With the recent increase in the federal unified gift and estate tax exclusion amount of up to $15 million per person (indexed for inflation), the overwhelming majority of households will not have to plan for federal estate taxes. However, taxes on estates at the state level are still an important factor for many. Careful consideration must be given to efficiently transfer wealth to heirs given the differences between the federal transfer tax system and certain state rules. Currently, 12 states and the District of Columbia tax estates, while five states tax inheritances. Maryland is the only state that imposes both. Also, the only state that taxes lifetime gifts is Connecticut. Note that, like the federal system, property left to surviving spouses or charities is not subject to state transfer taxes.

How Do State Transfer Taxes Differ?

- Tax applied at much lower wealth thresholds

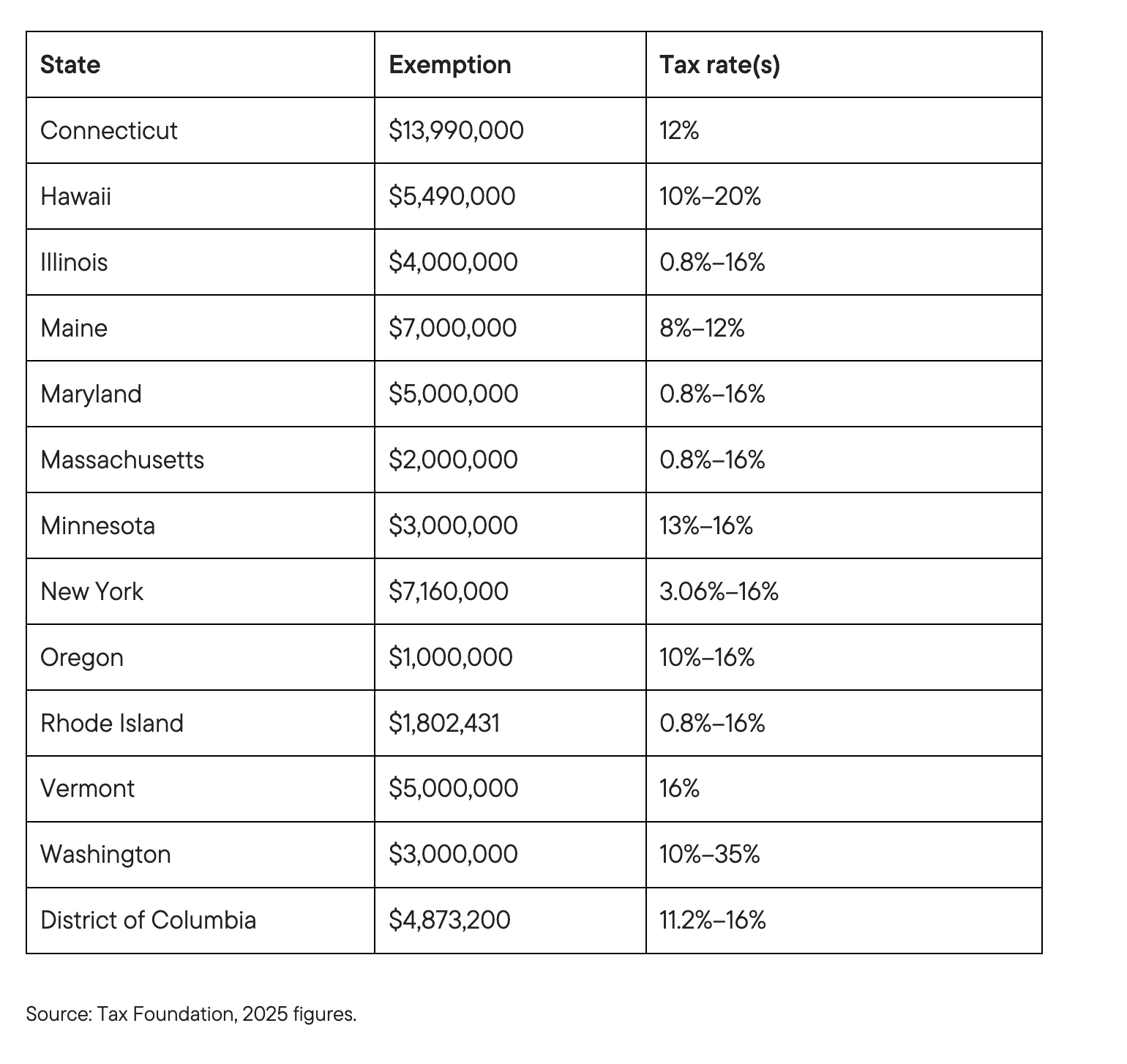

The level of wealth upon which estate taxes apply at the state level may be significantly lower than the federal threshold of $15 million. For example, Oregon taxes estates over $1 million, Rhode Island taxes estates over $1,802,431 and Massachusetts taxes estates over $2 million. Here’s a look at estate tax exemptions by state, including the tax rate(s):

- Most states don’t allow portability between spouses

The federal system allows transfer of the unused portion of the lifetime gift exemption from the first deceased spouse to the surviving spouse. This is known as the portability provision. At the death of the first spouse, a federal estate tax return (IRS Form 706) must be filed to claim the deceased spouse’s unused exemption (DSUE). For example, a surviving spouse may benefit from their own $15 million exemption plus their deceased spouse’s $15 million exemption, if that spouse did not make any lifetime gifts that would have reduced their unified gift and estate tax exemption. Only two states (MD and HI) allow portability under state tax systems.

- Beware the “cliff” effect

While most states apply tax on just the amount of the estate above the exemption threshold, there are a couple of states (IL, NY) that will essentially tax the entire estate if the value of the estate at death exceeds the exemption. For example, consider a taxable estate valued at $5.1 million within a state where the exemption threshold is $5 million. Under federal rules, and most states, the amount of the estate subject to tax would only be the amount exceeding the exemption ($100,000 in this example). However, in a state with a “cliff” system, if the estate exceeds the exemption, then the entire estate is taxed, resulting in a much higher tax bill. For this reason, some estate plans for residents of these states may include a clause that triggers a charitable gift for the dollar amount that exceeds the state’s exemption threshold for estates. Make sure to consult with a qualified legal professional for guidance on specific state rules.

- Certain inheritances may be taxed

Under the federal system, heirs are not taxed on inheritances. However, five states (KY, MD, NE, NJ and PA) will tax certain heirs. Depending on the state there will be different dollar thresholds and rules that apply. Typically, the determination of the inheritance tax will depend on the relationship of the heir to the deceased. For example, closer relatives such as a child receive more preferential treatment under these state tax systems than more distant or non-relatives. For example, New Jersey classifies four types of beneficiaries, the following of whom are exempt from inheritance tax: surviving spouse, civil union partner, domestic partner, parents, grandparents, children, stepchildren, grandchildren and great-grandchildren.*

* New Jersey Department of Taxation, 2026.

Read more: Estate Plans Designed Before OBBBA May Now Be Costing Your Clients Money

Planning Considerations for State Death Taxes

- Use the exemption amount of the first deceased spouse

Since the exemption amount between spouses is not portable, planning must be considered to apply the exemption amount upon the death of the first deceased spouse. There are a variety of ways to accomplish this, including an estate plan that funds the state’s exemption amount in an irrevocable trust at the death of the first spouse. In a state like Massachusetts, which has a $2 million exemption, this may help a married couple with $4 million in combined estate avoid state death taxes. For example, a credit shelter (or bypass) trust may allow the first spouse’s state exemption amount to be fully utilized while transferring remaining assets to the surviving spouse, thereby deferring estate taxes until the second death.

- Plan for liquidity at death

For families in states that impose estate or inheritance taxes, are there liquid funds available to cover those expenses? An efficient wealth transfer plan should account for these factors to avoid liquidating assets that may result in lower sales proceeds, higher taxes, or both. Life insurance may be an effective means to create liquidity for more flexible planning.

A well-structured gift strategy may help reduce potential state transfer tax exposure by reducing the value of the estate. This may include annual gifts up to the maximum federal amount ($19,000 per recipient for 2026), and in some cases larger gifts. Be aware that states may treat larger gifts differently when calculating the value of the estate for tax purposes. For example, Illinois will include larger gifts exceeding the annual gift exclusion when calculating the value of the estate subject to tax. Other states may not include these larger gifts in their calculation, that may allow more substantial gifting later in life to significantly reduce the value of an estate. Given the complexity of these rules, we recommend consulting with a local legal professional knowledgeable about specific state statutes.

- Relocate to another state

For some, changing domicile for tax purposes may be an option. This is a common occurrence for residents of northeast states such as New York and Massachusetts who relocate to southern states such as Florida or South Carolina as retirees. Note the use of the word “domicile,” which is much different from residency for tax purposes. A person’s domicile is considered their permanent legal home base. Someone may have multiple residences but only has one domicile. Changing domicile is not as straightforward as merely spending the majority of days in that particular state. The individual must demonstrate a clear intent to leave one state and establish a permanent presence in the new state, as evidenced by a number of factors. Since the individual generally bears responsibility for proving the change in domicile, one must be prepared to document this process that should include multiple factors. This may include real estate owenership, driver’s license, automobile and other property registrations, voting registration, civic affiliations, financial accounts, club memberships, business relationships, healthcare providers and others. Note that even if you change domicile, certain property (real estate or local business interests, for example) held in your estate may be subject to taxation by your former state.

Seek Professional Guidance

Given the complexity and variation of different state tax systems, consultation with a qualified legal professional is critical. A thoughtful, well-crafted and comprehensive wealth transfer plan customized to the state’s specific rules may help improve the efficiency of wealth transfer to heirs.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Any information, statement or opinion set forth herein is general in nature, is not directed to or based on the financial situation or needs of any particular investor, and does not constitute, and should not be construed as, investment advice, forecast of future events, a guarantee of future results, or a recommendation with respect to any particular security or investment strategy or type of retirement account. Investors seeking financial advice regarding the appropriateness of investing in any securities or investment strategies should consult their financial professional.

Franklin Templeton, its affiliated companies, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties or complying with any applicable tax laws or regulations. Tax-related statements, if any, may have been written in connection with the “promotion or marketing” of the transaction(s) or matter(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

WF: 11108950

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Franklin Templeton has environmental, social and governance (ESG) capabilities; however, not all strategies or products for a strategy consider “ESG” as part of their investment process.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com. Investments are not FDIC insured; may lose value; and are not bank guaranteed.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© Franklin Templeton

More Sustainable Investing Topics >