Impact investing, which seeks to make a direct—and measurable—social or environmental impact while generating a financial return, has historically been synonymous with the private debt and equity markets. But that ignores the hugely important public market of municipal finance.

With profits from forced labor estimated at US$150 billion a year, some companies in global portfolios could be unwittingly associated with modern slavery. The good news: businesses and investors can help tackle the problem—individually and through collaboration.

In high yield specifically, investors tend to think about it as a risky way to play fixed income. But we like to turn that thinking on its head, actually: that you should think about it as a way to de-risk your overall portfolio rather than to re-risk your fixed-income side.

As one of the fastest-growing bond sectors, emerging-market (EM) corporate debt has become too big to ignore. With US$2.7 trillion outstanding across more than 600 companies, it’s now larger than the entire EM sovereign sector and is equal to the US-dollar and euro high-yield markets combined.

Equity investors focused on a low-carbon strategy needn’t compromise on company fundamentals. When quality and compelling valuations are equally considered, joining the global fight against climate change and generating strong return potential can work hand in glove.

The revolutionary technology of synthetic biology is poised to make a profound impact on the way a vast array of products are manufactured, from lab-grown meat to cosmetics to biodegradable packaging. Yet investors are paying relatively little attention to the huge business potential.

Inflation and rising interest rates have prompted many equity investors to reconsider technology and high-growth companies. But this inflationary environment is different, and so are the companies best poised to rise above it.

One advisor whom I coach uses a color-coded checklist with every client to track which areas of a financial plan have been completed and which tasks are pending. It’s a brilliant way to shift a client’s attention from portfolio performance to the larger, more important elements that make up a holistic financial plan.

It’s not uncommon for stakeholders in large organizations to have different views on the meaning of ESG and the importance of its pillars in defining organizational success. That’s understandable, and in fact, diverse perspectives can be a source of strength when making investment decisions.

After years of anxiously watching for inflation, it’s here. Unfortunately, what many expected to be a short, COVID-19-induced visit has turned into an extended stay, thanks to robust demand and a snarled supply chain. The question now is does the supply chain pose a threat to our economic outlook?

Investors are sitting on a mountain of cash as household reserves now stand four times higher than pre-COVID-19 levels, while money market reserves rose to all-time highs. However, a trifecta of concerns from rising interest rates, persistent inflation, and an evolving US tax picture are making investors reluctant to deploy that cash.

Renewed impetus behind China’s goal of “common prosperity” has raised concerns that Beijing plans a redistribution of wealth that could hurt growth and investment. The reality, however, is more nuanced—and a good deal more positive for China’s long-term growth ambitions.

Soaring energy prices highlight the challenges of shifting toward renewable power sources. The continuing need for oil and gas during the transitional phase raises complex questions about balancing environmental needs and social concerns on the journey to a net-zero world.

Inflationary pressures are threatening corporate profitability. As third-quarter earnings season winds down, we’re gathering intelligence to identify companies that will have advantages sustaining quality earnings and margins amid rising prices.

When rates are rising, investors need portfolio protection. But it’s no time to sit idly in cash and wait things out. Every day spent on the sidelines means income and opportunities lost. A passive, set-it-and-forget-it investing approach isn’t ideal either. Buy-and-hold laddered portfolios tend to lock in low yields that disappoint if the market begins to offer more.

Investing is about to get a lot harder, with thinner return streams and potential pitfalls from inflation, rising rates and market volatility dominating the landscape. In our view, the solution is to build a portfolio that has better up/down capture. Getting that balance right is the challenge for every investor—and requires three main elements: better beta, efficient structure and targeted alpha. Each element can create a favorable return sequence and be even more powerful in combination.Download AB’s guide to get our views on how to design a portfolio around these elements in the post-pandemic environment.

When I look at the opportunity, it’s all about how well corporate America has done in terms of increasing profit margins. We’re at record levels now, so the revenues have come back, but all the costs haven’t come back. And that means tremendous earnings growth. That’s the positive.

After decades of saving for a comfortable retirement, plan participants eventually face the question of how to create an income stream from those savings. Most aren’t sure how to do that, even though income is the main reason they’re saving in the first place...

Well, on the surface, it's been a very solid year for the second year in a row. But under the surface, it's been unusually volatile.

When the history of COVID-19 is written, the pandemic period will be seen as more than just a health and economic crisis. Both contributed to a social reckoning, with a growing focus on inequality around the world, while the intensifying global climate crisis has added new and unpredictable threats.

The shift to electric vehicles means major changes across the supply chain and involves multiple ESG challenges. As the auto industry strives to institute sustainable practices, investors need to engage with governments and corporates to encourage and accelerate the process of change.

Interest rates are rising, and bond investors are worried about the potential impact on their portfolios. But they’re not entirely at the mercy of the markets.

Concerns about China’s slowing economy have focused on issues affecting property and manufacturing. But these are only part of the story. Investors seeking a fuller understanding of the risks and opportunities need to take a broader perspective.

The strong economic and market trends of the first half of 2021 wavered during the third quarter. The coronavirus delta variant caught up with the US at the height of the summer, just as vaccinations slowed and concerns grew that inflation might flare and persist.

In business as in life, a healthy sense of self-awareness is often the first step to meaningful change. Companies that are conscious of their flaws and eager to address the root problems offer a source of solid return potential for equity investors who identify the turnaround stories early.

Inflationary pressures are mounting, based on evidence from the recent earnings season. The question for investors is, which companies can pass on those costs to help protect profit margins?

The US high-yield market has staged a strong comeback since its downturn at the onset of the COVID-19 pandemic and—despite historically tight spreads—fundamentals for credit continue to improve. Along with a strong global economic recovery, credit spreads are getting positive tailwinds from declining default expectations, falling levels of distressed debt, and improving access to capital.

The US Federal Reserve will soon slow its open market purchases of fixed-income securities. These purchases have served to keep rates low and liquidity flowing, but as the post-pandemic economy heals, it’s time for the Fed to taper. As they step back from buying, who is going to step forward?

Executive pay is a powerful motivating factor. But investors need to consider whether executive pay incentives are fully aligned with the goals of the business. We find that companies with meaningful ESG goals embedded in their executive compensation schemes tend to have a better understanding of the ESG factors that are material to their business, use specific key performance indicators (KPIs) and are more likely to achieve them.

With COVID-19 still a top employer concern, protecting workers’ health and well-being naturally comes first. But the pandemic’s impact isn’t limited to only physical and mental health: financial wellness is also ailing. The crisis has exacerbated the problem, but it’s not exactly a sudden occurrence.

In December, the European Central Bank (ECB) is likely to announce the retirement of its Pandemic Emergency Purchase Programme (PEPP) next March. But how will the central bank manage this process? And what will this mean for euro-area bond yields?

One of the most crucial components of investing in commercial mortgage-backed securities (CMBS) is assessing the underlying collateral value. But what if investors are disregarding risks that threaten a property’s very existence?

Major central banks are exploring digital currencies, which seem likely to become a mainstay of tomorrow’s economy. As policymakers wrestle with the many moving parts of digital dollars, euros and yuan, their decisions will shape the next dimension in national currency—and could reshuffle international currency leadership.

COVID-19 has increased inequality and aggravated social problems across emerging market economies, fueling populist pressures—but several emerging countries share features that make them particularly vulnerable. Assessing key environmental, social and governance (ESG) metrics can help identify potential pressure points.

Disruptions and dislocations associated with COVID-19 mean current economic data may not be a reliable guide to the future. But by turning to the past, we find compelling evidence that inflation regime change is accelerating.

A single-minded approach to price stability is under threat as policymakers start to focus on what are—arguably—more pressing concerns.

Defensive stocks are often misunderstood. In recent years, even when they have delivered strong and steady earnings, returns have disappointed.

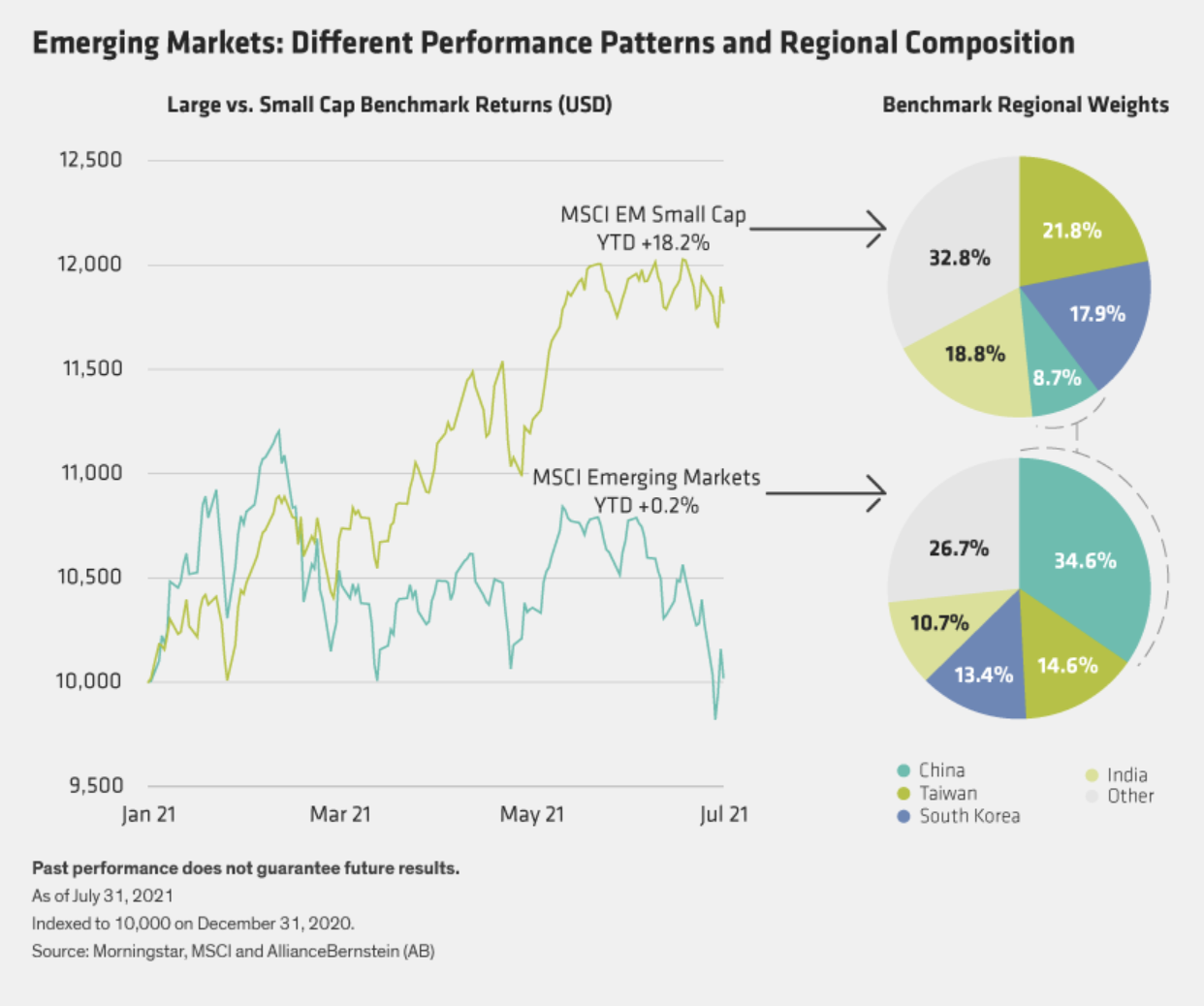

Emerging-market (EM) stocks have hit a rough patch, but shares of smaller companies have held up well.

Much of the volatility that has recently shaken China’s credit markets has been associated with government interventions.

What You Need to KnowMunicipal bonds are the cornerstone of many portfolios, but efficiently navigating today’s complex, fragmented and ever-changing muni market can be overwhelming. Unfortunately, many managers research, evaluate and trade municipal bonds like it’s 1995, missing out on opportunities because they can’t find them in the chaos. The right technology can change that.

Technology is advancing at a rapid pace, exerting downward pressure on prices

Many investors, perhaps scarred by 2013’s “taper tantrum,” are focused on the likelihood that the Federal Reserve will start reducing its bond purchases in the next few months.

Today’s complex, fragmented, fast-moving muni market is rapidly outpacing the capability and capacity of traditional portfolio-construction methods.

As equity style winds shift, investors are still debating the merits of growth versus value stocks.

What we’ve seen this year is an exceptionally high rate of earnings growth across markets, but that’s not going to persist.

As the summer progresses, US vacationers are out in force while the European and Asian holiday scene remains relatively subdued.

Central banks are being forced to address many challenges—inequality, climate change, and debt management to name but three.

There’s considerable uncertainty in today’s municipal market. Questions persist about the likelihood of rising interest rates, inflation that may not be transitory and the impact on municipalities once the benefits of fiscal stimulus fades. Active bond managers have many decisions to make and need to be nimble in a changing landscape. What’s next for municipal bonds, and how can trading and portfolio management technology help investors navigate this changing environment?

Inflation has been on the rise recently, raising concerns about long-run inflation and its impact on the spending power of those who can least afford it—investors approaching or already in retirement.

China’s regulatory crackdown on education and tech companies led early this week to a dramatic sell-off that started in Chinese stocks and extended into offshore Chinese currency and credit markets.