A rough start to the year for bond traders just got worse as data showed a buoyant US labor market with few of the stresses that could prompt the Federal Reserve to lower interest rates.

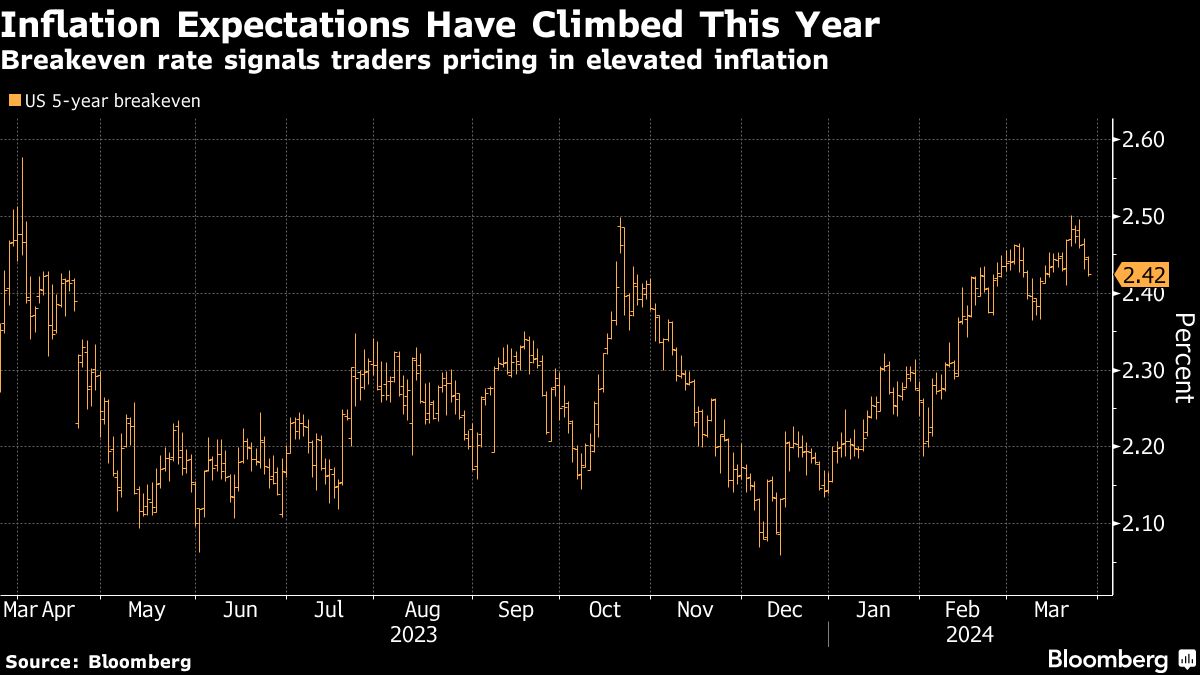

Federal Reserve Chair Jerome Powell’s increasing focus on protecting the job market is encouraging a swath of bond traders putting bets on inflation rates to remain elevated.

Bond traders are cautiously reloading wagers that burned them just weeks ago as the Federal Reserve and key global peers finally appear set to begin reducing interest rates as soon as June.

After dialing back their expectations for 2024 Federal Reserve interest-rate cuts substantially since the start of the year, bond traders on Wednesday will take their next cue when policymakers release their own updated projections for their benchmark.

This week, the US bond market faces its own Super Tuesday of sorts: the release of fresh inflation data investors will use to predict when the Federal Reserve will start cutting interest rates.

What was supposed to be the darling trade of 2024 has unraveled, thanks to the Federal Reserve upending predictions over how fast it would lower interest rates.

Investors are beginning to war-game how the Federal Reserve can manage a US economy that just won’t land, with some even debating whether interest-rate hikes will be needed only weeks after a steady run of reductions appeared all but certain.

Traders ratcheted down their expectations for a Federal Reserve’s interest-rate cut before July, and Treasury yields soared, after a report showed that inflation remains sticky in the US.

Bond traders have come more in line with the Federal Reserve’s trajectory for the upcoming easing cycle. Strategists at Citigroup Inc. say what’s missing now is traders hedging the risk of a very brief easing cycle followed by rate increases shortly thereafter.

Bond traders are finally heeding one of the market’s oldest lessons: Don’t fight the Fed.

The US government sold $25 billion of 30-year bonds at a lower-than-anticipated yield, soothing investor nerves about demand for longer-dated debt.

Treasuries are headed for their biggest two-day loss in months as strong economic data reinforced the message of Federal Reserve officials including Chair Jerome Powell that interest-rate cuts are unlikely to begin before May.

The US economy is testing bond traders’ faith that the Federal Reserve will deliver a series of interest-rate cuts this year.

Jerome Powell delivered a clear message to traders eager for the central bank to start slashing interest rates: Not so fast.

The US Treasury boosted the size of its quarterly issuance of longer-term debt for a third straight time and suggested that no more increases are likely until next year.

Trading in bonds these days means having to put up with more frequent market gyrations — and that’s just fine with big investors like Pimco and BlackRock Inc.

Wall Street is widely expecting the US Treasury to announce a final increase to its sales of long-term debt this week, after a steady ramp up in supply that’s sometimes tested buyers’ appetites for funding a widening budget deficit.

After years of regulatory tinkering, Washington is now forcing through the most rigorous overhaul of the world’s biggest bond market in decades.

Bond traders are growing convinced that US Treasury yields are on the brink of returning to the way they’ve traded for most of their existence — it’s the how, why and when of the normalization that keeps financial markets bouncing around.

Bond traders are growing more convinced that US yields are heading lower as they bet on a series of Federal Reserve interest-rate cuts, yet the path to cheaper borrowing costs is set to be extremely bumpy.

Bond traders shrugged off higher-than-anticipated inflation readings for December, pricing in a larger total amount of Federal Reserve interest-rate cuts this year beginning in May.

Right around the start of November, two words suddenly disappeared from the chatter in the bond market: debt supply.

Traders betting on a 2024 bond rally are unfazed by the recent pullback, seeing it as a chance to seize on elevated yields before the Federal Reserve starts driving down interest rates.

AlphaSimplex Group’s Kathryn Kaminski says her firm closed out a more than two-year short bet against US bonds, with its model signaling that it’s starting to become a time to buy as the market emerges from its worst rout in decades.

All across Wall Street, on equities desks and bond desks, at giant firms and niche outfits, the mood was glum. It was the end of 2022 and everyone, it seemed, was game-planning for the recession they were convinced was coming.

Treasuries rallied along with global bonds, sending benchmark yields to multi-month lows, as traders bet the world is entering a new, disinflationary period by wagering on more interest-rate cuts next year.

US stock and bond prices will see modest gains as the Federal Reserve pivots to cutting interest rates next year, though the easing may not be as aggressive as markets are now expecting.

The bond market’s bold bet on US interest-rate cuts is set for its biggest test yet.

Treasury yields resumed their downward slide — with the benchmark 10-year note’s falling to the lowest level since Sept. 1 — after the latest sign of labor-market cooling bolstered bets that a Federal Reserve shift to policy easing isn’t far off.

A torrid bond market rally shows traders are convinced the Federal Reserve’s rate-rising cycle is over. The debate now turns to when central bankers start cutting, and by how much.

In a year in which little has gone right in the US bond market, November turned out to be a month for the record books.

US regulators’ swift action in March to ring-fence the banking sector after the collapse of Silicon Valley Bank might have had an unintended consequence of driving cash out of bond funds, by enhancing the appeal of deposits.

The world’s biggest bond market has clawed its way back after spending chunks of 2023 underwater. Now many US debt watchers see the pathway clearing for a real revival.

The Treasury Department’s top domestic finance official said the US government debt market has functioned well during a year of outsized interest-rate volatility, a regional banking crisis and the recent hack of the world’s largest bank.

A normal day for markets became something extraordinary after a hotly anticipated report on US inflation gave traders the greenlight to declare that the Federal Reserve’s most aggressive interest-rate hiking cycle in decades is over.

It’s the buzz word on Wall Street and in the hallways of the Federal Reserve and Treasury Department. It’s blamed for triggering bond selloffs, shifts in debt auctions and interest-rate policy.

Hoisington Investment Management Co. was pummeled by its bullish stance on US bonds in recent years, driving its Treasury fund to some of the industry’s biggest losses as the Federal Reserve’s rate hikes sent prices tumbling.

A prospect that might have seemed unthinkable just a couple short weeks ago is coming into view for bond traders: The potential for US Treasuries to post an annual gain for the first time since 2020.

The selloff in US debt appears close to being over as the Federal Reserve nears winding up its most aggressive rate hikes in a generation.

The US Treasury increased its planned sales of longer-term securities by slightly less than most major dealers expected in its quarterly debt-issuance plan, in a move that signals officials may be concerned about the surge in yields over the past several months.

The US Treasury reduced its estimate for federal borrowing for the current quarter thanks to stronger-than-expected revenues, offering some relief for investors concerned about the rapidly widening fiscal deficit.

The worst selloff of longer-term Treasuries in more than four decades is putting a spotlight on the market’s biggest missing buyer: the Federal Reserve.

On Monday, the 10-year Treasury yield climbed over 5%, a 16-year high. It’s a level few would have predicted during the long run of rock-bottom interest rates that followed the Great Financial Crisis.

Treasury-market liquidity has mostly righted itself since the dislocations caused by the several regional bank failures in March, according to a Federal Reserve Bank of New York economist.

Bond investors are coalescing around a segment of the Treasuries market that offers a measure of protection from this year’s brutal rout and also positions them for the recession that some still anticipate.

Bond investors face the crucial decision of just how much risk to take in Treasuries with 10-year yields at the highest in more than a decade and the Federal Reserve signaling it’s almost done raising rates.

The resilience of the world’s biggest bond market is top priority as US debt officials prepare to start buying back government debt, according to Josh Frost, the Treasury Department’s assistant secretary for financial markets.

Bond traders are bracing for Treasury yields to keep pushing higher after the Federal Reserve signaled it’s likely to hold interest rates at lofty levels well into next year.

US five- and 10-year yields rose to the highest levels since 2007 after hotter-than-anticipated inflation data in Canada and rising oil prices added to global concerns about resurgent price pressures.

Federal Reserve policymakers’ updated forecasts for their benchmark interest rate, due Wednesday, are looming as a key potential decider for a US Treasuries market at risk of a third straight year of losses.