from Bitcoin mining, you can cut that to nine months.

That’s the advantage that Bitcoin miners such as HIVE bring to the table. We already control the power contracts, the substations, the cooling system and the land.

New Demand, Old Constraints

I’ve spent my career investing in commodities and natural resources, and I’ve learned that the biggest opportunities tend to emerge when a new source of demand collides with physical constraints. Gold, oil, copper—every great commodity cycle has followed this pattern.

AGI is no different, except the constrained resource this time is electricity and the infrastructure to deliver it.

As Aschenbrenner points out, the timeline to AGI is compressing. The capital flowing into the space is accelerating. And the people who understand the technology best—the builders, the researchers, the fund managers who staked their reputations on it—are placing their bets not on software, but on the physical infrastructure required to make it all real.

Airlines and Shipping

Strengths

- The best-performing airline stock for the week was Frontier, up 22.2%, on no major news. Ryanair confirmed that it repaid its last EUR1.2 billion bond, leaving the Ryanair Group effectively debt-free as it heads into a challenging summer of growth at low fares.

- As reported by Bank of America, April new shipbuilding orders remained strong (+21% year-over-year (YoY)), supporting a 7.7% increase in the global order book. Tankers continued to lead ordering activity, while bulker orders began to recover from March, driven by rising freight, charter and secondhand rates, particularly for Capesize vessels. Newbuild prices continued to firm on a month-over-month (MoM) basis, with China’s newbuild price index turning positive YoY, supported by strength in tankers and bulkers.

- Singapore Air’s passenger demand and yield outlook remain positive and resilient in the near term, with the company expecting continued resilience in both metrics despite a challenging cost environment. Management, during the fiscal year 2025/26 (FY25/26) briefing, highlighted that forward bookings remain robust in the near term, and no material demand destruction has been observed even as airfares have increased to partially offset higher jet fuel costs, according to JP Morgan.

Weaknesses

- The worst-performing airline stock for the week was Tongcheng Travel, down 4.9%. American Airlines noted that its corporate volume is 20% below pre-pandemic levels. However, this has been offset by higher fares.

- According to Bank of America, the tanker market is seeing clear impacts from the Hormuz closure, with April seaborne crude trade down 19.6% year-over-year (YoY). All eyes are on a Hormuz reopening, which could drive another rate spike. Hormuz transits were around 3% of normal levels in the past week, with some tanker transits coordinated with Iran.

- Boeing noted that it has financial penalties on current deliveries due to delays, which are expected to burn off over the next 1–2 years. The 787 program is experiencing production instability at eight aircraft per month due to business-class seating shortages and slow engine deliveries.

Opportunities

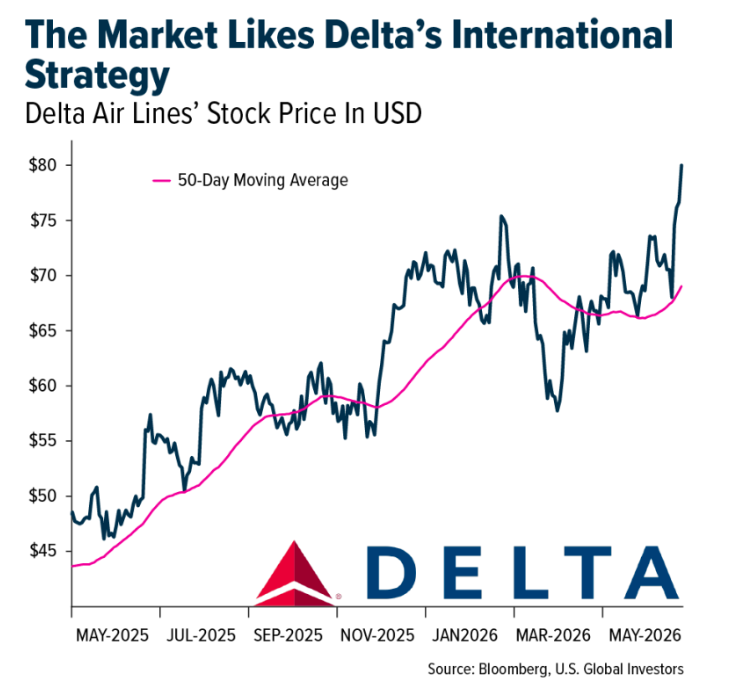

- According to Morgan Stanley, Delta has indicated that it is prioritizing international growth over mergers or consolidation in the U.S. airline market, viewing overseas expansion as a stronger long-term opportunity than competing for additional domestic market share. The airline plans to expand its presence through new international routes and partnerships in regions including India, Saudi Arabia, Hong Kong, South America and Mexico.

- For Japanese shippers, while the Middle East conflict has both positive and negative effects, JP Morgan sees upside potential relative to each company’s guidance. The firm expects container freight rates to rise toward the summer peak season and favors each company’s initiatives to improve capital efficiency and increase valuations.

- Despite likely sharp earnings decline amid elevated oil prices, Spring Airlines in China may remain profitable in Q2 due to strong cost controls. By contrast, UBS expects China’s Big Three carriers (Air China, China Eastern and China Southern) to be loss-making in Q2. As of now, Spring Airlines’ load factor and flight volume have both increased year-over-year (YoY), while many peers have notably reduced capacity. Although the total number of Chinese carriers’ flights on the China-Japan route fell 70% YoY, Spring Airlines’ existing flight capacity on the route has become more profitable YoY, driven by strong demand.

Threats

- If the historical jet fuel/TRASM relationship holds, current consensus may be overstating earnings, with downside risk to unit revenues. While a lower fuel price environment is welcome, both BMO may be underappreciating the potential for unit revenue decline. In general, expectations are for fuel to fall +17% between fiscal year 2026 (FY26) and FY27 and +20% between FY26 and FY28. Consensus, however, is that unit revenues are expected to be flat to up low-single-digits over the corresponding periods. If history holds, there is risk that unit revenues instead fall roughly 3%.

- According to Morgan Stanley, Q1 shipping operating margins averaged 5.2%, above pre-COVID levels and 2023 lows. As new supply continues to enter the market, the firm sees downside risk to rates.

- This week, third-quarter 2026 (3Q26) domestic capacity growth fell by 80 basis points (bps) to 0.8%, as airlines broadly reduced growth, according to Bank of America. As noted in last week’s monthly scorecard, September capacity growth was elevated relative to the summer, and American had reduced less capacity than peers. This week, reductions to 3Q26 domestic capacity were concentrated in September and led by American Airlines, as September growth fell to +2.1% from +4.1% last week.

Luxury Goods and International Markets

Strengths

- Compagnie Financière Richemont reported full-year sales growth of 11%, driven by continued strength in its jewelry business, where sales rose 14% at constant exchange rates. Management highlighted a significant improvement in cash flow, supported by stronger profitability, disciplined cost management, and resilient demand for high-end jewelry brands such as Cartier and Van Cleef & Arpels.

- Industrial profits in China improved more than expected, with profits at major industrial firms rising 18.2% year-over-year (YoY) in the January–April period, up from 15.5% growth in the first quarter. April profits alone surged 24.7%, marking the fastest pace of growth since late 2023. The improvement was driven by stronger manufacturing activity, higher demand for technology and industrial metals, and continued support from government stimulus measures.

- Cettire, an online luxury fashion retailer, was the best-performing stock in the S&P Global Luxury Index over the past five trading days, with shares surging more than 30%. The rally followed the company’s announcement of a strategic partnership and the launch of a flagship store on Alibaba’s Tmall Global platform, a move expected to strengthen its presence in the Chinese luxury market.

Weaknesses

- Capri Holdings, known for Michael Kors and Jimmy Choo, reported weaker-than-expected quarterly sales. The Michael Kors brand, which accounts for approximately 80% of group sales, continues to experience declining revenue in the United States and Asia.

- Eurozone consumer confidence remains weak. The final May consumer confidence reading came in at -19, down from -12.4 at the end of February, before tensions in the Middle East escalated. A reading of -19 indicates that pessimistic consumers significantly outnumber optimistic consumers, reflecting concerns about the economic outlook and the potential for weaker consumer spending.

- Ananti, a South Korean luxury hospitality and resort developer, was the worst-performing stock in the S&P Global Luxury Index, with shares falling nearly 11% over the past five trading days. The stock posted its second consecutive week as the index’s weakest performer, as investor sentiment remained pressured by concerns over weakening earnings, rising financial risks, and softer-than-expected results.

Opportunities

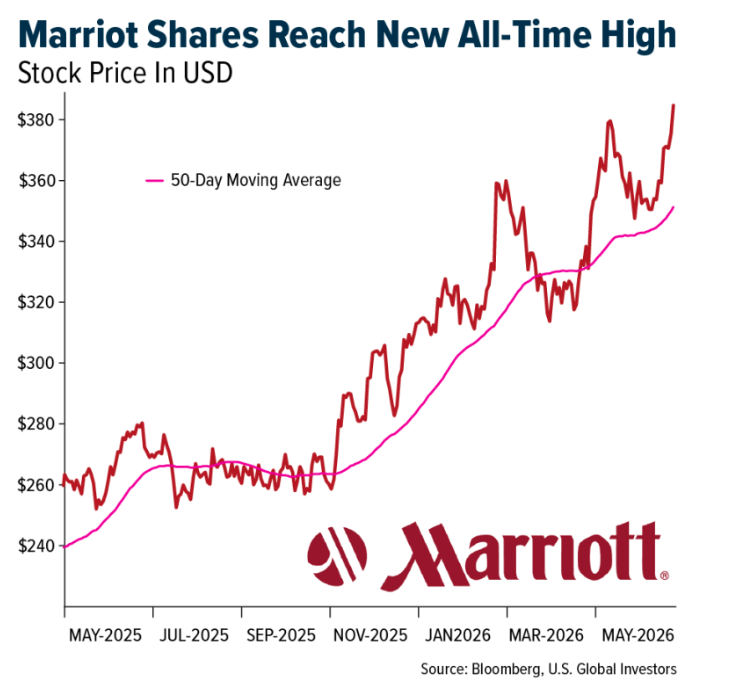

- Shares of Marriott International reached a new record high as investors continued to favor the company’s asset-light business model, which generates strong fee-based revenue with lower capital requirements. Optimism around global travel demand, improving hotel occupancy trends, and resilient consumer spending further supported sentiment toward the hospitality sector.

- Consumer discretionary and travel stocks rebounded this week as oil prices declined on prospects for reopening the Strait of Hormuz, potentially easing disruptions to regional oil transport. While U.S.-Iran peace negotiations remain fragile, further signs of de-escalation could provide additional support for equities.

- American Express continued to report strong spending trends among affluent consumers, with luxury merchant sales rising 18% in the first quarter, accelerating from 15% growth in fourth quarter 2025 (4Q25). The increase highlights resilient demand for premium travel, dining, and luxury retail purchases.

Threats

- Shares of Ferrari came under pressure this week following the unveiling of the company’s first fully electric vehicle. Critics argued that the design resembles an SUV more than a traditional Ferrari sports car, raising concerns that the model could dilute Ferrari’s exclusive luxury-performance image. The vehicle is expected to carry a price tag of approximately €550,000, with first deliveries in Europe scheduled for October.

- Zalando’s expansion into pre-owned luxury through its partnership with Vestiaire Collective highlights growing consumer acceptance of secondhand luxury goods, which could pose a challenge to traditional luxury brands. By making authenticated pre-owned products from more than 50 designer brands accessible across 14 European markets, the partnership may divert spending away from new luxury purchases, particularly among younger and more price-conscious consumers.

- Eurozone inflation data is scheduled for release next week. According to Bloomberg analysts, inflationary pressures are expected to increase, driven largely by higher energy costs in a region that remains heavily dependent on energy imports. The May Consumer Price Index (CPI) is forecast to rise to 3.2%, up from 3.0% in April.

Energy and Natural Resources

Strengths

- The best-performing commodity for the week was natural gas, which rose 8.57% as June weather forecasts moved higher, reflecting hotter-than-expected conditions. Natural gas demand tends to surge when consumers turn on their air conditioners and utilities need to fire up gas-powered turbines to meet peak electricity demand. Aluminum prices have also remained strong due to disruptions in shipments from the Middle East, which accounts for roughly 80% of global supply. In addition, some production curtailments have occurred, and restarting facilities from a warm idle state back to operating temperatures of approximately 960°C can take anywhere from several weeks to two or three months, suggesting price strength could persist.

- Copper remained firm as the tariff arbitrage trade reemerged. Trafigura withdrew approximately 51,000 metric tons from LME warehouses—the largest orders since 2013 and valued at more than US$700 million—driving Comex copper to a premium of more than US$500 per ton over LME cash prices for the first time since last autumn. With copper up approximately 43% year-over-year (YoY) and trading near US$13,746 per ton, the Commerce Secretary’s late-June Section 232 update is the next key catalyst for additional U.S.-bound flows.

- The Trump administration is redirecting approximately 20 tons of surplus weapons-grade plutonium into advanced reactor fuel, providing a potential boost to Oklo and the broader nuclear renaissance trade. However, increased use of recycled Cold War-era material could reduce future demand for newly mined uranium and enrichment services.

Weaknesses

- WTI crude futures were the worst-performing commodity of the week, falling 9.05% after U.S. officials confirmed that negotiators had reached a memorandum of understanding with Iran to extend the ceasefire by 60 days and begin further talks on the nuclear issue, pending President Trump’s approval.

- BHP faces reputational risks after leaked memos revealed it shelved US$1.7 billion in Pilbara renewable energy projects, including a US$400 million solar-and-battery project and a US$1.3 billion proposal, while purchasing 62 diesel trucks expected to remain in service through 2041. Internal warnings about potential damage to its social license to operate may further widen the credibility gap with investors and regulators.

- Surging sulfuric acid prices, driven by disruptions related to the Strait of Hormuz, are raising production costs for lithium, nickel, cobalt, and rare earth producers, increasing the risk of curtailments and project delays. The impact extends to both agriculture and industrial metals, as sulfuric acid is critical to fertilizer production and copper processing.

Opportunities

- The Shanxi coal mine disaster could create opportunities for seaborne and Mongolian coal suppliers, with Mongolian imports already up 80% year-over-year (YoY) in Q1, as China scrambles to secure supply ahead of peak summer demand. Australian hard coking coal exporters may be among the primary beneficiaries if Chinese import demand increases.

- Codelco and SQM’s proposed US$3 billion direct lithium extraction (DLE) rollout in the Atacama could improve recovery rates, reduce environmental impacts, and help de-risk the technology globally. A successful deployment would strengthen Chile’s position as a leading lithium supplier and benefit technology providers and battery supply chains, although large-scale DLE remains unproven.

- The sulfuric acid squeeze is creating winners and losers across the mining sector. Producers with domestic sulfur supply, copper smelters benefiting from higher acid byproduct values, and geographically diversified miners are better positioned than peers reliant on Middle Eastern sulfur.

Threats

- The Aurora uranium project highlights how water scarcity is becoming a key constraint on permitting, infrastructure development, and competition between agricultural and industrial users in arid regions. This creates potential timing risks for uranium and other critical mineral projects, even as demand for nuclear energy continues to grow.

- The buffer remains thin: the U.S. Department of Energy released 9.1 million barrels from the Strategic Petroleum Reserve (SPR) in the week ended May 22, following a record 9.9 million-barrel release the prior week. These back-to-back drawdowns could leave the U.S. more exposed if the ceasefire falters or disruptions in the Strait of Hormuz intensify.

- Europe enters the gas storage refill season with inventories 14% below the five-year average and LNG supplies still constrained. With Qatari force majeure expected to continue through mid-August, the market remains vulnerable to renewed price spikes heading into next winter, even as near-term premiums ease.

Bitcoin and Digital Assets

Strengths

- Mastercard Incorporated secured a New York State BitLicense, one of the most stringent crypto regulatory approvals in the United States, as it continues expanding its digital asset and stablecoin services. The company has partnered with more than 100 crypto and fintech firms, including Binance, Circle, PayPal, and MetaMask, to integrate blockchain-based payments with traditional financial rails. The approval strengthens the link between traditional finance and digital assets while reinforcing institutional confidence in regulated crypto infrastructure.

- Tether Holdings Limited said supply of its regulated stablecoin USA₮ grew nearly 540% month-over-month (MoM), rising from about 22 million tokens in March to more than 140 million in April. USA₮ was launched to align with proposed U.S. stablecoin regulations under the GENIUS Act and is issued by Anchorage Digital Bank, the first federally chartered crypto-native bank in the United States. The rapid growth highlights rising demand for regulated digital dollars and reinforces the expanding role of stablecoins within the traditional financial system.

- The Bank for International Settlements (BIS) said its Project Agorá initiative successfully demonstrated how tokenization and blockchain technology could make wholesale cross-border payments faster, more efficient, and less exposed to settlement risk. The project includes seven major central banks, including the Federal Reserve Bank of New York, Bank of England, and Bank of Japan, alongside more than 40 financial institutions. The initiative highlights growing institutional confidence in blockchain-based financial infrastructure and reinforces the expanding role of tokenization in the global financial system.

Weaknesses

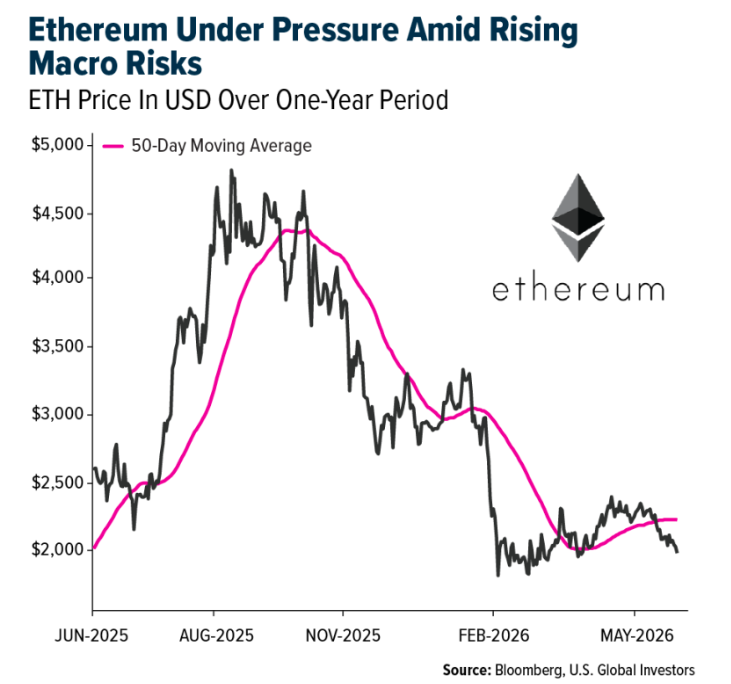

- BlackRock, Inc. saw its spot Bitcoin ETF, the iShares Bitcoin Trust (IBIT), record nearly US$528 million in outflows on Wednesday, marking the fund’s second-largest daily withdrawal since launch. The selloff contributed to an eight-day streak of net outflows across U.S. spot Bitcoin ETFs, totaling roughly US$2.6 billion, as Bitcoin fell below US$75,000. The sustained withdrawals highlight weakening institutional demand and softer investor confidence in digital assets, adding pressure to Bitcoin prices and the broader crypto market.

- Bitcoin remained under pressure and failed to recover above US$73,000 even after reports of a potential U.S.–Iran agreement boosted equities and pushed oil prices lower. The muted reaction compared to traditional markets highlights softer investor confidence and reduced momentum in crypto. At the same time, inflation concerns continue weighing on digital assets, with the Federal Reserve’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) Index, rising to 3.8%, its highest level since 2023, reinforcing expectations that higher interest rates could continue to pressure cryptocurrencies.

- Argentina introduced a bill that would prohibit banks, payment providers, and crypto firms from servicing unauthorized online gambling platforms, increasing regulatory pressure on parts of the digital asset industry. The proposal would allow authorities to block crypto-related transactions tied to unlicensed operators and impose additional compliance requirements on exchanges and payment providers. The measure highlights how rising regulation around crypto-linked betting and prediction market platforms could limit activity and create new operational challenges for parts of the crypto ecosystem.

Opportunities

- Samsung affiliates are deepening their exposure to the digital asset industry through a US$408 million investment in Dunamu, operator of Upbit, South Korea’s largest cryptocurrency exchange. Samsung Securities will acquire a 2% stake, while Samsung Card and Samsung SDS will also participate. The deal highlights growing institutional confidence in crypto infrastructure and deeper integration between traditional finance, technology, and digital assets in one of Asia’s most active crypto markets.

- VanEck launched the first U.S. spot BNB ETF on Nasdaq, expanding institutional access to digital assets beyond Bitcoin and Ethereum. BNB is the native token of BNB Chain, a blockchain network supporting decentralized applications, digital payments, and crypto transactions. The ETF allows investors to gain exposure to BNB through traditional brokerage accounts without directly holding the token, underscoring the scale of the ecosystem, which processes more than 14 million daily transactions and holds over US$16 billion in stablecoins.

- Megapot, a decentralized blockchain lottery protocol, partnered with Protocol Guild, a funding collective supporting Ethereum core developers, to launch what it describes as the crypto industry’s first programmable charity lottery. The model automatically directs 100% of referral fees from ticket sales to Ethereum developers via smart contracts, reducing reliance on traditional donations and centralized funding. The initiative comes as Protocol Guild estimates Ethereum may require US$30 million to US$60 million annually to support long-term development and scalability.

Threats

- Geopolitical tensions in the Strait of Hormuz triggered a broad, risk-off move across global markets, pushing Ether below $2,000 for the first time since March. The selloff led to nearly US$959 million in crypto liquidations, including $897 million in long positions. Ethereum open interest rose to a record 16.39 million ETH ($32.6 billion) even as prices fell, signaling growing bearish positioning and highlighting risks from rising oil prices and inflation pressures on digital assets and broader risk assets.

- Speculative capital continues rotating out of cryptocurrencies and into artificial intelligence and semiconductor equities, weakening momentum across digital assets. While Bitcoin surged more than 650% from its 2022 lows to nearly US$126,000 in 2025, attention has shifted toward AI infrastructure and memory-chip names such as Micron, which rose from a US$70 billion valuation to over US$1 trillion in a year. The trend underscores the risk that crypto markets may lag as investors pursue newer high-growth themes and mega-IPO opportunities such as SpaceX and OpenAI.

- UniCredit warned that the EU’s Markets in Crypto-Assets (MiCA) regulation could increase systemic risk by tying stablecoin reserves more closely to the banking system. MiCA requires issuers to hold reserves in bank deposits and government securities, raising exposure to bank stress events. UniCredit also pointed to limited deposit insurance in Europe versus the U.S., referencing the 2023 Silicon Valley Bank collapse, when Circle briefly lost its USDC peg after revealing US$3.3 billion in reserves at SVB.

Defense and Cybersecurity

Strengths

- Micron’s meteoric rise to a US$1 trillion valuation is being powered by an extraordinary AI-driven surge in demand for memory chips, pushing revenue, pricing, and earnings to historic highs. With supply struggling to keep up and data center buildouts accelerating, the company now sits at the center of the global AI infrastructure boom, turning what was once a cyclical industry into one of the market’s most powerful growth engines.

- Musk’s SpaceX has received a US$2.29 billion contract to build a secure satellite communications network linking military sensors, weapons systems, and command capabilities.

- Rheinmetall secured a €1.02 billion Bundeswehr order to supply more than 2,000 military transport vehicles under an existing framework agreement, with deliveries starting in the first half of 2026 and most expected to be completed by year-end.

Weaknesses

- Zscaler delivered revenue of US$850.5 million, up 25.4% year-over-year (YoY) and 8.1% quarter-over-quarter (QoQ), alongside non-GAAP EPS of US$1.08, up 28.6% YoY and 4.9% QoQ, both beating consensus estimates of US$835.7 million and US$1.01. Despite the double beat, the stock fell sharply due to soft fiscal fourth-quarter revenue guidance of US$875 million to US$878 million and compressed full-year free cash flow margins of 23% driven by rising data center capital expenditures.

- Following the collapse of diplomatic talks, the U.S. has imposed new sanctions on Iran’s oil, shipping, and banking networks in late May 2026. The measures significantly increase Middle East instability, raising risks of supply chain disruptions and energy price shocks for global markets.

- A Russian drone struck a residential high-rise building in Galați, Romania, during an overnight attack targeting Ukrainian ports. Two civilians were injured, prompting Bucharest to condemn the incident as a severe escalation.

Opportunities

- Pennsylvania Senators McCormick and Fetterman have introduced a bill requiring the U.S. Department of Defense to develop a comprehensive, all-domain drone warfare strategy.

- Palantir and Dell Technologies have partnered to deliver a secure on-premises AI operating system for regulated enterprises. The solution targets defense, healthcare, and banking customers, integrating Palantir’s data and AI platform with Dell’s infrastructure.

- Nvidia announced plans to invest $150 billion annually in Taiwan, including a new local headquarters and expanded partnerships with TSMC and Foxconn, underscoring Taiwan’s role as an AI manufacturing hub.

Threats

- Belarus said Ukraine attempted to attack its border about 116 times over the past week. Russia also launched one of its largest-scale strikes on Kyiv this weekend, using the Oreshnik missile, with impacts largely on civilian buildings and homes.

- The U.S. military’s key weapons systems’ stockpiles are significantly depleted due to the Iran war, with a replenishment timeframe of at least three years. This creates a strategic vulnerability despite increased defense spending proposals.

- Chinese chipmaker CXMT is rapidly scaling mass production of DDR5 DRAM ahead of a potential IPO, aiming to compete with Micron, Samsung, and SK Hynix. However, the company faces significant geopolitical headwinds, including U.S. export controls and sanctions that could constrain long-term production.

Gold Market

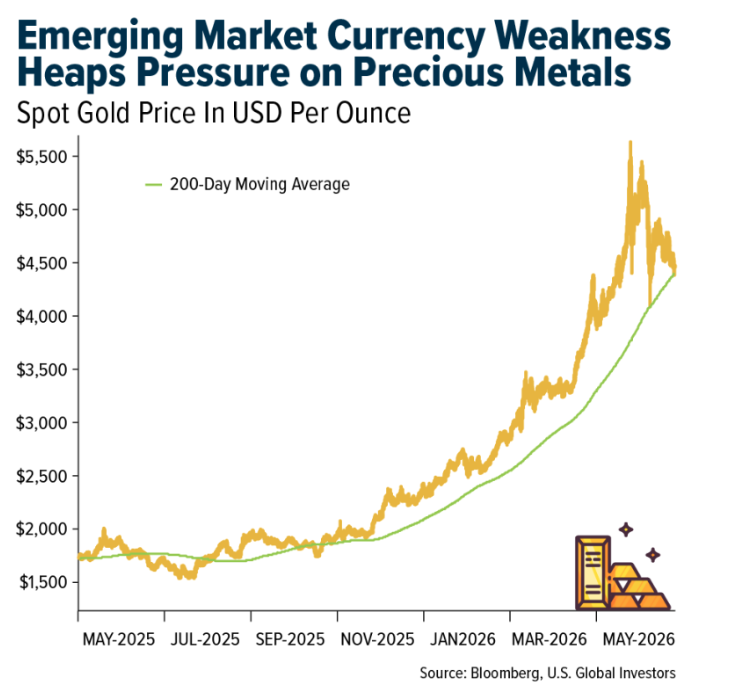

This week gold futures closed the week at $4,576.70, up $20.30 per ounce, or 0.45%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.97 The S&P/TSX Venture Index came in up 3.91%. The U.S. Trade-Weighted Dollar fell 0.35%.

Strengths

- The best-performing precious metal for the week was gold, up 0.45%, while the yield on the 2-year note fell 11.2 basis points (bps) for the week amid cooling geopolitical tensions. The Silver Institute’s 2026 World Silver Survey showed that global supply rose 7% and demand fell 2% year-over-year (YoY) in 2025. The increase in supply was driven mainly by a 3% YoY rise in mine production and a 2% YoY increase in recycling. Despite higher production, structural tightness persists, marked by the fifth consecutive year of market deficit and potential upside from growing solar demand amid higher hydrocarbon fuel costs.

- Ghana’s central bank said it plans to increase gold purchases from large-scale domestic producers to 30% of output from 20%, starting June 1. The Bank of Ghana, which currently buys 20% of refined gold from mining firms in cedis for its reserves, has finalized plans to raise that share to 30% of doré (unrefined) gold, according to Paul Bleboo, head of gold management at the regulator.

- China’s Guangzhou Futures Exchange (GFEX) is exploring the launch of night trading, primarily for platinum and palladium contracts, in response to trader feedback, according to people familiar with the matter. The exchange is studying the feasibility of overnight sessions to better capture international price movements, according to Bloomberg.

Weaknesses

- The worst-performing precious metal for the week was platinum, down 0.58%, with silver down 0.49% and palladium off 0.26%. Uzbekistan, one of the world’s largest gold producers, resumed full-scale gold exports in April after a six-month pause. The country exported about US$1.5 billion of non-monetary gold in the first four months of the year, according to the National Statistics Committee, with most shipments occurring in April.

- Early in the week, gold fell as military strikes in the Persian Gulf reduced hopes for a U.S.–Iran peace deal and reinforced concerns that persistent inflation could keep interest rates higher for longer. U.S. and Iranian forces clashed near the Strait of Hormuz overnight, underscoring ongoing tensions even as both sides signaled progress toward an interim agreement, according to Bloomberg.

- Spot gold is approaching a potential daily close below its 200-day moving average for the first time since October 2023, with traders not expecting a quick rebound. Downward pressure is being driven in part by emerging market central banks drawing down reserves to defend currencies against a strong U.S. dollar. Indian authorities have also tightened gold import rules to support the rupee amid Middle East tensions, although reports of a potential 60-day cease-fire later in the week helped ease credit market stress and reduce pressure on gold.

Opportunities

- According to Scotia, in Nunavut for Agnico Eagle, current focus includes: (1) permitting mine life extension (2031–2036), including testing the waterline for saline water discharge; (2) progressing the mill expansion; and (3) exploration drilling to extend mine life. At Hope Bay, near-term priorities include: (1) site readiness for construction and planning for the 2026 sealift season; (2) workforce expansion; and (3) continued exploration drilling to extend mine life.

- With Q1/26 earnings season complete, share buybacks continue to stand out as a key use of strong free cash flow, with senior producers repurchasing US$3.1 billion to date versus US$5.1 billion in all of 2025. Canaccord notes that intermediate producers have also accelerated buybacks, repurchasing US$921 million year-to-date, already exceeding last year’s US$821 million.

- Sunshine Silver Mining & Refining Co. is seeking to raise as much as US$330 million in a U.S. initial public offering (IPO) to help restart a mine in Idaho that previously produced silver, antimony, and other minerals. The company is marketing 20 million shares at US$13.50 to US$16.50 to fund development, purchase mining equipment, and cover drilling costs at the Sunshine mine, according to its filing with the U.S. Securities and Exchange Commission (SEC).

Threats

- Gold Fields Ltd. must present its development plans to Ghana’s Minerals Commission to renew the leases for its Tarkwa mine, according to Reuters, citing regulator Chief Executive Officer Isaac Tandoh. Any decision on renewal will follow a ministerial-level presentation.

- Silver’s recent resilience contrasts with a downtrend in investor positioning, leaving the metal vulnerable to a pullback. The metal has been hovering around US$75 per ounce for several weeks, reflecting cautious optimism that prior speculative momentum could return if the U.S. reaches a peace deal with Iran, according to Bloomberg.

- As silver prices rose sharply, solar PV manufacturers faced significant margin pressure, prompting efforts to reduce silver usage in industrial applications. Lower demand could reduce the silver deficit by as much as 90% this year, with even modest investor selling potentially flipping the market into surplus. While a gold rally could push silver above $100 per ounce in the coming months, Bank of America does not expect silver to sustainably outperform due to weakening fundamental demand.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2026):

Ryanair Holdings

Singapore Airlines

Boeing

American Airlines

Delta Air Lines

Air China

China Southern Airlines Co Ltd.

Micron Technology

Zscaler Inc.

Palantir Technologies Inc.

NVIDIA Corp.

Micron

Compagnie Financière Richemont

Marriot

Ferrari

Zalando

Agnico Eagle Mines

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The Personal Consumption Expenditures (PCE) Index is a U.S. inflation measure that tracks changes in the prices of goods and services consumed by households and is the Federal Reserve’s preferred gauge of inflation.

The PHLX Semiconductor Sector Index (SOX) is a widely followed benchmark index that measures the performance of 30 top U.S.-listed companies engaged in the design, distribution, manufacture, and sale of semiconductors.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting our prospectus page or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All