Monthly Market Update

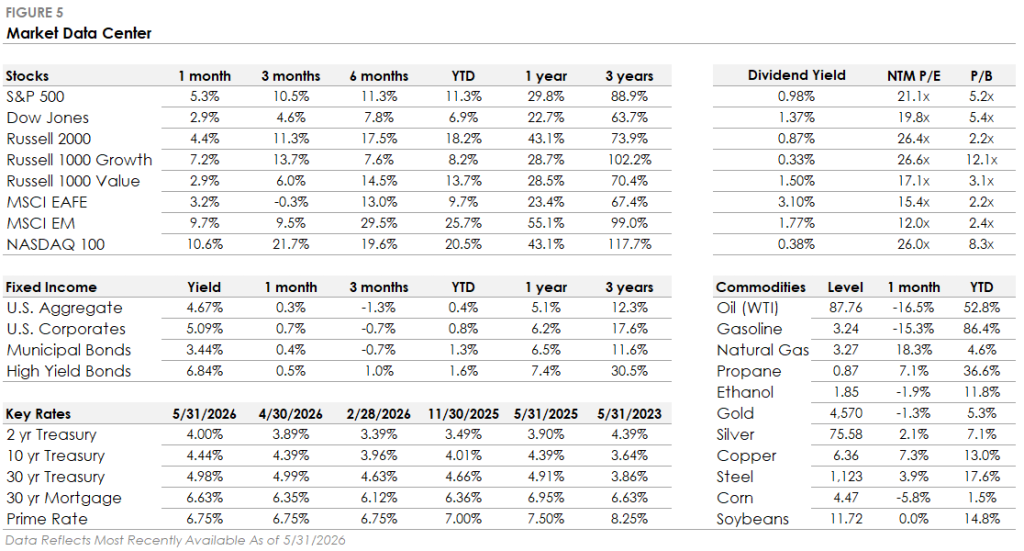

- S&P 500 gained 5.3% in May and set multiple new all-time highs. Technology led by a wide margin, gaining 16.0%, followed by Consumer Discretionary (up 2.6%) and Health Care (up 2.5%). Eight of eleven sectors declined, led by Energy (down 5.6%), Utilities (down 5.1%), and Consumer Staples (down 3.2%).

- Bonds rose modestly despite a spike in yields. The U.S. Bond Aggregate returned 0.3%, with investment-grade corporates gaining 0.7% and high-yield returning 0.5%. Mid-month, the 30-year Treasury yield spiked above 5% (last seen in 2007) and the 10-year set a new 52-week high before partially retracing.

- International stocks were mixed. Emerging markets gained 9.7%, outpacing the S&P 500 for the second consecutive month. Developed markets rose 3.2% and lagged both EM and U.S. equities.

- The Fed narrative reversed sharply. Back-to-back hot CPI and PPI reports pushed markets to price in a greater than 50% probability of a Fed rate hike at the December 2026 meeting, a significant shift from earlier this year when the consensus assumed a path of rate cuts.

- Oil prices fell. West Texas Intermediate crude ended the month below $90 per barrel, declining 16.5% in May as U.S.-Iran negotiations progressed. The Strait of Hormuz remains closed, however, and a full reopening of shipping traffic would take months even under a successful deal.

The Index Hit New Highs. Most Stocks Didn’t.

May’s headline number was the leading story as the S&P 500 gained 5.3% and set multiple record closes. However, what happened below the surface in the index is the most interesting story. Eight of eleven sectors finished the month lower, and ten of eleven underperformed the overall index. Growth stocks jumped 7.2% for the month, value continued to lag and increased just 2.9%. Bottom line: the performance gap was stark.

Read more:

Within the growth stock rally technology’s 16% gain was the story. The AI infrastructure buildout, which has been building throughout 2026, is now showing up directly in corporate earnings (Returns are being earned, as we discussed in our 2026 Outlook). Forecasted capital spending across the leading technology companies will exceed $600 billion this year, the majority directed at AI infrastructure: data centers, semiconductors, power generation, and networking equipment. That spending is converting into revenue and profit growth for the companies closest to the build, which explains why tech’s outperformance isn’t just sentiment or momentum. There are real earnings behind it. Supply chain bottlenecks are creating additional pricing power for companies in constrained parts of the technology stack, and rapid product repurposing for AI is accelerating revenue at companies that had been growing modestly just two years ago.

For investors in diversified portfolios, May reinforced something familiar: concentration risk cuts both ways. When tech leads, it leads hard, and anything without meaningful tech exposure lags significantly. In our view, the AI capex cycle still has years to run, and the earnings momentum in infrastructure is real. But a rally where one sector does all the work and eight sectors decline is not a market in full health, and that unevenness matters for how portfolios are constructed.

The Fed Narrative Flipped

For most of 2026, the baseline assumption was that the Fed’s next move would be a rate cut. That assumption is now gone on the back of hot inflation reports, CPI and PPI, which all showed that price pressures have not subsided to a degree that gives the Fed room to ease. The 30-year Treasury yield spiked above 5% mid-month, reaching levels last seen in 2007, and the 10-year set a new 52-week high. By month-end, futures markets were pricing a greater than 50% probability of a rate hike at the December meeting.

Part of the inflation persistence traces directly to the Middle East. The Strait of Hormuz has been effectively closed since the war began in late February, and the resulting supply disruption has kept upward pressure on energy prices even as oil itself fell in May. WTI dropped 16.5% on news that U.S.-Iran negotiations were making progress, but progress is not resolution. The Strait remains closed, and even a deal would take months before shipping volumes return to pre-conflict levels (See our commentary – Leads, Lags and the 4:10 to Yuma).

In the meantime, oil-driven inflation is keeping the (new) Fed in an uncomfortable position: it can’t cut rates while inflation is re-accelerating, and it has limited appetite to raise them aggressively into what is still a functioning economy. A Fed that was expected to cut three or four times this year is now being priced as possibly hiking once. That’s not a small shift, and it has implications for everything from equity valuations to refinancing costs to the housing market. We think this matters more for portfolio positioning than the equity market is currently acknowledging.

What Matters Now

Three things worth holding onto heading into June.

- First, the AI earnings story is becoming verifiable, not just speculative. When $600 billion in annual capex starts flowing through earnings reports in a visible way, that changes the risk profile of the theme. It’s not a bet on a future that might not arrive; it’s a reflection of investment that’s already committed.

- Second, the Fed flip matters. Interest rate expectations shape valuations, bond yields, and sector rotation in ways that take months to fully work through. If rates stay higher for longer or actually rise, the math changes for rate-sensitive parts of the market: utilities, real estate, long-duration growth stocks.

- Third, the Middle East negotiation path is worth watching closely. A genuine reopening of the Strait would relieve oil price pressure, remove a meaningful source of inflation persistence, and potentially give the Fed back the optionality it lost this spring.

For investors carrying significant fixed income exposure, the current environment is a reminder that bonds can generate real income while also being subject to price risk when rates move. For “conservative” investors, that can mean portfolios that move down in value more than expected. Make sure portfolio risks are truly understood, especially when it comes to fixed income and duration (interest rate) exposures.

If you want to talk through how this environment affects your specific allocation, we’re happy to do that.

Please read important disclosures here.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Defiant Capital Group

Read more commentaries by Defiant Capital Group